Morning Forecast: Friday 26 June

SpaceX joins a major index today, Bitcoin's biggest options expiry of the year hits, and Apple's price hike drags tech lower.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🚢 Ship Strike Reopens Hormuz Control: A projectile hit a container ship off Oman, lifting oil and halting the UN seafarer evacuation.

🍎 Apple Hikes Prices, Shares Tumble: Apple raised Mac and iPad prices on memory costs, and the stock fell 6%.

📉 AI-Cost Fear Spreads Globally: Memory costs split markets into AI winners and payers; Kospi fell 8% and halted trading.

🚀 SpaceX Enters Russell on Rebalance: FTSE Russell adds SpaceX to its large-cap index today, with about $150 billion set to trade.

📊 GDP Beat Masks Frozen Consumer: First-quarter GDP rose to a 2.1% rate, but consumer spending nearly stalled as inflation topped 4%.

🛢️ Iraq Threatens OPEC Exit: Iraq weighed quitting OPEC over its quota after Hormuz disruption crushed exports well below target.

💾 SK Hynix Files Record Listing: SK Hynix filed for a $29 billion Nasdaq listing, potentially the largest US share sale ever.

💊 Merck KGaA Buys Bio-Techne: Germany’s Merck KGaA agreed to buy Bio-Techne for $11.3 billion, a 36% premium to recent prices.

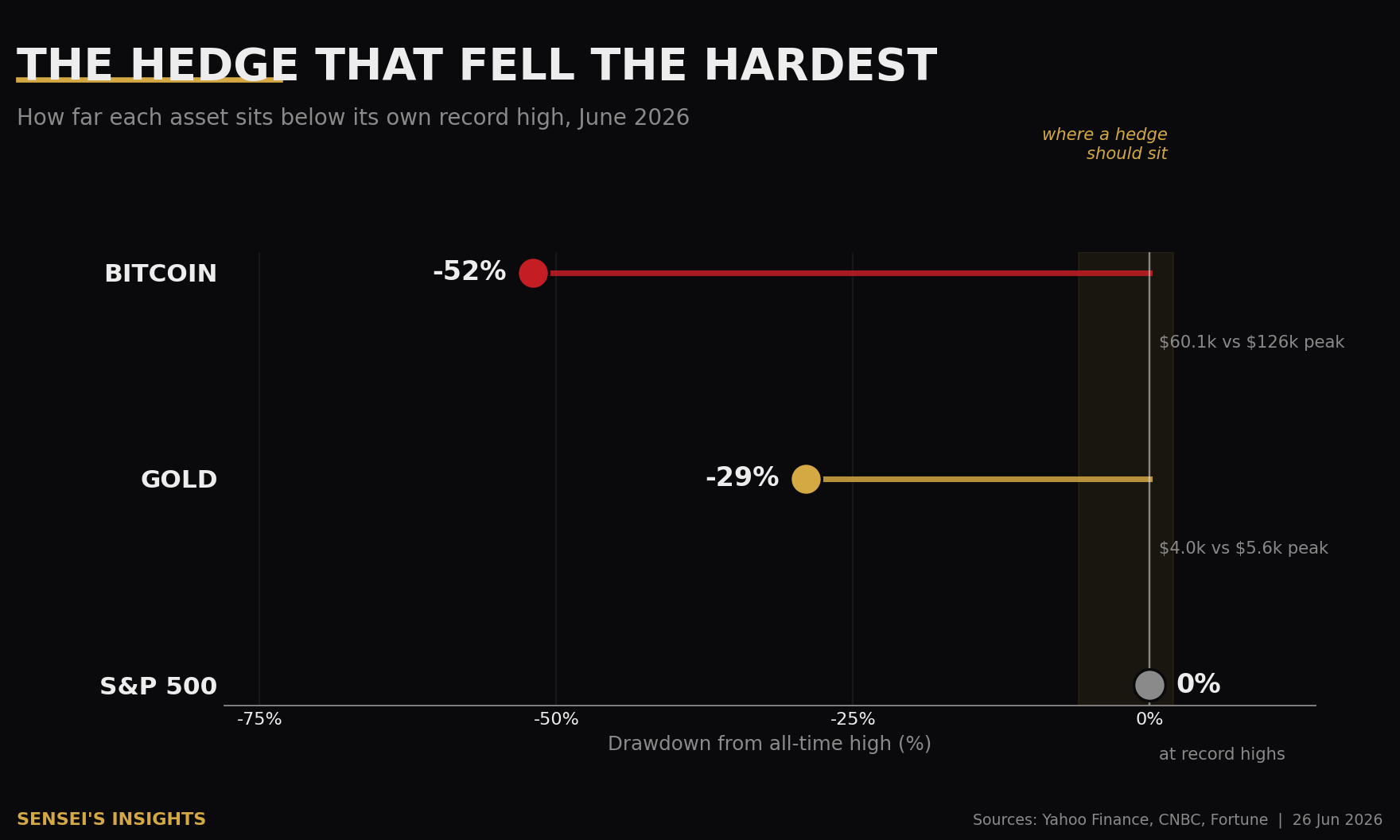

🪙 Bitcoin Breaks Below $60,000: Bitcoin fell to its lowest since October 2024, dropping harder than the assets it should hedge.

📈 Bitcoin Chart Eyes $52,000: The bear flag broke down and the Sensei Trigger flipped bearish, with 52,000 the next downside target.

🧠 One Big Thing

Today's edition has one thread running through it: the AI buildout has stopped being only a demand story and become a cost story that now reaches the Fed. Memory prices have roughly quadrupled in three quarters, forcing Apple's mid-cycle price hike, handing Micron an 85% margin, and helping push inflation to 4.1%. That inflation print is why markets now lean toward a rate hike, not the cuts expected earlier this year. The tension is that the AI trade is feeding the rates trade, and richly valued chip names sit on the wrong side of a hawkish Fed. Watch whether memory pricing cools or the next inflation read locks in the hike.

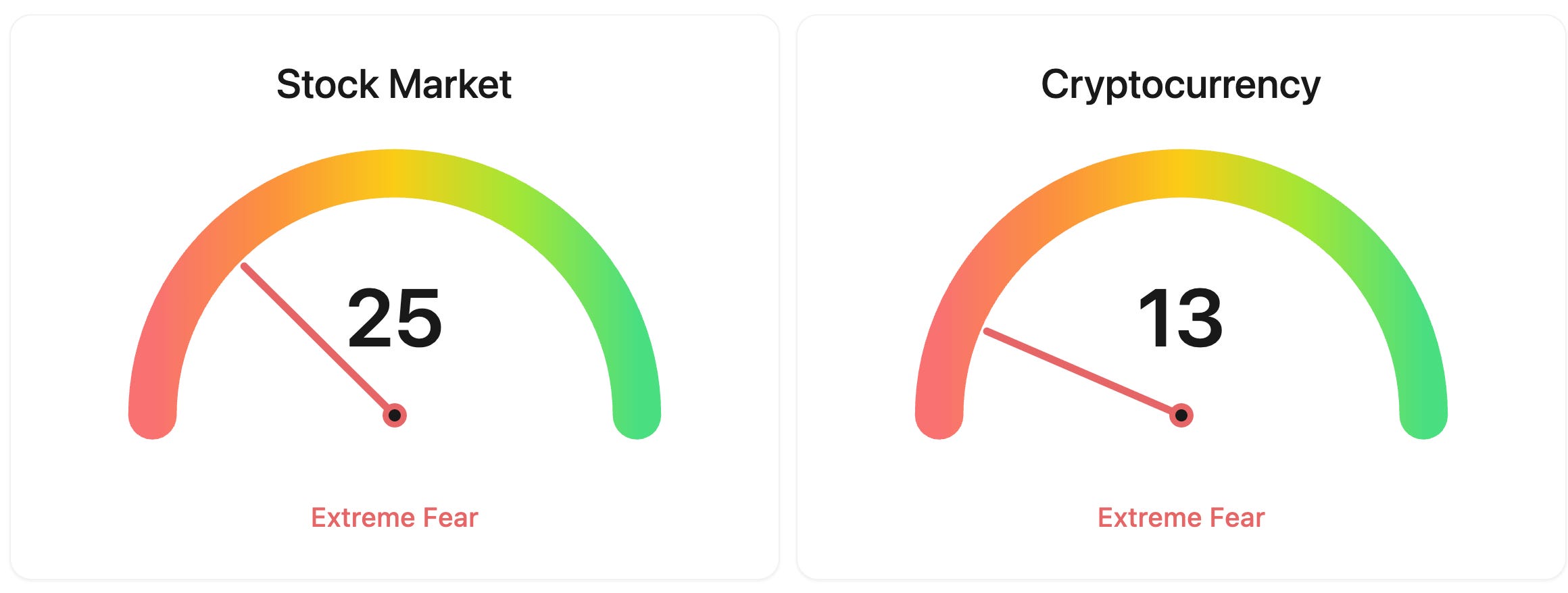

⚖️ Fear & Greed

📉 The Number That Matters

$200

Pricier memory could add about $200 to each iPhone, and with the autumn launch where most of Apple’s revenue sits, that $200 decides whether the AI-cost squeeze hits the product that matters most.

⚔️ Winners vs Losers

Winners

ACAD 0.00%↑: ACADIA Pharmaceuticals jumped in pre-market trading with no specific catalyst identified.

Losers

ON 0.00%↑: ON Semiconductor dropped after agreeing to acquire Synaptics in a $7 billion all-stock deal, with the dilutive structure and questions about its push deeper into physical AI and edge computing weighing on the shares.

TSEM 0.00%↑: Tower Semiconductor slid as high-flying AI chip names gave back gains in a broad semiconductor pullback, cooling after a roughly 75% run over the prior three months.

ARM 0.00%↑: Arm Holdings extended its decline on profit-taking after a 235% year-to-date run, pressured by a recent New Street Research downgrade to Neutral, a wave of executive insider selling, and a sector-wide rotation out of richly valued AI chip stocks.

BABA 0.00%↑: Alibaba Group Holding slid to a 16-month low after Anthropic accused it of illicitly accessing its Claude AI models, with additional pressure from reports that high-profile investors Cathie Wood and Bill Ackman exited their ADR positions.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $59,377 (▼0.54%)

Ethereum (ETH): $1,546 (▼1.23%)

XRP: $1.02 (▼1.65%)

Equity Indices (Futures):

S&P 500: 7,387 (▼0.50%)

NASDAQ 100: 29,371 (▼1.19%)

FTSE 100: 10,440 (▼0.79%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.37% (▼0.36%)

Oil (WTI): $70 (▼2.28%)

Gold: $4,054 (▲0.69%)

Silver: $58.36 (▲0.96%)

Data as of: UK: 12:34 BST / US: 07:34 EDT / Asia (Tokyo): 20:34 JST

✅ 5 Things to Know

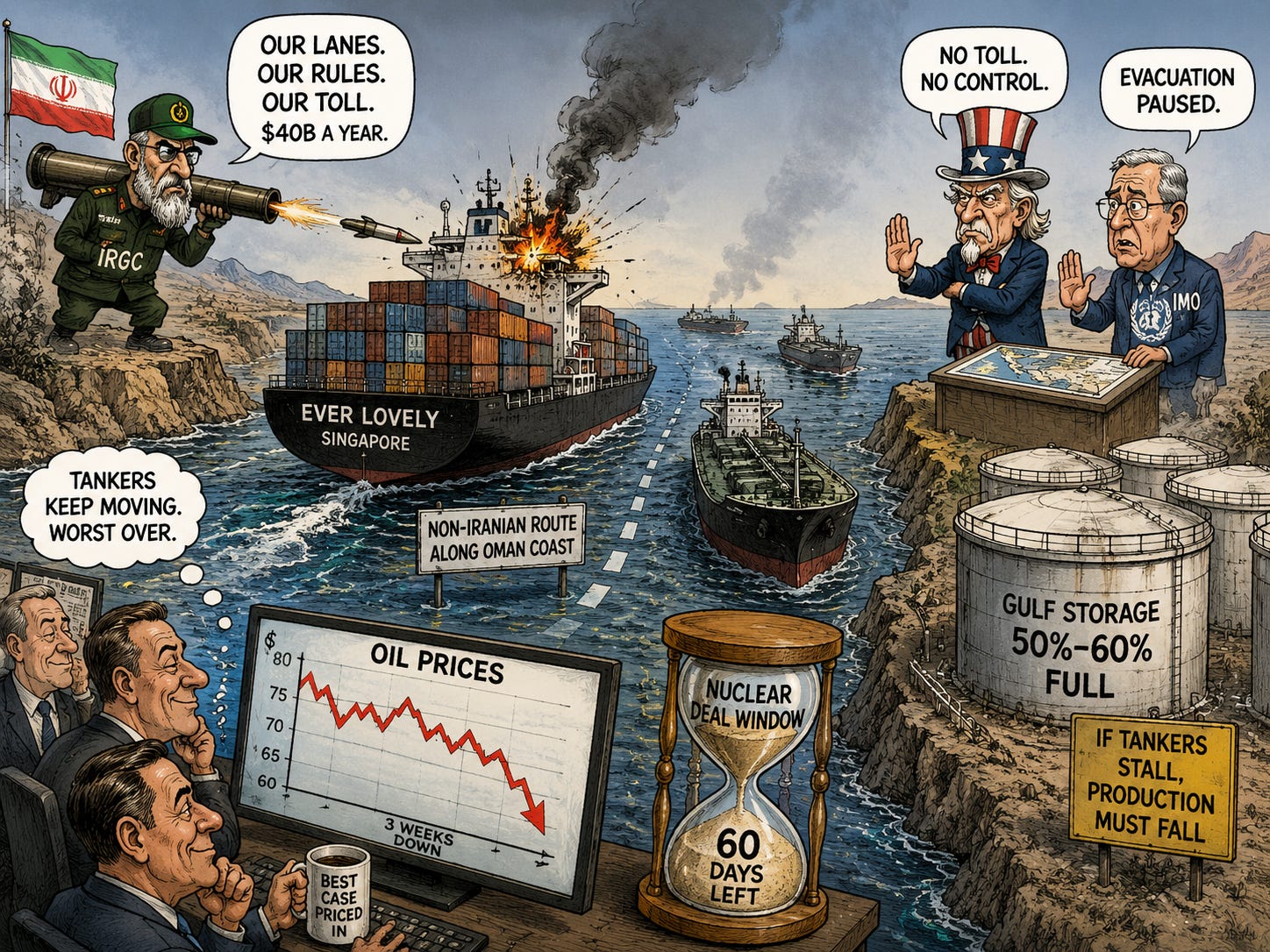

🚢 Ship Attack Jolts Oil, Freezes Hormuz Evacuation

A projectile strike on a Singapore-flagged container ship near Oman on Thursday sent oil higher and forced the United Nations to halt its rescue of vessels trapped in the Persian Gulf. The International Maritime Organization, the UN’s shipping agency, paused an operation to evacuate hundreds of ships and about 11,000 stranded seafarers after the Ever Lovely was hit roughly 14 kilometres off Oman’s coast, damaging its bridge with no injuries reported. Brent crude, the global benchmark, settled up 2.1% at $75.26 a barrel and US crude rose 2.3% to $71.92. After the close, two US officials said Iran’s Revolutionary Guard fired the shot. (Reuters)

The strike matters because it reopened a question markets thought was closing: who controls the Strait of Hormuz, the narrow channel that carried about a fifth of the world’s oil before the war. Iran wants ships to use only its own designated lanes and has floated charging up to $40 billion a year for “security” services; the US rejects any toll, and the IMO had routed traffic along Oman’s coast to skirt Iranian waters. The attacked ship was on that non-Iranian route. By Friday morning the spike had largely faded, with Brent back below $75 as tankers kept crossing, but Iran and Oman are now set to negotiate the strait’s future control. (Reuters)

The fragility is the point. The US-Iran deal opened only a 60-day window to settle the nuclear dispute, and Gulf storage tanks sit 50% to 60% full. If inbound tanker traffic doesn’t recover, producers will have to cut output, pushing a full supply recovery into 2027. For now the market is betting the worst is over, with crude heading for a third straight weekly drop even after a ship took fire.

Sensei’s Insight: Oil has fallen three weeks running even with a vessel hit, because tankers keep moving and traders are pricing the best case. The figure that decides the next move is inbound traffic. Gulf storage is already 50% to 60% full, and stalled shipments force production cuts.

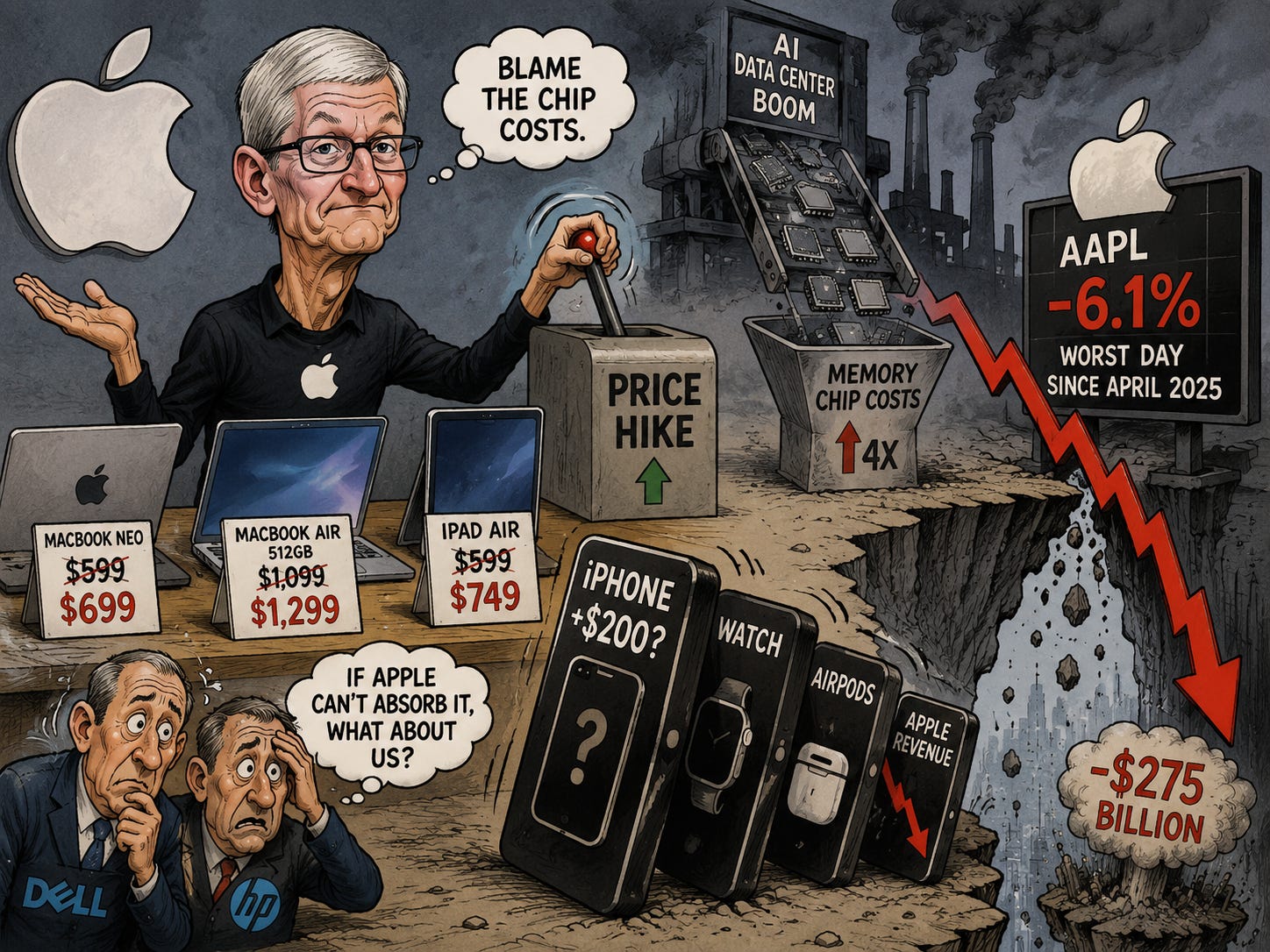

🍎 Apple Hikes Mac and iPad Prices, Stock Drops 6%

Apple did something it almost never does: raise prices in the middle of a product cycle. On Thursday it lifted US prices on MacBooks, iPads and several other devices, blaming a surge in memory and storage chip costs driven by the AI data-center boom. The entry MacBook Neo went from $599 to $699, a MacBook Air with 512 gigabytes of storage from $1,099 to $1,299, and the iPad Air from $599 to $749. The iPhone, Apple Watch and AirPods were left untouched for now. Investors punished the move: Apple fell 6.1%, its worst day since April 2025, erasing about $275 billion in market value. (CNBC)

The hike matters because Apple runs the best supply chain in consumer tech, so if it can’t absorb these costs, weaker rivals like Dell and HP may have to raise prices even more. Memory chips, the DRAM that runs apps and the NAND flash that stores files, have roughly quadrupled in cost over three quarters as suppliers divert capacity to AI servers. That turns the AI boom into a consumer-inflation story. The bigger risk sits ahead: analysts estimate pricier components could add about $200 to each iPhone, and Apple’s autumn iPhone launch is where the squeeze would hit the bulk of its revenue. (Reuters)

Sensei’s Insight: The iPhone is the domino that counts. Apple left it, the Watch and AirPods out of this round, but components could add roughly $200 a phone, and the autumn launch is where memory costs meet most of Apple’s sales. Watch whether buyers absorb it or balk.

📉 Futures Slide as AI-Cost Fear Spreads Worldwide

Wall Street is splitting along a new line: who profits from AI versus who pays for it. Stocks closed mixed Thursday, with the Dow up 0.14% to 51,920, the S&P 500 flat, and the Nasdaq down 0.46% for a fourth straight loss, its longest losing streak since February. Memory maker Micron soared 15.7% on record results, reporting quarterly revenue of $41.5 billion and guiding to roughly $50 billion next quarter. But Apple’s 6% drop and softness in Nvidia, Microsoft and Alphabet dragged the index. The tension underneath: Micron’s record 85% gross margin comes straight out of the costs its customers, Apple among them, now have to pay. (Reuters)

That worry went global overnight, and it points to a rough open. By early Friday, S&P 500 futures were down 0.8% and Nasdaq 100 futures off 1.6%. In Asia, South Korea’s Kospi plunged more than 8% and tripped a circuit breaker that halted trading, while Japan’s SoftBank sank more than 11%, both dragged down by memory names Samsung and SK Hynix. Adding to the unease, a report that OpenAI may delay its IPO into next year because it can’t lock in demand at a $1 trillion valuation rattled the AI complex. With inflation back above 4% and a more hawkish Federal Reserve under new chair Kevin Warsh, money is moving out of crowded tech and into industrials, healthcare and financials. (CNBC)

Sensei’s Insight: Micron’s record 85% margin is the clearest sign the money is moving from device makers to chipmakers. The question now is whether the AI spenders, Nvidia and the cloud giants, can hold up as the market starts pricing the cost of the buildout, not just the demand.

🚀 SpaceX Lands in Russell 1000 on a $150 Billion Day

One of the year’s busiest trading days lands today, when FTSE Russell completes its semi-annual rebuild of the Russell US indexes after the close. Reconstitution means the index provider re-ranks every US company by size and resets which belong in the large-cap Russell 1000 versus the small-cap Russell 2000; every fund tracking those indexes then has to buy the additions and sell the deletions at the 4 p.m. close to match the new list. The headline addition is SpaceX, fast-tracked into the Russell 1000 just weeks after its record June 12 IPO. Analysts at Stephens estimate nearly $150 billion will change hands, making this a key liquidity day. (Reuters)

For ordinary investors, this runs on autopilot: anyone holding a Russell 1000 fund such as IWB or IWF will simply own SpaceX on Monday with no action needed. The deeper change is the new fast-entry rule, written for megacap listings like SpaceX, OpenAI and Anthropic, which lets giant IPOs into the index after just five trading days instead of waiting months. S&P Dow Jones declined to follow, keeping its profitability and 12-month seasoning requirements, so SpaceX won’t reach the S&P 500 until at least 2027. That matters because S&P 500 funds, the kind most Americans hold in retirement accounts, can’t buy it yet, leaving Russell and Nasdaq trackers as the main forced buyers. (Yahoo Finance)

Sensei’s Insight: SpaceX is already more than 30% below its June peak and S&P 500 funds can’t touch it until 2027, so today’s Russell and Nasdaq buying is most of its mechanical demand for now. Watch the last few minutes before the 4 p.m. close for outsized swings in added and dropped names.

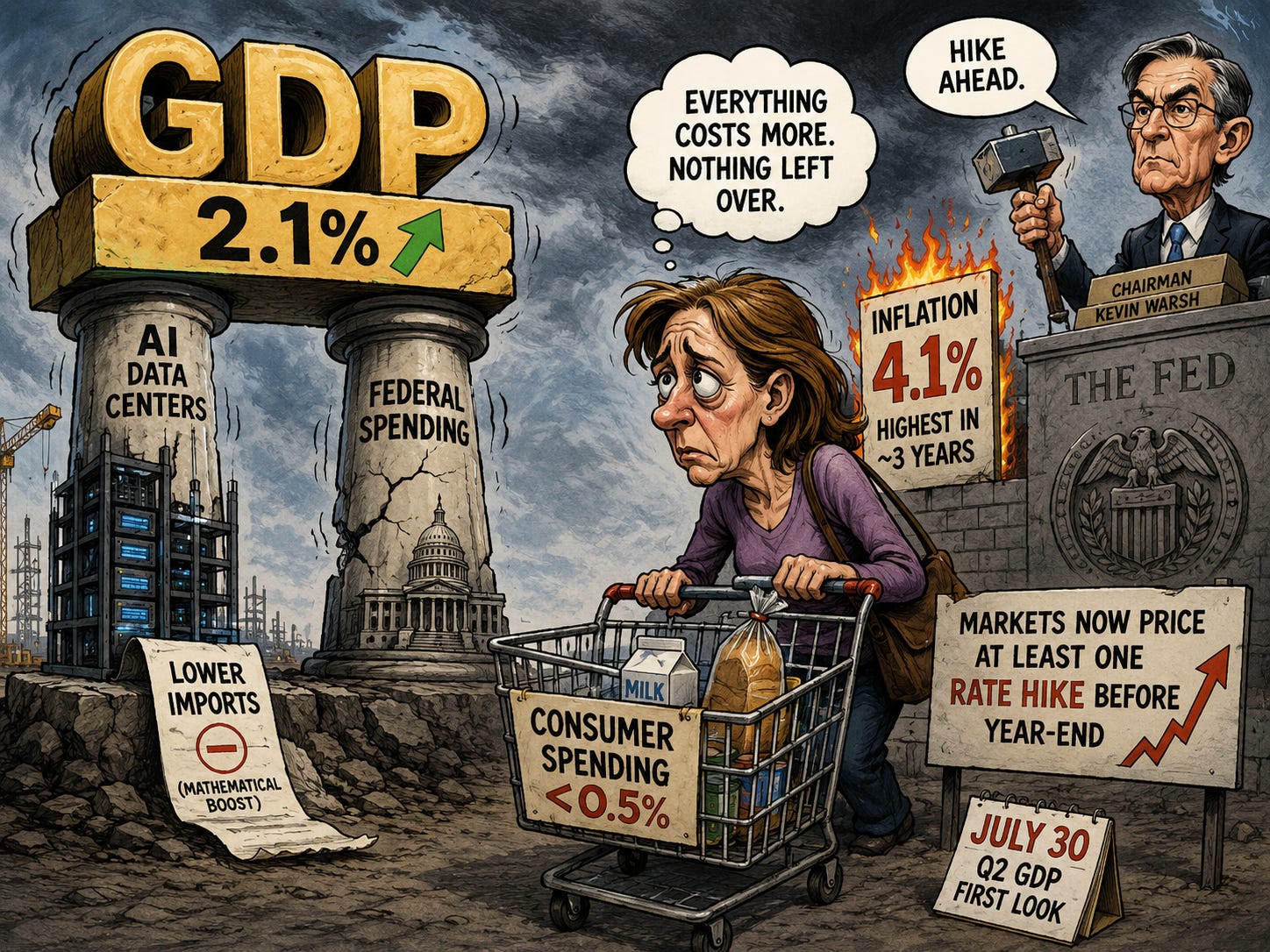

📊 Strong GDP Headline Hides a Stalling Consumer

The economy looked stronger on paper and weaker underneath. The government’s final reading of first-quarter gross domestic product, the total value of everything the economy produces, was revised up to a 2.1% annual rate from 1.6%, beating forecasts. But the upgrade was mechanical: it came almost entirely from lower imports, which lift GDP by subtraction rather than from stronger demand. Consumer spending, more than two-thirds of the economy, was cut to a crawl of less than half a percent, down from 1.4%. The same morning, the Federal Reserve’s preferred inflation gauge showed prices up 4.1% in May, the highest in about three years. (Reuters)

The mix matters more than the headline, because a 2.1% print propped up by an import quirk, paired with a near-frozen consumer and 4% inflation, is a weak hand for the Fed. Growth is leaning on two narrow pillars, AI data-center construction and federal spending. With inflation accelerating, markets now price at least one quarter-point rate hike before year-end under new Fed chair Kevin Warsh, a reversal from the cuts investors expected earlier this year. Consumer-facing stocks are the most exposed if households keep pulling back; the first read on second-quarter growth arrives July 30. (Reuters)

Sensei’s Insight: Consumer spending nearly stalled while inflation runs above 4%, the squeeze that has historically come before weaker spending on non-essentials. The Fed’s next move now leans toward a hike, not the cut markets wanted, with the first look at second-quarter growth due July 30.

Stories You Might Have Missed

🛢️ Iraq Threatens to Quit OPEC Over Its Quota

Iraq, OPEC’s second-largest producer and a founding member, has weighed leaving the cartel if it isn’t allowed to pump more oil, sources said Thursday, though its oil ministry later called an exit not the government’s official position. The threat reads as leverage: the Iran war and Hormuz disruption have crushed Iraq’s exports, with May output at just 1.48 million barrels a day against a quota of 4.378 million. It follows the United Arab Emirates’ departure on May 1. If members keep peeling off, OPEC loses its grip on supply, which over time points to more oil and softer prices, good for drivers and inflation, hard on energy producers. (Reuters)

💾 SK Hynix Files for Record $29 Billion Nasdaq Listing

SK Hynix, the world’s second-largest memory chipmaker and the dominant supplier of the high-bandwidth memory that powers AI servers, filed to raise up to about $29 billion in a US listing on Nasdaq, targeting a July 10 debut. At the top of its range it would be the largest such offering ever, beating Alibaba’s $25 billion in 2014. It is the same AI memory boom squeezing Apple and minting record profits at Micron, now giving US investors a second pure-play way to bet on it. SK Hynix shares jumped about 12% Thursday and are up more than 300% this year. (CNBC)

💊 Merck KGaA to Buy Bio-Techne for $11.3 Billion

Germany’s Merck KGaA, no relation to America’s Merck, agreed to buy Minnesota life-sciences tools maker Bio-Techne for $73 a share in cash, valuing it at about $11.3 billion. The price is a 36% premium to Bio-Techne’s one-month average and the German group’s biggest deal in over a decade. It signals that strategic buyers are using depressed valuations to scoop up research-tools companies after the post-Covid biotech slump. Bio-Techne shares jumped toward the offer, rising as much as 19% Thursday, while Merck KGaA rose about 5% in Frankfurt. The deal is expected to close in late 2026 or early 2027. (Reuters)

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

Bitcoin Below $60,000, and the Myth of Digital Gold

Bitcoin slipped under $60,000 this week, its lowest level since October 2024 and down more than half from the $126,000 record it set last autumn. In the same stretch, US stocks printed fresh all-time highs and even gold, the asset Bitcoin was meant to replace, held up far better. Today brings the biggest options expiry of the year. The story underneath the price is more interesting than the price itself: the asset sold as a hedge just fell harder than the things it was supposed to protect you from.

What happened

Bitcoin traded around $60,100 on Friday after sliding below $60,000 on Thursday, the weakest it has been since October 2024 (CNBC, Yahoo Finance). From its $126,000 peak in October 2025, that is a drop of roughly 52 percent (Yahoo Finance).

Now hold that next to everything else. The S&P 500 closed above 7,600 earlier this month, its 24th record high of 2026, and is up about 11 percent on the year (Fortune). Gold, after a wild run to about $5,600 in January, has cooled to roughly $4,000, down around 29 percent from its high (Yahoo Finance). So in 2026 the riskiest-looking thing on the board, Bitcoin, has fallen the most, and the boring metal has fallen less.

A hedge is not supposed to fall the most

This is the part worth sitting with. Bitcoin was marketed for a decade as “digital gold,” an asset that moves on its own clock, immune to central banks, a place to hide when everything else wobbles. The test of that claim is simple: in a risk-off moment, a real hedge falls less than stocks, or it rises. Bitcoin did the opposite. It fell more than stocks and more than gold.

The reason is who actually owns it now. When US spot Bitcoin ETFs launched in January 2024, they made it trivial for institutions to buy. They also made it trivial to sell. The marginal buyer stopped being a true believer holding through anything and became a tactical allocator with a risk model. To that allocator, Bitcoin is simply a high-volatility position to trim when nerves fray. That is why it trades like a leveraged version of the Nasdaq rather than like a vault. The “uncorrelated” story was always a story about who held the coins, and the holders changed.

Today’s $10.6 billion expiry

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.