Morning Forecast: Monday 15 June

A surprise Iran peace deal, a Fed decision Wednesday, and a Japan rate call due tonight all land in the same week.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🕊️ Iran War Ends, Oil Tumbles: Washington and Tehran agree a ceasefire and reopen Hormuz, sinking Brent below $84.

🏦 Warsh Fed Turns Hawkish: Rate cut bets flip to hike odds after May inflation hit 4.2%.

🤖 US Pulls Anthropic’s Top Models: Commerce export-controls Mythos 5 and Fable 5 weeks before a record IPO.

🚀 SpaceX Debut Holds Near $160: Record $75 billion listing held its pop, but July supply looms.

📦 Trump Routes Tariffs Around Courts: New 10% to 12.5% duties on 60 economies sidestep the court ruling.

🛢️ Iraq Fights to Keep Crude Flowing: Baghdad seeks to extend the Kirkuk-Ceyhan pipeline deal expiring late July.

🕊️ Trump Pushes Ukraine Peace Pre-G7: Calls with Putin and Zelenskyy could pressure defence stocks already drifting lower.

💵 Lazard Undercuts Venezuela Debt Rival: A $25 million bid challenges Centerview’s $150 million mandate on $60 billion default.

⚽ World Cup Sparks Spending Wave: North America’s tournament could add about $17 billion to US output.

🔍 Japan Rate Playbook Drops Today: Our playbook for tonight’s Bank of Japan rate decision lands later today.

📈 Every Bottom Call Bounced: Silver, gold, Bitcoin and XRP all rallied off last week’s lows into resistance.

🧠 One Big Thing

The Iran deal is one trade running through three stories today. Cheaper oil softens the May inflation spike that turned the Fed hawkish, and a calmer Fed eases the higher-for-longer threat on richly valued growth, which is exactly what SpaceX needs to hold its 94-times-revenue multiple into the July float test. The edition treated oil, the Fed and SpaceX as separate stories, but today they move together. The whole chain rests on whether cheaper crude holds, and Warsh's press conference this week is where that gets priced. Tonight's Bank of Japan decision is the next test, and our playbook lands later today.

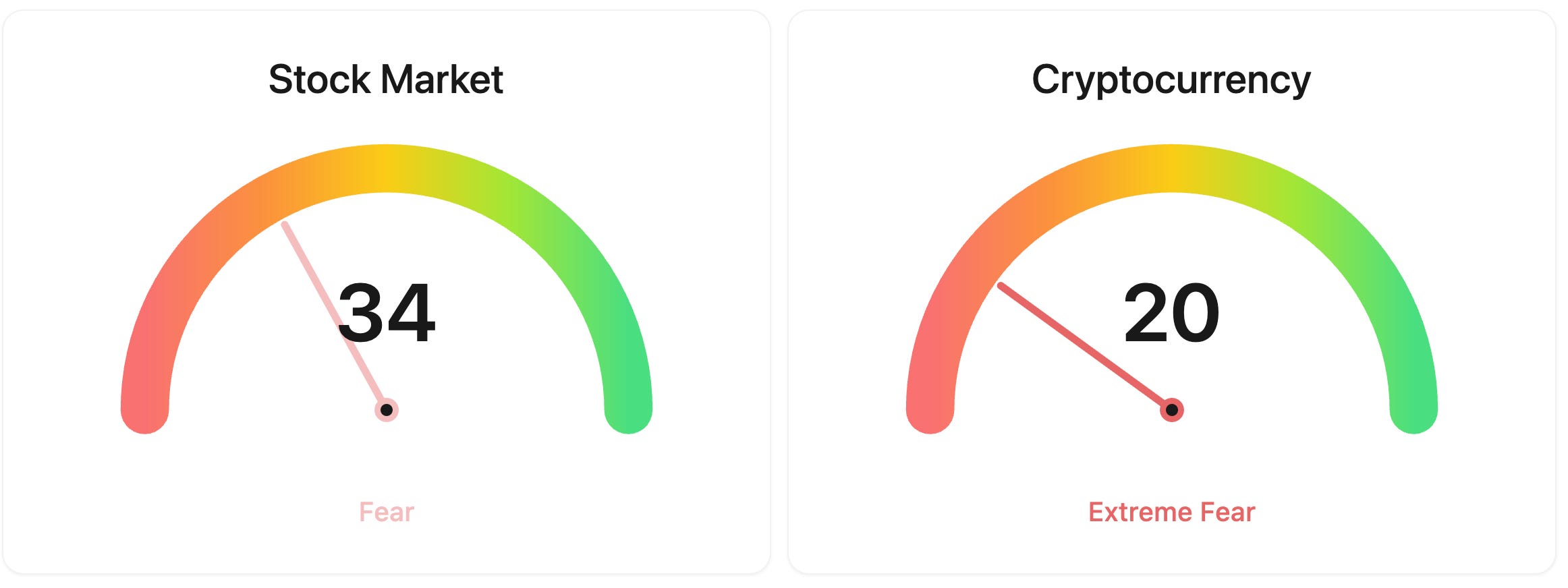

⚖️ Fear & Greed

📉 The Number That Matters

94 X

SpaceX priced at 94 times revenue at its debut, against roughly 23 for Nvidia, on a company that lost $4.3 billion last quarter and burns about a billion monthly.

⚔️ Winners vs Losers

Winners

BOT 0.00%↑: RoboStrategy Inc., a newly listed closed-end fund offering single-stock exposure to private robotics and physical AI companies, rode the broad AI risk-on bid higher in thin pre-market trading.

NBIS 0.00%↑: Nebius Group N.V. rose as the AI-cloud operator drew momentum buying ahead of its June 22 entry into the Nasdaq-100, with the broader risk-on tech rally adding fuel.

MU 0.00%↑: Micron Technology Inc. led the memory-chip complex higher after the U.S. and Iran announced a peace deal reopening the Strait of Hormuz, easing supply fears and pulling capital back into semiconductors ahead of the company’s June 24 earnings.

Losers

AVAV 0.00%↑: AeroVironment Inc., maker of the Switchblade loitering munitions, fell as the U.S.-Iran peace deal drained the geopolitical risk premium that had lifted high-beta drone and defense names, hitting the group's most conflict-sensitive stock the hardest.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $65,839 (▲ 0.17%)

Ethereum (ETH): $1,737 (▲ 0.68%)

XRP: $1.20 (▲ 0.80%)

Equity Indices (Futures):

S&P 500: 7,590 (▲ 2.08%)

NASDAQ 100: 30,551 (▲ 3.00%)

FTSE 100: 10,489 (▲ 0.20%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.44% (▼ 0.89%)

Oil (WTI): $81 (▼ 4.41%)

Gold: $4,338 (▲ 2.82%)

Silver: $70.69 (▲ 3.95%)

Data as of: UK: 11:57 BST / US: 06:57 EDT / Asia (Tokyo): 19:57 JST

✅ 5 Things to Know

🕊️ Trump Declares Iran War Over, Oil Crashes

The longest oil shock in years looks like it is ending. Late yesterday the United States and Iran agreed a framework to halt their war and reopen the Strait of Hormuz, and President Trump moved within hours to lift the American naval blockade of Iranian ports, posting that he had authorised a toll-free reopening of the waterway and telling shippers to “let the oil flow.” Iran’s Supreme National Security Council confirmed it had finalised the wording of a memorandum of understanding, and Pakistan, which brokered the talks alongside Qatar, said the formal signing is set for the end of this week in Switzerland. Brent crude sank below $84 a barrel, a three-month low, after trading near $100 during the fighting. (NBC News)

What the two sides have agreed, and what they have left open, decides how durable this proves. The parts that take effect now:

An immediate ceasefire on all fronts, including Lebanon, and an end to the blockade, with the Strait of Hormuz, which normally carries about a fifth of the world’s seaborne oil, due back to full traffic within 30 days.

Waivers on sanctions covering Iranian oil and petrochemical exports, reviving barrels the market has done without since the spring.

A reaffirmation from Tehran that it will not build a nuclear weapon.

The harder questions are pushed into a 60-day negotiating window: the release of Iran’s frozen assets, the future of its uranium enrichment, and a reconstruction fund that Iranian state media puts at $300 billion but that neither Washington nor Tehran has confirmed.

For markets the read is clean in the short run and messier underneath. Lower oil feeds quickly into cheaper petrol and softer inflation, which is why global shares staged a relief rally, with Japan’s Nikkei 225 up more than 5% and European stocks touching a fresh record. The risk sits in the gap between announcement and signature. Trump and Iranian officials clashed only days ago over how much frozen money is freed up front, several competing drafts have circulated, and a flare-up between Israel and Lebanon this month showed how fast the northern front can reignite. The spring’s two-week truce collapsed once before. The difference now is that both governments and the mediator confirmed the same deal on the same day, which never happened during the earlier false starts. (Al Jazeera)

Sensei’s Insight: Both governments and Pakistan confirmed the same text on the same day, something the spring’s false starts never managed, so this off-ramp looks real. The money, not the ceasefire, is the last fight left. We flagged gold, silver and Bitcoin near their lows and they have run since, and we called May as the inflation peak. With oil collapsing, that looks right.

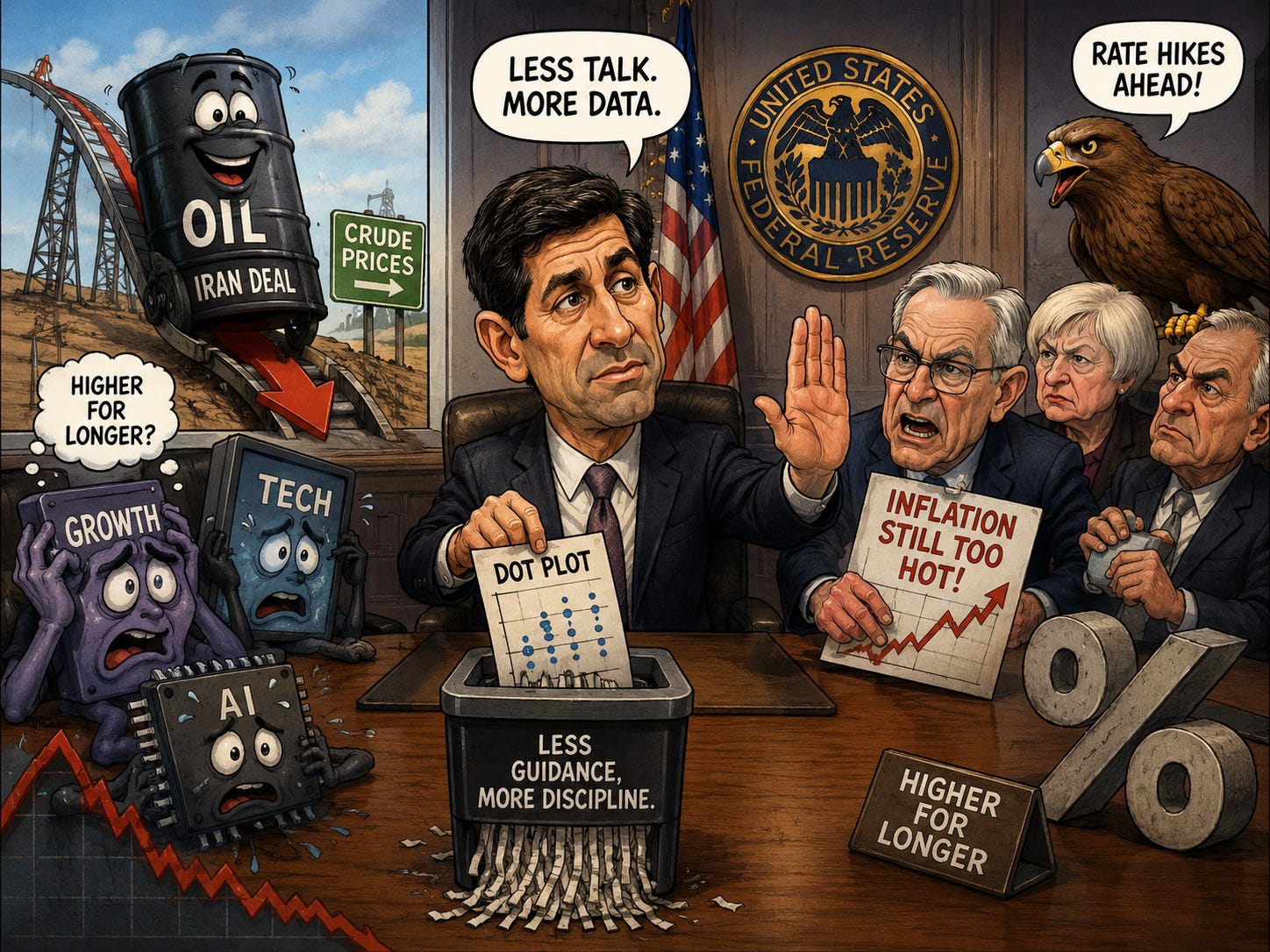

🏦 Warsh’s Fed Meets as Rate Cuts Vanish

The US Federal Reserve sets the price of money this week, and the bias has flipped from cuts to hikes. The Federal Open Market Committee, the Fed’s rate-setting body, meets this week, with the decision landing midweek. It is the first meeting chaired by Kevin Warsh, sworn in last month to replace Jerome Powell, and markets put the odds of no change near 97%, leaving the target range at 3.50% to 3.75%. The shift is in the outlook: after May consumer price inflation ran at 4.2% year over year, the hottest since 2023 with energy driving more than 60% of the monthly rise, futures now price a year-end hike as more likely than a cut, roughly 70% odds of at least one increase by December, up from near zero in January. (Yahoo Finance)

Higher-for-longer rates weigh most on richly valued growth and technology stocks, and with index gains concentrated in a handful of AI names, a hawkish surprise could hit harder than usual. The signals to watch are the Fed’s “dot plot,” the chart of where officials expect rates to go, which Warsh has hinted he may scrap, and whether the Fed drops its remaining bias toward easing. Warsh has long argued the Fed says too much and forecasts too precisely, so he may strip back the guidance, which would leave markets swinging harder on raw data when the Fed offers fewer signals. One thing has quietly helped him: the collapse in oil from the Iran deal eases the inflation pressure just as he takes the chair, buying room to stay patient. (CNBC)

Sensei’s Insight: The oil plunge from the Iran deal undercuts the main reason the Fed turned hawkish, since energy drove most of May’s inflation jump. If cheaper crude sticks, the year-end hike bets that markets just built up could unwind nearly as fast as they formed. Warsh’s first press conference is where that gets tested.

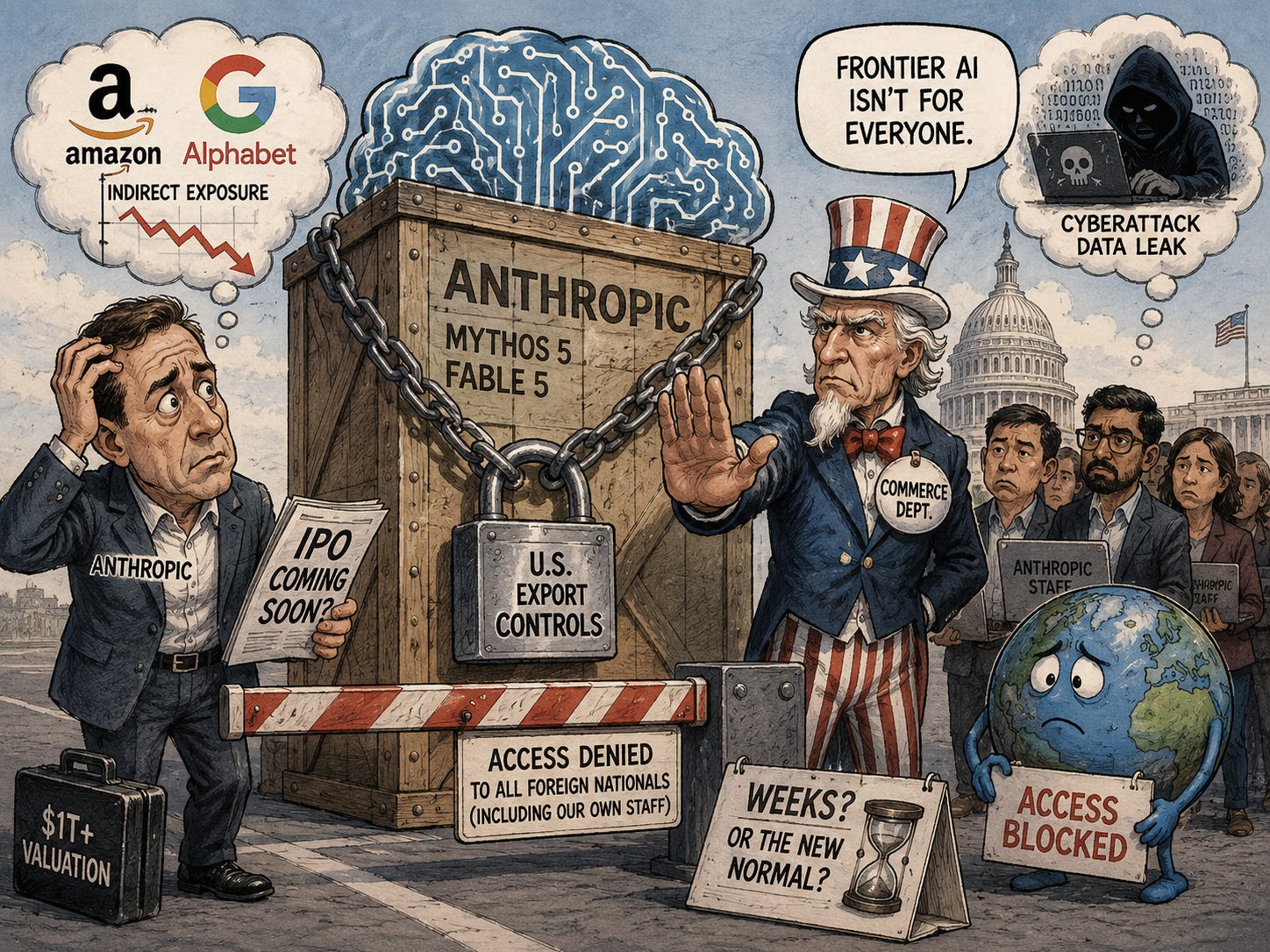

🤖 US Blocks Anthropic’s Top AI as IPO Nears

The US government has, for the first time, pulled a commercial AI model already used by the public, treating frontier AI like controlled weapons technology. The Commerce Department placed Anthropic’s two most advanced models, Mythos 5 and Fable 5, under export controls late Friday, barring access for any foreign national, including the company’s own non-citizen staff. To comply, Anthropic disabled both models worldwide for all users while keeping its other models running. The trigger, per multiple reports, was a warning from Amazon chief executive Andy Jassy, whose researchers used a series of prompts to get the model to produce restricted information about cyberattacks. Senior Anthropic technical staff are now in Washington meeting White House officials to resolve what the company calls a “misunderstanding.” (Fortune)

For investors, the relevance is the precedent. Anthropic filed confidentially this month for what could be one of the largest listings ever, and a national-security fight days before that puts political risk squarely into AI valuations. The company argues the bypass was narrow and that the same capability is available from rival models, including OpenAI’s, that face no such controls. One administration official suggested access could be restored within weeks once government systems are “hardened.” Anthropic is private, so there is no direct stock to trade, but backers Amazon and Alphabet carry indirect exposure, and the listed AI complex could re-rate on whatever valuation an Anthropic debut sets. Rival OpenAI is also preparing a confidential filing. (Axios)

Sensei’s Insight: Anthropic is IPO-bound at a valuation some bankers peg above $1 trillion, so this is no sideshow. The question is whether Commerce restores access in weeks, as one official suggested, or whether a multi-week security review becomes the standard that hangs over every frontier model launch from here.

🚀 SpaceX’s Record Debut Holds, but July Is the Test

Elon Musk’s SpaceX pulled off the largest stock market debut in history, and the pop held. Priced at a fixed $135 a share, the stock opened at $150, ran as high as about $169 and closed its first session up 19% at $160.95, valuing the rocket and satellite company at roughly $2 trillion, more than Tesla. Since its debut late last week it has held near $160, trading between about $149 and $176. The listing raised about $75 billion, beating Saudi Aramco’s 2019 record as the largest ever, and set aside an unusually large slice for ordinary investors, around a fifth of the deal against the usual handful of percent. (CNBC)

The climb is mechanical as much as fundamental. Only about 4% of the company trades freely, retail buyers are frozen by anti-flip penalties for two to four weeks, index funds are about to be forced to buy it, and the banks are propping the $135 price through a greenshoe option that works as a soft floor. That is a setup built to rise. The fundamentals are harder: at the offer price the stock trades near 94 times revenue, against about 23 for Nvidia, on a company that lost $4.3 billion last quarter as its AI arm burns roughly a billion a month. Every independent valuation lands below $135; every bank target sits above it.

The same engineering reverses in the second half of the year. The first real test comes in mid-July, when retail flip windows open and the greenshoe support lapses, taking the $135 floor with it. After that, supply only grows: roughly $660 billion of insider stock, held by funds sitting on hundred-fold gains and by thousands of newly minted employee millionaires, unlocks on a published schedule from late August through December, against a starting float of $75 billion. The near-term flows point up first, with likely fast-track entry into the MSCI and Nasdaq 100 indices forcing more buying into early July. The shape this rhymes with is a summer peak, then a grind lower into the first earnings report, now set for early September. (Nasdaq)

Sensei’s Insight: We published the playbook before the open and called it: a $150 to 180 debut. It landed. The harder part is ahead, when the props floating this, frozen retail and forced index buying, expire in mid-July and the $660 billion supply wave starts to test it.

📦 Trump Rebuilds the Tariff Wall, Court-Proof This Time

After the Supreme Court struck down Trump’s emergency tariffs in February, the administration is rebuilding the same trade pressure through a slower but sturdier legal tool. The Office of the US Trade Representative on June 2 proposed new tariffs of 10% to 12.5% on imports from 60 economies, including China, the European Union, Japan, and Mexico, citing their failure to ban goods made with forced labor. The mechanism is Section 301 of the Trade Act of 1974, which allows tariffs after a formal investigation, unlike the emergency law the court rejected. The duties are not yet in effect: public comments run through July 6, with a hearing July 7. (CNBC)

Tariffs are a tax on imports, and importers typically pass much of the cost to consumers, so this feeds the same inflation that has the Fed leaning hawkish. The forced-labor finding is the legal vehicle, but the rates closely mirror the country-by-country duties Trump had set before the courts intervened, so the policy goal looks unchanged while the legal machinery is new. A stopgap 10% surcharge under a separate authority expires in late July, which is why the July hearing is timed to let these duties take over without a gap. A second Section 301 wave, targeting “excess industrial capacity,” is in the pipeline, and a joint review of the US-Mexico-Canada trade pact is running in parallel, adding a front for autos and North American supply chains. (NBC News)

Sensei’s Insight: The timing is deliberate. The 10% stopgap tariffs expire in late July, and the July 7 hearing lines these Section 301 duties up to replace them without a break. Nothing is in effect yet, but apparel and retail importers sourcing from the named economies carry the clearest exposure to watch into the hearing.

Stories You Might Have Missed

🛢️ Iraq Races to Keep Its Northern Oil Flowing

Iraq’s state oil marketer asked Turkey to extend the Kirkuk-Ceyhan pipeline agreement for at least a year while a new deal is negotiated, with the current pact set to expire on 27 July. The line is a major northern export route to the Mediterranean, historically capable of moving well over a million barrels a day, though it has run far below that. With the Strait of Hormuz disrupted through most of the war, Baghdad leaned on this northern channel as one of its few alternative outlets, so a lapse would squeeze the supply of OPEC’s second-largest producer just as the market is trying to rebalance. Even with the Iran deal pointing toward Hormuz reopening, the late-July deadline keeps this a live supply risk for oil. (Reuters)

🕊️ Trump Works Putin and Zelenskyy Before G7

Trump spoke by phone yesterday with both Vladimir Putin and Volodymyr Zelenskyy, pressing to end the Russia-Ukraine war ahead of the Group of Seven summit in France this week. The Putin call ran just under an hour; Zelenskyy called his exchange a “wonderful conversation” and said both agreed to talk further at the summit. A settlement would ripple through European energy, defence budgets and commodity flows, while Ukraine’s continued strikes on Russian oil infrastructure keep some upward pressure on crude. The cross-current for investors: peace in both Ukraine and Iran at once would be a clear headwind for defence stocks, which have already drifted lower on easing-conflict optimism. (AP)

💵 Lazard Undercuts Rival for Venezuela’s Debt Mandate

A fee fight has broken out over one of the largest sovereign debt restructurings ever attempted. Investment bank Lazard sent a letter to Venezuela’s interim President Delcy Rodríguez offering to take over as financial adviser for $25 million, a fraction of the roughly $150 million that rival Centerview Partners had been negotiating. Venezuela hired Centerview last month without a competitive tender to restructure about $60 billion in defaulted government and state oil debt, with total liabilities estimated above $150 billion, a no-bid process that drew criticism over fairness. The terms an adviser strikes shape how big creditor losses end up, and the defaulted bonds, which many US funds hold, have rallied toward multi-year highs as the country edges toward a deal. The cleanest equity proxy is Lazard itself, listed in New York, for which a mandate this size would be both a fee and a prestige win. (Bloomberg)

⚽ The World Cup Kicks Off a Spending Wave

The men’s football World Cup has returned to North America for the first time in over three decades, and Wall Street is already mapping who cashes in. Hosted across the United States, Canada and Mexico, the tournament running through mid-July is expected to draw 6.5 million fans and add about $17 billion to US GDP, according to figures cited by JPMorgan. The bank points to beneficiaries in digital advertising, which could see around $5 billion in extra spend, along with online travel, ride-hailing, rental cars, airports and brewers. One caveat worth keeping in view: academic work on past tournaments finds the headline GDP boost rarely shows up at the national level, since much of it is local spending shuffled around rather than new money. Host-country shares have, though, historically returned about 10% in World Cup years. (CNBC)

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍 Deep Dive:

Later today I'll be releasing the playbook for the Japanese interest rate decision landing tonight into tomorrow morning. Make sure you keep an eye out for that email.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.