Morning Forecast: Monday 13 July

Oil surges as the Hormuz standoff reignites, the big banks report tomorrow, and June CPI looms.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🛢️ Oil jumps as strikes resume: Brent rose about 3% toward $78 after the US and Iran traded fresh attacks and Tehran claimed Hormuz was closed.

📊 Inflation test lands tomorrow: June CPI and Kevin Warsh’s first testimony arrive together, the clearest read yet on whether a Fed hike is live.

🏦 Banks open earnings season: JPMorgan, Goldman and three more report before tomorrow’s open, with Goldman’s profit seen up 32% on trading.

💾 SK Hynix round trip: The chip giant’s US shares fell about 8% today, handing back much of its record 13% Nasdaq debut pop.

₿ Bitcoin dips before rules week: Bitcoin slipped near $63,000 as traders eyed a Senate back in session and this week’s CLARITY Act crypto hearing.

🥇 Gold falls as war flares: Gold slid to about $4,058, roughly 25% below January’s record, as the inflation read overpowered its haven bid.

🖥️ Chip earnings loom too: ASML and TSMC report later this week, offering markets a fresh real-time gauge of AI hardware demand after the banks.

🎰 MGM weighs a $12.4bn buyout: MGM set up a committee to weigh Barry Diller’s $12.4bn bid for the casino group’s remaining shares.

🔍 Tech’s $2.9tn AI debt binge: The cash-rich giants have become the bond market’s biggest borrowers to fund a $2.9tn data-centre build.

📈 Chart of the Day: the level Sensei is watching now, with the triggers that matter.

🧠 One Big Thing

Look at what moved together this morning. Oil jumped, gold fell, and yields held firm, which is the market’s way of pricing a supply and inflation shock, not a growth scare. That is the most awkward possible setup into tomorrow’s CPI. A fresh energy spike lifts headline prices just as a split Fed decides whether a hike belongs on the table, and a chair who has already floated one steps in front of Congress hours later. The read to carry into the week: watch the 10-year Treasury yield and the core CPI number, because together they decide whether risk assets keep their footing.

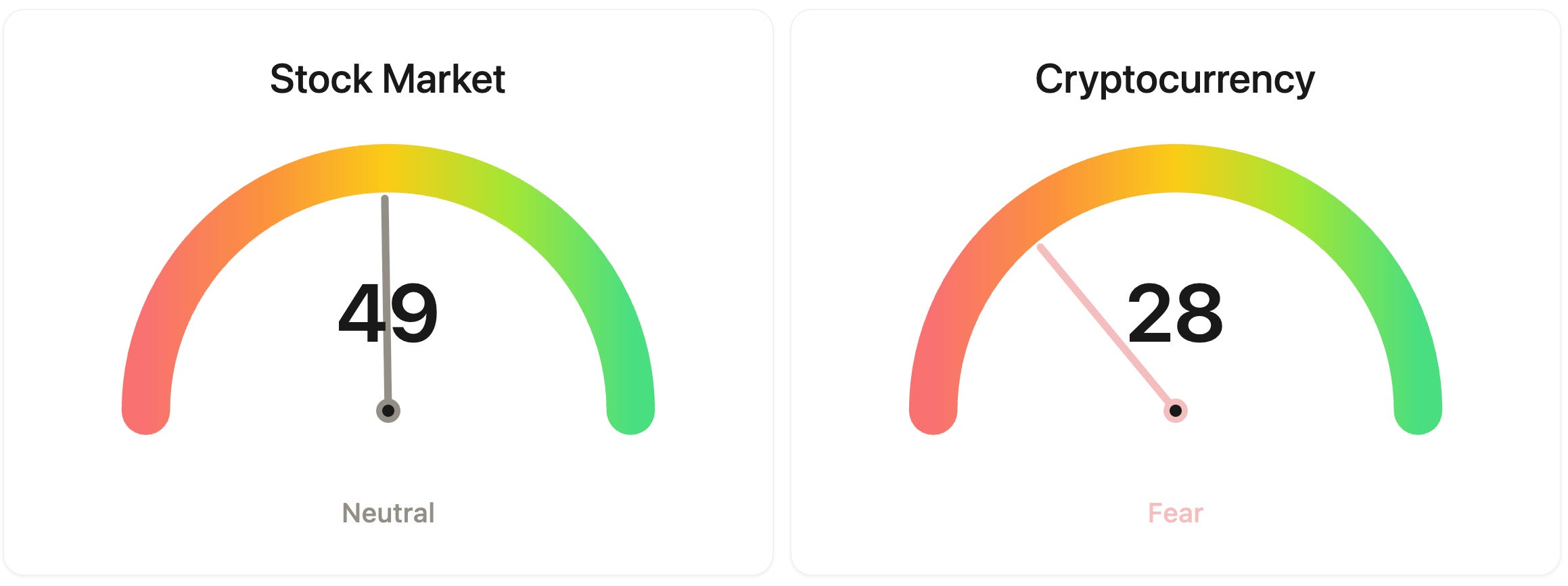

⚖️ Fear & Greed

📉 The Number That Matters

4.2%

May’s annual inflation rate, the hottest since 2023, is the bar June’s CPI has to clear when it lands tomorrow, with rising oil now threatening to keep price pressure alive.

⚔️ Winners vs Losers

Winners

QTTB 0.00%↑: Q32 Bio Inc. soared into this morning’s 36-week topline readout from Part B of its SIGNAL-AA trial of bempikibart in severe alopecia areata, having already surged in Friday’s after-hours session when the readout date was set.

AGEN 0.00%↑: Agenus Inc. jumped after announcing an $85 million private placement led by Commodore Capital, a raise that could reach $340 million if all warrants are exercised and extends the company’s cash runway through the end of 2031.

Losers

JLHL 0.00%↑: Julong Holding Limited extended a violent unwind in the newly listed Chinese building systems micro-cap, which has been hit with repeated Nasdaq volatility halts as speculative positioning washes out of a thin float.

STRS 0.00%↑: Stratus Properties Inc. fell on a mechanical adjustment as today marks the record date for its $5.00 per share initial liquidating distribution, part of the Austin developer’s plan of complete liquidation and voluntary Nasdaq delisting.

FIZZ 0.00%↑: National Beverage Corp. dropped as shares went ex-dividend on a $3.25 per share special payout, a mechanical move that accounts for nearly the entire decline.

MU 0.00%↑: Micron Technology, Inc. fell on the same SK Hynix shock, which reignited questions over whether AI memory pricing has already peaked.

BE 0.00%↑: Bloom Energy Corporation kept sliding under twin short-seller attacks, with Hunterbrook Capital alleging the fuel cell maker understated its reliance on Chinese scandium suppliers and Crossroads Capital disclosing its own short a day later.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $63,020 (▼1.13%)

Ethereum (ETH): $1,782 (▼1.30%)

XRP: $1.08 (▼0.51%)

Equity Indices (Futures):

S&P 500: 7,598 (▼0.30%)

NASDAQ 100: 29,755 (▼0.92%)

FTSE 100: 10,485 (▼0.31%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.57% (▲0.26%)

Oil (WTI): $74 (▲2.95%)

Gold: $4,066 (▼1.33%)

Silver: $58.56 (▼2.14%)

Data as of: UK: 12:04 BST / US: 07:04 EDT / Asia (Tokyo): 20:04 JST

✅ 5 Things to Know

🛢️ Oil jumps as the US and Iran trade fresh strikes

Oil climbed to start the week after the US and Iran exchanged a new round of attacks over the weekend, reviving fears over the Strait of Hormuz, the channel that carries roughly a fifth of the world’s seaborne oil. Brent crude rose about 3% toward $78 a barrel and US WTI traded near $73, paring bigger early gains. US Central Command said its forces hit dozens of targets, using one-way attack sea drones for the first time, in retaliation for an Iranian strike on a container ship that was left ablaze with one crew member missing. Iran said the strait was closed “until further notice,” a claim CENTCOM rejected (CNBC).

The escalation puts last month’s 60-day interim peace deal in doubt and lands at the worst possible moment for markets, hours before the year’s most watched inflation report. Higher oil feeds straight into headline prices, and a fresh energy shock is exactly what could push an already-split Fed toward a hike rather than a cut. Shipping data shows the strait thinning out, with only six vessels tracked crossing in one recent overnight window against 18 to 22 a day earlier this month. Watch whether traffic seizes up further, because a genuine closure, rather than the threat of one, is what turns an oil scare into an oil crisis.

Sensei’s Insight: Markets have learned to fade these Hormuz flare-ups, and every prior scare this year reopened within days. The difference now is timing. An oil spike into tomorrow’s CPI hands the Fed an inflation excuse just as it debates a hike.

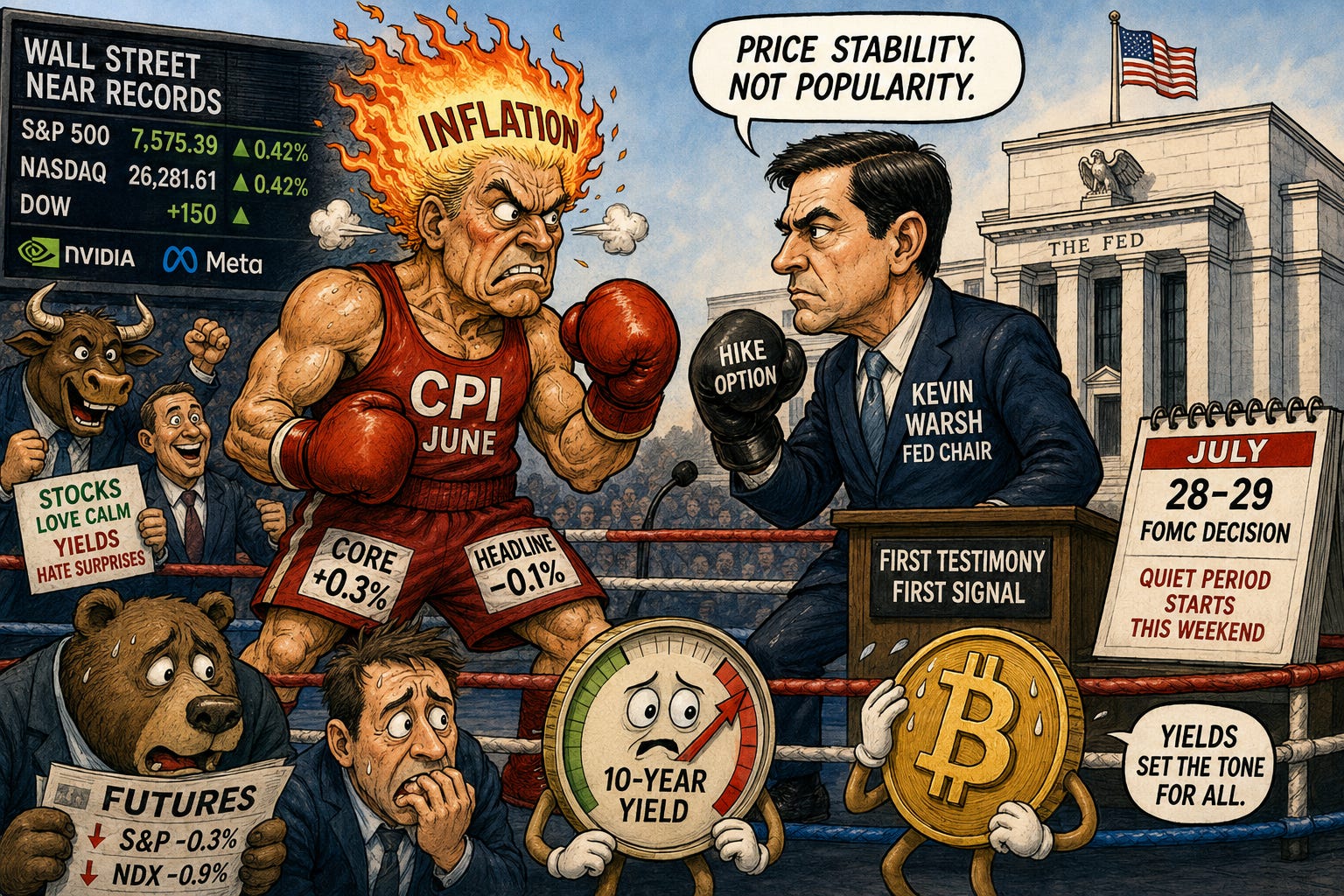

📊 CPI and the new Fed chair headline a huge week

Wall Street closed last week near records, with the S&P 500 finishing at 7,575.39, up 0.42%, the Nasdaq Composite at 26,281.61 and the Dow adding about 150 points, helped by Nvidia and Meta (CNBC). That calm is about to be tested. Tomorrow brings June CPI, the most important inflation reading of the year after May’s 0.5% monthly jump lifted the annual rate to 4.2%, its hottest since 2023. Economists expect headline prices to slip 0.1% as energy cools, while core, which strips out food and energy, is seen up 0.3%. Futures wavered to start the week, with S&P contracts off about 0.3% and Nasdaq-100 futures down 0.9%.

Hours after the print, Kevin Warsh delivers his first testimony as Fed chair, then repeats it before the Senate midweek, giving markets their clearest read yet on how hawkish he really is. He has already floated a hike as an option, so a hot core reading plus rising oil could harden that case and lift yields, while a soft print would calm nerves before he speaks. The Fed enters its pre-meeting quiet period at the weekend, so this is the last real policy signal before the 28 to 29 July decision. Watch the 10-year Treasury yield, which has been setting the tone across stocks and crypto alike.

Sensei’s Insight: Two numbers decide the week: core CPI and Warsh’s first line on hikes. A market that spent the year pricing cuts has quietly stopped, and it is not braced for a chair who sounds comfortable holding rates higher for longer. There’ll be a cheat sheet for it tomorrow,

🏦 Big banks fire the starting gun on earnings

The second-quarter earnings season opens before tomorrow’s bell, and as ever the big banks go first. JPMorgan, Bank of America, Goldman Sachs, Wells Fargo and Citigroup all report, giving the first hard look at how the economy is actually behaving through loan demand, credit quality and trading desks. Expectations are high: analysts see JPMorgan earning about $5.52 a share, up roughly 10% on the year, and Goldman around $14.47, a jump of more than 32%, on a rebound in dealmaking and trading (Yahoo Finance). Across the S&P 500, second-quarter profits are expected to rise about 24%.

The bar is set high enough that a beat may not be enough on its own, with options markets pricing swings of about 6% for Goldman and 4.4% for JPMorgan on the day. The metric that matters most is net interest income, the gap between what banks earn on loans and pay on deposits, because it shows how the higher-for-longer rate picture is filtering through. Their tone on the consumer and on credit provisions often sets the mood for every report that follows. Watch the guidance and the language on loan losses more than the headline profit, because that is where any crack in the economy shows up first.

Sensei’s Insight: Bank results are the market’s first unfiltered look past the survey data. If the biggest lenders sound relaxed on credit while trading prints records, it steadies the whole tape into CPI. Cautious guidance would feed the slower-hiring worry the jobs numbers keep hinting at.

💾 SK Hynix hands back its record debut

SK Hynix, the world’s second-largest memory-chip maker, gave back much of its blockbuster Wall Street debut to start the week. Its US-listed shares fell about 8% in early trading, and its Seoul stock sank more than 15% in its worst day, after the shares had jumped 13% in their Nasdaq debut to close at $168.01 (Bloomberg). The Nasdaq listing raised $26.5 billion, the biggest first-time share sale by a foreign company in the US, topping Alibaba’s $25 billion in 2014, with demand running at about seven times the shares on offer. The stock trades under SKHYV before switching to SKHY tomorrow.

The round trip captures the whole debate over the AI trade in one session. Investors will pay up for the memory that feeds AI data centres, then think twice at the price, especially with chip names leading futures lower this morning and Middle East risk back on the screen. SK Hynix supplies more than half the high-bandwidth memory that sits beside Nvidia’s chips, so its shares have become a proxy for how durable that demand really is. Watch ASML’s order book and TSMC’s results later this week, the two reports that will either confirm the AI-capex boom or start to question it.

Sensei’s Insight: A debut that pops 13% then falls 8% two sessions later is not a verdict on the company, it is a verdict on the price. The memory cycle is real. The argument now is how much of it is already sitting in the stock.

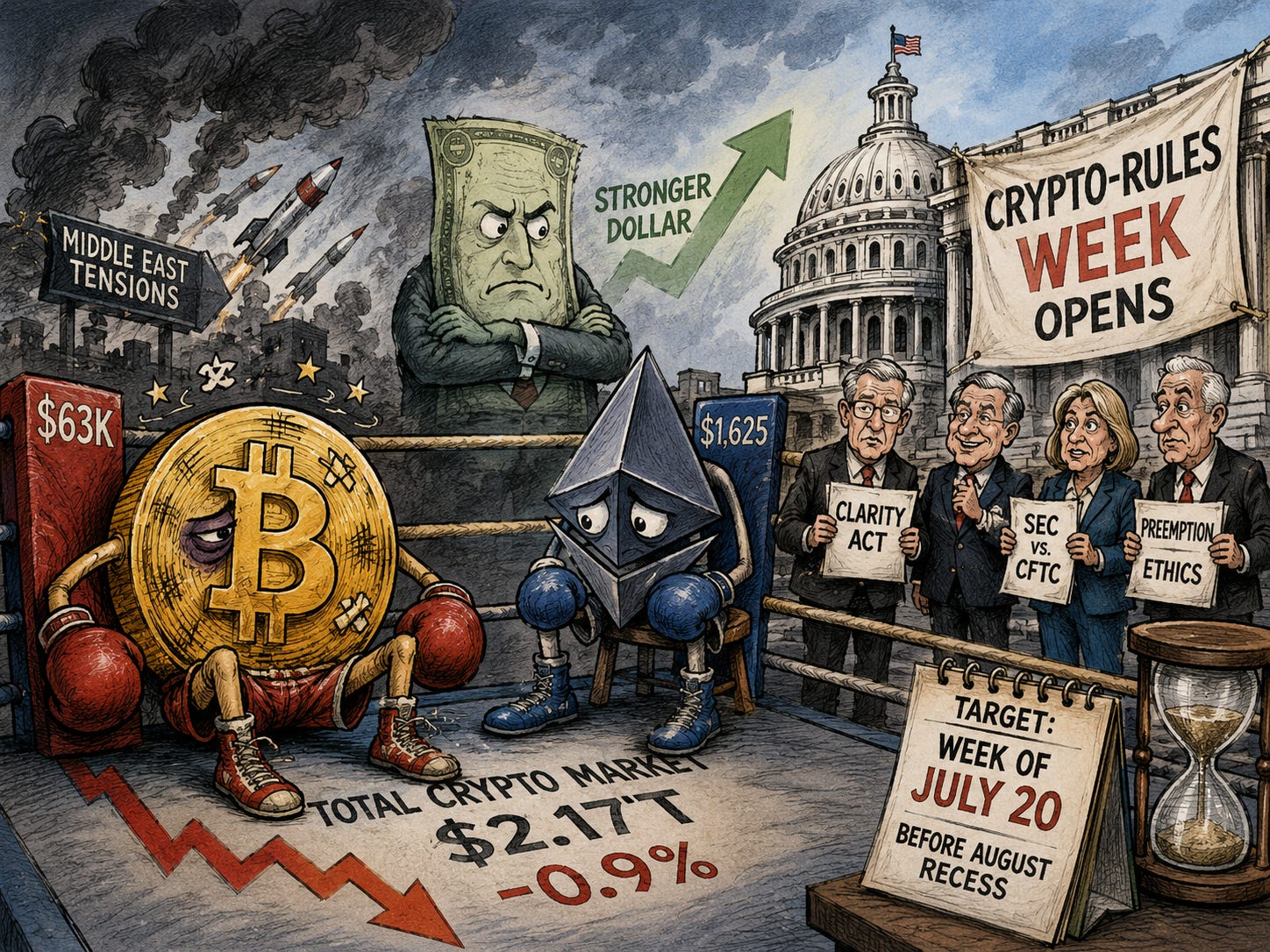

₿ Bitcoin slips as a decisive crypto-rules week opens

Bitcoin started the week on the back foot, trading near $63,000 as the risk-off mood from the Middle East and a firmer dollar weighed on crypto. Ethereum slipped toward $1,780 and the total crypto market fell about 0.9% to $2.17 trillion (CoinDesk). The bigger story is in Washington. The Senate returns from recess today, restarting the clock on the CLARITY Act, the market-structure bill that would split oversight of crypto between the SEC and the CFTC and give the industry the rulebook it has wanted for years.

A new draft of the bill is expected in the coming days, with backers hoping for a Senate floor vote as soon as the week of 20 July, though ethics rules, federal preemption and the SEC-CFTC split are still unresolved and time is short before the August recess. A House field hearing on the bill lands later this week, a talking-shop event rather than a vote. For now crypto is trading on the macro, not the politics, but a genuine breakthrough on rules would be the first real catalyst in weeks. Watch whether the new text actually drops, because the market has been promised it before.

Sensei’s Insight: Crypto has spent the year moving with the Nasdaq, not against it, so the same CPI and Fed signals driving stocks are driving Bitcoin. Regulation is the one thing that could hand it a catalyst of its own, if the Senate finally delivers.

Stories You Might Have Missed

🥇 Gold falls even as the war flares

Gold fell to start the week even as US-Iran strikes escalated, with spot gold down about 1.5% near $4,058 an ounce. The usual haven bid gave way to a colder logic: higher oil raises the odds of a fresh inflation shock, which keeps the Fed hawkish and lifts the dollar and yields, all of which weigh on an asset that pays nothing to hold. Gold is now roughly 25% below its January record around $5,595, a reminder that in this cycle the rates story has repeatedly overpowered the crisis story. Tomorrow’s CPI is the next test of whether that holds (Yahoo Finance).

🖥️ The chip earnings that could steal the show

The banks open earnings season, but the reports markets may care about most come later in the week from the chip world. ASML, which makes the machines that print the most advanced chips, reports midweek, and its order book is read across markets as a real-time gauge of AI hardware demand. Taiwan Semiconductor, which manufactures the most advanced silicon for Nvidia and Apple, follows soon after with its results and 2026 spending plans. After SK Hynix’s wild debut and today’s reversal, both prints will shape how investors price the whole AI-infrastructure trade (CNBC).

🎰 MGM weighs Barry Diller’s $12.4 billion buyout

MGM Resorts has formed a special board committee to weigh a takeover proposal from Barry Diller’s People Inc., the company formerly known as IAC, which already owns about 26% of the casino operator and has offered to buy the rest at $48.30 a share (Bloomberg). The bid values MGM at roughly $12.4 billion, and the company has told advisers it believes the offer undervalues its assets. JPMorgan is helping finance Diller’s side. It is an early sign that large US dealmaking is thawing again, a theme the bank results this week should help confirm or cool.

🔍 Deep Dive: A $2.9 Trillion Bill, Paid on Credit

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.