Morning Forecast: Thursday, 19 March

Central Banks Held Rates This Week. All Blamed the Same War.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🏛️ Fed Pauses On Inflation Fears: Rates held steady as energy shocks delay potential cuts.

🛢️ Oil Surges After Energy Strikes: Crude hits $119 as Israel and Iran target gas infrastructure.

🇯🇵 Japan Holds Rates Despite Risks: The BOJ kept rates steady while warning energy costs fuel inflation.

💾 Micron Sales Triple On AI: Revenue soared as record demand sold out capacity, signaling a supercycle.

🇨🇳 Nvidia Resumes China Chip Sales: Beijing approved H200 exports, including a 25% US surcharge that monetizes trade.

🔍 War Halts UK Rate Cuts: Soaring oil prices threaten to keep rates higher than expected.

🧠 One Big Thing

Geopolitical Stagflation Derails the Pivot

A violent escalation in Middle East hostilities has derailed the global transition toward lower interest rates. With Brent crude reaching $119 after strikes on energy infrastructure, central banks in the U.S., Japan, and Britain are maintaining restrictive policies to combat renewed inflation. This shock forces a conflict between price stability and supporting cooling labor markets or stagnant growth. Markets are now erasing previously anticipated rate cuts for 2026. This shift replaces the soft landing narrative with a period of geopolitical stagflation. Investors must now prepare for a regime where energy supply dictates monetary policy despite economic fragility.

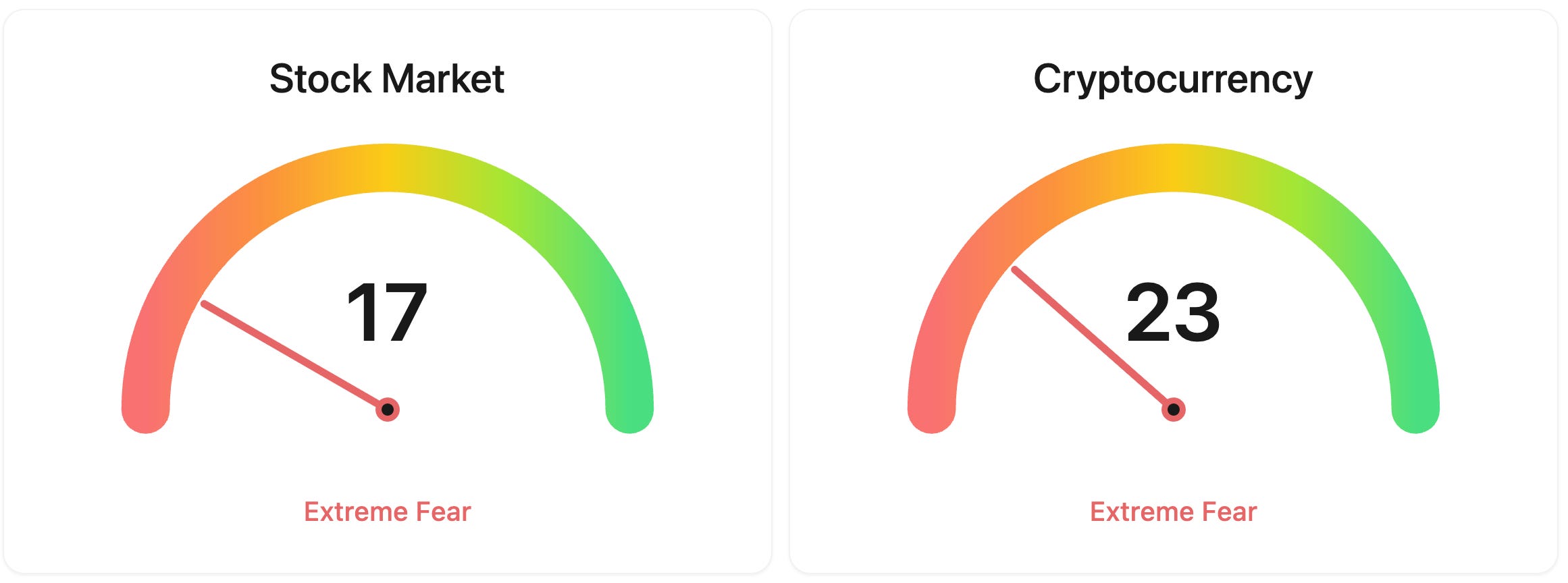

⚖️ Fear & Greed

📉 The Number That Matters

0.75%

The Bank of Japan maintained its benchmark rate at 0.75% despite rising inflationary pressure from the Middle East. Governor Ueda warned that the current oil shock could force companies to pass on costs more aggressively, risking a carry trade unwind.

⚔️ Winners vs Losers

Winners

VACH 0.00%↑: Voyager Acquisition Corp. is rallying as the SPAC approaches the closing of its business combination with oncology-focused VERAXA Biotech AG, which shareholders approved on March 12 and is expected to list on Nasdaq under the new ticker VRXA.

DLTH 0.00%↑: Duluth Holdings reported Q4 results this morning showing a dramatic turnaround to net income of $7.8 million from a year-ago loss of $5.6 million, with adjusted EPS of $0.23 and inventory slashed by 21%.

VG 0.00%↑: Venture Global continues to climb following last week’s final investment decision and $8.6 billion financing close for Phase 2 of its CP2 LNG project, the largest standalone project financing in U.S. bank market history, while multiple analysts raised price targets.

Losers

CSIQ 0.00%↑: Canadian Solar reported a Q4 loss of $1.66 per share this morning, far worse than the $0.47 loss analysts expected, with revenue of $1.22 billion missing estimates by over $150 million and soft Q1 2026 guidance of just $900 million to $1.1 billion.

AGL 0.00%↑ : Agilon health announced a 1-for-25 reverse stock split effective March 19, compounding ongoing pressure from a forecast of 7.5% cost growth in 2026 shared at the Barclays Healthcare Conference last week.

NEM 0.00%↑: Newmont and the broader gold mining sector are selling off as gold slipped below $5,000 per ounce on expectations the Fed will keep rates higher for longer amid sticky inflation and surging oil prices from the Middle East conflict.

MU 0.00%↑: Micron fell despite posting record Q2 results last night with EPS of $12.20 (vs. $9.31 expected) and revenue of $23.9 billion, as investors reacted to a capex plan above $25 billion and news of a missile strike on Qatar’s Ras Laffan LNG hub threatening Asian chip factory energy supplies.

WPM 0.00%↑: Wheaton Precious Metals is tracking the broader gold selloff as bullion retreats on a stronger dollar and hawkish Fed positioning ahead of sticky inflation data.

B 0.00%↑: Barrick Mining is falling in sympathy with the gold price decline, which has seen the metal drop roughly 10% since the onset of the U.S.-Iran conflict as rising real yields and a stronger dollar override the traditional safe-haven bid.

AEM 0.00%↑: Agnico Eagle Mines is tracking the sector-wide precious metals selloff driven by gold’s slide below $5,000 per ounce.

FCX 0.00%↑: Freeport-McMoRan is under pressure alongside copper and base metals as the stronger dollar and higher-for-longer rate expectations weigh on industrial commodities.

SCCO 0.00%↑: Southern Copper is declining alongside Freeport as copper prices soften on the same macro headwinds pressuring the metals complex broadly.

ACN 0.00%↑: Accenture reports Q2 fiscal 2026 results this morning into a stock already down roughly 25% year-to-date, with investors bracing for impact from reduced U.S. federal spending under DOGE and concerns that AI could commoditize parts of its consulting business.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $70177 (▼ -1.53%)

Ethereum (ETH): $2172 (▼ -1.46%)

XRP: $1.47 (▲ 0.01%)

Equity Indices (Futures):

S&P 500: $6617 (▲ 0.10%)

NASDAQ 100: $24376 (▼ -0.05%)

FTSE 100: £10096 (▼ -1.28%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.28% (▲ 0.38%)

Oil (WTI): $97 (▼ -2.50%)

Gold: $4694 (▼ -2.60%)

Silver: $70.75 (▼ -6.11%)

Data as of: UK (GMT) 11:15 / US (EST): 06:15 / Asia (Tokyo): 20:15

✅ 5 Things to Know Today

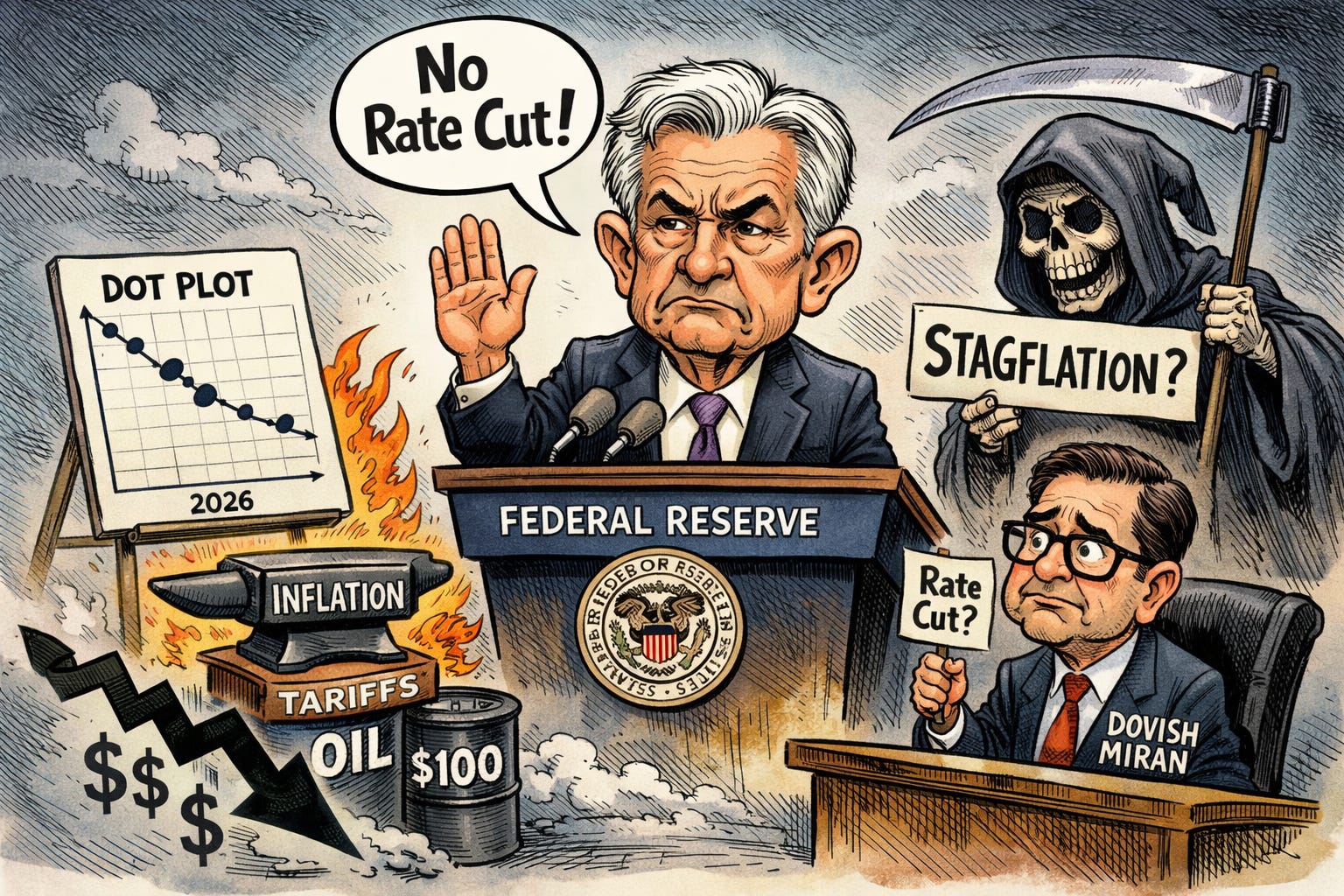

🏛️ Fed Holds Rates, but Powell Says Don’t Count on That Cut

The Federal Reserve held interest rates at 3.50%-3.75% last night in an 11-1 vote, with only Governor Stephen Miran dissenting in favour of a cut. The updated dot plot, which maps where each member expects rates to go, kept the median at 3.4% for year-end, implying one 25 basis point cut in 2026. But the range narrowed significantly, from 2.1%-3.9% in December to 2.6%-3.6%, with four or five members shifting from two projected cuts to one. The Summary of Economic Projections (SEP) raised the core Personal Consumption Expenditures (PCE) inflation forecast from 2.5% to 2.7%, while GDP was upgraded from 2.3% to 2.4%. The statement added a new line acknowledging the Iran conflict for the first time: “The implications of developments in the Middle East for the U.S. economy are uncertain” (CNBC).

The real action came during Chair Powell’s press conference. He said the Fed cannot “look through” the oil shock until tariff-related inflation clears first, calling it a precondition that has not been met. He revealed that Fed staff estimates show effectively zero net private sector job creation over the past six months after adjusting for overcounting, and described the labour market balance as carrying “a feel of downside risk.” He confirmed that rate hikes were discussed at this meeting and the previous one, though the “vast majority” do not see a hike as their base case. Markets sold off as he spoke. The S&P 500 closed down 1.36% at 6,625, now around 9% off its highs earlier this year. CME FedWatch traders moved to price zero cuts for 2026 despite the dot plot showing one. Governor Christopher Waller, who dissented for a cut in January, flipped to hold, leaving Miran as the sole dovish voice (Yahoo Finance).

Sensei’s Insight: Powell described “tension between the goals” but would not say stagflation. Yesterday’s PPI at double consensus, oil above $100, and tariff inflation still working through the system make that tension worse, not better. Watch the February core PCE on March 28. That is the number that decides whether the one cut in the dots survives or dies.

🛢️ Oil Hits $119 as Iran and Israel Trade Strikes on Energy Infrastructure

Brent crude surged as high as $119 a barrel overnight after Iran and Israel exchanged strikes on major energy facilities across the Middle East. Israel hit Iran’s South Pars gas field, the world’s largest natural gas reserve, in what marked the first direct attack on Iran’s upstream energy infrastructure since the war began on February 28. Iran retaliated by firing missiles at Qatar’s Ras Laffan Industrial City, home to the world’s largest liquefied natural gas (LNG) export plant, causing what QatarEnergy called “extensive damage.” Iran also struck two oil refineries in Kuwait and targeted facilities in Saudi Arabia and the UAE. European natural gas futures surged as much as 35%, more than double their pre-war level. US gasoline prices hit their highest since October 2022, reaching $3.88 a gallon (CNBC).

The attacks mark a dangerous escalation. Qatar had already halted LNG production on March 2 after an earlier Iranian drone strike, taking roughly a fifth of global LNG supply offline. Analysts at Global Risk Management warned that Qatar’s gas output “could be offline for months and, in the worst case, for years.” Saudi Aramco briefly halted crude loadings at its Red Sea port of Yanbu, its only remaining export route with the Strait of Hormuz still effectively closed. Brent has now rallied roughly 60% since the eve of the war, while US benchmark West Texas Intermediate (WTI) has lagged behind, trading at its widest discount to Brent in 11 years. Trump attempted to de-escalate, warning that the US would “massively blow up” Iran’s South Pars field if Qatar’s LNG facilities were hit again, but Tehran continued striking Gulf targets throughout the night (Bloomberg).

Sensei’s Insight: Brent and WTI are both oil benchmarks, but Brent sets the price for Europe and Asia while WTI reflects the US market. They have diverged to the widest gap in 11 years because Gulf supply disruptions hit Brent directly while the US has its own production cushion. That means Europe and Asia are absorbing a far worse shock than American consumers. Meanwhile, Trump publicly distanced himself from Israel’s strike on South Pars, saying the US “knew nothing” and was “in no way, shape, or form, involved.” Watch whether that friction changes the pace of escalation.

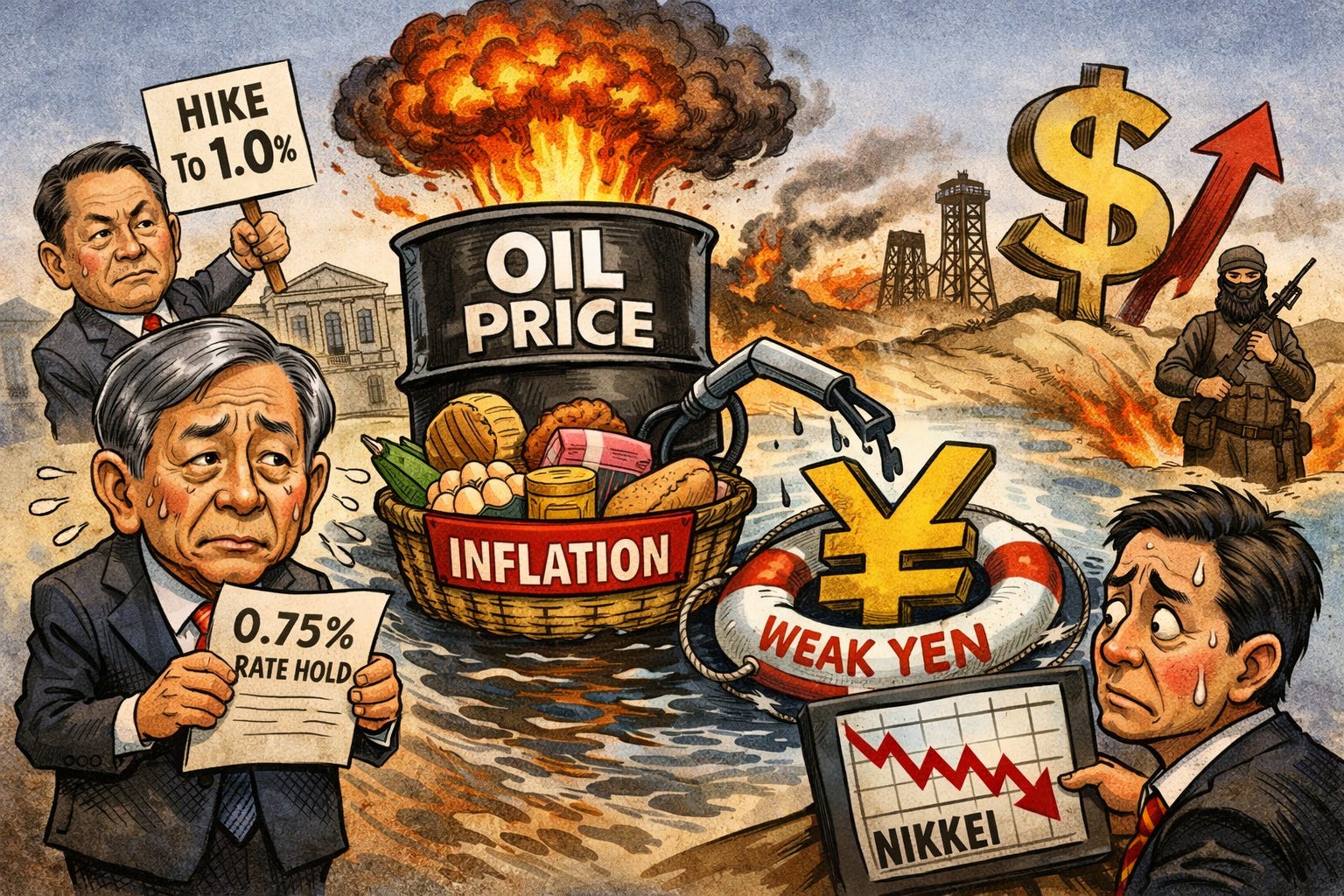

🇯🇵 Bank of Japan Holds at 0.75% but Warns Oil Shock Could Fuel Inflation

The Bank of Japan (BOJ) held its benchmark rate at 0.75% this morning in an 8-1 vote, with hawkish board member Hajime Takata again pushing for a hike to 1.0%, the same proposal he made in January. The hold was unanimous among expectations, but the tone was notably more cautious. The BOJ formally added the Middle East conflict to its list of economic risks for the first time, warning that “risks to the outlook include the future course of the situation in the Middle East as well as developments in crude oil prices.” Governor Kazuo Ueda went further in his press conference, noting that Japanese companies are “already actively pushing up prices and wages,” which means they “could pass on costs more aggressively than after the war in Ukraine.” The Nikkei 225 fell as much as 3% on the session as oil surged past $115 (CNBC).

Japan imports roughly 95% of its crude oil, and every $10 rise in Brent costs the country an estimated 2 trillion yen (around $13 billion) per year in additional energy imports. That makes the current oil shock an acute problem for both inflation and the trade balance. The yen has weakened to near 159 against the dollar, approaching the 160 level where the BOJ and Ministry of Finance have previously intervened, including spending roughly $100 billion defending the currency in summer 2024. ANZ expects a rate hike as soon as April, and ING has flagged that if the yen breaks through 160, the timeline could be pulled forward from October to the second quarter. That matters for global markets because a surprise BOJ hike at these levels risks triggering a carry trade unwind, where investors who borrowed cheaply in yen to fund positions in higher-yielding assets are forced to sell. The August 2024 carry trade unwind, triggered by the BOJ’s last surprise move, sent shockwaves through global equities and crypto (Reuters).

Sensei’s Insight: The Fed is stuck between inflation and a fragile labor market. The BOJ has the same problem but worse. Japan imports 95% of its crude. Every move higher in oil feeds directly into consumer prices, weakens the yen, and tightens the pressure to hike. But hiking risks killing an economy that only just started growing again and could trigger another carry trade unwind. Powell said he does not know what the war will do to the US economy. For Japan, it is not a question. It is already doing it.

💾 Micron Triples Revenue and Signals a Memory Supercycle

Micron Technology reported fiscal second-quarter earnings on Wednesday that shattered expectations across every metric. Revenue hit $23.86 billion, nearly tripling from $8.05 billion a year ago. Non-Generally Accepted Accounting Principles (GAAP) earnings per share came in at $12.20 versus the $9.31 consensus and $1.56 a year prior. Gross margins exploded to 74.9%, up from 36.8% twelve months earlier. Capital spending will now exceed $25 billion for fiscal 2026, up from prior guidance of $20 billion, itself already raised from an initial $18 billion. CEO Sanjay Mehrotra said fiscal 2027 capex will “step up meaningfully,” with construction costs increasing by over $10 billion. Third-quarter guidance was staggering: revenue of approximately $33.5 billion, implying over 200% year-over-year growth, gross margins of roughly 81%, and earnings per share of around $19.15. The board approved a 30% dividend increase (Bloomberg).

Micron is a critical bottleneck in the artificial intelligence (AI) supply chain. The company can currently meet only 50 to 66% of customer demand. Its entire 2026 High Bandwidth Memory (HBM) production capacity, the specialised high-speed memory stacked vertically and used in every major AI accelerator from Nvidia’s GPUs to Google’s TPUs, is 100% sold out under binding long-term agreements. That is a departure from the volatile spot-pricing model that historically made memory stocks boom-and-bust plays. The HBM market is projected to grow from $35 billion in 2025 to $100 billion by 2028, a milestone two years ahead of prior projections and larger than the entire DRAM market in calendar year 2024. Micron also announced it had begun high-volume production of HBM4 designed for Nvidia’s Vera Rubin platform. Despite the massive beats, shares fell in extended trading as investors weighed the enormous capex intensity. The sell-off deepened on Thursday morning after news of the Iranian missile strike on Qatar’s Ras Laffan energy complex broke during Micron’s earnings call, raising concerns about energy costs for chip manufacturing facilities across Asia.

Sensei’s Insight: The real signal is the shift from spot pricing to binding multi-year agreements. If memory pricing becomes contractual rather than cyclical, the traditional “sell the peak” playbook for semiconductor stocks stops working. Micron’s first-ever five-year supply agreement suggests the company is betting this cycle is structurally different from every one before it.

🇨🇳 Nvidia Wins Beijing’s Approval for H200 Chip Sales

Beijing has granted approval for Nvidia to sell its H200 AI chips to Chinese customers, CEO Jensen Huang confirmed at the company’s GTC developer conference. The H200 features 141 gigabytes of HBM3e memory, nearly double the capacity of the previous-generation H100, and is roughly six times more powerful than the H20, the most capable chip previously available to China. Initial approvals cover approximately 400,000 chips for ByteDance, Alibaba, and Tencent, worth an estimated $11 billion at around $27,000 per unit. Nvidia is also preparing a China-compatible version of its Groq inference chip, technology acquired through a roughly $20 billion deal with Groq Inc. in December 2025, expected to be available by May (Reuters).

China historically generated 20 to 25% of Nvidia’s data centre revenue before escalating US export controls sent its market share, in Huang’s own words, “from 95% to zero.” The deal required dual approval from Washington and Beijing. The Trump administration approved H200 sales in December 2025 with a 25% surcharge paid to the US Treasury. Nvidia’s fiscal 2027 first-quarter guidance of $78 billion includes zero China data centre compute revenue, making any actual shipments pure upside. The stock barely moved on the news, trading at roughly $182, still 20% below its 52-week high, reflecting investor fatigue after repeated China approval headlines that previously failed to result in shipments. Senator Elizabeth Warren is pushing legislation to block the sales, arguing chips could reach China’s military.

Sensei’s Insight: The 25% surcharge is the detail that matters most. Washington is not reopening China trade out of goodwill. It is monetising it. If this model works, expect surcharge-gated export approvals to become a template for other advanced technologies, turning trade restrictions into a revenue tool rather than a pure containment strategy.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: The Bank of England Decides Today. Here Is Why the War Changed Everything.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.