Morning Forecast: Monday, 30 March

The Fed Hasn't Raised Rates Since 2023. That Might Change Today.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

Quick note for all premium members: keep an eye out for correspondence over the next 48 hours so you can get access to the training course and the Discord integration.

👀 Today’s Stories at a Glance

🚨 The War Just Got Bigger: Houthis fire on Israel, a second chokepoint is now in play, and Brent crude is up 55% this month.

🎓 Powell Takes the Stage Unscripted: Rate hike odds have crossed 50% for the first time this cycle. Every word at Harvard moves markets.

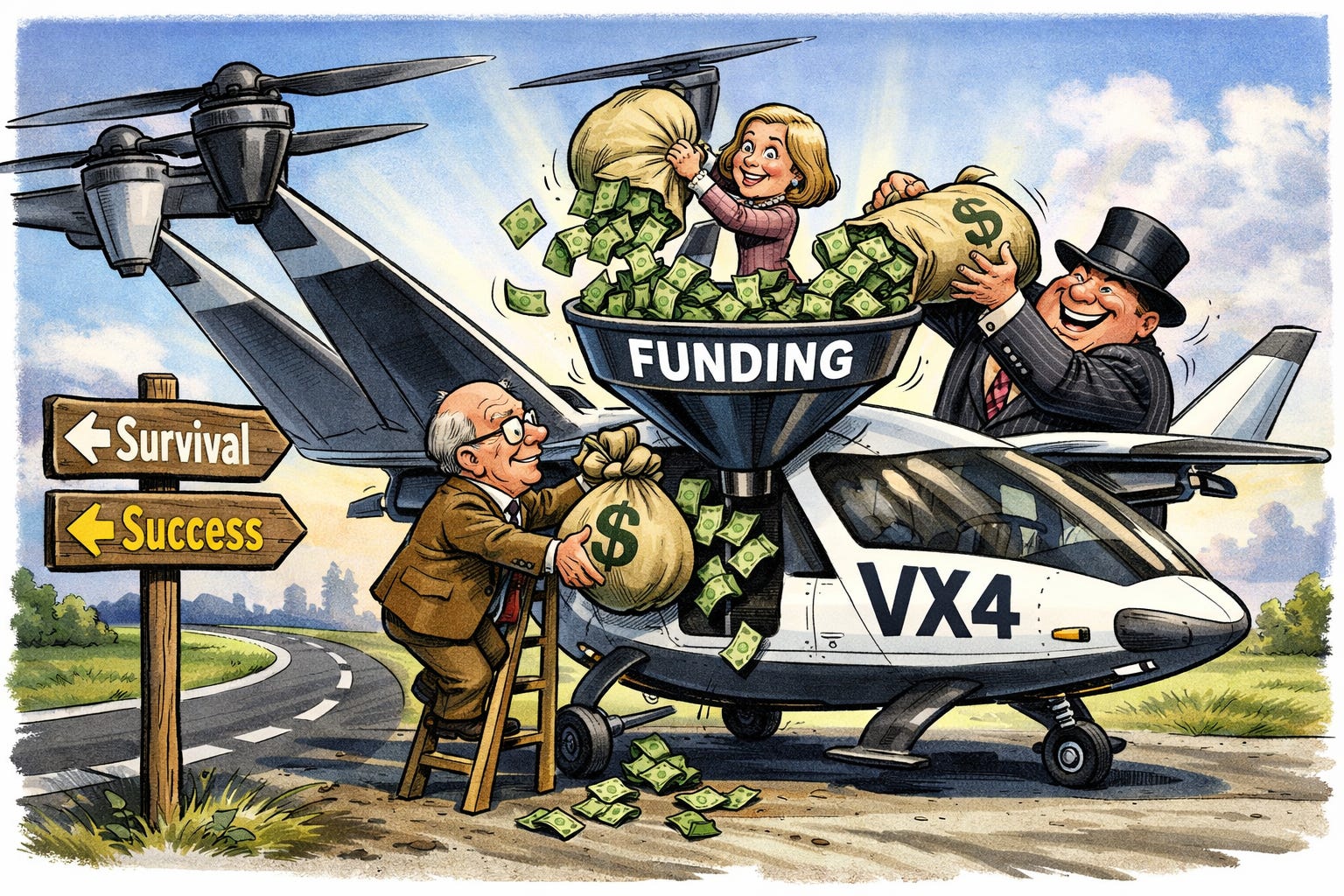

✈️ Vertical Aerospace’s $800M Signal: A reported mega-raise would fund the final push to certification and a path to flights by 2028.

🪨 Iran Bombs the World’s Aluminum Supply: Strikes on two of the largest smelters have knocked out production capacity that takes years to rebuild.

🚀 SpaceX IPO Could Land Any Day: A $1.75 trillion valuation, $75 billion raise, and 30% retail allocation would shatter every record.

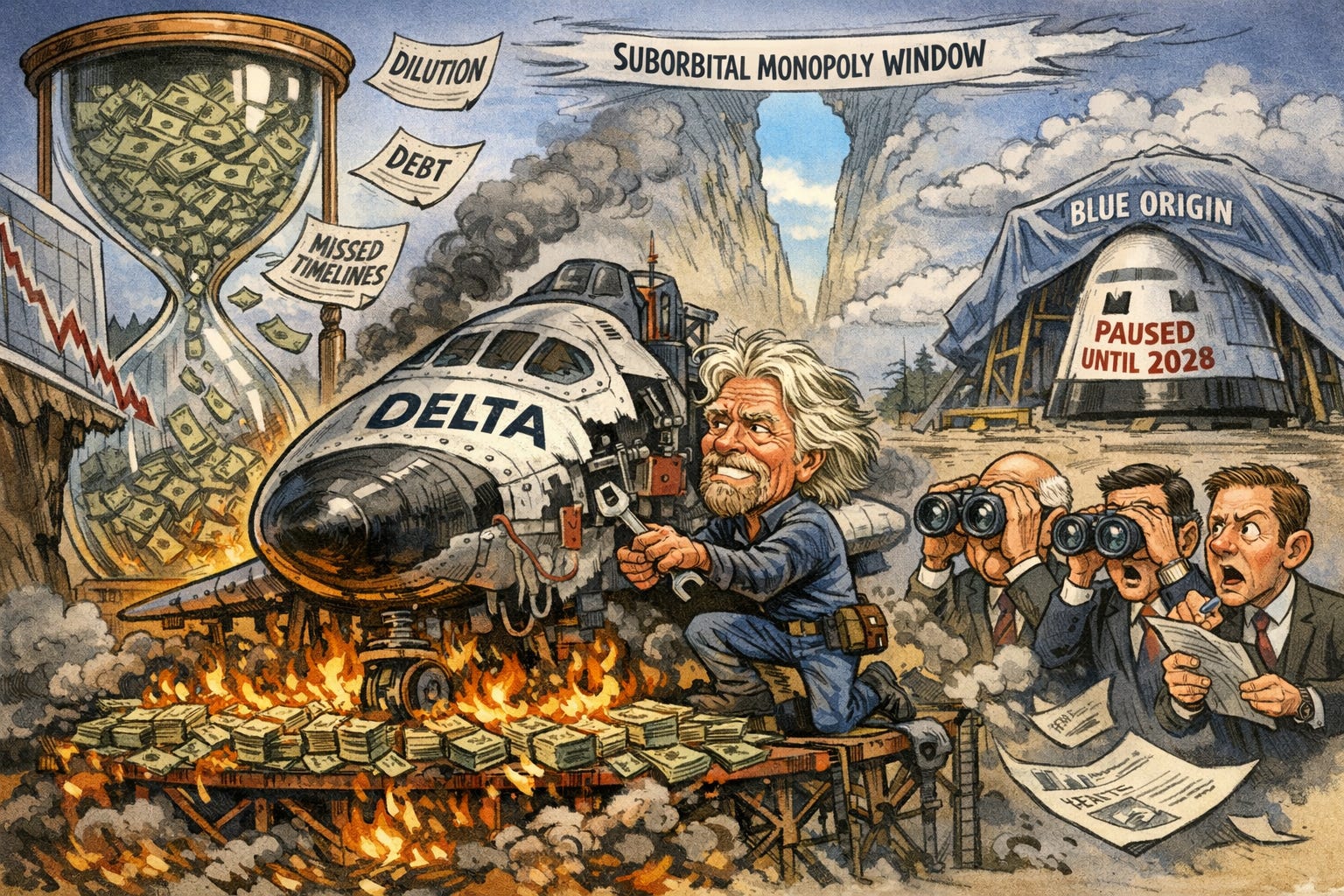

🔍 Virgin Galactic’s $165M Survival Test: Tonight’s earnings call reveals whether the cash runway holds long enough for Delta to fly.

🧠 One Big Thing

The Dual-Chokepoint Energy Crisis

The Houthis have entered the Iran conflict, and with that, the war now threatens both of the Middle East’s critical oil transit routes at the same time. The Strait of Hormuz has been contested since the conflict began. The Bab el-Mandeb Strait, connecting the Red Sea to the Gulf of Aden, is now in play. Together, these two waterways handle the vast majority of the region’s seaborne oil exports, and there is no alternative route that comes close to replacing them at current volumes. Brent crude has surged more than 55% this month alone. The US is sending thousands of additional troops. Société Générale warned this morning that a simultaneous disruption at both chokepoints would produce the most severe oil supply shock ever recorded. This is no longer a regional conflict with energy side effects. It is an energy crisis with a war attached to it.

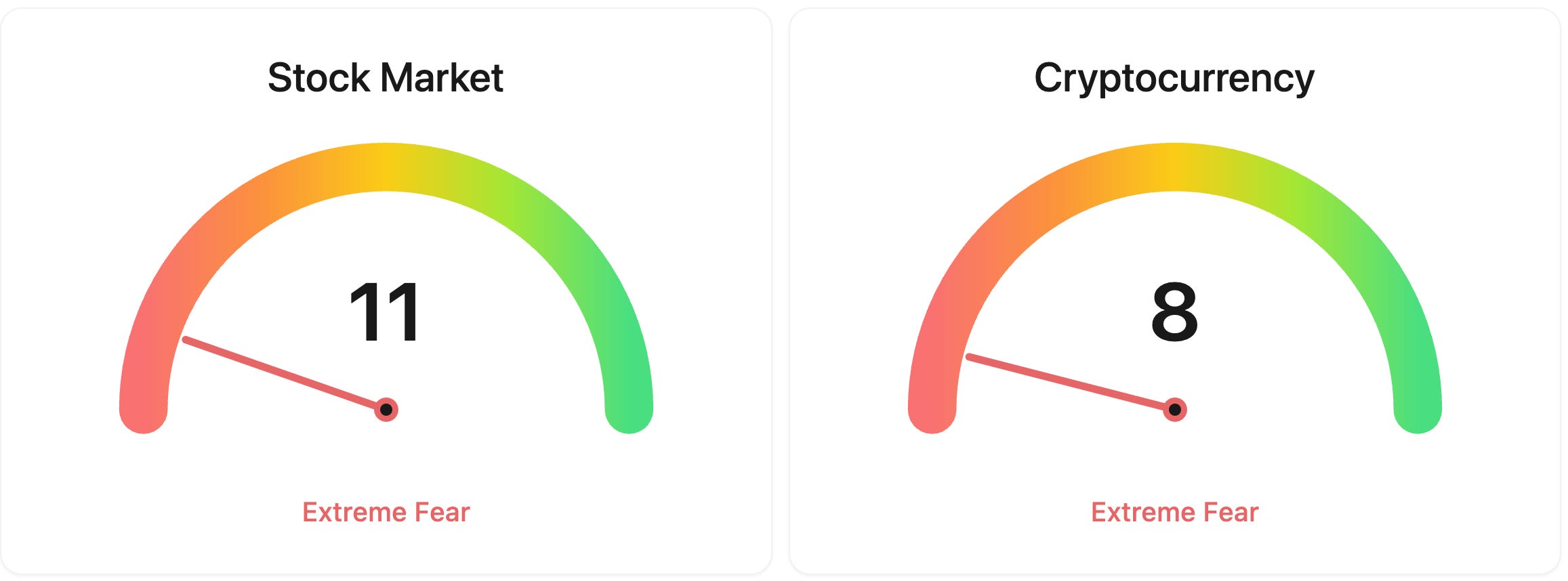

⚖️ Fear & Greed

📉 The Number That Matters

$116.75

Brent crude reached $116.75 per barrel after Houthi militants entered the Iran conflict. The price represents a 55% monthly surge, the largest on record, as markets price in threats to the Bab el-Mandeb oil chokepoint.

⚔️ Winners vs Losers

Winners

PRQR 0.00%↑: ProQR Therapeutics surged ahead of a virtual investor and analyst event scheduled for April 8, where the company plans to unveil the primary indication for its lead RNA editing candidate AX-0810 and announce new pipeline programs with upcoming clinical data readouts.

UTHR 0.00%↑: United Therapeutics jumped as investors positioned ahead of the imminent TETON-1 data readout, a pivotal Phase 3 trial of nebulized Tyvaso in idiopathic pulmonary fibrosis expected in the first half of 2026 that would support an FDA supplemental filing alongside the already-published TETON-2 results.

SGML 0.00%↑: Sigma Lithium surged ahead of its Q4 2025 earnings release this morning, with elevated premarket volume reflecting optimism after recent operational progress including resumed premium lithium oxide sales and a $96 million production-backed revolving credit facility closed earlier in Q1.

Losers

VRDN 0.00%↑: Viridian Therapeutics collapsed in premarket on what appears to be a negative or disappointing readout from the REVEAL-1 Phase 3 trial of subcutaneous elegrobart in active thyroid eye disease, the company's most critical near-term catalyst which was expected to deliver topline data in Q1 2026. A confirmed press release had not yet been published at the time of research.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $67,551 (▲ 2.41%)

Ethereum (ETH): $2,062 (▲ 4.00%)

XRP: $1.35 (▲ 1.76%)

Equity Indices (Futures):

S&P 500: $6,410 (▲ 0.88%)

NASDAQ 100: $23,433 (▲ 0.45%)

FTSE 100: £10,061 (▲ 1.71%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.37% (▼ 1.26%)

Oil (WTI): $101 (▼ 0.30%)

Gold: $4,542 (▲ 1.09%)

Silver: $71.14 (▲ 2.00%)

Data as of: UK (BST) 12:27 / US (EDT): 07:27 / Asia (Tokyo): 21:27

✅ 5 Things to Know Today

🚨 The War Just Got Bigger: Houthis Enter, a Second Chokepoint Looms, and Trump Wants Iran’s Oil

The Iran war entered its fifth week with a significant escalation over the weekend. Yemen’s Iran-backed Houthi militants fired ballistic missiles at Israel yesterday, their first direct involvement in the conflict, and vowed to keep fighting until US-Israeli attacks on Iran and its allied groups cease. The same weekend, a US amphibious assault group carrying around 3,500 Marines and sailors arrived in the region with fighter aircraft and ground assault equipment, and reports emerged that the Pentagon is weighing whether to send up to 10,000 additional troops. Brent crude surged as much as 3.7% this morning to $116.75 a barrel, putting the benchmark on track for a monthly gain of more than 55%, which would be the largest ever recorded. Asian equity markets fell sharply at the open before paring losses as the session progressed (Bloomberg).

The Houthi entry has introduced a threat that markets were not fully pricing before the weekend. The Bab el-Mandeb Strait, the narrow waterway connecting the Red Sea to the Gulf of Aden through which roughly 4 to 5 million barrels of oil pass per day, sits squarely within Houthi range. Analysts at Societe Generale warned this morning that if the Houthis move to restrict that route, the knock-on effect on Saudi Arabia’s East-West pipeline could remove a further 5 million barrels per day from global markets. That pipeline, currently the last major alternative oil export route, is already running at its full capacity of 7 million barrels per day. Energy historian Daniel Yergin, vice chairman of S&P Global, said a combined disruption at both Hormuz and Bab el-Mandeb could produce the most severe oil supply shock in recorded history (Axios).

Diplomatic signals over the weekend were contradictory. President Trump told reporters on Air Force One that Iran “gave” the US most of the 15 demands it had sent to Tehran, without specifying what concessions had been offered, a claim Iran publicly rejected. Trump also told the Financial Times he wants to “take the oil in Iran,” describing a military seizure of Kharg Island, Iran’s main export hub, as his preferred outcome, and separately suggested the US has already achieved regime change through the killing of Supreme Leader Khamenei. Pakistan said this morning it is ready to host US-Iran peace talks within days, after foreign ministers from Pakistan, Saudi Arabia, Turkey, and Egypt met in Islamabad over the weekend. Markets are paring early losses slightly on the diplomatic headlines, but analysts at RBC Capital Markets noted Trump has repeatedly claimed progress in negotiations only for Tehran to flatly contradict him (Bloomberg).

Sensei’s Insight: Iran controls Hormuz and the Houthis control Bab el-Mandeb. The two chokepoints together handle the vast majority of the Middle East’s seaborne oil exports. A coordinated closure of both, even partial, would leave no viable alternative route for Gulf oil at the volumes the world currently needs. The Pakistan diplomacy may provide a circuit-breaker, but Tehran has rejected every US proposal publicly so far. Watch Bab el-Mandeb shipping data as closely as Hormuz from here.

🎓 Powell Takes the Stage at Harvard: Every Word Will Move Markets

Federal Reserve Chair Jerome Powell will sit down for a moderated discussion with Harvard University’s introductory economics class at 10:30am Eastern time this morning, roughly 3:30pm London time, at Sanders Theatre on campus. No prepared remarks are planned, making it one of the few recent appearances where he speaks entirely without a script. The timing is unusually charged. The Fed held rates steady at 3.5% to 3.75% at its March meeting, with its dot plot projecting just one quarter-point cut for the full year. Since then, the probability priced into futures markets of a rate hike before year-end has crossed 50% for the first time in this cycle, a sharp reversal from the broad expectation of cuts that defined the early 2026 outlook. Brent has added more than 55% since March began, and the Organization for Economic Co-operation and Development (OECD) now forecasts US inflation at 4.2% for 2026, well above the Fed’s own 2.7% projection (Barron’s).

Markets will be listening for three things. First, whether Powell signals the Fed is moving closer to considering a rate hike or holds the line on the wait-and-see framing from the March meeting. Second, whether he adds clarity on the oil shock and the question of “looking through” energy-driven inflation. He broke with standard central bank practice at the March press conference by explicitly stating the Fed was not prepared to simply ignore the oil price surge, and any elaboration on that position matters enormously for bond pricing. Third, whether he touches on the institutional pressure bearing down on the Fed. His chairmanship expires on 15 May, the Justice Department probe into him continues after a judge quashed subpoenas and prosecutors vowed to appeal, and Senator Thom Tillis has blocked nominee Kevin Warsh’s Senate confirmation hearing until the legal matter is resolved. Powell accepted the Paul Volcker Public Integrity Award at the weekend, invoking Volcker’s willingness to hold firm against political pressure, a signal widely read as directed at the White House (CNBC).

Sensei’s Insight: Rate hike probability crossing 50% is the quiet bomb in this week’s data. The Fed has not raised rates since 2023. If Powell says anything at Harvard that even gently validates the hiking scenario, or simply fails to push back on it, it could accelerate a bond repricing that tech stocks and growth names are not yet fully discounting. Watch two-year Treasury yields as the real-time signal during and after the speech.

✈️ Vertical Aerospace’s $800M Funding Leak Signals a Turning Point

Contributed by Vaz

Vertical Aerospace is a UK-based electric aviation company developing the VX4, an electric vertical take-off and landing (eVTOL) aircraft designed for urban and regional air mobility. Positioned as one of Europe’s leading players alongside global competitors such as Joby Aviation and Archer Aviation, the company has progressed into the final phase of piloted testing, the most critical stage of validation ahead of certification. Reports of a potential $800 million funding raise have now emerged, which, if confirmed, would align directly with this phase of the programme. Rather than early-stage capital, this would represent targeted funding to complete certification, scale production readiness, and support a roadmap that includes potential UK passenger flights as early as 2028, a path to cash-neutral operations by 2029, and profitability as early as 2030.

Until now, investor sentiment has been heavily influenced by concerns over Vertical’s financial position and its ability to secure sufficient capital, particularly in a challenging geopolitical environment where funding has become more constrained and risk-sensitive. This uncertainty has weighed on the stock and driven a narrative centred on survival. The reported $800 million raise, even at this unconfirmed stage, begins to shift that perspective toward structured execution, especially when viewed alongside increasing customer interest in the VX4, continued supplier alignment, and disciplined capital messaging from management.

Vaz’s Insight: We have followed Vertical Aerospace very closely on their journey, dedicating substantial airtime to the company on our channel, hosting them on multiple occasions, and delivering a significant amount of exclusive content, often world-first within our network. As a result, we have built a strong base of investors and enthusiasts closely following Vertical’s story. There has been clear fear among investors in recent months, and this development, even if not yet confirmed, brings important clarity in what has been a challenging environment. Management has consistently presented a disciplined and structured strategy, and as more of these elements come together, the bigger picture is starting to emerge.

🪨 Iran Targets Two of the World’s Biggest Aluminum Plants. The Metal Surged 6%

Iran’s Islamic Revolutionary Guard Corps struck two of the world’s largest aluminium smelters over the weekend, reshaping the global supply picture for a metal used in everything from aerospace components to food packaging and solar panels. Emirates Global Aluminium (EGA), the Middle East’s biggest producer, reported significant damage to its Al Taweelah facility in Abu Dhabi’s Khalifa Economic Zone after missile and drone strikes. The site produced 1.6 million metric tonnes of cast metal last year. Aluminium Bahrain, also known as Alba, which operates the world’s largest single-site smelter at an annual capacity of 1.623 million metric tonnes, confirmed two employees were injured and said it was still assessing the extent of the damage. London Metal Exchange aluminium prices surged as much as 6% to $3,492 per tonne at today’s open. Shares in Australian producers jumped in response, with Alcoa up 11% and South32 climbing 6.7% (Bloomberg).

The strikes compound disruption that was already building before this weekend. Gulf aluminium producers, which account for roughly 9% of global primary supply, had already been unable to ship via normal channels since the Strait of Hormuz effectively closed at the end of February. Alba had declared force majeure on March 4, formally notifying buyers it could not fulfil delivery obligations due to circumstances beyond its control, and had already shut 19% of its production capacity as a precautionary measure. Iran said the strikes were retaliation for US-Israeli attacks on Iranian steel plants, citing both producers’ ties to US military and aerospace supply chains. EGA and Alba both supply Boeing and Airbus with premium aluminium alloys. EGA had separately announced plans last year to build a $4 billion smelter in Oklahoma, a project designed to give US manufacturers more supply security from a Gulf partner. That plan now sits against a backdrop of significant damage to the same company’s core facilities. The US Midwest aluminium premium, the additional cost American buyers pay above the London benchmark for physical metal, hit a record $1.10 per pound this week (The National).

Sensei’s Insight: Aluminium is the war’s first direct industrial escalation beyond oil and gas. The Hormuz closure hurt supply by disrupting shipping routes. These strikes hit production capacity itself, and damage to smelting infrastructure takes months or years to repair, not days. China produces around 60% of global supply and could partially cushion the shortfall, but the cost and logistics of redirecting that volume to aerospace and packaging buyers currently sourcing from the Gulf will show up in earnings guidance before it shows up in headlines. Watch Boeing, Airbus, and consumer packaging names in the coming earnings season.

🚀 SpaceX’s IPO Prospectus Could Land Any Day. Here Is What Investors Need to Know

SpaceX is expected to confidentially file its initial public offering (IPO) prospectus with the Securities and Exchange Commission imminently, according to reporting from the Wall Street Journal, The Information, and Reuters, with none of those reports independently confirmed by SpaceX itself. The company is reportedly targeting a $1.75 trillion valuation and a capital raise of up to $75 billion, which would make it the largest public offering in financial history by a margin of more than two and a half times, eclipsing Saudi Aramco’s then-record $29.4 billion listing in 2019. A June listing date is under discussion. None of these figures are confirmed: they are based on sources close to the process, and the timeline remains subject to change. What is not speculative is the underlying business. SpaceX’s Starlink satellite internet division had approximately 9.2 million subscribers at the end of 2025 and generated more than $10 billion in revenue last year, with analyst projections for 2026 ranging between $15.9 billion and $24 billion. SpaceX also commands roughly 80% of the commercial rocket launch market (Reuters).

The structure of the offering, if it proceeds as reported, is deliberately unconventional. Musk’s chief financial officer Bret Johnsen has communicated to investment banks that the company is considering allocating up to 30% of shares to retail investors, at least three times the standard 5% to 10% reserved for individuals in a typical listing. Morgan Stanley would use its E*Trade platform to reach smaller investors, Bank of America would target family offices and high-net-worth clients, and UBS and Citigroup would handle global and international distribution respectively. Musk is also reportedly considering an extended lock-up period beyond the standard six months on major early shareholders to reduce the risk of a post-listing institutional sell-off. The prospectus faces regulatory scrutiny around how the February 2026 merger with xAI, Musk’s artificial intelligence company, is disclosed inside the combined entity, which has already pushed the filing back from its original February target. The confidential filing process, a standard pathway for large listings, means the documents will be reviewed privately by regulators before any public roadshow begins (CNBC).

Sensei’s Insight: The 30% retail allocation is the headline within the headline. A typical IPO reserves 5% to 10% for individual investors, with institutions getting the rest and often flipping shares on day one. If Musk follows through, it sets a precedent for how the biggest listings treat retail investors. But the valuation deserves scrutiny: $1.75 trillion is roughly 20 times Starlink’s 2025 revenue, and the prospectus, when it arrives, will be the first time the market can actually stress-test those numbers.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: Virgin Galactic: A $165 Million Bet on a Spaceship That Doesn’t Exist Yet

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.