Morning Forecast: Friday 19 June

Israel's strike in Lebanon just froze the Iran deal, the one thing keeping oil and your gas bill down.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🇮🇱 Lebanon strikes freeze Iran deal: heaviest assault since the truce postpones Switzerland talks and threatens reopened oil flows.

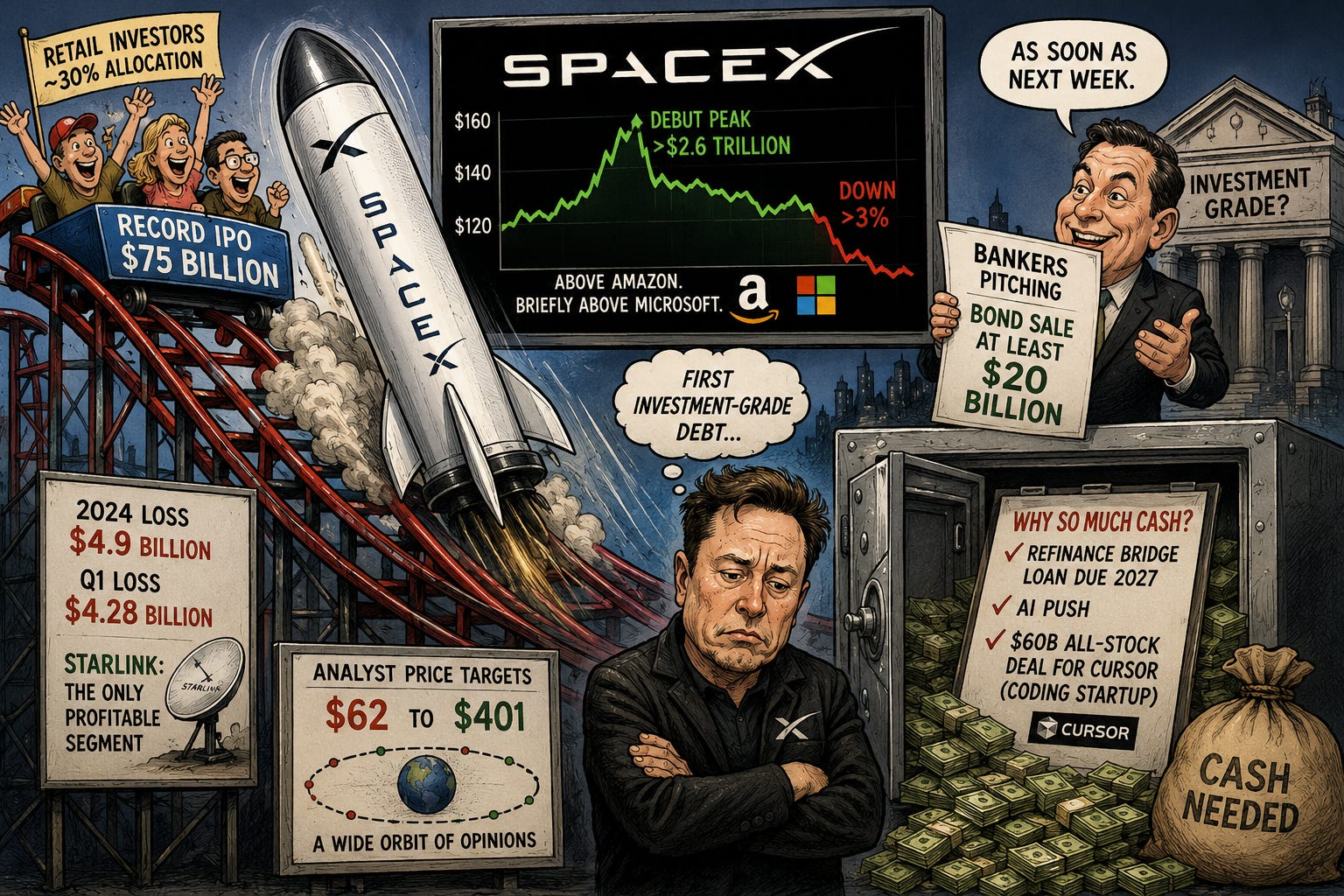

🚀 SpaceX slides, eyes record debt: shares fell again as bankers prepare a $20 billion bond pitch next week.

💻 Intel jumps on Apple claim: stock closed up about 10% on Trump’s unconfirmed post, with no terms attached.

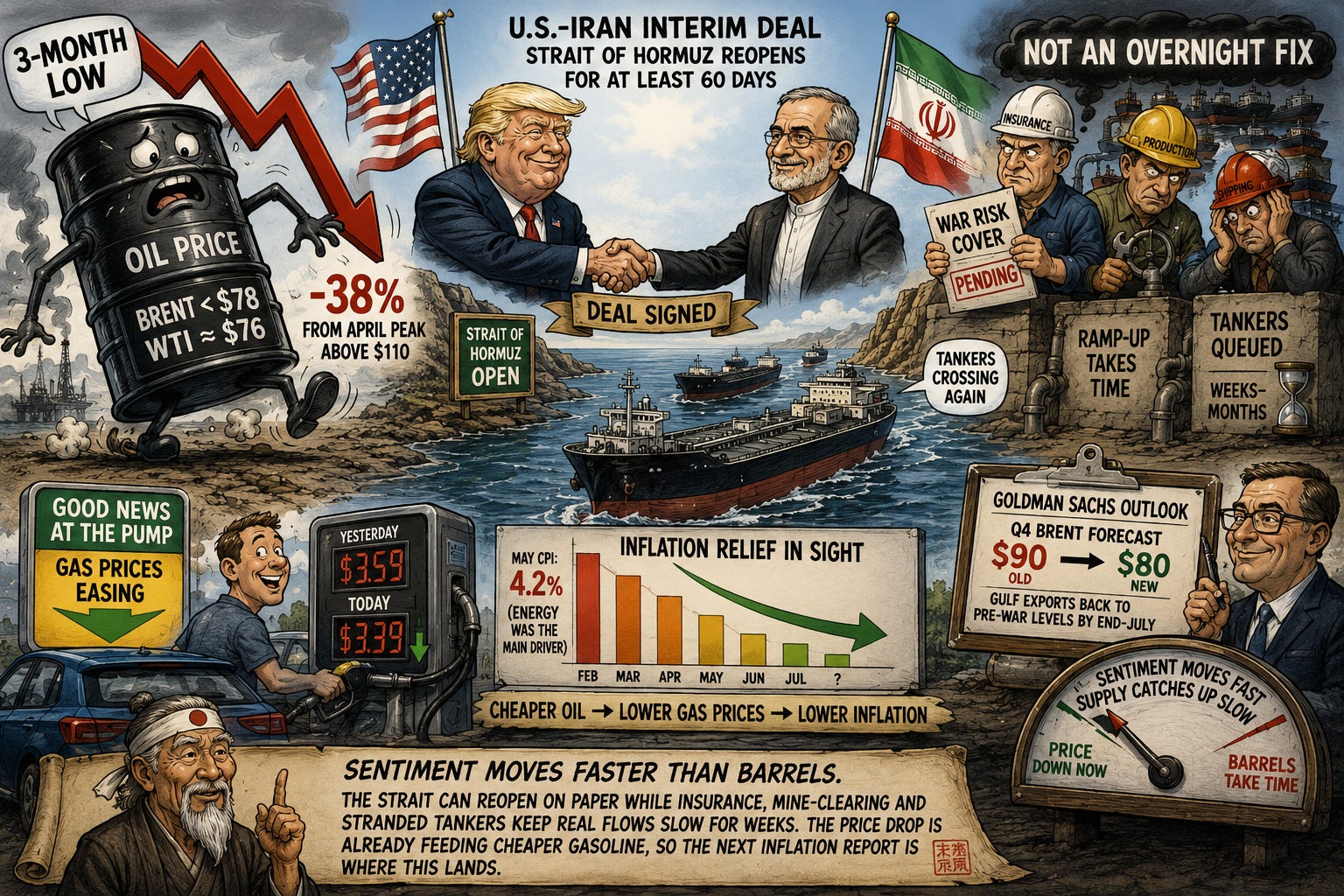

🛢️ Oil hits three-month low: Brent fell below $78 after Trump and Pezeshkian signed an interim Hormuz deal.

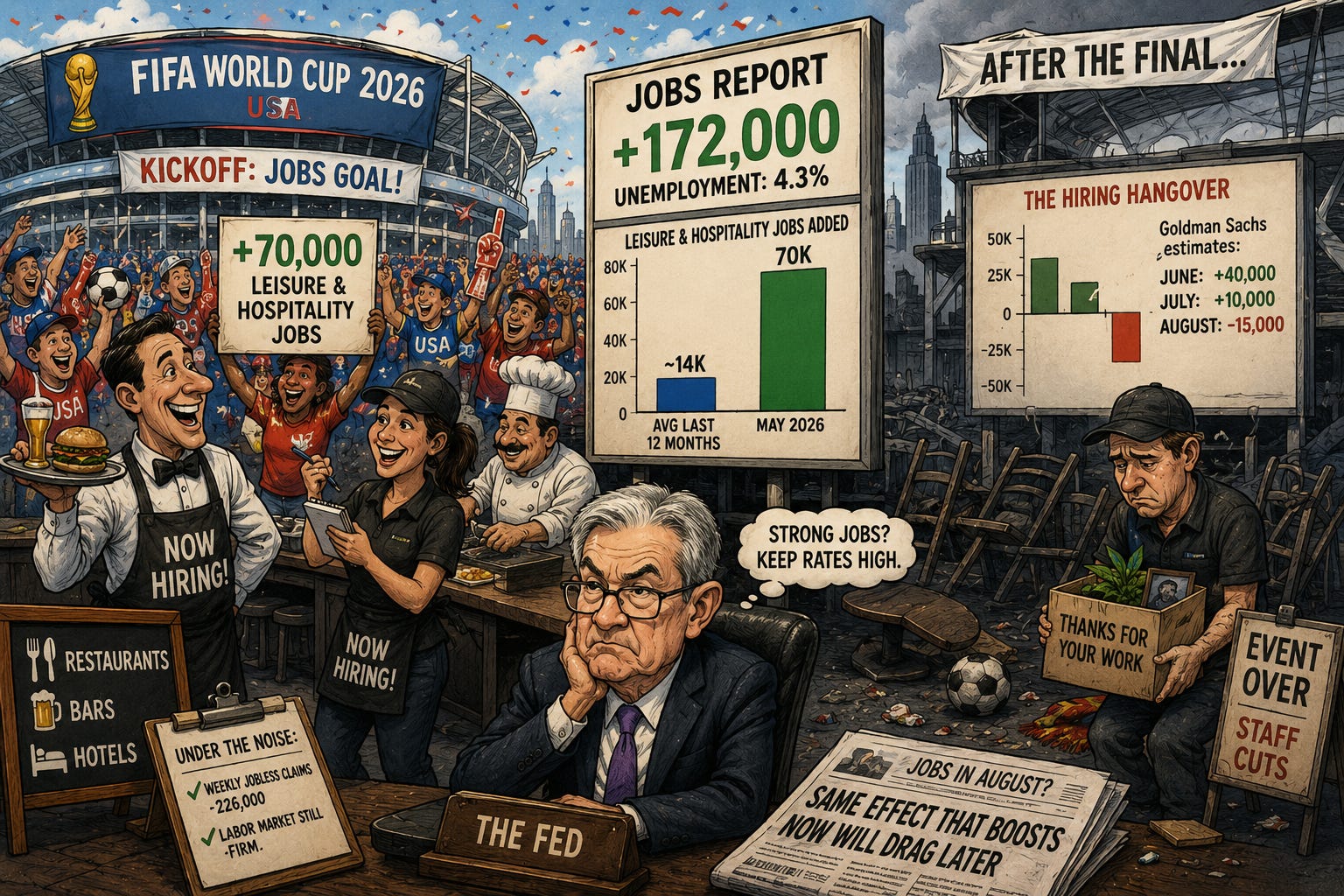

⚽ World Cup flatters jobs data: tournament hiring lifted last month’s payrolls, a boost set to reverse by August.

📈 Strategist warns of Fed hike: Ed Yardeni says rates may rise if the Fed targets 2% inflation.

📦 FedEx and Micron report next: a major shipper and the cleanest AI memory gauge headline next week’s earnings.

🪙 SEC weighs tokenised stocks: a proposed exemption could let crypto firms offer blockchain versions of regular shares.

🇬🇧 Bank of England holds rates: policymakers kept rates at 3.75% in a 7-2 vote, two pushing to hike.

🧠 One Big Thing

The thread tying SpaceX and Intel together today is the sheer cost of the AI build-out. SpaceX raised a record $75 billion, then lined up at least $20 billion in debt a week later, with only Starlink profitable against billion-dollar quarterly losses. Intel, now roughly a third government-owned, jumped about 10% on an unconfirmed Apple claim carrying no terms, while real foundry commitments stay unproven until its July earnings. Both show money and hype running well ahead of delivered results. The test is funding cost, since that $20 billion bond pitch lands just as central banks turn more hawkish. Watch credit spreads and how the SpaceX deal prices next week.

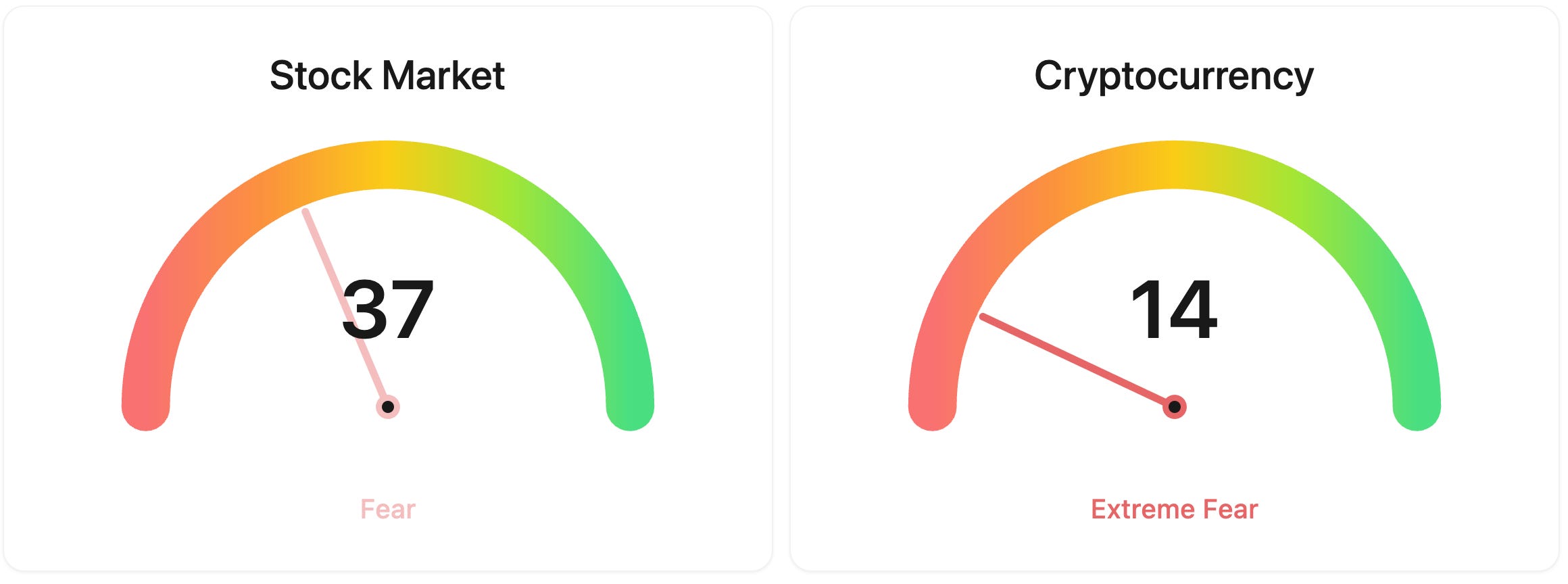

⚖️ Fear & Greed

📉 The Number That Matters

$62 TO $401

The spread on SpaceX analyst price targets runs from $62 to $401, a range so wide it signals almost no agreement on what a company valued above $2 trillion is actually worth.

⚔️ Winners vs Losers

No gainers or losers today. U.S. markets are closed for Juneteenth National Independence Day, the federal holiday marking June 19, 1865, when enslaved people in Galveston, Texas learned they were free, more than two years after the Emancipation Proclamation. The NYSE and Nasdaq are shut, with regular trading resuming Monday, June 22.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $62,458 (▼ 0.71%)

Ethereum (ETH): $1,689 (▼ 1.22%)

XRP: $1.12 (▼ 1.84%)

Equity Indices (Futures):

S&P 500: 7,553 (▼ 0.24%) US market closed

NASDAQ 100: 30,611 (▼ 0.35%) US market closed

FTSE 100: 10,374 (▼ 0.32%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.46% (▼ 0.71%)

Oil (WTI): $76 (▲ 0.46%)

Gold: $4,154 (▼ 1.55%)

Silver: $64.94 (▼ 1.24%)

Data as of: UK: 11:26 BST / US: 06:26 EDT / Asia (Tokyo): 19:26 JST

✅ 5 Things to Know

🇮🇱 Israel’s Lebanon assault stalls the Iran deal

Israel’s escalation in Lebanon is now the thing freezing the Iran peace deal that pulled oil prices down this week. Talks between Washington and Tehran meant to begin in Switzerland today were postponed, with US Vice President JD Vance pulling out of the trip. The official reason was logistics. The real trigger was an overnight Israeli assault on southern Lebanon, the heaviest since the memorandum of understanding took effect, which killed 18 people and wounded 33 across nearly a dozen locations. Israel’s far-right national security minister, Itamar Ben Gvir, brushed off American pressure with “all due respect to the US” and posted that “the whole of Lebanon must burn.” Israel insists it is not party to the deal and will keep troops inside Lebanon until it judges Hezbollah no longer a threat. The deal demands a halt to all fighting, Lebanon included, so Israel is the obstacle. (CBS News)

Washington is no longer hiding its anger. President Trump has sworn at Prime Minister Benjamin Netanyahu in calls, accusing him of nearly wrecking the agreement, and Vance has warned the Israeli cabinet not to blow it up, saying that where Israel’s political goals clash with American interests, Trump will choose America’s. For markets, one clause decides everything: the permanent halt to fighting on all fronts is what keeps the Strait of Hormuz open and oil moving. Brent crude sits near $80 a barrel, down about 8% this week but still roughly 30% higher than where it started the year, all on the bet that Hormuz normalises. Vance has said plainly that if the strait does not stay open, there is no final deal. Iran suspended talks once already over Lebanon, and it could again. What to watch: whether Vance travels this weekend, the 60-day clock that just started, and Israel’s October election, which gives Netanyahu’s coalition every reason to keep striking. (Bloomberg)

Sensei’s Insight: The deal needs Israel to stop fighting in Lebanon, but Netanyahu faces an October election and a public that backs the strikes. The incentive runs toward more, not fewer. Until that holds, the lower oil prices markets just bet on could reverse.

🚀 SpaceX Cools, and Already Wants $20 Billion More

SpaceX (SPCX) fell for a second straight session yesterday, dropping as much as 10% before trimming the loss to close down more than 3%, after a near-5% slide two days earlier. Even after the pullback, the stock sits well above the $135 price from last week’s record $75 billion initial public offering (IPO), the largest in history. The drop broke a three-day debut rally that had briefly lifted the company’s value past $2.6 trillion, above Amazon and momentarily Microsoft. It came as bankers prepared to pitch investors, as soon as next week, on a bond sale of at least $20 billion, which would be SpaceX’s first investment-grade debt. (Yahoo Finance)

The cooling matters because the IPO carried an unusually large retail allocation, near 30% against the typical 5% to 10%, so ordinary investors hold a big slice and feel every swing. The bond plan reframes the story. A company valued above $2 trillion is lining up at least $20 billion in debt right after raising $75 billion, mostly to refinance a bridge loan due in 2027 while funding an expensive artificial-intelligence push that included a $60 billion all-stock deal for coding startup Cursor. Its filings show a $4.9 billion loss last year and a $4.28 billion loss in the first quarter, with Starlink the only profitable segment. Analyst price targets run from $62 to $401, a spread that shows how little agreement there is on what it is worth. (Investing.com)

Sensei’s Insight: A company this expensive raising a record $75 billion, then lining up $20 billion in debt a week later, shows how much cash the AI plan needs. Starlink is still the only profitable piece. The bond pitch next week is the next real test. As we set out in our playbook, $220 is an area I would sell, and I would look to buy back around IPO prices

💻 Intel Jumps 10% on Trump’s Unconfirmed Apple Claim

President Trump said in an overnight social-media post that Apple has agreed to work with Intel to design and build chips in the United States, and Intel (INTC) closed up about 10% at $133.99, near a record. Neither company confirmed it, and both declined to comment. Trump named no products, volumes, or timeline. The claim echoes a preliminary deal the Wall Street Journal reported in May, after more than a year of talks, for Intel to make some chips for Apple. Apple, which designs its own processors but has them built almost entirely by Taiwan Semiconductor Manufacturing Company (TSMC), rose less than 1%. (CNBC)

For retail investors the useful lesson is to separate a post from a contract. Intel has surged roughly fourfold since the US government took a stake near 10% last year, and yesterday’s move added billions in value on a claim with no terms attached. The substance is further out. Intel’s next manufacturing process, 18A-P, only entered early trial production this week, and analysts expect meaningful Apple volume no sooner than 2027, likely starting with lower-end chips. Bloomberg has reported Apple held parallel talks with Samsung. The real check comes at Intel’s July 23 earnings, when chief executive Lip-Bu Tan is expected to spell out actual foundry customer commitments. (Bloomberg)

Sensei’s Insight: The government owns about 10% of Intel, so the loudest promoter of an unconfirmed Apple deal is also its biggest shareholder. No terms, no timeline, no volume. The figure that matters is what Intel actually discloses at its July 23 earnings.

🛢️ Oil Hits a 3-Month Low on the Iran Deal

Oil fell to its lowest in more than three months yesterday after President Trump and Iranian President Masoud Pezeshkian signed an interim agreement to end their war and reopen the Strait of Hormuz, the narrow Persian Gulf passage that carries about a fifth of the world’s oil. Brent crude, the global benchmark, dropped below $78 a barrel and US crude settled near $76, leaving oil down about 38% from its April peak above $110. The deal calls for a fee-free reopening for at least 60 days, and several tankers have already started crossing again. (Reuters)

Cheaper oil is the clearest disinflation signal in months, and it counts because energy drove the bulk of last month’s jump in consumer prices to 4.2%. The complication is timing. Reopening a chokepoint is not a switch. Shipping executives say clearing the tanker backlog, restoring war-risk insurance, and ramping Gulf production will take weeks, and in some cases months. Goldman Sachs cut its fourth-quarter Brent forecast to $80 from $90 and sees Gulf exports back to pre-war levels by end-July. For now, US gasoline should keep easing into the summer, which feeds straight into the next inflation reading. (CNBC)

Sensei’s Insight: Sentiment moves faster than barrels. The strait can reopen on paper while insurance, mine-clearing and stranded tankers keep real flows slow for weeks. The price drop is already feeding cheaper gasoline, so the next inflation report is where this lands. Oil is starting to look attractive as a buy

⚽ How the World Cup Is Flattering the Jobs Data

Last month’s US jobs report looked strong, with employers adding 172,000 jobs, more than double what economists expected, and unemployment steady at 4.3%. The detail behind it explains the beat. Leisure and hospitality added 70,000 jobs, five times its average over the prior year, with restaurants and bars accounting for most. Economists tie much of that to hiring ahead of the 2026 FIFA World Cup, which kicked off this month across 11 US host cities and runs through mid-July. It was the third straight stronger-than-expected jobs report. (CNBC)

This matters because the Federal Reserve reads strong jobs as a reason to keep rates high, or even to hike, and a temporary tournament bump can make the labor market look healthier than it is. Goldman Sachs estimates the World Cup will add about 40,000 jobs above trend this month and 10,000 next month, then subtract about 15,000 in August as the hiring unwinds. So the same effect flattering the data now will drag on it later. Weekly jobless claims fell to 226,000, which still points to a firm market underneath the noise, but the clean read on the trend only arrives after the final. (Bloomberg)

Sensei’s Insight: Event hiring always reverses. Goldman expects the World Cup to add jobs through July, then cut about 15,000 in August. A soft August payroll print may not signal a weakening economy, only a tournament that packed up. The Fed will read it that way.

Stories You Might Have Missed

📈 A Top Strategist Says the Fed May Hike

Veteran strategist Ed Yardeni said yesterday the Federal Reserve may have to raise interest rates if it is serious about getting inflation back to 2%, the morning after new Fed Chair Kevin Warsh’s hawkish debut. Yardeni has been ahead of the pack: in May he forecast a quarter-point hike as soon as July, a call that looked outlandish when markets put the odds near 5%. It looks less so now that the Fed’s own projections show nine of 18 officials expecting at least one hike this year. Yardeni, who coined the term “bond vigilantes” in 1983 for investors who dump bonds to push back on loose policy, argues that with consumer prices at 4.2% and five straight years above target, simply dropping the easing bias is not enough. He stays bullish on stocks anyway, with a year-end S&P 500 target of 8,250. (Bloomberg)

📦 FedEx and Micron Headline a Big Earnings Week

Two reports worth marking land next week. FedEx (FDX) reports fiscal fourth-quarter results after the close on June 23, its first since spinning off its freight trucking business on June 1, so the new standalone structure and first guidance for 2027 are in focus; as a major shipper, FedEx is treated as a read on the wider economy. Micron (MU) follows on June 24 and is the cleanest gauge of the artificial-intelligence hardware boom, having guided to record revenue near $33.5 billion. The number to watch is its commentary on high-bandwidth memory (HBM), the specialized chips that feed AI servers, where pricing has been the swing factor. Options imply a move of roughly 9% for Micron and about 7% for FedEx once they report. (Yahoo Finance)

🪙 The SEC Inches Toward Blockchain-Based Stocks

The Securities and Exchange Commission (SEC) is preparing a policy that could let crypto companies offer blockchain-based versions of regular stocks, known as tokenized equities, through what officials have described as an “innovation exemption.” The appeal is round-the-clock trading and faster settlement, which could open a new business line for platforms like Coinbase and Robinhood and pressure traditional exchanges. The risk for buyers is that tokenized stocks can lack some of the shareholder rights and protections that come with owning the real shares, and stock exchanges have already urged regulators to rein them in. It is early-stage, but it points at how the basic act of trading could change. (Reuters)

🇬🇧 Bank of England Holds, Two Vote to Hike

The Bank of England kept its main interest rate at 3.75% yesterday in a 7-2 vote, with two policymakers pushing for a hike, as it weighs whether the US-Iran deal and falling oil will cool inflation fast enough to avoid tightening. UK inflation has eased to 2.8% but is expected to climb again this year on still-high energy costs. The pound fell 0.6% to about $1.32, two-year UK government bond yields rose, and the FTSE 100 slipped around 1%. The split mirrors the Federal Reserve’s problem: above-target inflation driven by an energy shock nobody is sure will fade. (Reuters)

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.