Morning Forecast: Friday 17 July

Netflix slides after hours, a chip selloff grips tech, and SpaceX falls below its IPO price.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

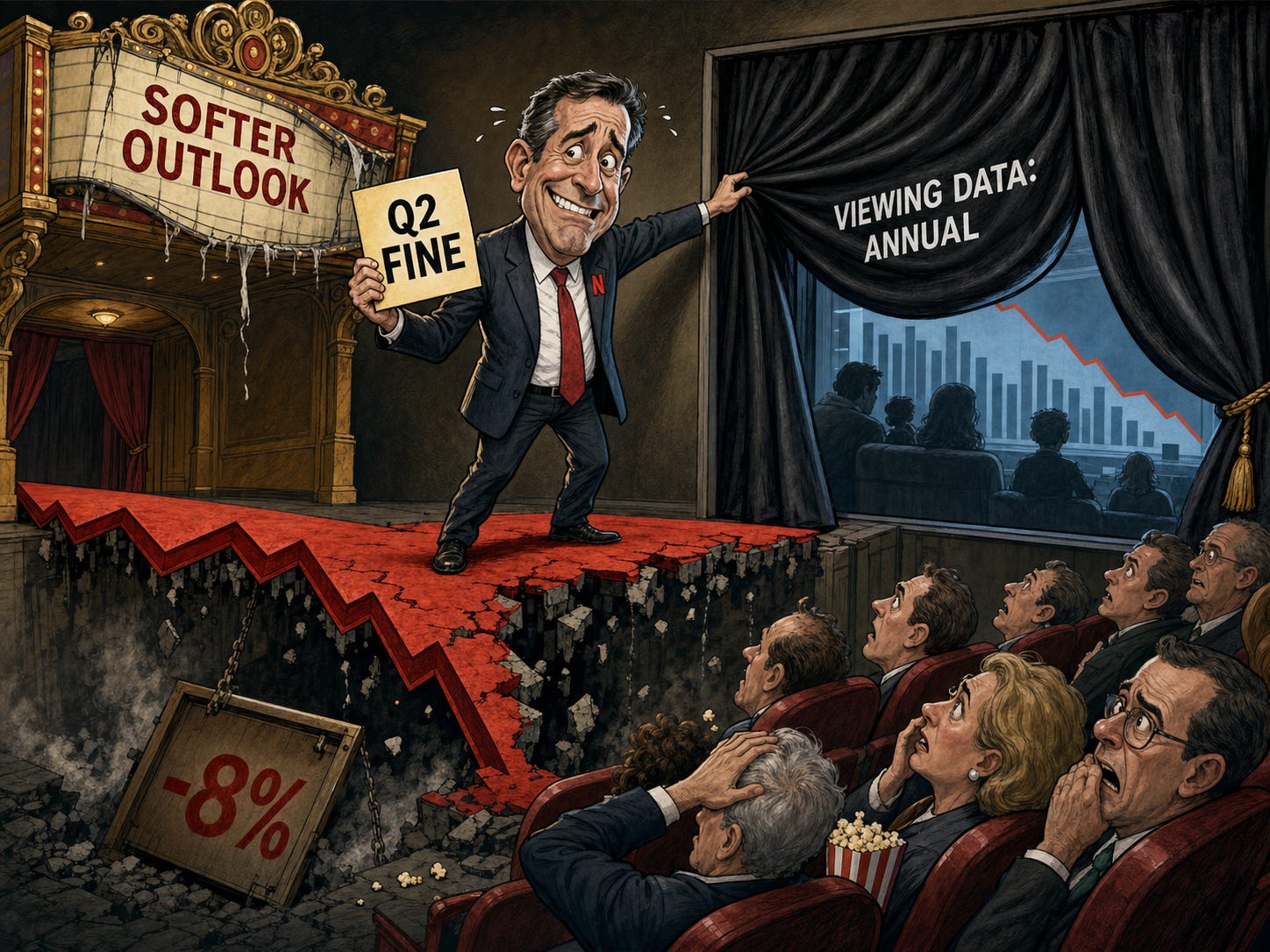

🎬 Netflix cools after hours: A soft third-quarter outlook sent the stock down more than 8%, even as the quarter itself met forecasts.

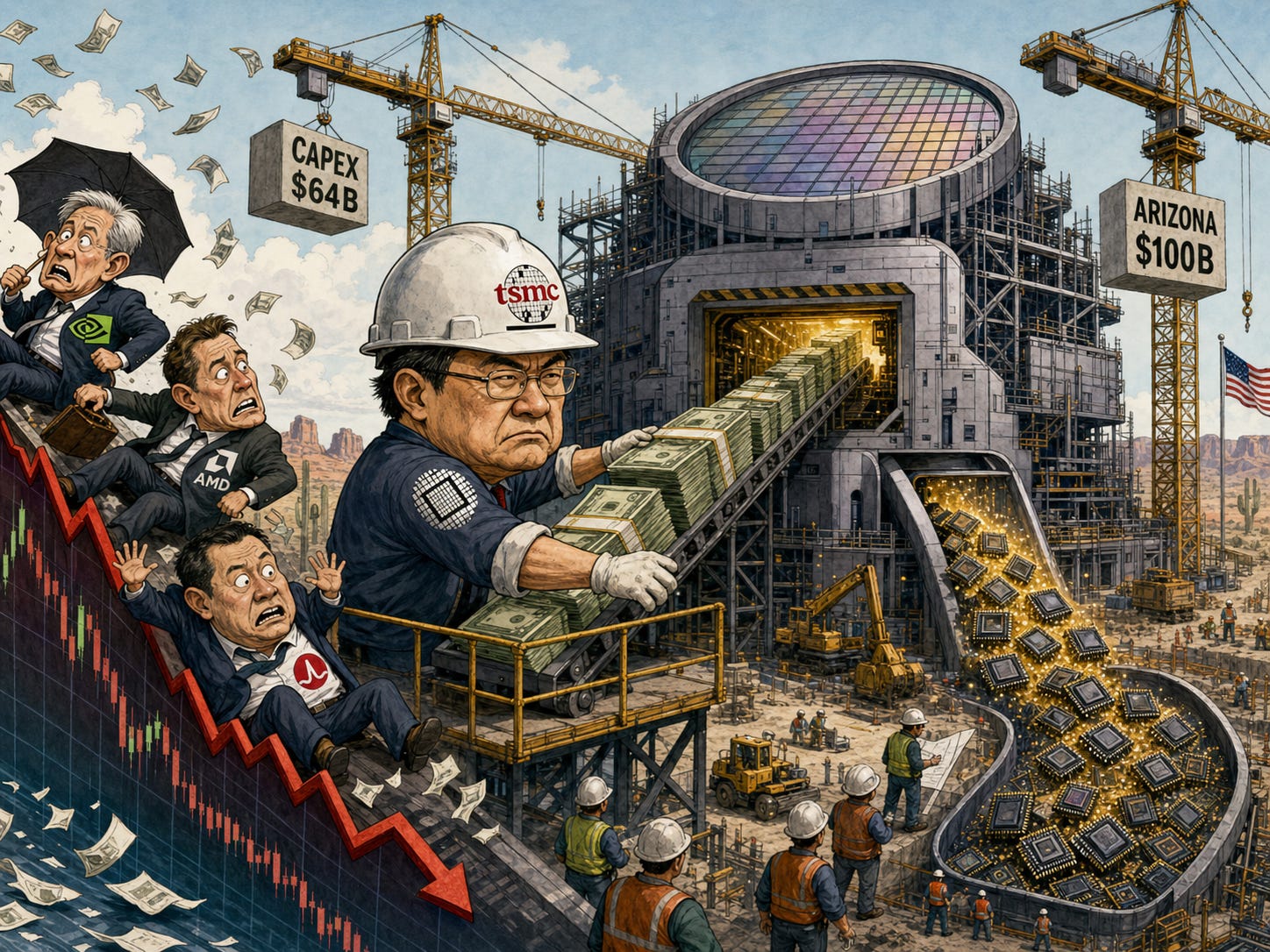

📉 Chips extend the rout: TSMC’s jump in spending plans deepened fears over the cost of AI, dragging the Nasdaq to a second straight loss.

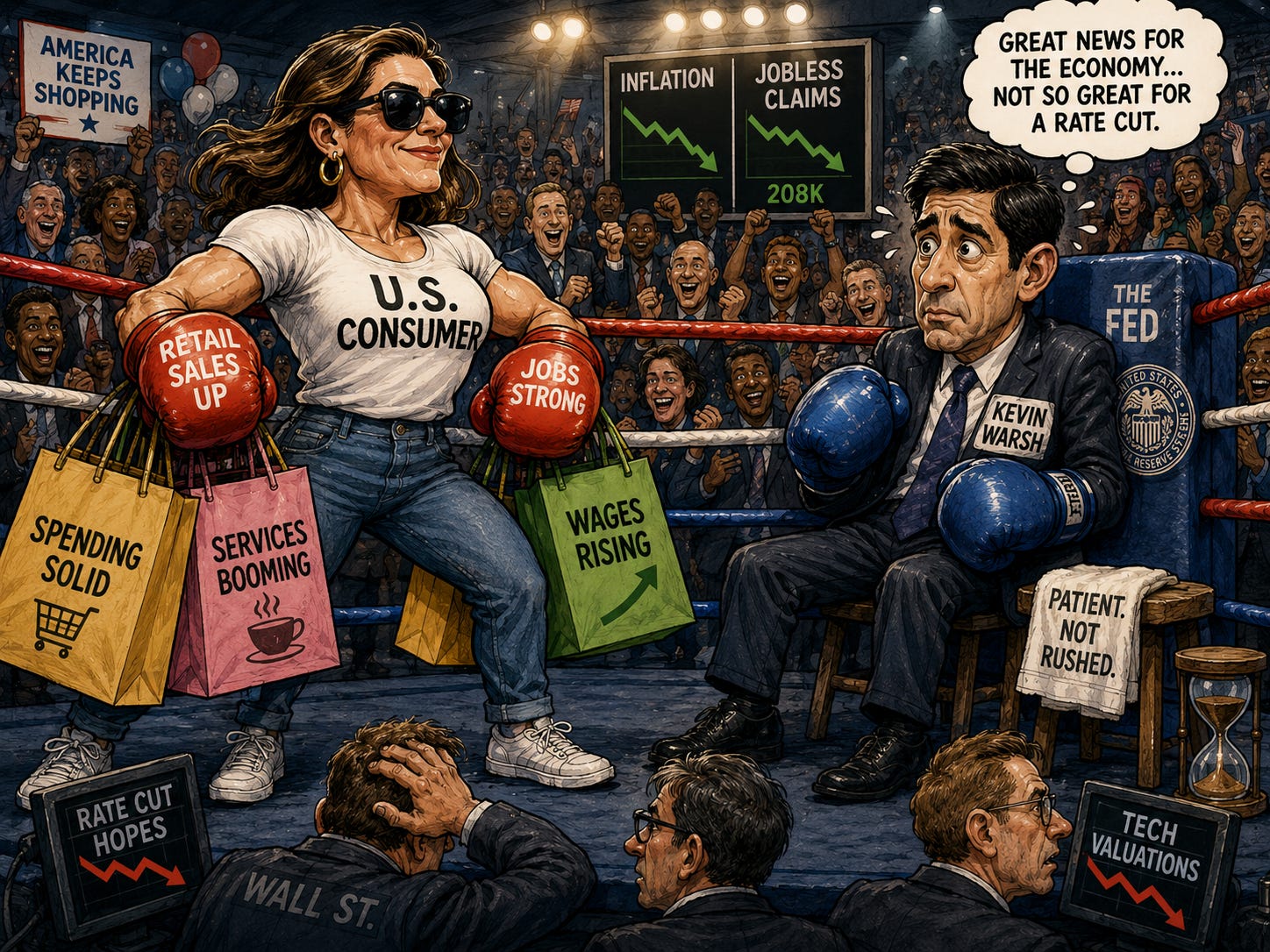

🛍️ Shoppers box in the Fed: June retail sales held up and jobless claims fell to 208,000, giving policymakers little reason to cut soon.

🏥 UnitedHealth beats and raises: Adjusted profit of $6.38 crushed the $4.85 forecast, and shares jumped 8% as the outlook rose.

🛢️ Oil grinds higher again: A sixth night of US strikes on Iran left Brent near $85 and up about 12% on the week.

₿ Crypto’s bill hits Wall Street: The CLARITY Act gets a New York hearing today as Bitcoin holds near $63,100, though no vote is scheduled.

🥇 Gold’s haven bid fades: Bullion is heading for its worst week in six, stuck near $4,000 as rate fears outweigh the war.

🔍 The SpaceX playbook, five weeks on: The pre-IPO base case has tracked almost date for date, with the stock now slipping below its $135 offer.

📈 Chart of the Day: Silver is sliding under its trendline and Momentum Band, with $50 the psychological level Sensei is watching into the drop.

🧠 One Big Thing

TSMC just told the market that AI demand is so strong it will spend as much as $64 billion this year and pour another $100 billion into Arizona, and the market sold chips anyway. That reaction is not a vote against AI; it is a question about the return. Capex is a cost booked today against profits that arrive years later, and when the Fed refuses to cut, those distant payoffs get discounted harder. The tension now is whether the big spenders can show revenue catching up to the bill. Watch whether Nvidia and AMD steady the group, and watch the 10-year yield.

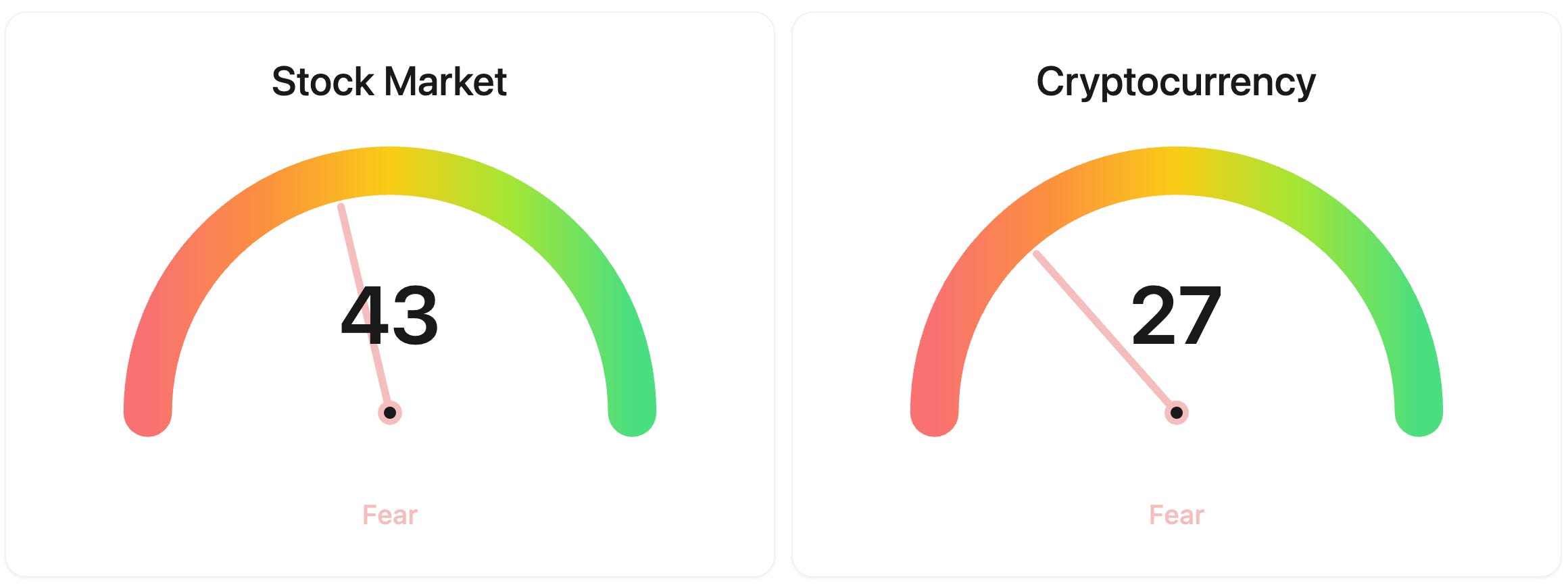

⚖️ Fear & Greed

📉 The Number That Matters

$12.86 billion

Netflix’s third-quarter revenue guide, short of the roughly $13 billion Wall Street wanted, which knocked the stock more than 8% after hours.

⚔️ Winners vs Losers

Winners

No major winners today

Losers

STAA 0.00%↑: -11.90% STAAR Surgical fell after posting preliminary second quarter net sales above $90 million that still underwhelmed the market, as Middle East weakness and the continued absence of full year guidance overshadowed the headline growth.

ISRG 0.00%↑: -11.26% Intuitive Surgical slid despite beating on both revenue and earnings, with investors fixating on slowing surgery volumes, a recent Class II recall of certain da Vinci components, and a stretched valuation.

NFLX 0.00%↑: -9.89% Netflix dropped after its second quarter report showed revenue slightly below expectations and softer third quarter guidance, even as earnings came in ahead of estimates.

POWL 0.00%↑: -6.27% Powell Industries moved sharply lower in pre-market with no specific catalyst identified.

PURR 0.00%↑: -5.60% Hyperliquid Strategies fell in sympathy with a roughly 9 percent overnight drop in the HYPE token that its treasury strategy tracks directly, amid a broader crypto pullback.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $63,123 (▼1.05%)

Ethereum (ETH): $1,835 (▼1.51%)

XRP: $1.09 (▼0.07%)

Equity Indices (Futures):

S&P 500: 7,519 (▼0.78%)

NASDAQ 100: 28,800 (▼1.46%)

FTSE 100: 10,546 (▼0.14%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.53% (▼0.70%)

Oil (WTI): $80 (▲0.55%)

Gold: $3,992 (▲0.35%)

Silver: $55.29 (▼0.40%)

Data as of: UK: 12:00 PM BST / US: 7:00 AM EDT / Asia (Tokyo): 8:00 PM JST

✅ 5 Things to Know

🎬 Netflix stumbles on a softer outlook

Netflix reported second-quarter revenue of $12.56 billion, up about 13% from a year earlier, with earnings of $0.80 a share edging past forecasts by a penny and an operating margin near 33%. The quarter itself was fine. What unsettled investors was the outlook: the company guided third-quarter revenue to $12.86 billion, growth of just under 12% but shy of the roughly $13 billion analysts wanted, and it pointed to a second straight quarter of slowing sales. It also said it would disclose less, cutting its viewing report to once a year from 2027. The shares fell more than 8% after the close (CNBC).

The drop matters because Netflix had become a proxy for the whole streaming trade, and the stock went in already down about 42% from last summer’s high. A slowing top line collides with a company that has leaned on price rises and a young advertising business to keep growth alive, and the reduced disclosure makes it harder to check how engagement is really trending against YouTube and TikTok. The read-across runs to the ad-supported tier and to peers reporting later this month. For a market already nervous about paying up for growth, a marquee name guiding lower is the kind of signal that spreads.

Sensei’s Insight: The quarter was not the problem, the guide was. When a company this closely watched trims both its growth and how much it will tell you, the market fills the gap with caution. That is what a nervous tape does to any richly priced name.

📉 Chips deepen the selloff as AI-spending fears bite

A global selloff in semiconductors dragged Wall Street to a second straight loss, and the trigger was spending rather than demand. TSMC, whose results were strong, lifted its 2026 capital budget to as much as $64 billion from a prior ceiling near $56 billion, and flagged another $100 billion for its Arizona plants. Investors read the surge as a sign that the cost of building AI is climbing faster than the payoff, and they sold. The Philadelphia semiconductor index fell more than 2.6%, Nvidia, AMD and Broadcom slid between roughly 2% and 3%, and the Nasdaq Composite closed down 1.47% at 25,881.95 (CNBC).

This is the same worry that hit the memory names earlier in the week, now aimed at the foundry leader: demand is real, but the bill is enormous and the return is years out. Futures pointed lower again this morning, with a sixth night of US strikes on Iran adding to the caution. The next tests are concrete. Chip-equipment orders read strong earlier in the week, so the question is whether the AI leaders can convert record spending into the revenue growth that justifies it. Until they do, every large capex number gets read as a cost first and a promise second.

Sensei’s Insight: Spending more is usually a confidence signal. The market flipped it into a worry because the Fed will not cut, so distant payoffs are discounted hard today. Watch whether the biggest names steady the group or the fear keeps spreading.

🛍️ Resilient shoppers keep the Fed boxed in

The US consumer and the jobs market both refused to buckle. June retail sales rose 0.2% on the month and 6.7% from a year earlier, in line with forecasts, with a 5.3% drop at petrol stations masking a firmer 0.7% gain once fuel is stripped out. Weekly jobless claims fell to 208,000, below the 217,000 economists expected, and continuing claims came in lighter too. After cooler inflation readings earlier in the week, the data shows an economy still growing at a steady clip rather than one crying out for lower rates (Yahoo Finance).

That is the tension for markets. Softer inflation had revived hopes of a rate cut, but a resilient consumer and a firm labour market hand the new Fed chair every reason to wait, and he has already said the inflation fight is not finished. With the Fed’s pre-meeting quiet period starting tomorrow and the decision due at the end of the month, today’s first read on July consumer sentiment is the last major data point before officials go silent. A strong economy is good news, except for anyone hoping cheaper money arrives soon.

Sensei’s Insight: Good news is awkward news right now. Every sign the consumer is fine pushes a rate cut further away, and that is exactly what stretched tech valuations did not want to hear. The data, not the Fed, may end up forcing the issue.

🏥 UnitedHealth beats big and lifts its outlook

UnitedHealth delivered the kind of clean beat the managed-care sector badly needed. Adjusted earnings came in at $6.38 a share against a consensus near $4.85, on revenue of $112 billion, and the company raised full-year adjusted profit guidance to a range of $19.50 to $20.00, well above the roughly $18.50 the market expected. It also lifted its cash-flow outlook toward $24 billion. The metric that matters most, the medical care ratio, improved to 86.7% from 89.4% a year earlier, the number that had spooked investors through a bruising stretch of rising costs. The shares jumped about 8% (Yahoo Finance).

The result matters beyond one company. UnitedHealth is a bellwether for the whole health-insurance industry and a heavyweight in the Dow, so a turnaround in its cost trend tends to lift peers and steady a corner of the market that had been a persistent drag. Management credited benefit redesign, firmer pricing and tighter medical management for the improvement, the levers investors wanted to see working. The question from here is durability: whether one strong quarter marks a genuine turn in medical costs or a single good print. For now, it is a rare bright spot on an otherwise heavy day.

Sensei’s Insight: The medical care ratio was the number that broke this stock, and it just moved the right way. One quarter is not a trend, but a beat this size alongside a raised outlook is the clearest sign yet that the cost scare is easing.

🛢️ Oil climbs again on a sixth night of strikes

Oil pushed higher for a third straight session as the conflict between the US and Iran escalated. US Central Command said it had completed a sixth consecutive night of strikes, hitting military and maritime targets, with reports of five bridges struck and seven people killed. The market’s focus is the Strait of Hormuz, the channel that carries about a fifth of the world’s seaborne crude, where confirmed transit has fallen 62% to 4.1 million barrels a day. Brent traded near $85 and WTI near $80, leaving crude up roughly 12% on the week (CNBC).

The stakes for everyone else run through the pump and the inflation data. Higher crude feeds into petrol prices and complicates the disinflation story that cooler CPI and PPI told earlier in the week, which is part of why gold has struggled and the Fed is in no rush to cut. A 60-day ceasefire memorandum signed last month expires in mid-August, and energy consultancy Rystad expects a narrow, face-saving deal rather than a full resolution. Until the strikes stop, the risk premium stays in the price, and it is the disruption, not a closure of the strait, that is doing the work.

Sensei’s Insight: This is a supply shock, not a growth scare, and it behaves differently. It lifts inflation risk, pressures the case for rate cuts, and keeps a bid under energy. The mid-August memo expiry is the date to circle.

₿ Crypto’s rulebook heads to Wall Street

The House Financial Services Committee holds a field hearing on the CLARITY Act in New York today, staged at Federal Hall under the title “Building the Future of Finance.” The bill would split oversight of digital assets between the CFTC and the SEC, and the House already passed it last year, so today is about building momentum and taking industry testimony, not casting a vote. The aim is to press the Senate to act before its August recess. Bitcoin held near $63,100 and Ether near $1,835 into the event, steady rather than spiking, a sign traders see a milestone in the making but not a done deal (Yahoo Finance).

🥇 Gold’s haven bid goes missing

Gold is heading for its worst week in six, hovering around $4,000 even as the US and Iran trade strikes, an unusual failure of the classic safe-haven trade. The reason is that the same forces lifting oil are working against bullion: firmer energy prices point to stickier inflation, that keeps the Fed leaning hawkish, and higher-for-longer rates plus a stronger dollar make gold, which pays no yield, less attractive than cash and Treasuries. For a metal that set a record above $5,500 in January, the slide shows how completely the rate outlook has taken over from fear as the driver (Yahoo Finance).

🔍 Deep Dive: The SpaceX Playbook, Five Weeks On

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.