Morning Forecast: Friday 3 July

A record Dow, a 7% Tesla drop, and Bitcoin back above $62,000.

US markets are closed today for Independence Day. With Wall Street shut, crypto, gold and Europe are the markets still live, and they carry the fallout from a jobs shock that has just reset the Fed’s path into a thin holiday weekend.

👀 Today’s Stories at a Glance

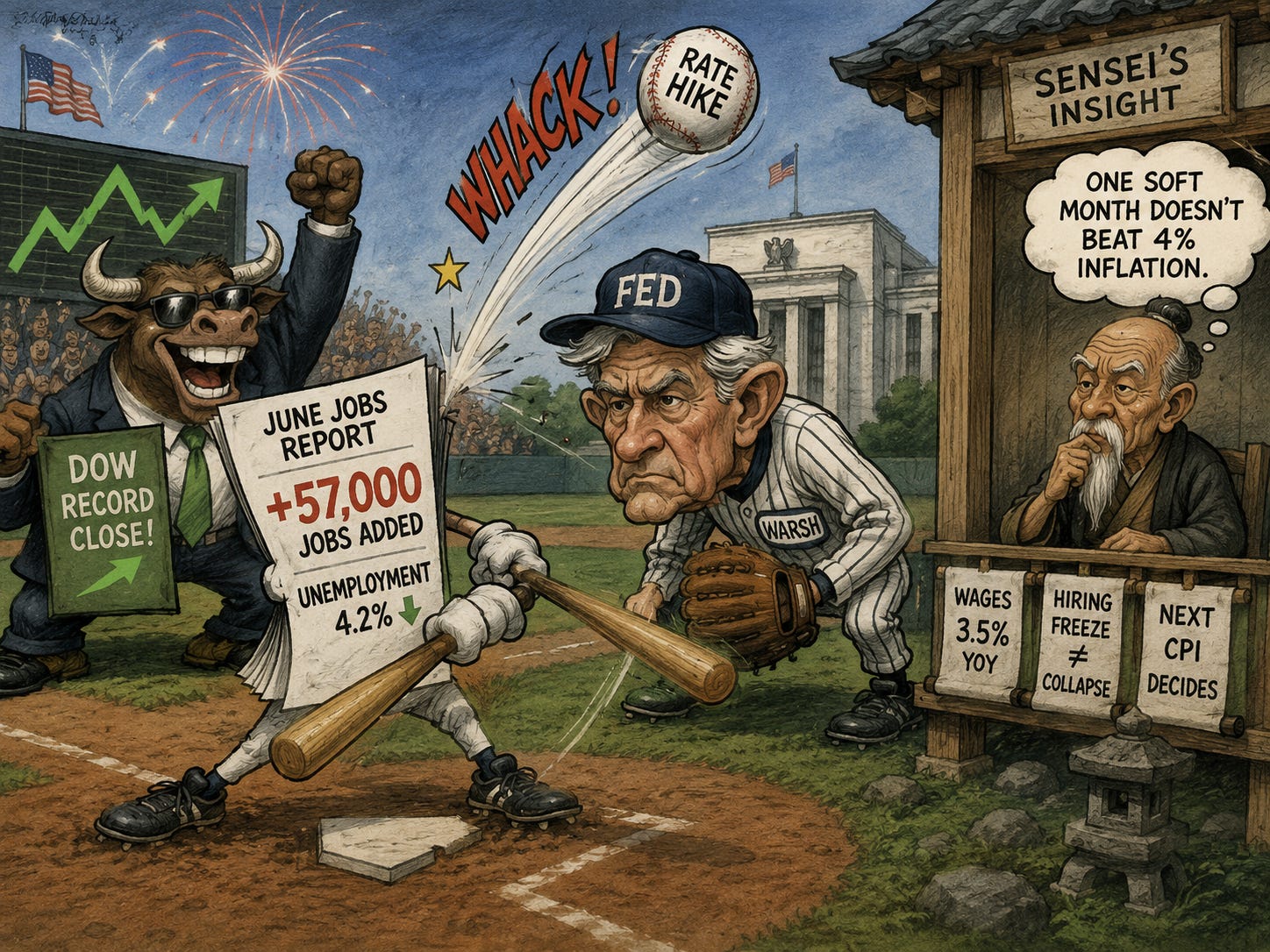

💼 Jobs miss resets the Fed: June payrolls came in at 57,000, half the forecast, cooling hike bets.

💾 Chip stocks crater again: The semiconductor ETF fell 4.5% as AI-demand fears spread.

🚗 Tesla’s record still sank it: 480,126 deliveries beat big, yet the stock lost about 7%.

₿ Bitcoin back above $62,000: BTC hit a monthly high as ETF money returned after ten red days.

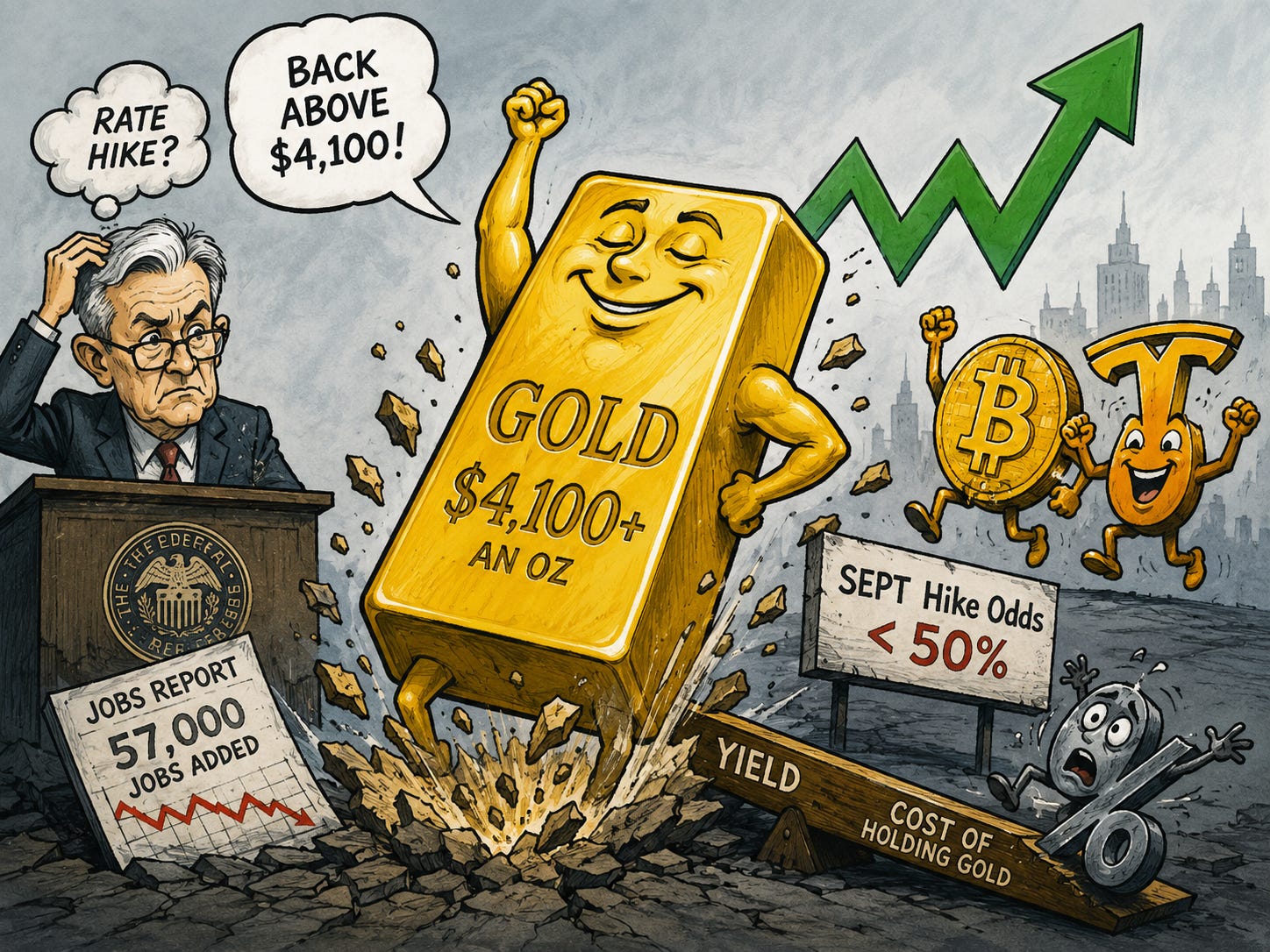

🥇 Gold breaks $4,100: Bullion jumped from an eight-month low as hike bets collapsed.

🛢️ Oil steadies into the weekend: WTI near $69 as US-Iran peace holds and Hormuz flows rise.

🚙 Rivian lifts its outlook: The EV maker raised 2026 guidance and shares jumped more than 8%.

🇬🇧 Europe hits fresh records: The FTSE 100 rose 1.7% with US markets shut for the holiday.

🧠 One Big Thing

The same news that made Meta the market’s darling has turned on the chip sector. Reports that Meta will lease out spare AI computing power added billions to its value, but yesterday traders read it a second way: if the biggest spender has capacity going spare, the industry may have over-built. That fear, plus a Citi note questioning whether AI spending is paying off, helped drive the semiconductor ETF down 4.5% even as the Dow closed at a record. The AI trade is splitting in two, rewarding the platforms that own the compute and punishing the equipment makers that armed the build-out. Watch chip-equipment orders and hyperscaler capex guidance for confirmation.

⚖️ Fear & Greed

📉 The Number That Matters

57,000

The US economy added just 57,000 jobs in June, roughly half what economists expected and the fewest in four months, the print that took a July rate hike off the table.

⚔️ Winners vs Losers

No major winners or losers today due to the market being closed.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $61,863 (▲0.60%)

Ethereum (ETH): $1,740 (▲2.41%)

XRP: $1.11 (▲1.92%)

Equity Indices (Futures):

S&P 500: 7,552 (▲0%)

NASDAQ 100: 29,886 (▲0%)

FTSE 100: 10,606 (▼-0.55%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.49% (▲0%)

Oil (WTI): $69 (▲0.23%)

Gold: $4,178 (▲1.33%)

Silver: $62.28 (▲2.15%)

Data as of: UK: 12:03pm BST / US: 7:03am EDT / Asia (Tokyo): 8:03pm JST

✅ 5 Things to Know

💼 Jobs miss takes a Fed hike off the table

The June jobs report, pulled forward before today’s Independence Day close, landed well short yesterday. The US economy added just 57,000 jobs, roughly half the 115,000 economists expected and the fewest in four months, while the unemployment rate slipped to 4.2% from 4.3%. The detail was softer still: April and May were revised down by a combined 74,000, and leisure and hospitality shed 61,000 posts despite a World Cup tourism boost. Wages rose 0.3% on the month and 3.5% over the year. Wall Street cheered anyway, sending the Dow up nearly 600 points to a record close (Yahoo Finance).

The report rewired the rate debate. For weeks the argument was whether Fed chair Kevin Warsh would raise rates with inflation above 4%, and a print this soft makes a July hike almost impossible while cutting September hike odds below 50% from about 67%. The complication is the falling jobless rate, which stops this reading as an outright downturn and keeps Warsh’s “prices are too high” warning alive. With US markets shut today and the bond market having closed early yesterday, the full repricing plays out in thin holiday liquidity, and the next inflation print becomes the referee (Yahoo Finance).

Sensei’s Insight: The market heard “no more hikes” and bought everything rate-sensitive. I am less sure. Unemployment fell, so this is a hiring freeze, not a collapse, and one soft month does not undo 4% inflation. I am watching wages and the next CPI, not the headline count.

💾 Chip stocks crater as AI-demand fears spread

The stocks that led the first half fell hardest again yesterday. The VanEck Semiconductor ETF dropped 4.5% on the first full session of the quarter, with Teradyne down 13.6%, KLA off 11.5%, Micron losing 5.5% and Nvidia slipping 1.4%, even as the Dow closed at a record. It was the second straight day of heavy selling in the group that added trillions in value through the spring, and it dragged the Nasdaq to a 0.8% loss while the rest of the market rose (Yahoo Finance).

The trigger was a shift in the story investors tell themselves about AI. A Citi analyst questioned whether the big cloud platforms can keep spending at this rate without proof the outlay is paying off, and the prior session’s news that Meta will lease out spare computing power was reread as a warning. If the largest buyer has capacity going spare, the industry may have over-built, which points to thinner future orders for memory chips and GPUs. Memory-price cycles have turned before, and the equipment names that sell the build-out tend to feel it first.

Sensei’s Insight: The AI trade is separating into owners and armourers. Platforms that hold the compute keep the pricing power; the equipment makers that sold the boom carry the overcapacity risk. I am watching capex guidance from the hyperscalers, because that is the number that settles who is right.

🚗 Tesla delivers a record and the stock still sinks

Tesla reported its strongest quarter ever yesterday and the shares fell about 7%, their worst day in nearly a year. The company delivered 480,126 vehicles in the second quarter, up roughly 25% on last year and well above the 397,000 the Bloomberg consensus expected, with energy storage deployments of 13.5 gigawatt hours. On paper it was a blowout. In practice the stock had already climbed about 12% into the report, so the beat was priced in, and attention swung straight to the profit margins Tesla reveals on 22 July (CNBC).

The reaction says more about expectations than about the cars. Part of the strong quarter reflected buyers rushing to beat expiring US EV tax credits and higher pump prices from the Iran conflict, both one-off tailwinds that may pull demand forward rather than sustain it. With a valuation near 400 times earnings, the market is pricing Tesla as an AI and robotaxi company, and a delivery number, however large, does not move that story. The full results in three weeks, and any read on margins, now matter more than the volume (Yahoo Finance).

Sensei’s Insight: A record quarter that sends the stock down 7% tells you what the market actually cares about, and it is not cars any more. I am watching the 22 July margins: if discounts and tax-credit pull-forward flattered this quarter, the number that counts could still disappoint.

₿ Bitcoin reclaims $62,000 as ETF money returns

Bitcoin has swung from a slump to a monthly high in barely a session. It rose almost 4% yesterday to $62,038, its highest level in about ten days and a sharp turn from the 21-month low near $57,700 it touched days earlier. The weak jobs report did the work, because softer hiring eases the pressure on the Fed and cheaper money tends to flow toward risk assets. US spot Bitcoin ETFs took in a net $221.7 million yesterday, ending a ten-session run of outflows, while Ethereum pushed back above $1,700 and XRP added 3.2% to around $1.09 (CoinDesk).

The timing matters because crypto is about to be the only market open. US equities are shut today and trading is thin across the long weekend, so any weekend headline will move Bitcoin with little to absorb it. Europe’s MiCA deadline, the other crypto event this week, passed with barely a ripple in price, which says the recent selling was macro-driven rather than regulatory. Whether Bitcoin can hold $60,000 through the holiday is the cleanest test of how convinced buyers are that the rate scare has passed (Yahoo Finance).

Sensei’s Insight: One green day after a brutal month is a bounce, not yet a bottom. The ETF inflow is the piece that matters, because it shows sellers stepping back rather than a leverage-driven pop. I am watching whether the money keeps coming through the quiet weekend.

🥇 Gold breaks $4,100 as hike bets unwind

Gold jumped back above $4,100 an ounce yesterday, rebounding from an eight-month low, as the soft jobs report knocked the case for higher rates. Bullion had spent weeks under pressure while traders bet the Fed might still tighten, and the 57,000 payrolls print reversed that in a session, with futures now putting the odds of a September rate hike below 50%, down from about 67% before the data. Lower rates lift gold because the metal pays no yield, so the cost of holding it falls when bond returns look less attractive (Yahoo Finance).

The move fits the day’s pattern, in which everything sensitive to interest rates caught a bid while the chip and Tesla trades unwound. Gold has spent 2026 well below the record above $5,500 it set in January, held back by a strong dollar and the higher-for-longer view, so a break back above $4,100 reads as a signal that the view is shifting. The next test is whether the move survives contact with the coming inflation data, which could just as easily hand the hawks their argument back.

Sensei’s Insight: Gold and Bitcoin rose for the same reason yesterday, and that is the real signal: the market is repricing the whole path of rates, not chasing one asset. I am watching the dollar, because a weaker dollar is what turns a gold bounce into a trend.

Stories You Might Have Missed

🛢️ Oil steadies into the long weekend

Oil edged higher this morning before the US holiday weekend, with West Texas Intermediate near $68.83 and Brent around $72.10, both up about 0.2%, after the prior session took them to their lowest since before the February war on Iran. The calm comes from de-escalation, as flows through the Strait of Hormuz keep rising, Saudi exports recover to about 90% of their pre-war level, and Kuwait lifts output sharply. Attention now turns to Iran, which hosts foreign officials from backers including China and Russia this weekend for the funeral of former Supreme Leader Ali Khamenei, with US-Iran talks set to resume afterwards (CNBC).

🚙 Rivian raises its outlook as Tesla stumbles

While Tesla fell, Rivian climbed more than 8% to around $18.63 on a stronger quarter and a raised forecast. The EV maker delivered 12,194 vehicles in the second quarter, above both its own guidance and the roughly 11,000 analysts expected, and lifted its full-year target to between 65,000 and 70,000 vehicles from a prior 62,000 to 67,000. Demand for its commercial vans and R1 models held up, and deliveries of the new, cheaper R2 have begun. Rival Lucid missed expectations the same day, so the read is company-specific rather than a broad EV recovery, but Rivian’s R2 ramp is the number to track from here (CNBC).

🇬🇧 Europe hits records with Wall Street shut

With US markets closed, the action moved to Europe, where the jobs miss lifted shares to fresh highs. The FTSE 100 climbed 1.7% to 10,652.87, with Frankfurt’s DAX and Paris’s CAC 40 also higher, as investors read softer US hiring as one less reason for the Fed to tighten and applied the same “bad news is good news” logic driving Wall Street. Thin holiday liquidity can exaggerate moves in both directions, so the size of the gain matters less than the direction of it. The bigger question is whether the rally holds when US traders return after the long weekend (Yahoo Finance).

👀 Keep an eye out later today for an XRP/Ripple stock pie, the latest addition to the Trading Challenge.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.