Morning Forecast: Monday 6 July

SpaceX joins the Nasdaq-100 and forces a $27 billion buy, while chips lead Wall Street’s reopen higher

👀 Today’s Stories at a Glance

💻 Chips lead the reopen: analyst upgrades lift the group off its worst week of the year as Nasdaq-100 futures climb over 1%.

🚀 SpaceX enters the Nasdaq-100: index funds must buy about $27 billion of stock tomorrow, chasing a float of barely 3% to 5%.

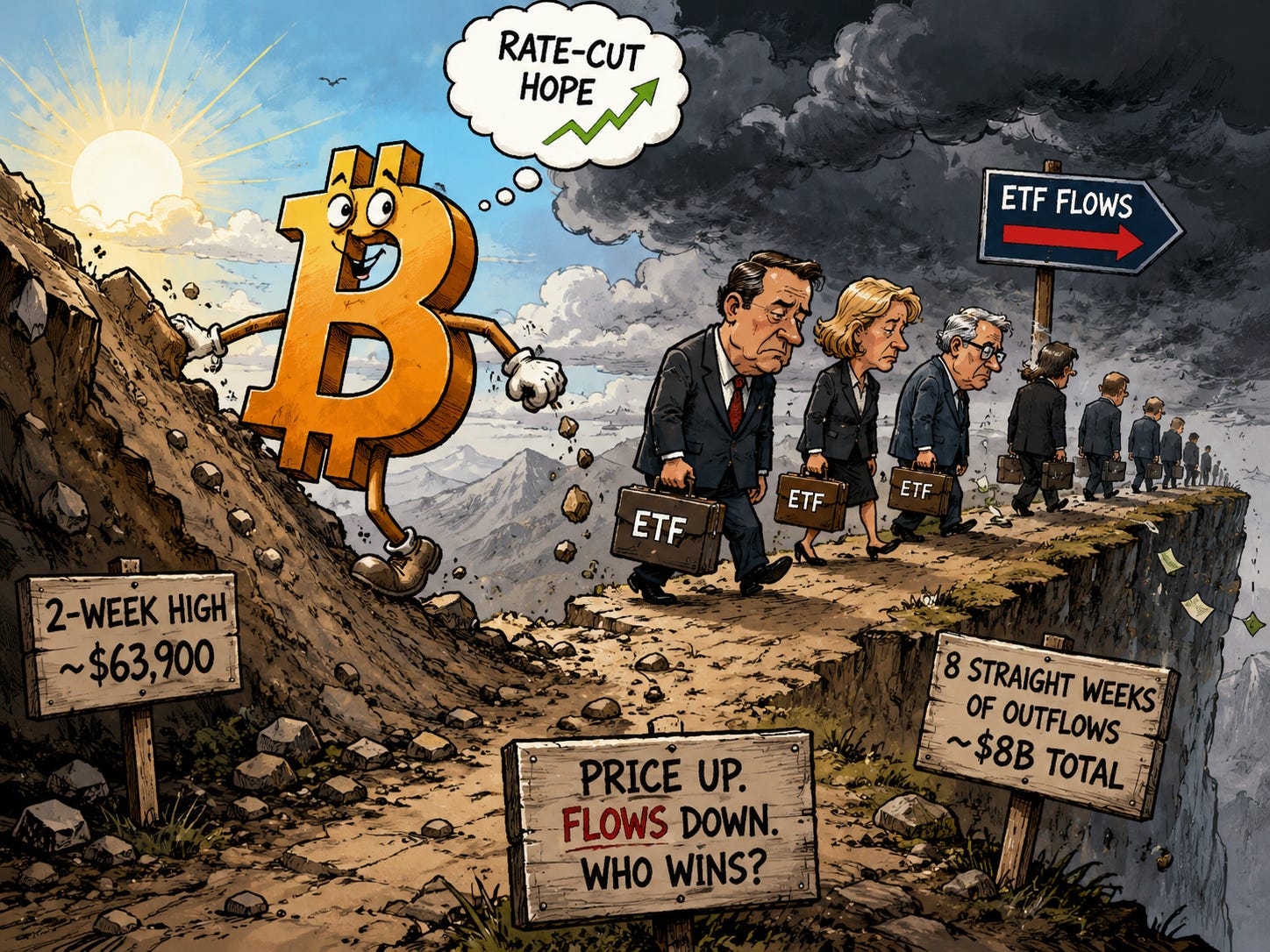

₿ Bitcoin’s two-week high: the coin hit near $63,900 at the reopen on the soft jobs print, even as ETFs bled an eighth week.

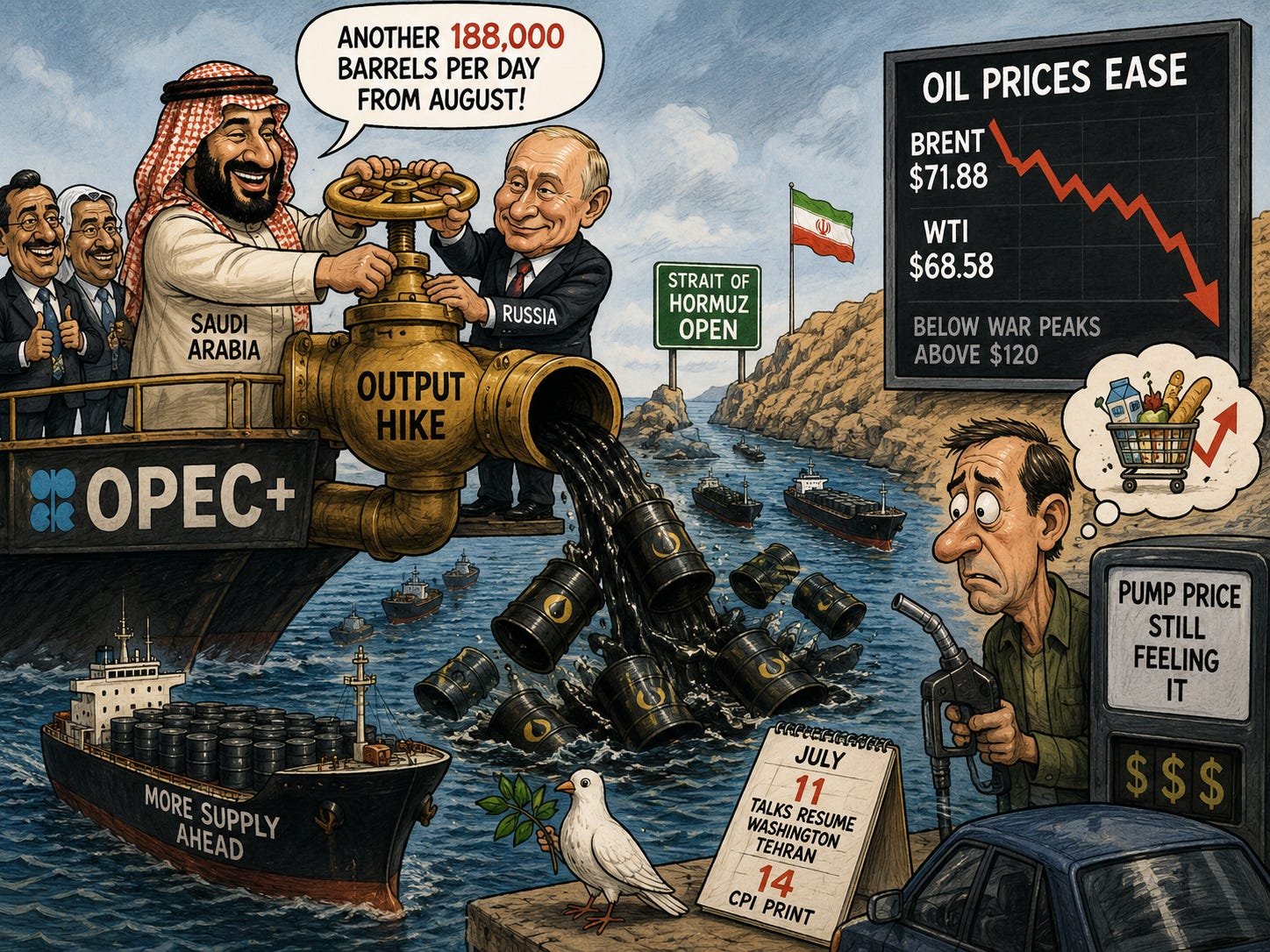

🛢️ OPEC+ opens the taps: the group approved another 188,000 barrels a day from August, pulling Brent and WTI to pre-war lows.

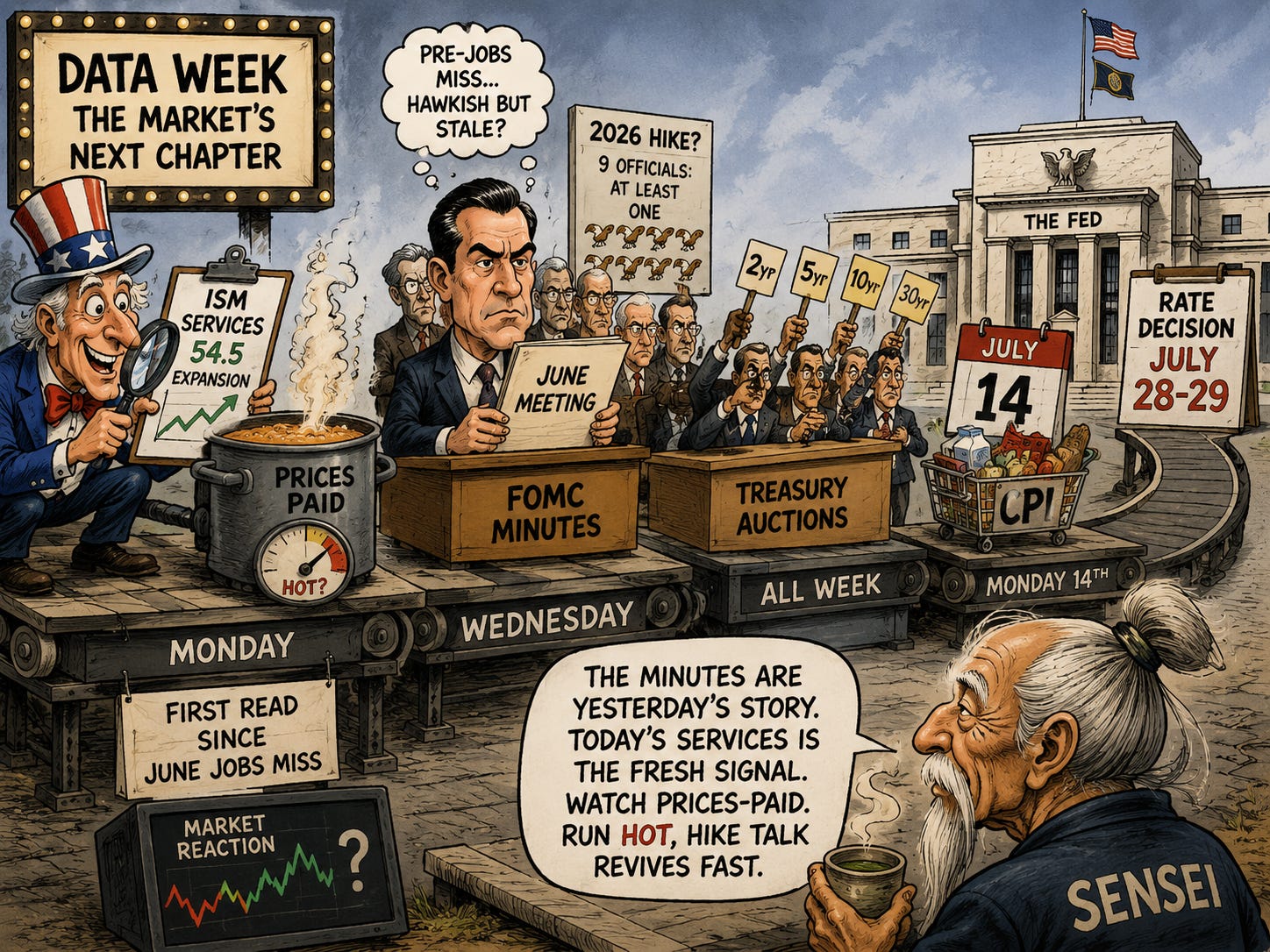

🏛️ The data week begins: ISM services lands today, the first read since the jobs miss, with Warsh’s first minutes due midweek.

🥇 Gold holds near a high: rate-cut bets keep bullion firm around $4,183, its first weekly gain in five, with silver near $62.

⚽ World Cup last eight: all four quarter-finals play on US soil from the 9th, a quiet consumer-spending lift for host cities.

📈 Chart of the Day: XRP was rejected at the multi-year trendline near $1.16, its bull/bear line; below points to $1, above opens $1.30.

🧠 One Big Thing

The reopen is rewarding exactly what it punished a week ago. The same chip names that fell double digits on fears AI spending had outrun demand are being lifted this morning by upgrades built on AI spending staying strong: Morgan Stanley across the equipment makers, Bernstein raising ASML by more than 30%. Nothing in the fundamentals changed over a three-day weekend. Only the analyst framing did, which makes the bounce a positioning move rather than new information. The season that starts on the 9th is where the 148% projected chip profit surge either validates the rebound or exposes it. Watch guidance from the chip complex, not the tape between now and then.

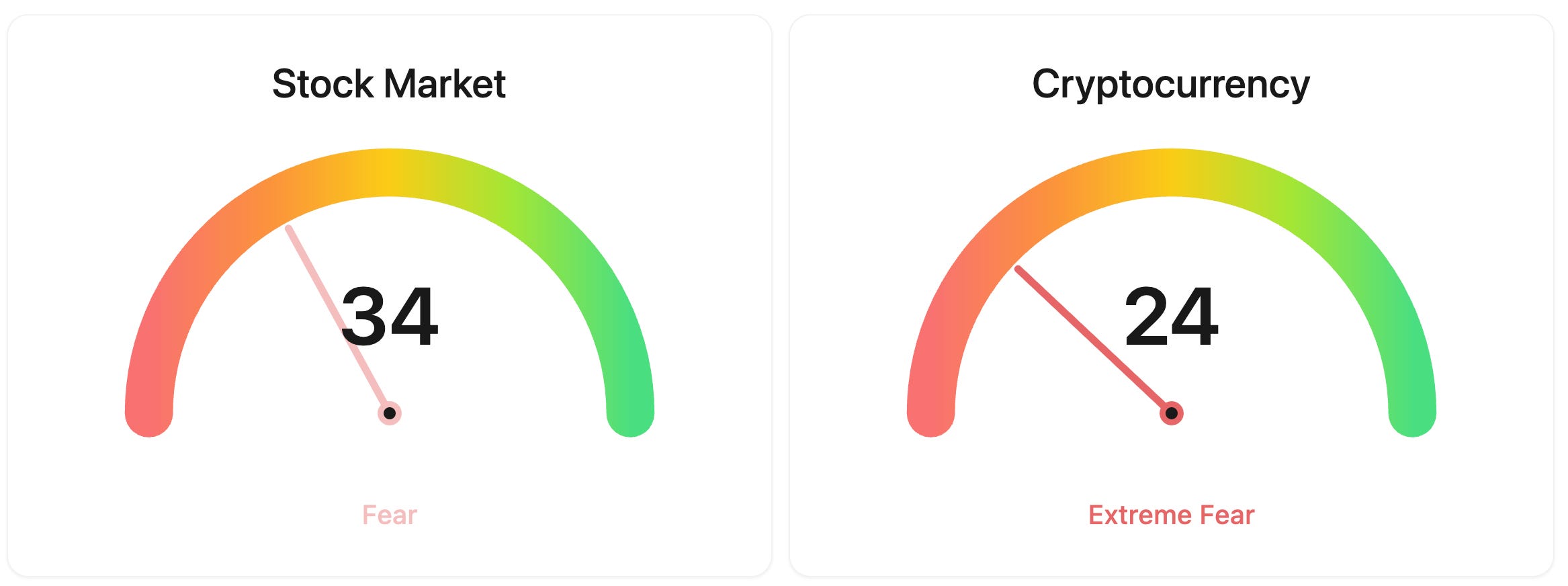

⚖️ Fear & Greed

📉 The Number That Matters

$27 billion

Index funds are forced to buy roughly $27 billion of SpaceX at tomorrow’s Nasdaq-100 rebalance, and its public float is only 3% to 5% of the company, so that demand chases a very thin pool of shares.

⚔️ Winners vs Losers

Winners

SEER 0.00%↑: Seer, Inc. surged after its chairman and CEO Omid Farokhzad delivered an unsolicited, non-binding proposal to take the proteomics company private at $2.45 per share in cash plus two contingent value rights, a steep premium to its recent close. Shares got a further lift from an investor presentation filed ahead of the July 28 annual meeting as the company fights an activist proxy campaign.

WULF 0.00%↑: TeraWulf Inc. jumped after announcing an AI data center lease with Anthropic at its Justified campus alongside the sale of its majority stake in the Abernathy joint venture to Fluidstack, a package the company projects will generate roughly $19 billion in revenue and that deepens its pivot from bitcoin mining toward high performance computing.

Losers

DDOG 0.00%↑: Datadog, Inc. slipped after Bernstein SocGen downgraded the cloud observability company to Market Perform from Outperform, flagging softening demand across enterprise and AI Lab customers and warning that investor expectations had run ahead of the underlying demand environment.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $61,635 (▼ 3.08%)

Ethereum (ETH): $1,737 (▼ 2.63%)

XRP: $1.11 (▼ 3.68%)

Equity Indices (Futures):

S&P 500: 7,563 (▲ 0.45%)

NASDAQ 100: 29,918 (▲ 1.22%)

FTSE 100: 10,646 (▲ 0.20%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.46% (▼ 0.58%)

Oil (WTI): $68 (▼ 0.25%)

Gold: $4,134 (▲ 0.28%)

Silver: $61.51 (▲ 0.87%)

Data as of: UK: 1:49pm BST / US: 8:49am EDT / Asia (Tokyo): 9:49pm JST

✅ 5 Things to Know

💻 Chips lead the reopen after their worst week

Wall Street reopens from the long holiday with the chip complex bouncing hard on a wave of analyst upgrades. Morgan Stanley raised price targets across the semiconductor-equipment makers, sending Lam Research, Applied Materials and KLA up around 4% before the bell, while Bernstein lifted its target on ASML by more than 30%, to roughly $2,623, pushing the Dutch lithography maker up about 4% too. Nasdaq-100 futures rose more than 1%. The rebound follows the Philadelphia Semiconductor Index’s near 10% fall last week, its worst of the year, on fears that AI spending had run ahead of real demand (Yahoo Finance).

The reversal rests on the same AI-capex story that drove the sector all year, with the biggest cloud operators still guiding to hundreds of billions in data-centre spending this year. Over a three-day weekend the fundamentals did not move; the framing did. The real test arrives on the 9th, when earnings season opens and the chip names have to turn those higher targets into numbers. Consensus has semiconductor profits surging about 148% this quarter, roughly 11 points of the entire S&P 500 growth rate, which leaves the group that just whipsawed carrying the season (Forbes).

Sensei’s Insight: The bounce and the selloff share one cause: nobody knows whether AI capex holds. Last week the doubt won, this week the upgrades did, on no new data. Guidance from the 9th settles it. The moves in between are positioning.

🚀 SpaceX enters the Nasdaq-100 tomorrow

SpaceX joins the Nasdaq-100 before tomorrow’s open, less than a month after its record $1.75 trillion listing on 12 June, the largest IPO ever staged. The index change forces every fund tracking the Nasdaq-100 to buy the stock at the rebalance, an estimated $27 billion of passive demand, including about $4.3 billion from the QQQ ETF alone. Because only 3% to 5% of SpaceX shares trade freely, that buying chases a very small float. The stock edged up about 1% before the bell, to around $163.75 (Yahoo Finance).

The mechanics matter more than the milestone. To fund the SpaceX purchase, index funds have to trim every other Nasdaq-100 member, a quiet sell order spread across the biggest tech names on the same morning. The S&P 500 took the opposite path, rejecting a fast-track in early June and holding SpaceX out until at least mid-2027 on its profitability and seasoning rules. A thin float meeting forced demand is the classic setup for a sharp move in either direction, once the passive bid is filled and active traders take the wheel.

Sensei’s Insight: Forced buying is not a vote of confidence, it is a rule. Funds must buy SpaceX tomorrow whatever they make of the price, into a float this small. What the stock does after that passive bid clears is the first honest read on real demand.

₿ Bitcoin hits a two-week high as flows lag

Bitcoin pushed to a two-week high near $63,900 as US markets prepared to reopen, easing back to around $62,600, up from the low-$60,000s it held through the three-day closure. The move tracks the soft June jobs report, whose 57,000 print cut Fed-hike odds, pulled Treasury yields down and softened the dollar, lowering the cost of holding an asset that pays no yield. Crypto was the only market open across the long weekend, so it carried the rate-cut trade on its own (Yahoo Finance).

The flows tell a different story. Spot Bitcoin ETFs have now run eight straight weeks of net outflows, roughly $526 million last week and more than $8 billion across the streak, after June closed as the worst month on record for the funds at about $4 billion withdrawn. A single strong session just before the holiday drew money in, but the week around it still finished negative. Price rising on macro while institutional money keeps leaving is a gap that rarely holds for long, and the reopen puts the funds back in play: the first prints of the week decide whether there is a floor under this bounce.

Sensei’s Insight: Price says one thing, ETF flows say another, and flows usually win that argument. Eight weeks of outflows into a two-week high is divergence, not confirmation. I am watching the first flow prints of the week far more than the candle on the chart.

🛢️ OPEC+ confirms the output hike, oil eases

OPEC+ approved another rise in output targets at its weekend meeting, adding 188,000 barrels per day from August, the fifth straight monthly increase, with Saudi Arabia and Russia carrying the largest shares. Oil slipped on the decision, Brent easing toward $71.88 and WTI toward $68.58, roughly where both traded before February’s strikes on Iran and far below the peaks above $120 during the conflict. The group is steadily unwinding the voluntary cuts it made to hold prices up while the war kept the Strait of Hormuz shut to its biggest producers (CNBC).

The extra barrels arrive into a market that is already loosening. With Hormuz reopening, quota rises that sat largely on paper during the war can turn into real cargoes, and Iranian crude is moving more freely. Talks between Washington and Tehran resume on the 11th once Khamenei’s funeral ends, with Hormuz transit fees, frozen assets and the nuclear file all on the table. For households the read is simple: a heavier crude market into autumn keeps fuel costs, and the inflation they feed, pointing lower, which matters into the CPI print on the 14th.

Sensei’s Insight: The paper barrels are turning real. Earlier rises added little while Hormuz was shut, but with the strait open, loadings can finally catch up to the quotas. That is the bearish risk a $72 Brent has not fully priced, and it lands just before CPI.

🏛️ ISM services opens a stacked data week

US markets reopen straight into the week’s first real data. The ISM services survey, the broadest read on the part of the economy that employs most Americans, lands this afternoon after the holiday pushed it back, with its prices-paid component watched as closely as the headline given the inflation debate. It sits at a prior 54.5, in clear expansion. This is the first fresh economic reading since June payrolls showed only 57,000 new jobs, a miss that roughly halved the odds of a Fed rate rise in September (Yahoo Finance).

The bigger event comes midweek. Minutes from the June FOMC meeting, the first chaired by Kevin Warsh, arrive midweek and should show how firmly the committee leaned toward a 2026 hike, with nine officials pencilling in at least one. The timing is awkward: those minutes describe a meeting held before the jobs miss, so hawkish language may read as stale on arrival. A run of Treasury auctions across the week tests appetite for government debt at today’s yields, and June CPI on the 14th is the last major inflation print before the decision due on the 28th and 29th.

Sensei’s Insight: The minutes are the record of a meeting the jobs data already overtook. Today’s services print is the fresher signal, the first read on the economy since the number that changed the rate path. Watch prices-paid: run hot, and the hike talk revives fast.

Stories You Might Have Missed

🥇 Gold holds near a two-week high

Gold held near a two-week high as the soft jobs report cooled expectations of another Fed rate rise, trading around $4,183 an ounce after posting its first weekly gain in five weeks, while silver slipped 0.6% to about $62.03 after touching its highest since late June. The metals are riding the same rate-cut trade lifting chips and Bitcoin: lower yields and a weaker dollar make assets that pay no income more attractive to hold. Bullion still sits well below January’s record above $5,500, and the swing factor from here is how convincingly this week’s data pushes the Fed off its hawkish stance (CNBC).

⚽ The World Cup reaches the last eight

The World Cup reaches its quarter-finals this week, with all four last-eight ties played on US soil from the 9th, in Foxborough, Inglewood, Miami and Kansas City. The group and last-16 rounds drew record crowds through the American host cities, and the co-hosts’ exit last week, Canada beaten 3-0 by Morocco, thinned the home interest without denting attendance. For markets the tournament is a quiet consumer-spending engine through an otherwise flat summer stretch, concentrated in travel, hospitality and media around the host metros (Yahoo Sports).

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.