Morning Forecast: Friday, 27 March

Five Weeks of Losses, 4.2% Inflation, and Every Hedge Is Broken.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🕊️ Trump Pauses Iran Strikes: Markets ignore the delay as energy shortages worsen and oil prices stay high.

🚀 SpaceX Targets Record IPO: Musk plans a record valuation while reserving 30% of shares for retail.

💰 Big Oil Profits Surge: Energy firms reap record gains as US shale replaces Middle Eastern supply.

📉 Market Selloff Intensifies: Stocks enter correction territory as inflation forecasts eliminate hopes for 2026 rate cuts.

☢️ Three Mile Island Delayed: Grid hurdles push the restart to 2031; threatening a Microsoft power deal.

🔍 Analyzing the Iran Conflict: US forces weigh seizing Kharg Island as energy driven inflation risks global stagflation.

🧠 One Big Thing

Markets Stop Buying the Diplomacy

Financial markets are ignoring diplomatic extensions in the Iran conflict because the Strait of Hormuz remains physically closed to oil traffic. This bottleneck has detached asset prices from political rhetoric, fueling a fifth straight week of losses for US equities. Traditional safety plays like gold and bonds are failing to protect portfolios while 2026 inflation projections climb to 4.2 percent. Persistent energy costs have effectively eliminated expectations for interest rate cuts this year. Consequently, the Federal Reserve cannot ease policy without further stoking price increases. Meaningful market recovery now hinges on confirmed commercial shipping flows rather than political headlines.

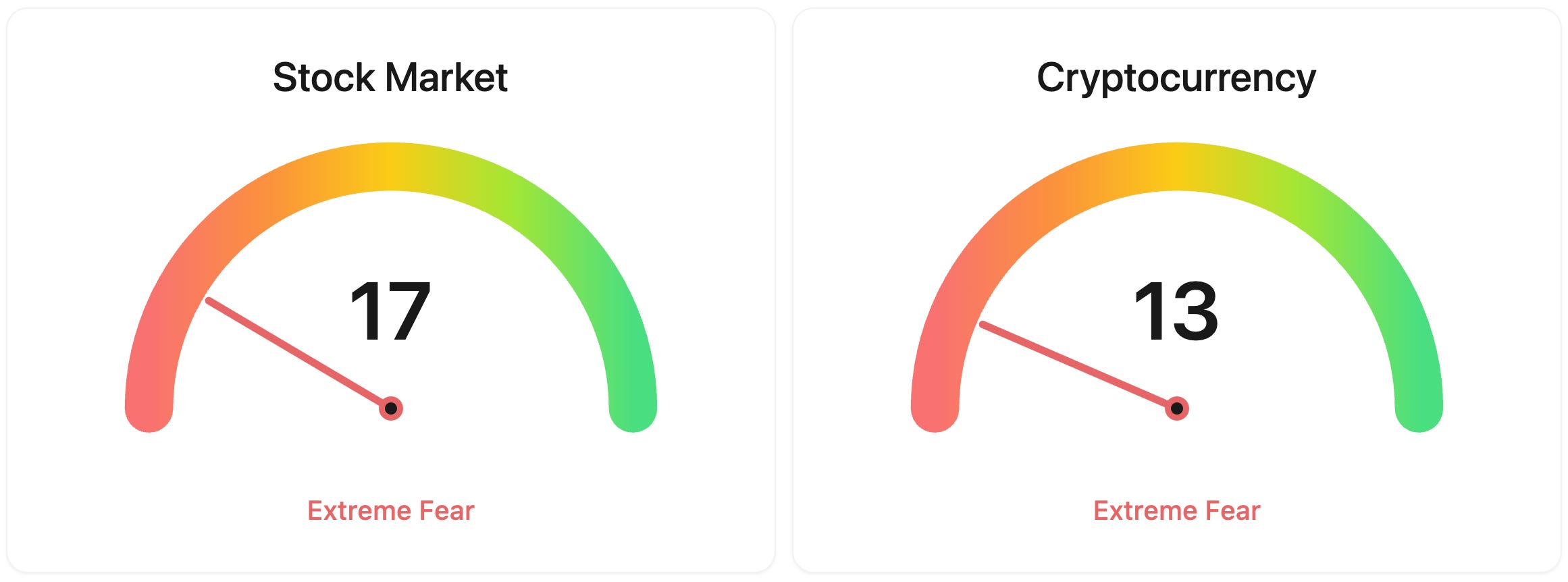

⚖️ Fear & Greed

📉 The Number That Matters

4.2%

The OECD projects US inflation will reach 4.2% in 2026, significantly higher than the Federal Reserve's 2.7% estimate. This macro backdrop has effectively eliminated the probability of interest rate cuts throughout the remainder of the year.

⚔️ Winners vs Losers

Winners

U 0.00%↑: Unity Software shares surged after the company raised its Q1 guidance well above prior targets, now projecting revenue of $505 to $508 million versus earlier guidance of $480 to $490 million, with adjusted EBITDA guidance lifted to $130 to $135 million, driven by 15% sequential growth in its Vector advertising platform.

Losers

DTCX 0.00%↑: Datacentrex shares tumbled after the digital infrastructure company priced a $20.17 million public offering at $2.00 per share, a steep discount to its prior closing price of $3.09, stoking dilution concerns among investors.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $66586 (▼ -3.22%)

Ethereum (ETH): $1993 (▼ -3.25%)

XRP: $1.34 (▼ -1.81%)

Equity Indices (Futures):

S&P 500: $6449 (▼ -0.61%)

NASDAQ 100: $23640 (▼ -0.65%)

FTSE 100: £9893 (▼ -0.51%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.46% (▲ 1.09%)

Oil (WTI): $97 (▲ 3.38%)

Gold: $4412 (▲ 0.70%)

Silver: $68.02 (▼ -0.10%)

Data as of: UK (GMT) 11:15 / US (EST): 07:15 / Asia (Tokyo): 20:15

✅ 5 Things to Know Today

🕊️ Trump Blinks Again, and Markets Are Done Caring

Trump extended his pause on striking Iran’s energy infrastructure by a further 10 days, pushing the new deadline to April 6, on the grounds that Iran requested the delay. He said 10 oil tankers had passed through the Strait of Hormuz as a “present” to the United States, and insisted that talks were going “very well.” Iran’s response made those claims difficult to reconcile with reality. Tehran formally rejected the US 15-point peace plan outright and submitted its own five-point counter-proposal, the centrepiece of which is a demand that Iran be granted formal authority over the Strait of Hormuz. Day 28 of the war shows no operational change: strikes on Isfahan intensified overnight, Israeli forces killed the head of the Iranian Revolutionary Guard’s navy, and the Strait remains effectively closed to commercial oil traffic (Bloomberg).

The market’s reaction to the extension tells the real story. Two weeks ago, Trump’s first pause sent Brent crude down 11% and stocks surging. Today, S&P 500 futures are down 0.2% despite the announcement, with Brent still trading near yesterday’s close of $108.01 a barrel. Markets have seen enough of these extensions to stop pricing peace into asset prices. The S&P 500 is on track to close out its fifth consecutive losing week. Iran’s insistence on formal sovereignty over Hormuz is a non-starter for any deal the US could credibly accept, which means the gap between Trump’s public optimism and the actual state of negotiations may be wider than at any point since the war began (CNN).

While Washington and Tehran trade proposals and counter-proposals, the human cost of a closed strait is becoming acute elsewhere. The Philippines today became the first country in the world to declare a national state of emergency over energy supply, with President Ferdinand Marcos Jr. warning of “imminent danger” to the country’s energy stability. The government estimates it has roughly 40-45 days of petroleum supply remaining. Protests erupted outside the Presidential Palace in Manila, with jeepney drivers (operators of the country’s distinctive passenger minibuses) unable to afford fuel. Thailand hiked gasoline prices between 14% and 22% overnight. India’s state-owned refiners purchased liquefied petroleum gas from Iran for the first time in nearly eight years, a sign of how fundamentally supply chains are being rerouted. Unlike the US or Europe, which hold strategic reserves capable of bridging a supply disruption, most Southeast Asian economies run on rolling imports with no meaningful buffer. The clock is ticking in a way that diplomatic deadlines are not.

Sensei’s Insight: Two weeks ago, an extension sent oil down 11% and stocks soaring. Today the same move barely registers. Markets are developing immunity to deadline extensions without verified Hormuz traffic. The bar for a real relief rally has quietly shifted: only confirmed commercial tanker flows will move the needle now.

🚀 SpaceX Is About to Change the IPO Market Forever

Bloomberg confirmed last night that SpaceX is scheduling investor briefings for April as it prepares to file what could be the largest initial public offering (IPO) in financial history. Reports suggest the company could file a confidential prospectus with the Securities and Exchange Commission (SEC) as soon as this week, targeting a valuation of around $1.75 trillion and a raise of up to $75 billion. For context, Saudi Aramco’s record-setting 2019 IPO raised approximately $29 billion, making SpaceX’s target more than two and a half times larger. Morgan Stanley and Goldman Sachs are reportedly competing to lead the underwriting. In an unprecedented move, Elon Musk is considering reserving up to 30% of the offering for retail investors, compared to the typical 5-10% allocation, which could give everyday investors rare access to a marquee tech debut (Bloomberg).

SpaceX is no longer purely a rocket company. Its February 2026 merger with Musk’s artificial intelligence venture xAI, valued at $1.25 trillion, transformed the combined entity into what analysts are calling a “space AI infrastructure” business. The Starlink satellite internet division is approaching 9.2 million subscribers and generated more than $10 billion in revenue in 2025, with projections for 2026 ranging between $15.9 billion and $24 billion. SpaceX also commands roughly 80% of the commercial rocket launch market. Space sector stocks have already responded: AST SpaceMobile and Rocket Lab both jumped around 10% earlier this week on initial IPO reports, and Firefly Aerospace climbed 16%. The SEC is scrutinising the xAI integration as part of the filing review, one of the reasons a February filing was delayed (CNBC).

Sensei’s Insight: The 30% retail allocation is the headline within the headline. A typical IPO gives retail investors 5-10%, with the rest going to institutions who often flip shares immediately after listing. If this holds, it sets a precedent that could permanently shift how high-profile public offerings treat small investors. Watch whether Musk follows through on that promise.

💰 Big Oil Is Having Its Best Quarter Since the 1970s

The financial details of Big Oil’s war windfall are becoming concrete. Brent crude closed at $108.01 a barrel yesterday, up roughly 49% from January’s average of $65, after Iran’s rejection of the US ceasefire proposal crushed the diplomatic optimism that had briefly lifted markets earlier in the week. The S&P 500 energy sector has hit an all-time record high, up 25-32% year-to-date and the only major sector in positive territory for Q1. Reuters calculated that ExxonMobil’s five million barrels per day of production likely generated approximately $5.1 billion in additional revenue in March alone, while Chevron’s four million barrels per day yielded around $4 billion extra. Six analysts revised Chevron’s first-quarter earnings-per-share forecasts upward by roughly 40% on average. “The first quarter is going to be phenomenal for these companies. I don’t think there’s any way around that,” said Leo Mariani of Roth Capital Partners (Reuters).

The winners and losers within energy are not uniform. US and Canadian shale producers, with no Middle East exposure, are the biggest beneficiaries, while oilfield-service companies like Schlumberger face revenue pressure as Gulf field activity slows. Asian liquefied natural gas (LNG) prices, which reflect the cost of natural gas shipped in liquid form at extremely low temperatures, have surged 143% since the war began after QatarEnergy declared force majeure (a legal mechanism that suspends contract obligations due to extraordinary events) on all its exports. Rystad Energy estimates US shale producers could collectively earn an additional $63 billion if oil averages $100 a barrel through 2026. Goldman Sachs warns Brent could exceed its 2008 all-time record of $147 if Hormuz flows remain near zero for 10 weeks, though December crude futures trading at around $79.70 suggest markets still expect a resolution (Reuters).

Sensei’s Insight: The LNG trade is the sleeper story inside the Big Oil windfall. US LNG exporters like Venture Global, up roughly 100% since January, are capturing Asian premium prices that were unthinkable six months ago. If Hormuz stays closed into summer, the US may permanently displace Qatar as Asia’s primary LNG supplier. That is a structural shift, not just a war premium.

📉 Five Weeks of Losses, 4.2% Inflation, and Nowhere to Hide

US equity markets are on track to close out their fifth consecutive losing week, and the selloff is becoming harder to classify by normal rules. The Nasdaq Composite confirmed correction territory yesterday, closing down more than 10% from its October record, while the S&P 500 fell 1.74% to 6,477 and is now trading below its 200-day moving average, a key long-term technical indicator, for the first time since spring 2025. This morning, despite Trump’s overnight extension on strikes against Iranian energy infrastructure, S&P futures are down another 0.2%, suggesting markets have stopped responding to diplomatic announcements without verified follow-through. The CBOE Volatility Index (VIX), a widely watched measure of expected near-term market turbulence, is holding at 25-26, its highest sustained level in nearly two years (CNBC).

What makes this selloff unusual is what has simultaneously stopped working as protection. Gold, historically one of the most reliable safe-haven assets in times of crisis, has fallen roughly 15% since the war began and is on track for its worst month since October 2008. US Treasury bond prices have also declined, sending the 10-year yield to around 4.46%, as inflation fears override the typical flight-to-safety impulse. Stocks, bonds, and gold are all falling together, while the US dollar, up around 2.3-2.8% in March near a 10-month high, is the sole consistent winner. Recession probability estimates are climbing: Moody’s Analytics puts the odds at 48.6%, Wilmington Trust at 45%, and Goldman Sachs at 30%. Technology has been the worst-hit sector, with AMD down 6.35% yesterday, Meta falling 8%, and Nvidia declining 3.83%.

The macro backdrop hardening behind the selloff comes from the Organisation for Economic Co-operation and Development (OECD), which released its interim economic outlook this week projecting US inflation will reach 4.2% in 2026, a full 1.2 percentage points above its December forecast and dramatically above the Federal Reserve’s own projection of 2.7%, published just eight days ago. CME FedWatch data now shows a 51.3% probability that US interest rates remain unchanged through all of 2026, with a 16% chance of at least one rate hike. The most publicly dovish member of the Federal Open Market Committee (FOMC), Governor Stephen Miran, raised his own year-end rate projection by 50 basis points at the March meeting despite voting to cut, attributing the revision not to oil prices but to pre-war inflation data. That distinction matters: it signals the Fed’s inflation problem predates this crisis entirely and will not simply resolve when the war ends (Reuters).

Sensei’s Insight: Gold’s 15% drop during a war looks baffling until you understand the rate logic. Gold pays no income, so when interest rates are high or rising, holding it carries an opportunity cost compared to cash or bonds that actually yield something. The market is pricing rate hikes, not cuts, which makes gold less attractive on a relative basis. But that is not the whole story. Gold was already deep into a multi-year bull run before the war started and had made most of its gains. A return to all-time highs this year is still a real possibility if the conflict drags on and inflation expectations become entrenched. It may just take longer than the war premium alone could deliver.

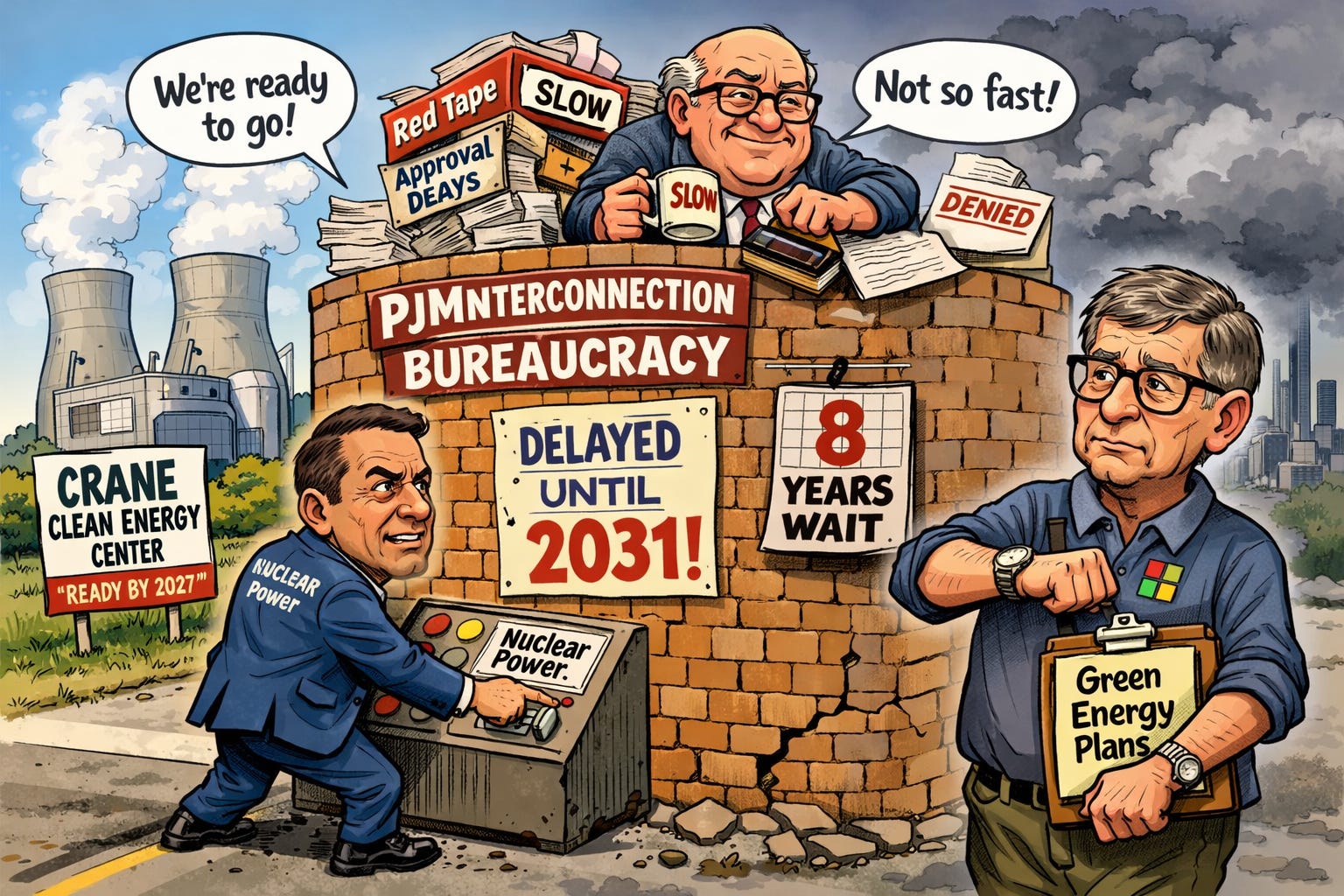

☢️ Nuclear’s Comeback Just Hit a Bureaucratic Wall

Constellation Energy’s plan to restart Three Mile Island, now renamed the Crane Clean Energy Center, suffered a significant setback this week. The company disclosed that PJM Interconnection, the grid operator serving 67 million people across 13 US states, told it the plant cannot connect to the grid until approximately 2031, a roughly four-year delay beyond Constellation’s 2027 target. The financial stakes are substantial. The entire commercial logic of the restart rests on a landmark 20-year power purchase agreement with Microsoft, Constellation’s largest contract ever, under which the plant’s 835 megawatts of output is expected to generate between $686 million and $805 million in annual revenue. Constellation’s shares fell around 2.7% on the news and trade well below analyst consensus targets averaging $400 per share, with JPMorgan maintaining that target and Morgan Stanley recently resuming coverage with an Overweight rating (Reuters).

The delay exposes a structural problem in the US energy system. PJM’s interconnection process, rated “D-minus” by the research group GridLab and the worst grade of any regional grid operator, now requires an average of eight years to bring new generation online. Network upgrade costs have surged from around $29 per kilowatt in 2017-2019 to $240 per kilowatt in 2020-2022. The painful irony is that PJM’s own most recent capacity auction failed to meet its reliability targets, yet its processes are simultaneously blocking a ready-to-restart plant from connecting. Constellation is pushing for fast-track mechanisms, Pennsylvania’s governor has urged PJM to expedite shovel-ready projects, and the Federal Energy Regulatory Commission (FERC) is under pressure to intervene. The 2031 date is not final, but it is the current planning assumption.

Sensei’s Insight: Three Mile Island can generate power by 2027. The grid just won’t accept it for four more years. This is the energy transition story in miniature: clean supply exists but the infrastructure to absorb it doesn’t. The real risk for Constellation is that Microsoft, staring at a 2031 connection date, starts searching for alternative clean power arrangements and the restart’s financial case begins to unravel.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: Boots, Oil, and the Point of No Return"

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.