🇺🇸 FOMC CHEAT SHEET: April 29, 2026

Powell’s Final Stand. No Dot Plot. No Safety Net.

This newsletter is for educational purposes only and does not constitute financial advice. Trading financial markets involves a high degree of risk and may not be suitable for all investors. You are solely responsible for your own investment decisions.

Why This One Is Different

Three things separate tonight from any FOMC we’ve covered.

It’s almost certainly Powell’s last press conference as Chair. His term expires May 15. He may stay on as a regular voting Governor through 2028, but the gavel passes either way.

There’s no SEP. No dot plot. April is not a projections meeting. We get a statement, a vote tally, and a press conference. Every word in the statement carries more weight tonight because there are no fresh forecasts to argue over.

The Warsh handover is now scheduled, not theoretical. The Senate Banking Committee voted 13–11 along party lines this morning to advance Kevin Warsh, after Tillis dropped his block over the weekend when the Powell investigation was closed. Warsh is on track for full Senate confirmation in time for the June FOMC.

⏰ The Timeline (UK / ET)

15:00 BST · 10:00 AM ET — Senate Banking Committee voted 13–11 to advance Warsh ✅

19:00 BST · 2:00 PM ET — 👨💻 FOMC statement drops

19:30 BST · 2:30 PM ET — 🎙️ Powell press conference (likely his final as Chair)

21:00 BST · 4:00 PM ET — 📝 Debrief Community Post on Discord Ships

13:30 BST 30 APR · 8:30 AM ET — Q1 GDP advance + March PCE (day +1)

Volatility usually arrives in two waves: the algo read at 19:00 BST, then the human read at 19:30 BST. Tonight the second wave matters more because there’s no SEP for the algos to chew on.

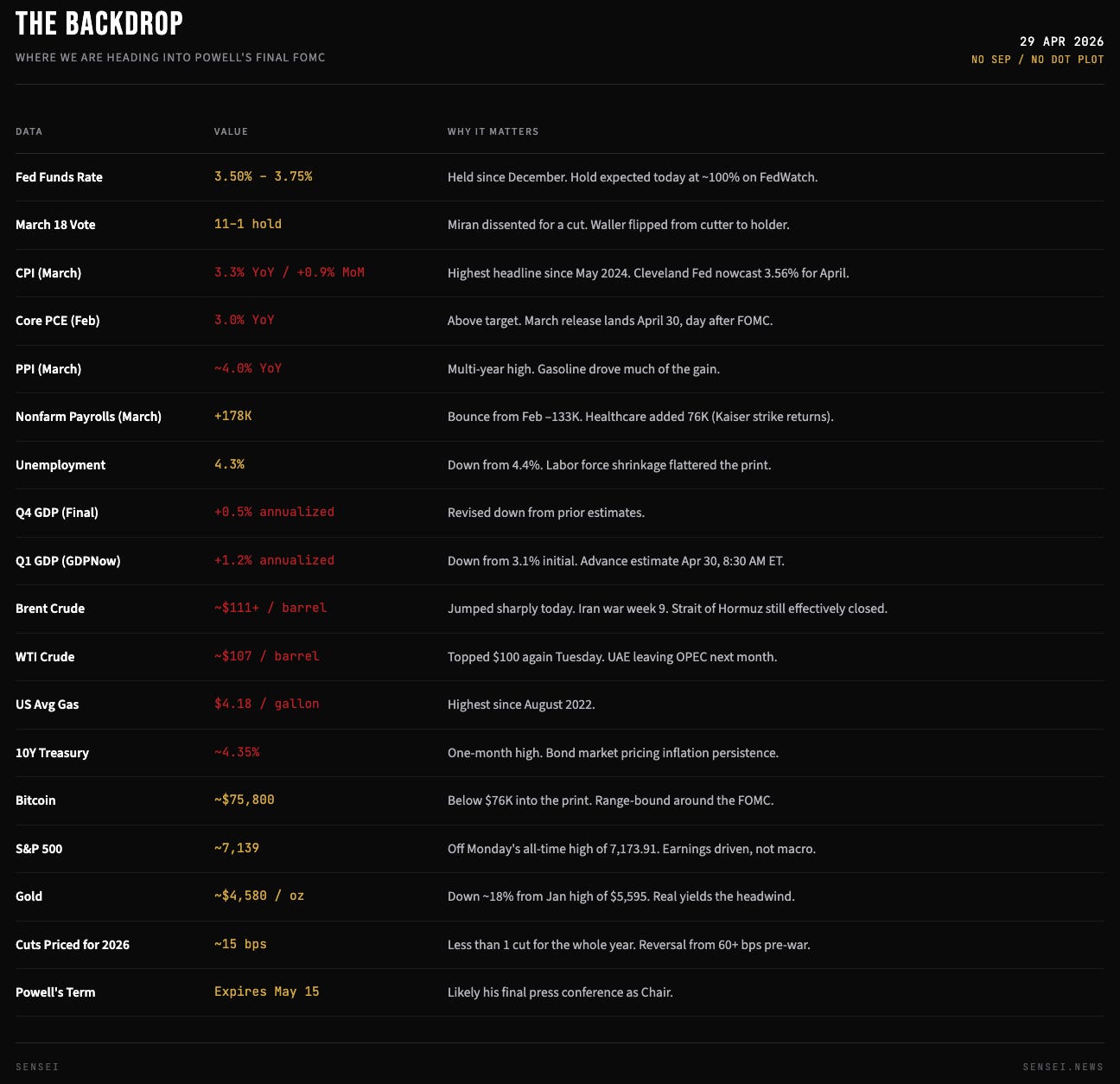

The Backdrop

Inflation hot. Growth soft. Oil on fire. Fed stuck.

PPI near 4% YoY. CPI at 3.3% YoY in March, the highest since May 2024. The Cleveland Fed nowcast has April CPI jumping again, to 3.56%. Core PCE (Feb) at 3.0%, running 100 bps over target. US gas at $4.18 a gallon, the highest since August 2022. Less than one cut priced for 2026, a complete reversal from the three-plus cuts the market had penciled in pre-war.

Underneath the headlines: Q4 GDP printed 0.5%. The Atlanta Fed Q1 nowcast is 1.2%. February payrolls were –133K. March bounced to +178K but most of that was healthcare workers returning from the Kaiser strike. The Dallas Fed thinks the breakeven payroll number is now near zero because of immigration declines.

That tension is the whole story.

🛢️ The Oil Picture (And Why It’s Bigger Today)

WTI at $107. Brent above $111. Both jumped sharply today on Trump rejecting Iran’s latest Hormuz proposal Tuesday and the UAE announcing it’s leaving OPEC next month. We’re now in week 9 of effective Hormuz closure, around 20% of global oil supply still off the table.

Every $10 move in oil maps to roughly +0.4% on inflation and –0.15% on GDP. The April CPI nowcast at 3.56% already prices in a chunk of this. If Brent stays bid above $110 through Q2, the next two prints get worse, not better.

Powell’s framework on supply shocks is to look through them. Prices rise once, growth absorbs the hit, the Fed doesn’t have to react. That works for a one-off. It breaks when the shocks stack: tariffs in goods, oil in energy, Hormuz closed, OPEC fragmenting. In March he tied elevated inflation readings to tariffs and committed to keeping inflation expectations anchored. The implicit warning was that you can’t keep calling stacked shocks transitory forever, at some point they stop looking like shocks and start looking like a regime.

Tonight is the test of whether he extends that thinking from tariffs to oil. Six weeks ago the war was three weeks old, easy to dismiss. Now we’re nine weeks in and oil just jumped again. If he holds the transitory line, that’s calming for risk. If he layers oil onto March’s tariff warning, that’s the 1970s playbook creeping into the language.

⚠️ A Word on Stagflation

Powell hates the term. In March he said he’d reserve it for “a much more serious set of circumstances.” Most of the audience will hear him reject it again tonight and assume the situation is fine. It isn’t.

Stagflation, in plain English, is three things at once:

Slowing or stagnant growth

Persistently elevated inflation

Rising unemployment

What makes it so bad is that the Fed’s tools point in opposite directions. To support growth and jobs, you cut. To fight inflation, you hike. You can’t do both, so policy gets stuck. The 1970s is the textbook case because oil shocks kept prices high while growth weakened.

What we have right now isn’t textbook stagflation. Growth is slow, not contracting (Q4 GDP +0.5%, Q1 nowcast +1.2%). Inflation is elevated, not runaway (CPI 3.3%, core PCE 3.0%). Unemployment is rising, not surging (4.3%). We’re in milder territory than the 70s on all three counts. Powell is technically correct to refuse the word.

But the trajectory is what should worry you. Growth is decelerating (3.1% nowcast → 1.2%). Inflation is accelerating (3.3% headline → 3.56% April nowcast). Breakeven payrolls have collapsed to near zero. It doesn’t qualify as the 70s in scale, but it’s the same shape of problem Powell would have to address, and the same problem his successor will inherit. The word he uses tonight matters less than whether he describes the combination openly.

🔥 The 5 Things That Matter Tonight

1. Does “somewhat” survive in the inflation sentence? March said “Inflation remains somewhat elevated.” If “somewhat” gets dropped, that one-word change tells us the Fed is no longer confident the inflation overshoot is contained. Watch this first.

2. Does the forward guidance still say “additional adjustments”? That phrase implies the next move is down. If it changes to anything two-way, hike optionality is officially live. Single most important sentence in the statement.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.