Morning Forecast: Friday 10 July

The biggest foreign listing in US history hits the Nasdaq today, Meta moves to build its own AI chip, and Delta beats to open earnings season.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

📈 AI lifts Wall Street higher: The Nasdaq closed at a record 26,206.89, up 1.3%, as chip names ran hot and traders shrugged off fresh Iran headlines.

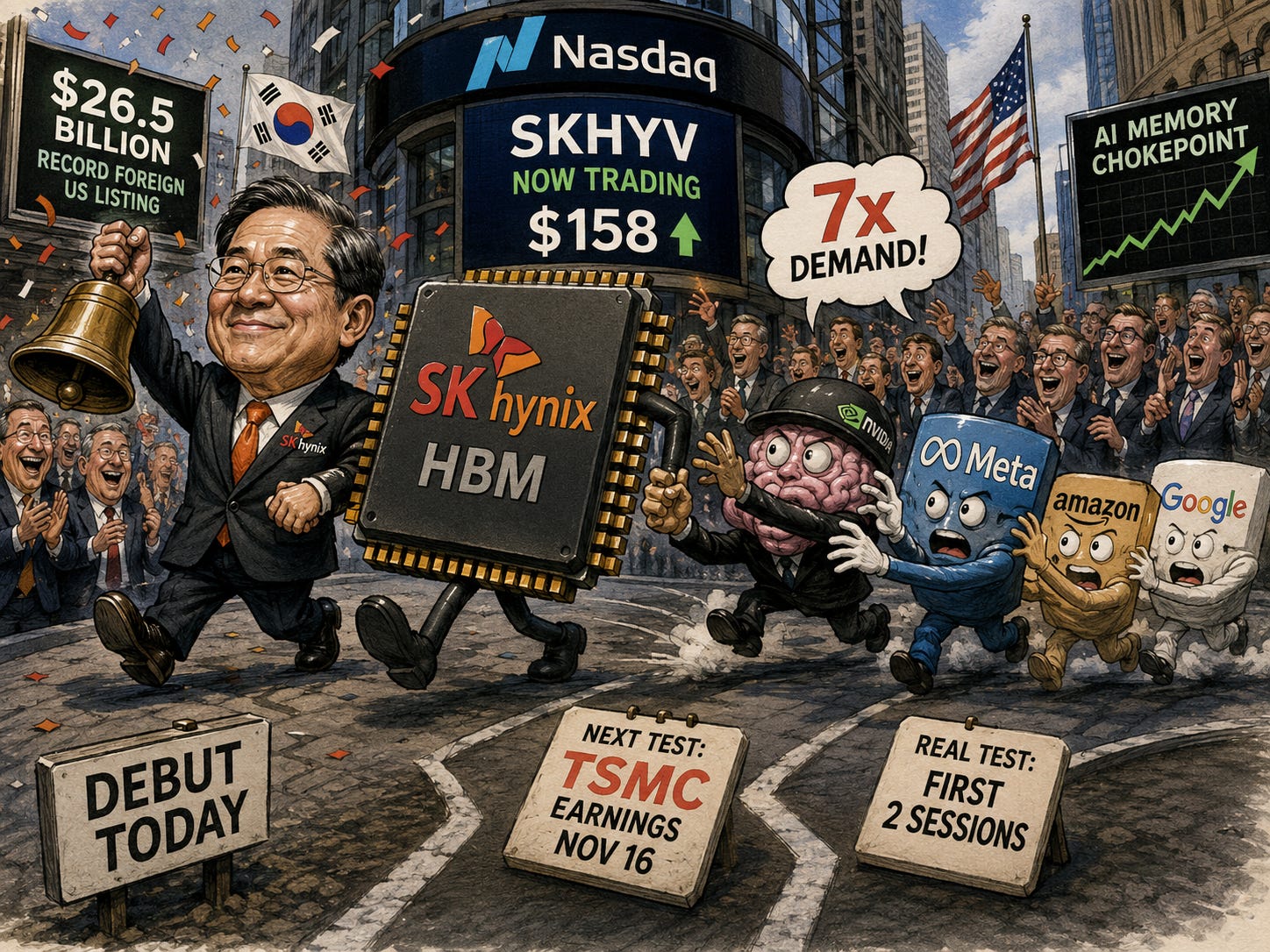

💾 SK Hynix lands on the Nasdaq: The Korean memory maker raised $26.5bn, the largest first-time US listing by a foreign company ever, and debuts today.

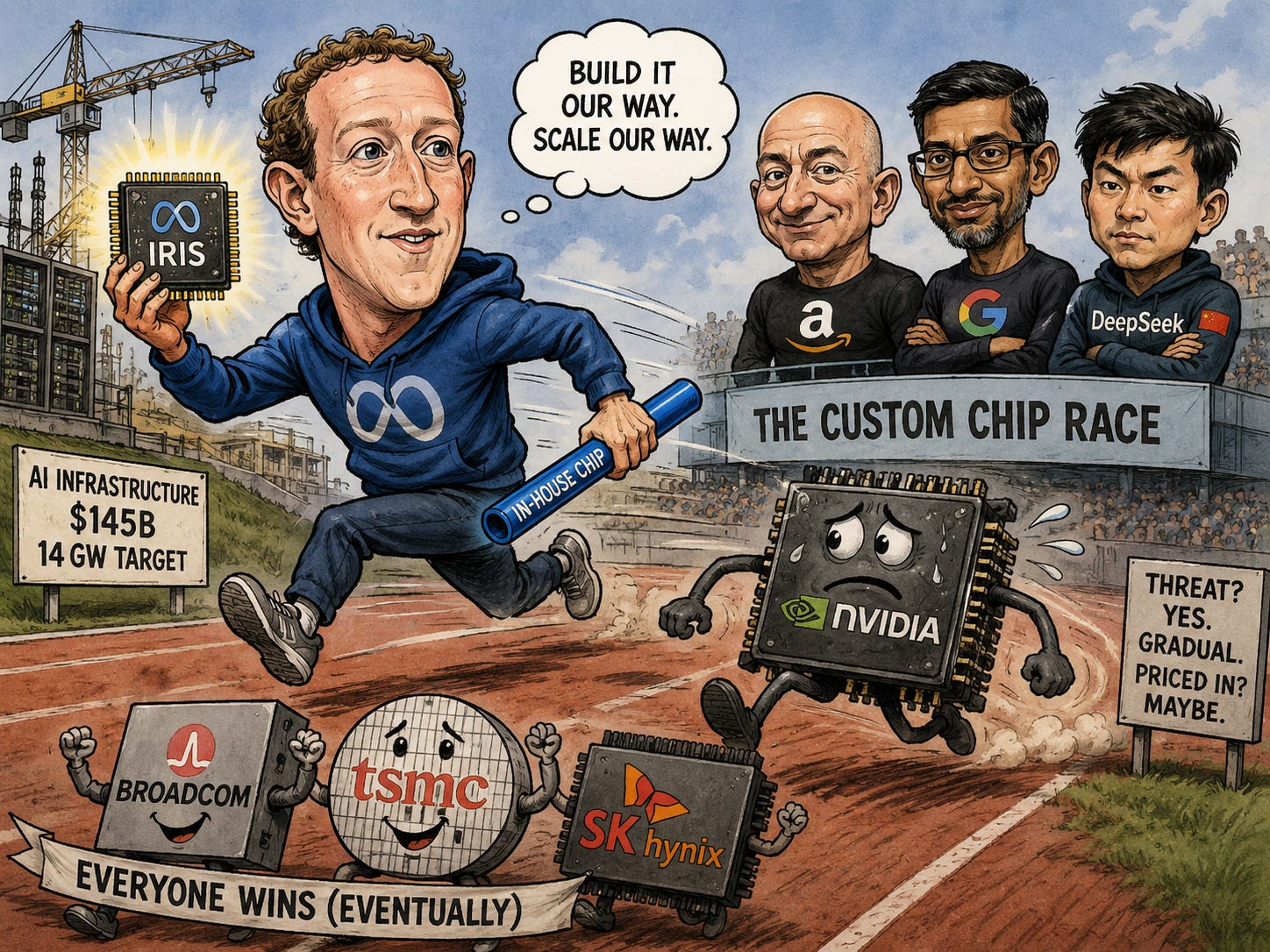

🧠 Meta builds its own chip: Facebook’s owner will start making an in-house AI chip in September, sending its shares up 4% on the plan.

✈️ Delta beats and holds its year: The airline topped estimates and guided Q3 profit to $2.00 to $2.50, opening earnings season on a firmer note.

₿ Regulation now moves crypto: Bitcoin held near $63,300 as Washington’s rulebook, not the Middle East, became the market’s main driver.

🛢️ Oil keeps sliding: Brent slipped toward $76 as returning Iranian barrels drained the war premium, even with US strikes still in the headlines.

🥇 Gold holds above $4,100: A softer dollar supported the metal, though rate-hike worries kept it well below January’s record near $5,600.

⚽ World Cup hits the last eight: Spain meet Belgium in Inglewood today, one of four quarter-finals played on US soil this weekend.

🔍 Washington’s four-week crypto window: Two US rulebooks, the SEC’s safe harbour and the CLARITY Act, could land or die by 7 August.

📈 Chart of the Day, XRP: XRP is pressing the multi-year trendline near $1.12; a clean break opens the road toward the $1.30 resistance

🧠 One Big Thing

Two stories landed today that point the same way: SK Hynix’s blockbuster debut and Meta’s move to make its own AI chip. The money in AI is quietly shifting from the merchant chip seller to the picks and shovels underneath it. Every hyperscaler now designing custom silicon, Meta after Amazon, Google and reportedly DeepSeek, still needs someone else’s memory and someone else’s foundry. That is why SK Hynix drew orders at seven times supply while Nvidia trades at its cheapest forward multiple since 2019. The trade may be splitting into who builds versus who sells. Watch memory and foundry names against Nvidia, with TSMC reporting on the 16th.

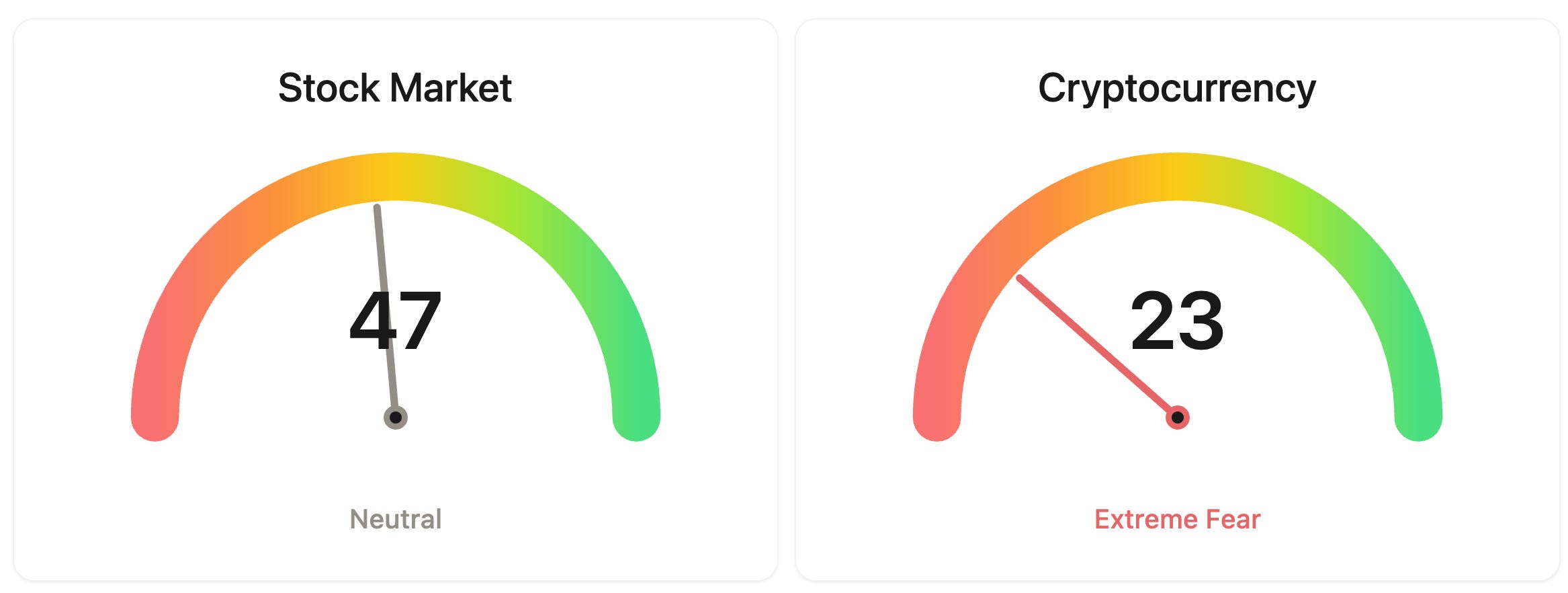

⚖️ Fear & Greed

📉 The Number That Matters

$26.5 billion

SK Hynix raised $26.5 billion in its US share sale, the largest first-time listing by a foreign company in American history, bigger than Alibaba’s 2014 debut, and it starts trading today.

⚔️ Winners vs Losers

Winners

JLHL 0.00%↑: Julong Holding Limited extended its low float squeeze into another pre-market session, with the thinly traded Chinese intelligent systems micro-cap ripping higher on momentum and short covering rather than any company news. The stock has tripped repeated volatility halts across recent sessions.

WDFC 0.00%↑: WD-40 Company jumped after its fiscal third quarter results blew past estimates, posting adjusted EPS of $2.33 versus roughly $1.57 expected and lifting full year revenue guidance.

CRCL 0.00%↑: Circle Internet Group surged after winning approval from the Office of the Comptroller of the Currency to establish Circle National Trust, a national trust bank that brings its USDC stablecoin infrastructure under direct federal oversight. A broad crypto rally with bitcoin back near $64,000 added a tailwind.

EQPT 0.00%↑: EquipmentShare.com raised its full year 2026 financial guidance on strong customer demand and authorized a new $500 million share repurchase program.

PNTG 0.00%↑: The Pennant Group moved sharply higher in pre-market with no specific catalyst identified.

META 0.00%↑: Meta Platforms climbed as its aggressive AI push drew fresh attention, with the company moving into the AI coding market and unveiling plans for a multibillion dollar Canadian data center to expand its compute footprint.

Losers

FRMI 0.00%↑: Fermi Inc. dropped after launching a $350 million convertible senior notes offering, later upsized to $375 million, with the dilution overhang weighing on the AI power developer as it works through an ongoing governance fight.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $64,378 (▲ 1.93%)

Ethereum (ETH): $1,800 (▲ 3.22%)

XRP: $1.11 (▲ 1.72%)

Equity Indices (Futures):

S&P 500: 7,584 (▼ -0.06%)

NASDAQ 100: 29,836 (▼ -0.34%)

FTSE 100: 10,463 (▲ 0.08%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.55% (▼ -0.04%)

Oil (WTI): $73 (▲ 1.28%)

Gold: $4,106 (▼ -0.41%)

Silver: $59.49 (▼ -0.77%)

Data as of: UK: 12:50 BST / US: 07:50 EDT / Asia (Tokyo): 20:50 JST

✅ 5 Things to Know

📈 AI powers Wall Street to fresh records

US stocks closed at highs yesterday as investors bet again on AI-driven demand and looked past a fresh flare-up in the Middle East. The Nasdaq Composite rose 1.3% to a record 26,206.89, the S&P 500 added 0.8% to 7,543.64, and the Dow gained 0.3% to 52,478.41 after a choppy session. Chip stocks led the charge: Micron climbed 5.2%, SanDisk jumped 7.6% and Applied Materials rose 3.2%, while Meta added 4% on plans to build its own AI chip. Futures were mixed this morning as traders waited for the Nasdaq debut of Korean memory maker SK Hynix (Yahoo Finance).

The pattern is the same one that has defined this week: any dip in the AI trade gets bought, and macro risks that would once have rattled markets are being waved through. That leaves the market leaning heavily on a single theme just as its two biggest near-term tests arrive. June inflation lands on the 14th and the first big banks report alongside it, either of which could interrupt the run. For now the momentum sits with the chipmakers and the hyperscalers spending on them, and the SK Hynix debut gives that appetite a live read this morning.

Sensei’s Insight: Records built on one theme are only as sturdy as that theme’s next data point. I am watching the 14 July inflation print and the bank results the same morning. If both pass cleanly, the AI bid likely keeps running; a hot number is where this week’s confidence gets tested first.

💾 SK Hynix’s $26.5bn Nasdaq debut

SK Hynix, the world’s second-largest memory chipmaker, pulled off the biggest first-time US listing by a foreign company on record and begins trading on the Nasdaq today. It sold American Depositary Shares at $149 each and raised $26.5 billion, a deal larger than Alibaba’s 2014 debut, with institutional orders running more than seven times the shares available. Trading opens under the temporary ticker SKHYV on a when-issued basis, with regular dealing under SKHY due to start on the 13th. Early indications put the stock near $158, which is below its Korean-share equivalent and short of the 20% premium HSBC had projected (Yahoo Finance).

Every AI system, the ones answering questions and generating images, runs on specialised chips, and those chips are close to useless without fast memory sitting right beside them to feed in data. That memory is called HBM, high-bandwidth memory, and SK Hynix makes more of it than anyone else on the planet, roughly 56% of global supply. So while Nvidia takes the headlines for the AI brain, SK Hynix quietly supplies a large share of the short-term memory that brain cannot think without. Listing in New York puts that business in front of American investors for the first time, in one of the largest fundraises the market has ever seen.

The listing lands amid a bigger shift running through the whole sector. Tech giants like Meta, Amazon and Google are racing to design their own custom chips rather than buy everything from Nvidia, yet they all still need the same ingredient underneath: memory. That turns SK Hynix into a rare name that wins almost regardless of which chip design comes out on top, since nearly every AI accelerator, whoever builds it, needs its parts. Demand running at seven times the shares on offer is the market saying it wants direct exposure to that chokepoint, not only to the famous names sitting above it (CNBC).

The opening price is a reality check rather than a verdict. A debut below its home-market value and below the premium the bankers wanted suggests a lot of optimism is already baked into the number, which is common when a listing arrives this hyped. The more useful signal is how SKHYV trades across its first few sessions, because it works as a live thermometer for the entire AI-hardware trade. It also lands a week before TSMC, the world’s biggest chip manufacturer, reports on the 16th and gives the next hard read on whether the AI spending boom is still accelerating.

Sensei’s Insight: Watch the first two sessions, not the opening tick. If SKHYV holds its ground once index and fund buying clears, the memory bid is real. If it fades instead, that is a hint even the strongest AI names may now be priced for too much to go right.

🧠 Meta moves to build its own AI chip

Meta plans to start production of an in-house AI chip code-named Iris in September, a step meant to cut its reliance on outside suppliers and roughly double its computing capacity. According to an internal memo, the chip is the latest generation of Meta’s own accelerator programme and will be manufactured with Broadcom and TSMC, after testing that reportedly took just six weeks and flagged no major problems. The plan sits inside an AI infrastructure budget that could reach $145 billion this year and a target of 14 gigawatts of computing power. Investors liked it: Meta shares rose 4% (CNBC).

The move matters because it puts Meta alongside Amazon, Google and, reportedly, China’s DeepSeek in designing custom silicon rather than buying every chip from Nvidia. That could reshape who captures AI’s profits over time, though it comes with a catch worth stating plainly: a custom chip still needs someone else’s memory and someone else’s foundry. Broadcom and TSMC gain a marquee customer, and SK Hynix, debuting today, sells into exactly this demand. The threat to Nvidia is real but gradual, and its shares now trade at their cheapest forward multiple since 2019, so much of that pressure may already be reflected.

Sensei’s Insight: Custom silicon is a margin story before it is a volume story. The read is not that Nvidia loses, it is that the value spreads to Broadcom, TSMC and the memory makers who supply everyone. I am watching how large Meta says the Iris order actually is.

✈️ Delta beats and lifts its outlook

Delta Air Lines opened earnings season with a better-than-expected quarter and a confident tone on the rest of the year. The carrier topped the roughly $1.48 per share Wall Street had modelled, even as profit fell sharply from a year earlier on higher fuel costs, and guided third-quarter earnings to a range of $2.00 to $2.50 against the roughly $2.02 analysts expected. It reaffirmed its full-year forecast of $6.50 to $7.50 per share. Chief executive Ed Bastian said the original profit goal is still in reach because the airline can pass higher fuel bills through to customers (CNBC).

Delta is the traditional curtain-raiser for the season, so its read on the consumer carries beyond the airline itself. The message is that demand for premium travel is holding and that pricing power has not cracked, even with costs elevated. That is a reassuring signal for the sector and a mild positive for the wider consumer picture the market has been fretting over since the soft June jobs report. The bigger test comes next week, when the large banks report and give a broader look at spending and credit (Yahoo Finance).

Sensei’s Insight: Guidance above the Street matters more than the beat here. Bastian is effectively saying fares can absorb the fuel bill, and that pricing power is the whole airline thesis right now. I am watching whether the other carriers echo it or quietly walk their numbers down.

₿ Regulation, not geopolitics, now drives crypto

Bitcoin held near $64,000 this morning, up around 2% over 24 hours, with the market’s attention swinging from Middle East headlines to Washington’s rulebook. The tone steadied as US spot Bitcoin ETFs snapped a long outflow streak, and the wider debate has moved to two pieces of policy. The CLARITY market-structure bill still sits on the Senate calendar with no floor vote scheduled, blocked by disputes over ethics disclosures, insider-trading rules and stablecoin yield. Separately, a statutory deadline for finalising GENIUS Act stablecoin rules falls on the 18th. The Senate returns from recess on the 13th (Yahoo Finance).

This is a real shift for anyone holding crypto: the next big move is more likely to come from a committee room than a conflict. A credible signal that CLARITY can clear its 60-vote Senate threshold before the August recess would be a genuine catalyst, since it would settle which tokens count as commodities and open the door to more regulated products. The flip side is that any sign of the bill slipping into next year removes a support the market has been leaning on. With roughly three usable weeks before the recess, the window is real but tight.

Sensei’s Insight: Crypto trading on legislation rather than price momentum is a maturing-market signal, not a boring one. I am watching the Senate’s first week back for any move on CLARITY. No vote is scheduled, so headlines about the timeline will do the moving until one is.

Stories You Might Have Missed

🛢️ Oil slips as Iranian barrels return

Crude kept falling this morning, with Brent trading near $76 after losing more than 2% yesterday and West Texas Intermediate below $72. The driver is supply, not calm: even with fresh US strikes on Iran and retaliatory attacks on American bases in the region keeping the Strait of Hormuz in the headlines, the return of Iranian crude has drained the war premium that spiked prices earlier in the week. Traders are treating the conflict as a supply story with a known offset rather than an open-ended shock, which is why the geopolitical risk has faded from the price faster than the headlines suggest. Lower oil also quietly helps the inflation picture heading into next week’s CPI (Bloomberg).

🥇 Gold holds above $4,100

Gold steadied above $4,100 an ounce, supported by a softer US dollar but capped by the risk that the Fed still tilts toward a rate hike. The tension is straightforward: a weaker dollar makes the metal cheaper for overseas buyers, while higher rates raise the cost of holding an asset that pays no yield. That tug-of-war has kept gold rangebound this week even as Middle East tensions flared, well below the record near $5,600 set in late January. Next week’s inflation print is the near-term swing factor, since a hot number would firm up hike expectations and weigh on the metal, while a soft one would loosen that grip (Yahoo Finance).

⚽ World Cup reaches the last eight on US soil

The World Cup hits its quarter-finals this weekend, with all four ties played in the United States as the co-host nation keeps the tournament close to home. Spain meet Belgium in Inglewood today, followed by three more over the weekend in Miami Gardens and beyond, including Argentina and England still in the hunt. For investors the angle is the consumer: a major tournament on home soil pulls spending into travel, hospitality, streaming and advertising, a small but real tailwind for those sectors through the summer. The US men’s team is already out, beaten by Belgium in the round of 16, which takes some domestic heat out of the ratings story but not the spending one (Yahoo Sports).

🔍 Deep Dive: The Four-Week Window That Could Set US Crypto Rules for a Decade

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.