Morning Forecast: Friday, 20 February

Markets Await Inflation data as Stablecoin Yields Face Ban

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

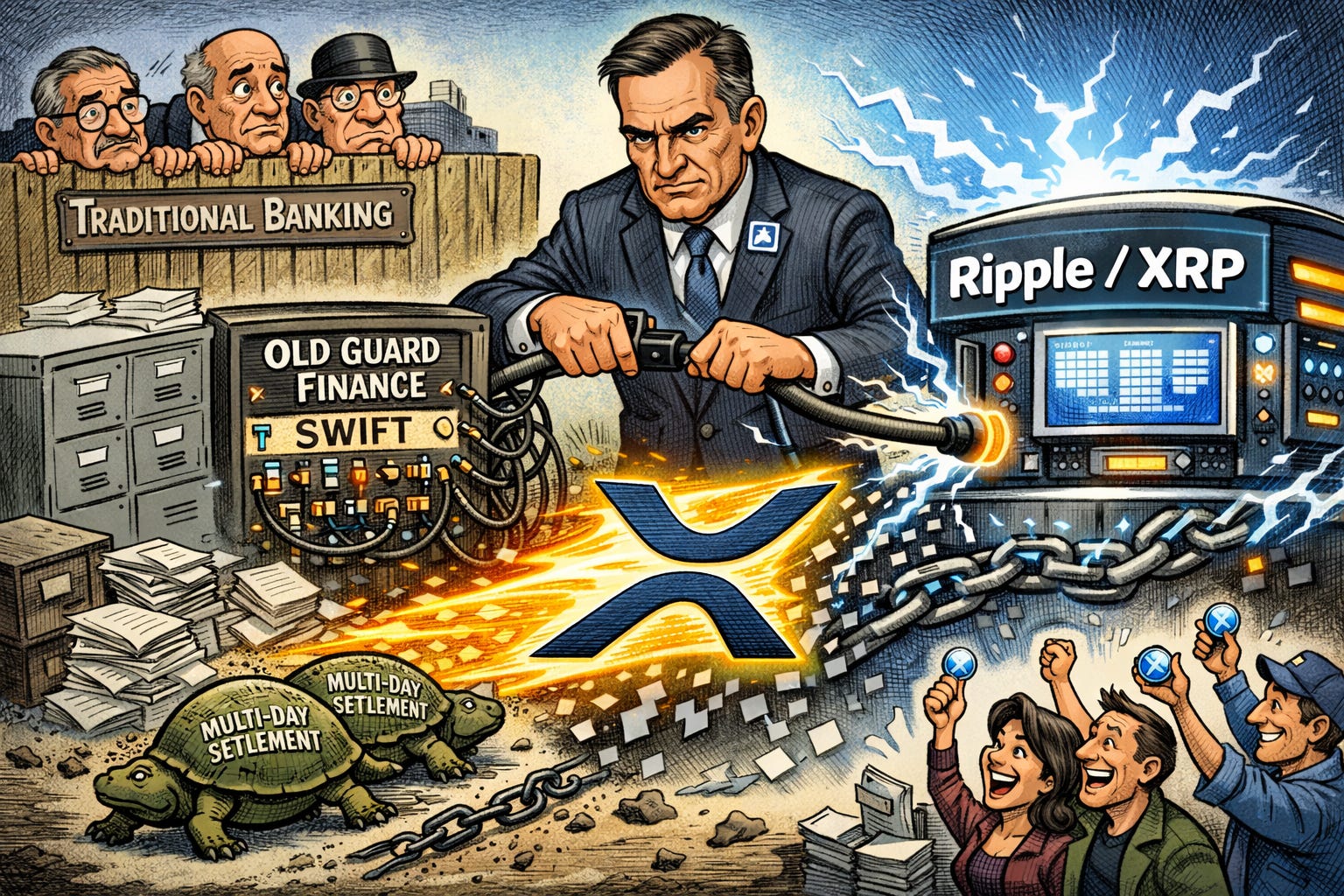

🇩🇪 Deutsche Bank adopts Ripple tech: Digital rails will modernize cross-border payments, slashing costs by removing the need for manual reconciliation.

🤖 AI agents trigger software reset: Investors pivot to semiconductors as autonomous agents threaten the traditional per-seat licensing revenue model.

⚖️ JPM fights Trump debanking suit: The bank seeks federal court transfer, arguing account closures involve regulatory risk rather than political motivations.

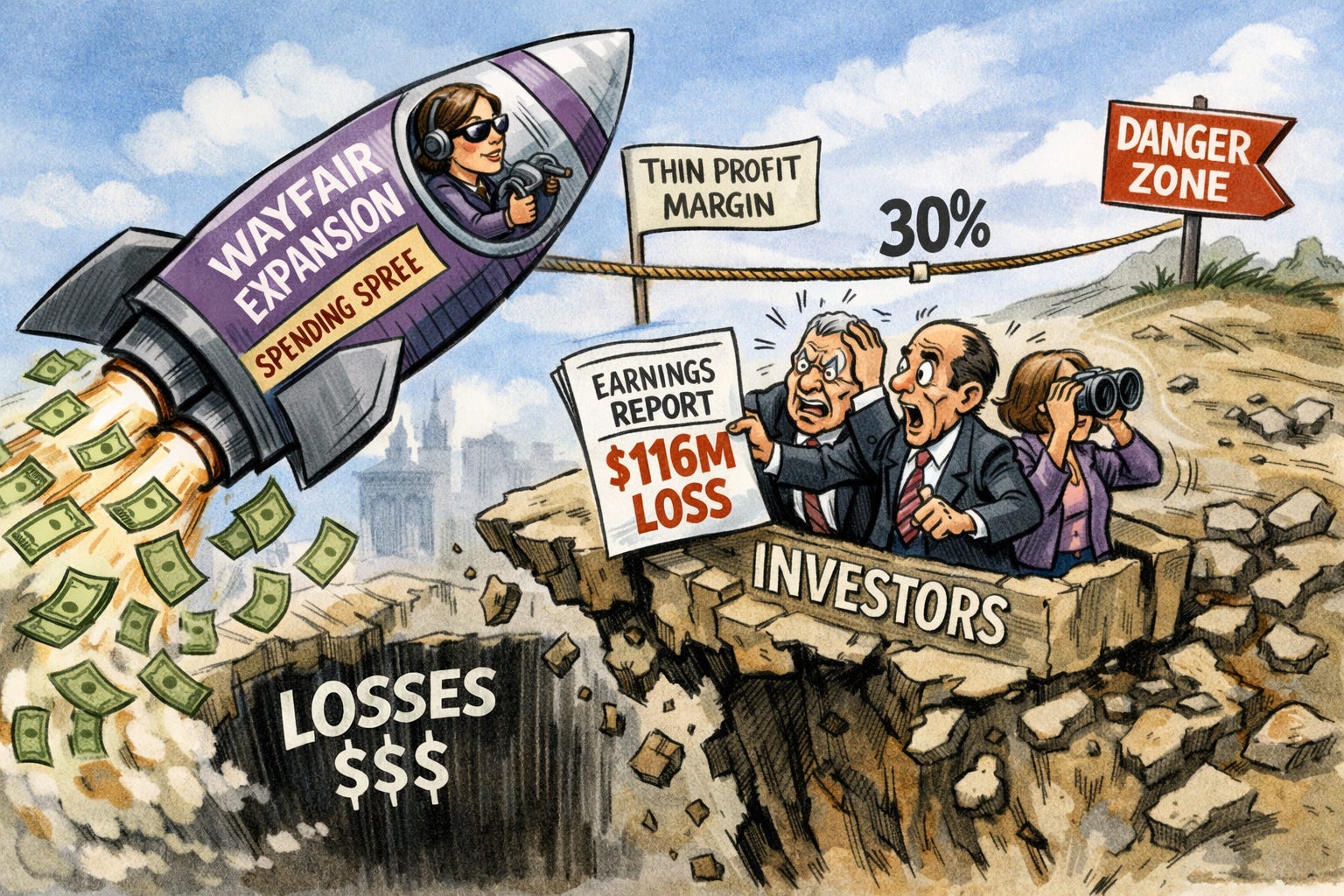

🛋️ Wayfair growth push spooks investors: Shares fell after management signaled they would sacrifice profit margins to aggressively capture furniture market share.

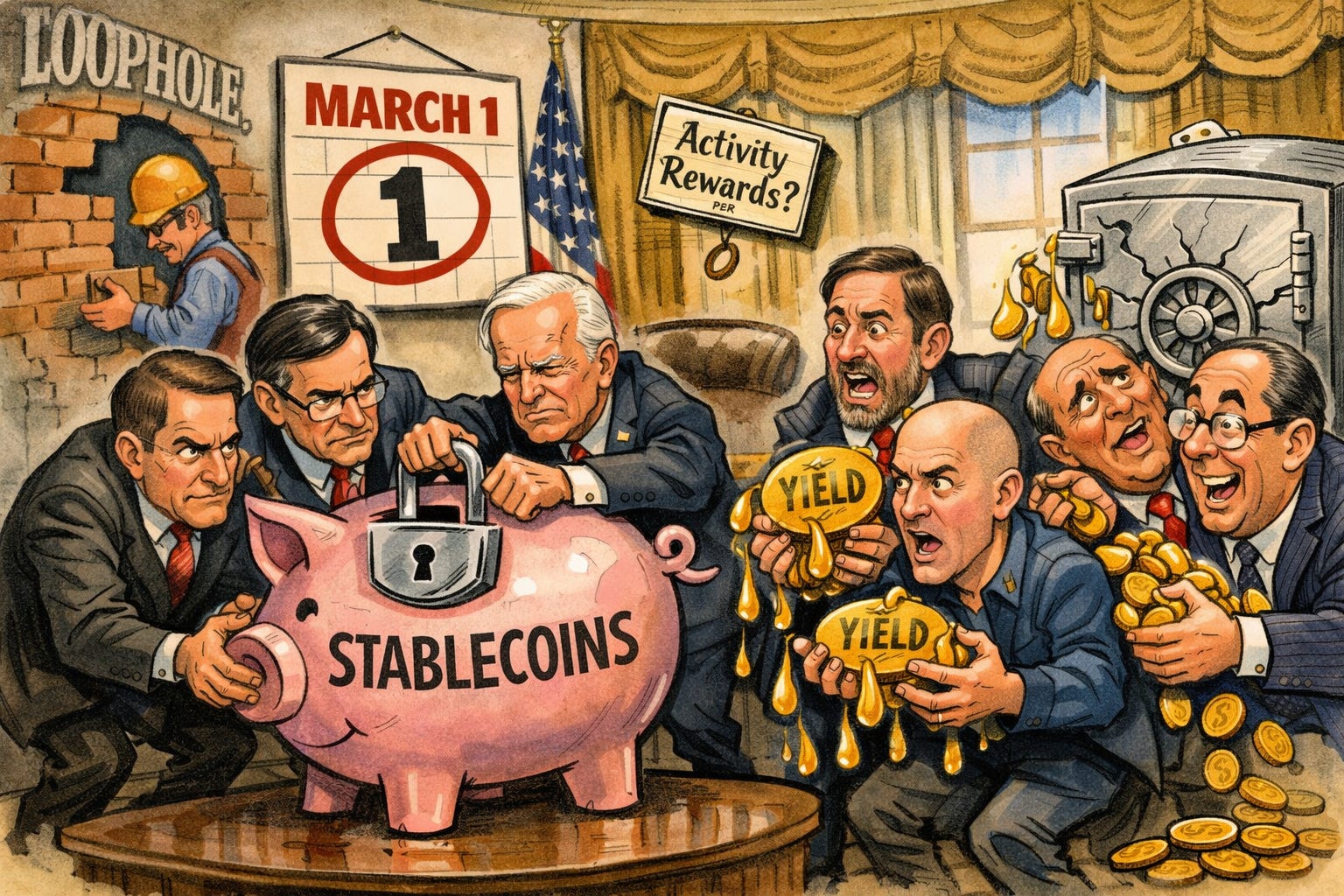

🏦 White House bans stablecoin interest: Proposed rules set a March deadline to prohibit yields, impacting retail investors seeking digital savings rewards.

🔍 PCE and GDP double-header looms: Markets await today’s critical inflation and growth data to determine if June rate cuts remain viable.

🧠 One Big Thing

The Stablecoin Yield Standoff

The White House has seized control of stablecoin negotiations, moving to prohibit interest on idle digital balances while allowing limited rewards for specific user activities. This shift directly addresses bank fears that high-yield crypto products would drain traditional deposits, though industry insiders suggest the banking lobby is motivated more by competitive pressure than actual liquidity risks. To enforce this compromise, federal regulators may gain authority to levy fines of $500,000 per daily violation against firms defying the yield ban. Investors should watch the end-of-month deadline as a pivotal moment for the CLARITY Act, which hinges on whether banks accept these narrow reward exceptions. The outcome will define the future revenue models for major platforms like Coinbase and Ripple.

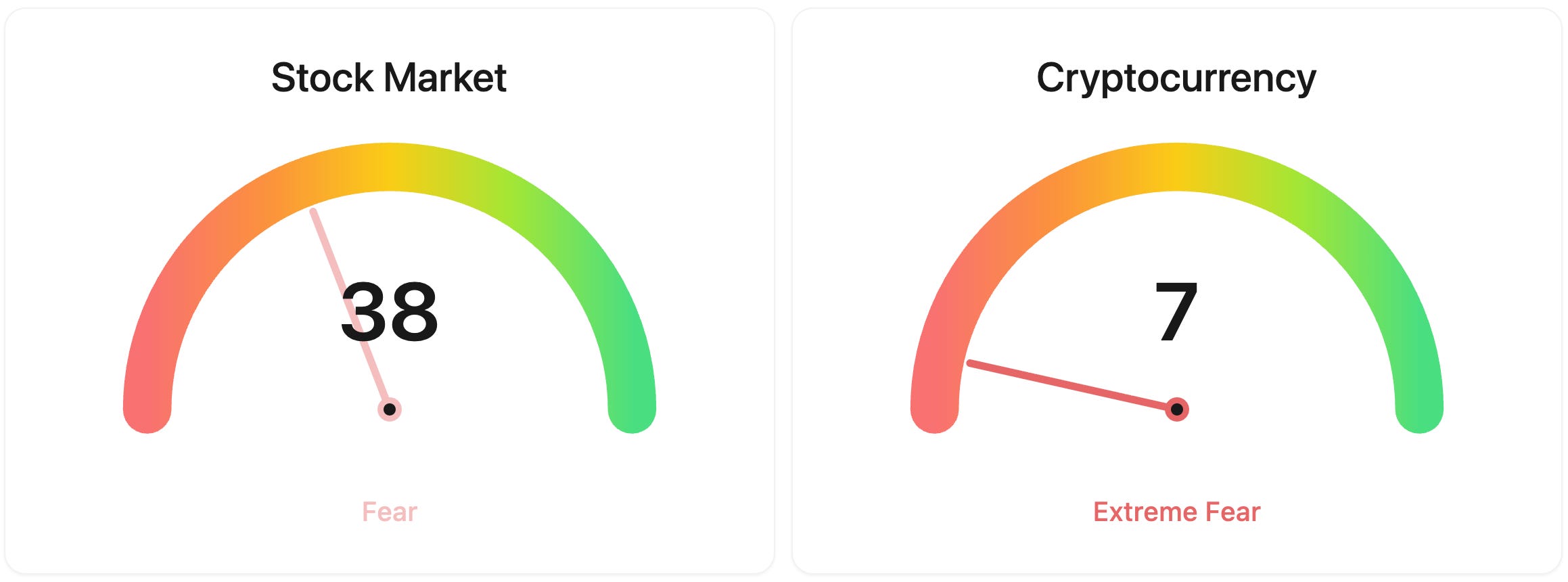

⚖️ Fear & Greed

📉 The Number That Matters

2.9%

Core PCE is projected to hit 2.9% year-over-year for December, marking a potential increase from November’s 2.8%. This critical inflation gauge remains 90 basis points above the Fed’s 2.0% target, keeping the timing of the first rate cut uncertain. The report is coming out soon. In the deep dive section below, you can find the full cheat sheet.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $67,678 (▲ 1.06%)

Ethereum (ETH): $1,950 (▲ 0.07%)

XRP: $1.41 (▲ 0.20%)

Equity Indices (Futures):

S&P 500: $6,862 (▲ 0.09%)

NASDAQ 100: $24,879 (▲ 0.08%)

FTSE 100: £10,690 (▲ 0.26%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.07% (▲ 0.05%)

Oil (WTI): $66 (▼ -0.61%)

Gold: $5,027 (▲ 0.51%)

✅ 5 Things to Know Today

🇩🇪 Deutsche Bank taps Ripple for payment overhaul

Deutsche Bank is reportedly deepening its use of Ripple’s infrastructure to modernize its cross-border payments and FX workflows. While we are still waiting for an official joint press release, reports from German outlet Der Aktionär suggest the bank is taking a lead role in SWIFT’s new blockchain-based ledger alongside 40 other institutions. The goal is to replace slow, multi-day settlement with near-instant transfers. Industry estimates suggest these distributed-ledger rails can slash operational costs by about a third, mainly by removing the need for manual reconciliation between banks. It’s a significant play for Germany’s largest bank, positioning it at the forefront of the technological shift in global finance (Der Aktionär).

This move serves as a massive validation for the Ripple ecosystem and its ability to handle Tier-1 bank requirements. For retail investors, seeing a giant like Deutsche Bank integrate this tech signals that the “old guard” is finally ready to embrace the efficiency of decentralized rails. While the bank is currently focused on the software and messaging side, the integration into such a massive global payment footprint creates a clear path for broader digital asset utility. It shows that blockchain is no longer just an experiment: it’s becoming the core plumbing for the world’s most important financial institutions.

Sensei’s Insight: We should wait for formal validation of the specific terms, but this is undeniably bullish for XRP. If confirmed, Deutsche Bank could be the first major global bank to fully adopt this tech at scale.

🤖 Software’s “Structural Reset” as AI Agents Arrive

Markets just hit the panic button on traditional software. Since Anthropic launched Claude Cowork in January, we’ve seen a violent rotation out of software and into AI semiconductors. The iShares Expanded Tech-Software ETF is down about 30% from its September highs, officially entering bear market territory. Big names like ServiceNow, Atlassian, and HubSpot saw double-digit slides in a single day as investors realized these agents can execute complex workflows without a human ever touching a dashboard. Meanwhile, hyperscalers like Google and Meta are funnelling roughly $750 billion into AI data centers, leaving traditional SaaS vendors in the cold (Barrons).

This isn’t just a bad earnings cycle: it’s a fundamental challenge to the “per-seat” licensing model. Tools like the open-source OpenClaw or Claude Cowork move the user interface from fixed apps to flexible prompts. If an agent can navigate your files, email, and calendar to do the work of a human team, the need for dozens of specialized software subscriptions evaporates. There’s also a massive security overhang. OpenClaw is being called a “security nightmare” because it runs with full system permissions, which explains why companies like CrowdStrike are already building tools to detect and block it. The market is effectively repricing the next decade of software cash flows based on this disruption.

Sensei’s Insight: Watch if “agentic” capabilities start appearing inside existing SaaS platforms to protect their moats. If they don’t, the valuation gap between chipmakers and software providers could widen even further.

⚖️ JPMorgan fights Trump’s $5 billion “debanking” lawsuit

JPMorgan is hitting back against Donald Trump’s $5 billion “debanking” lawsuit. In a new court filing, the bank argues that CEO Jamie Dimon was “fraudulently” included as a defendant to keep the case in Florida state court. JPMorgan wants the fight moved to federal court and eventually New York. Trump claims the bank shuttered his accounts for political reasons after January 6, 2021, and even circulated a secret “blacklist” to other lenders. The bank calls these claims “threadbare,” noting that federal laws often exempt bank officers from the specific Florida consumer statutes Trump is trying to use (Bloomberg).

This litigation tests the boundaries of “reputational risk” policies. Banks often “de-risk” by cutting ties with controversial clients to avoid regulatory friction. If Trump’s team manages to get into discovery, we might get a rare look at how megabanks handle Politically Exposed Persons (PEPs). On the other hand, if JPMorgan successfully moves this to federal court and gets the claims against Dimon tossed, it reinforces the legal shield banks use to fire customers they deem high-risk. For those of us holding bank stocks, political risk is now a permanent factor for firms like JPM and Capital One.

Sensei’s Insight: Watch if the case hits discovery. If internal “blacklist” evidence actually exists, it could force a massive shift in how major U.S. banks manage high-profile, politically sensitive client relationships.

🛋️ Wayfair’s growth push rattles investors

Wayfair reported Q4 2025 results that initially looked like a win: revenue hit $3.34 billion (up 6.9%) and adjusted earnings of $0.85 per share handily beat the $0.69 consensus. However, the stock tanked over 10% because the “clean” numbers told a different story. Under standard accounting (GAAP), Wayfair actually posted a $116 million loss, missing the breakeven results the market expected. This gap was driven by stock-based pay and debt costs, but the real kicker was management’s 2026 outlook. CFO Kate Gulliver signaled that gross margins, currently around 30%, could dip as the company aggressively spends to grab market share in a sluggish furniture market (MarketWatch).

This selloff is a classic “priced for perfection” reversal. After the stock rallied 300% from its lows, investors weren’t looking for excuses to spend more; they wanted proof that profitability was structural. By admitting they might sacrifice margins for growth, Wayfair spooked the broader home-furnishings sector, dragging down peers like Williams-Sonoma and RH. The market is clearly signaling that in an environment of high tariffs and cautious consumers, it values bottom-line stability over the promise of future market dominance. For retail investors, it’s a reminder that “adjusted” profits often mask the cash-burn reality that institutional sellers watch closely.

Sensei’s Insight: Watch the 30% gross margin level like a hawk. If Wayfair dips significantly below that “line in the sand” to buy customers, the stock’s valuation reset could get much uglier.

🏦 White House Targets Stablecoin Yields by March 1

The White House just turned up the heat on the CLARITY Act negotiations, setting a March 1 deadline for a compromise between crypto firms and banks. In a recent closed-door session with heavyweights like Coinbase and Ripple, the administration introduced draft language that flatly prohibits yield on idle stablecoin balances. This isn’t a suggestion: the proposal includes massive civil penalties of up to $500,000 per violation, per day. While the 2025 GENIUS Act already banned issuers from paying interest, this new move aims to close the loophole that allowed third-party exchanges to offer passive rewards to holders (Blockonomi).

For retail investors, this signals a shift in how stablecoins function. The “park and earn” model that many use as a high-yield savings alternative is clearly under fire from banking lobbyists who fear a massive drain on traditional deposits. However, it’s not a total blackout. Negotiators are still debating activity-based rewards, meaning you might still earn for specific actions like lending or payments, just not for sitting on your hands. If this framework passes, it could trade short-term yield for long-term institutional stability. Patrick Witt, the White House’s digital asset lead, suggests that trillions in capital are waiting for this exact kind of regulatory certainty before entering the market.

Sensei’s Insight: Watch the “activity” definitions. If the rules for rewards are too tight, the utility of holding stables drops. If they’re loose, it’s just a rebranding exercise for interest.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: PCE Day Cheat Sheet

December 2025 PCE Inflation + Q4 GDP + Personal Spending: everything you need to know before the number drops.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.