Morning Forecast: Monday, 13 April

Oil Clears $100 After Trump's Hormuz Blockade. The IEA's Emergency Reserves Run Dry in Three Weeks.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🚢 Trump Orders Navy Hormuz Blockade: Oil surged past $100 after peace talks collapsed and the U.S. Navy began enforcing restrictions on all vessels near Iranian ports.

🏦 Goldman Kicks Off Bank Earnings: Wall Street expects strong first-quarter numbers, but the real focus is on private credit exposure and credit quality commentary.

🇭🇺 Orbán Ousted in Landslide Defeat: Péter Magyar’s Tisza party won a projected supermajority, likely ending Hungary’s EU vetoes and unlocking billions in frozen recovery funds.

⛪ Trump Feuds With Pope Leo: The President attacked the pontiff over his criticism of the Iran war, risking alienation of Catholic swing voters.

📊 New Tool Shorts Private Credit: S&P launched a credit-default swap index letting investors bet against the $3 trillion private credit market for the first time

📉 Consumer Confidence Hits Record Low: The University of Michigan sentiment index fell to 47.6, its lowest reading since 1952, as war anxiety and energy costs hammer households.

🇯🇵 Japan Bond Yields Reach Peak: The 10-year yield hit 2.49%, its highest since 1997, as the Hormuz blockade reignited inflation fears across Asia.

🧠 One Big Thing

The failure of peace talks between the United States and Iran has culminated in a direct naval blockade of the Strait of Hormuz. Global energy markets responded instantly with crude prices climbing above $100 per barrel. The immediate tension lies in the rapidly depleting international emergency oil reserves. These strategic drawdowns currently disguise a daily supply deficit of five million barrels. When this temporary cushion evaporates in less than three weeks, the market will face the full impact of the shortage. Investors should view the impending exhaustion of these reserves as the primary catalyst for a severe pricing shift.

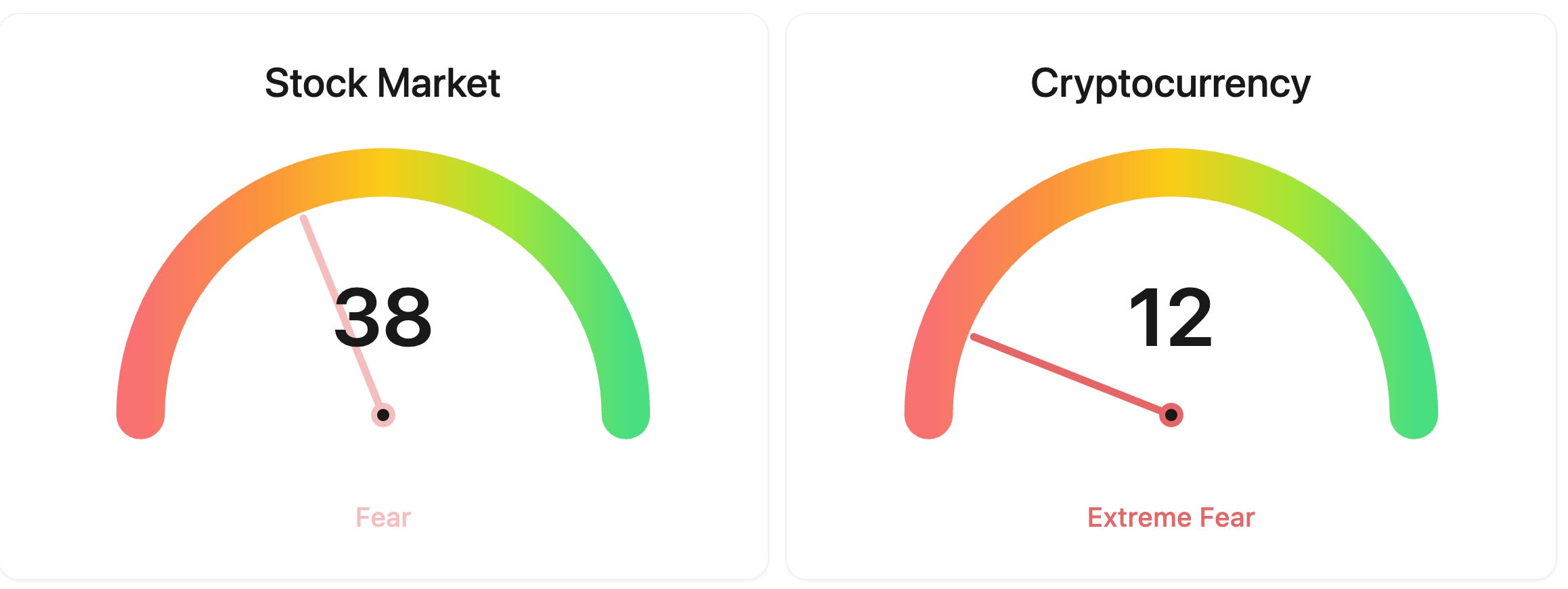

⚖️ Fear & Greed

📉 The Number That Matters

2.49%

Japan's benchmark 10-year government bond yield climbed to 2.49%, its highest level since July 1997. The spike was driven by renewed inflation fears after the Hormuz blockade sent oil prices surging, compounded by the yen sliding toward 160 against the dollar. The Bank of Japan faces a painful choice at its 28 April meeting: hike rates to defend the currency and fight imported inflation, or hold steady and risk letting prices run hotter in an economy already expected to slow. For a country with a debt-to-GDP ratio above 260%, every basis point higher translates directly into billions more in government interest costs.

⚔️ Winners vs Losers

Winners

IDYA 0.00%↑: IDEAYA Biosciences surged after releasing topline results this morning from its Phase 2/3 OptimUM-02 trial evaluating darovasertib plus crizotinib in first-line metastatic uveal melanoma, a highly anticipated binary event the market had been pricing as a potential catalyst for an accelerated FDA approval filing.

FFAI 0.00%↑: Faraday Future Intelligent Electric continued its volatile run after announcing it shipped 12 more embodied AI robots last week and teased an upcoming product event, building on recent momentum around its pivot from EVs to an AI robotics business.

MRVL 0.00%↑: Marvell Technology extended its rally following a Barclays upgrade to Overweight with a $150 price target citing an optical networking super-cycle, adding to gains driven by Nvidia’s $2 billion strategic investment and partnership announced late last month.

Losers

REPL 0.00%↑: Replimune Group collapsed after the FDA issued a Complete Response Letter rejecting its lead melanoma drug RP1 for the second time, prompting the company to announce workforce reductions and a pullback in U.S. manufacturing operations.

LOT 0.00%↑: Lotus Technology slid after reporting full-year 2025 results showing a 44% revenue decline and a 46% drop in vehicle deliveries, weighed down by tariff headwinds and inventory destocking across its key markets.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $70767 (▲ 0.02%)

Ethereum (ETH): $2183 (▼ -0.41%)

XRP: $1.33 (▲ 0.05%)

Equity Indices (Futures):

S&P 500: $6775 (▼ -0.73%)

NASDAQ 100: $25115 (▼ -0.66%)

FTSE 100: £10571 (▼ -0.25%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.34% (▲ 0.42%)

Oil (WTI): $104 (▲ 9.17%)

Gold: $4712 (▼ -0.73%)

Silver: $74.16 (▼ -2.21%)

Data as of: UK (BST) 11:30 / US (EDT): 07:30 / Asia (Tokyo): 20:30

✅ 5 Things to Know Today

🚢 Trump Orders Hormuz Blockade as Peace Talks Collapse and Oil Surges Past $100

The fragile ceasefire between the United States and Iran lasted less than a week before fracturing. After 21 hours of marathon negotiations in Islamabad, Vice President JD Vance flew home without a deal, citing Iran’s refusal to provide what he called an “affirmative commitment” not to develop nuclear weapons. Tehran has long maintained it is not pursuing a weapons programme, a position broadly consistent with international inspections, but the US made nuclear assurances a non-negotiable precondition. Within hours, Trump took to Truth Social and declared the US Navy would blockade “any and all ships trying to enter, or leave, the Strait of Hormuz.” US Central Command confirmed the blockade would begin at 10 a.m. Eastern Time today and apply to all vessels entering or departing Iranian ports. Brent crude surged 7.9% toward $103 a barrel in early trading, while West Texas Intermediate jumped over 8% to $104.80. European gas futures spiked as much as 18%. The S&P 500 was set to open 0.6% lower, the dollar strengthened 0.3%, and gold dipped near $4,710 an ounce (CNBC).

The blockade represents a significant escalation in a conflict now entering its seventh week. Iran responded by threatening that “no port in the Persian Gulf and the Sea of Oman will be safe” if its own facilities are targeted, and declared the US restrictions “illegal and an act of piracy.” Two fuel tankers attempted to exit the Persian Gulf by sailing close to the Iranian coast early today, the first vessels to test the waterway since the announcement. On the diplomatic front, Iran’s Foreign Minister Abbas Araghchi wrote that the two sides had been “just inches” from a memorandum of understanding before talks collapsed, blaming US “maximalism” and “shifting goalposts.” No path toward a second round of negotiations has emerged, with Trump telling reporters he does not care whether Iran returns to the table. France and the UK have announced plans to convene a conference on a multinational mission to safeguard navigation, while the UK confirmed it will not participate in the blockade itself. Onyx Capital Group warned that oil could reach $150 if the blockade is fully enforced, arguing that current prices do not reflect the scale of the risk (Bloomberg).

Meanwhile, the strategic petroleum reserve releases coordinated by the International Energy Agency (IEA) are approaching their limits. Those emergency drawdowns have been offsetting a supply shortfall of roughly 4.5 to 5 million barrels per day since the war began on 28 February, but analysts warn the gap could widen sharply to 10 to 11 million barrels per day if normal supply is not restored. Saudi Arabia’s crude shipments to China are set to halve next month, from roughly 40 million barrels to around 20 million. Shipping insurance premiums remain more than 1,300% above prewar levels, effectively locking most commercial vessels out of the strait regardless of the blockade.

Sensei’s Insight: The blockade puts a floor under oil prices, but what matters more is the IEA reserve buffer running dry. Strategic releases have masked the true scale of the supply shortfall for six weeks. When that cushion is gone, probably within the next two to three weeks, the market will discover what unmitigated 5-million-barrel-per-day deficit pricing actually looks like. That is the next inflection point, not the blockade itself.

🏦 Goldman Sachs Kicks Off a Bank Earnings Season Loaded With Questions

Goldman Sachs reports first-quarter results before the opening bell today, firing the starting gun on what could be the most scrutinised bank earnings week in years. Wall Street expects Goldman to deliver revenue of roughly $17 billion, up around 13% from a year ago, with earnings per share of approximately $16.50, reflecting continued strength in trading and investment banking. JPMorgan Chase, Citigroup, and Wells Fargo follow tomorrow, with Morgan Stanley and Bank of America the day after. The KBW Nasdaq Bank Index fell 6% in the first quarter for its worst stretch since 2023, rattled by the Iran war, but analysts expect the results themselves to show resilient profit growth across the board (Barron’s).

The numbers may be solid, but the questions waiting on the conference calls are anything but comfortable. Investors will press executives on banks’ exposure to private credit, a less regulated corner of the lending market where stress is building. Banks have extended billions in loans to private credit funds that in turn financed software companies now facing existential pressure from artificial intelligence. Fears that those borrowers could default have triggered an investor rush for the exits at several major non-traded funds. A UBS analyst framed the central question in a note last week: “Can solid results overcome a wall of worry?” Morgan Stanley’s analysts characterised banks’ private credit lending as “more of a headline risk than a fundamental risk,” but acknowledged that higher-for-longer oil prices would change that calculus. Among individual stocks, Citi has emerged as a sell-side favourite for its improving return profile, while JPMorgan is expected to benefit from its dominant markets and investment banking franchise (Bloomberg).

Sensei’s Insight: The first-quarter numbers should be strong, and the market already knows that. What will move bank stocks this week is the tone on credit quality, specifically whether executives signal that the private credit stress they have been calling manageable is starting to migrate into their own loan books. Watch the provisioning numbers and forward guidance language more closely than the headline beats.

🇭🇺 Orbán Ousted in Hungarian Landslide as Trump Loses His Closest European Ally

Viktor Orbán’s 16-year grip on Hungary ended yesterday in a landslide defeat that few polls predicted at this scale. Péter Magyar, a former Orbán loyalist who broke with the ruling Fidesz party in 2024, led his centre-right Tisza party to a projected supermajority of around 138 seats in the 199-seat parliament. Fidesz collapsed to roughly 55 seats from the 135 it held previously. Turnout was nearly 80%, a post-communist record, with young voters playing a decisive role. Magyar campaigned on corruption, healthcare, and EU re-engagement, pledging to rebuild Hungary’s relationships with the European Union and NATO after years of obstruction under Orbán (CNN).

The result carries geopolitical weight well beyond Budapest. Orbán was one of Trump’s closest international allies and a figurehead for the global populist right. JD Vance visited Budapest days before the vote in what was widely seen as an attempt to boost Orbán’s campaign. European Commission President Ursula von der Leyen said “Hungary has chosen Europe,” while European leaders from Paris to Warsaw welcomed the result. For markets, the immediate implication is that Hungary’s EU veto, used repeatedly by Orbán to block Ukraine aid packages and other joint actions, is now likely to disappear. Magyar has signalled he would end Hungary’s drift toward Moscow, a shift that could unlock billions in frozen EU recovery funds that Brussels had withheld over rule-of-law concerns. Trump has not publicly commented on the result (PBS).

Sensei’s Insight: The market story here is not Hungary’s equity index, which is small. It is what happens to EU decision-making when the most reliable veto is removed. Frozen EU recovery funds could be unlocked, joint defence spending could accelerate, and Ukraine aid packages could clear faster. European defence stocks and EU-exposed financials could be the quiet beneficiaries of a shift most investors are filing under “politics, not markets.”

⛪ Trump Attacks Pope Leo XIV as Religious Rift Over Iran War Deepens

President Trump launched an extraordinary public attack on Pope Leo XIV yesterday, calling the leader of the Catholic Church “WEAK on crime” after the Pope challenged the administration’s claim that God is on the side of the United States in the Iran conflict. “I don’t want a Pope who thinks it’s OK for Iran to have a Nuclear Weapon,” Trump wrote on Truth Social, adding criticism of Leo’s stance on the Venezuela operation. He followed the post with an image depicting himself in robes healing a sick patient, echoing religious imagery. The American-born pontiff had written on X that “God does not bless any conflict” and that “military action will not create space for freedom or times of peace,” a pointed response to repeated remarks from Trump and Defence Secretary Pete Hegseth couching the war in religious terms (Bloomberg).

The clash matters politically because roughly 52 million Americans identify as Catholic, a demographic that has been a swing vote in recent elections. Trump won Catholic voters in 2024, but polling since the start of the Iran war shows his support softening among this group. Leo has become an increasingly vocal counterweight to the administration’s war messaging, with CNN’s Vatican correspondent describing him as a “spiritual and diplomatic counterweight to President Trump.” The Pope is now embarking on a 10-day tour of four African countries, where his message on peace and reconciliation is likely to continue drawing contrasts with Washington’s approach. For investors, the domestic political signal is what counts: Trump is losing allies at home and abroad in the same weekend, with Orbán’s defeat in Hungary compounding the isolation.

Sensei’s Insight: Trump feuding with the Pope is dramatic, but the market signal is subtler. The President picked a fight with the Catholic Church on the same weekend he lost his closest European ally and came home from failed peace talks empty-handed. That is three credibility hits in 48 hours, and political capital is a finite resource when you need congressional support to fund a war and hold together a ceasefire.

📊 Wall Street Builds a Tool to Bet Against the $3 Trillion Private Credit Market

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.