Morning Forecast: Thursday 2 July

A $179 billion pop, a $138 billion drop, and jobs day. (Cheat Sheet included inside)

👀 Today’s Stories at a Glance

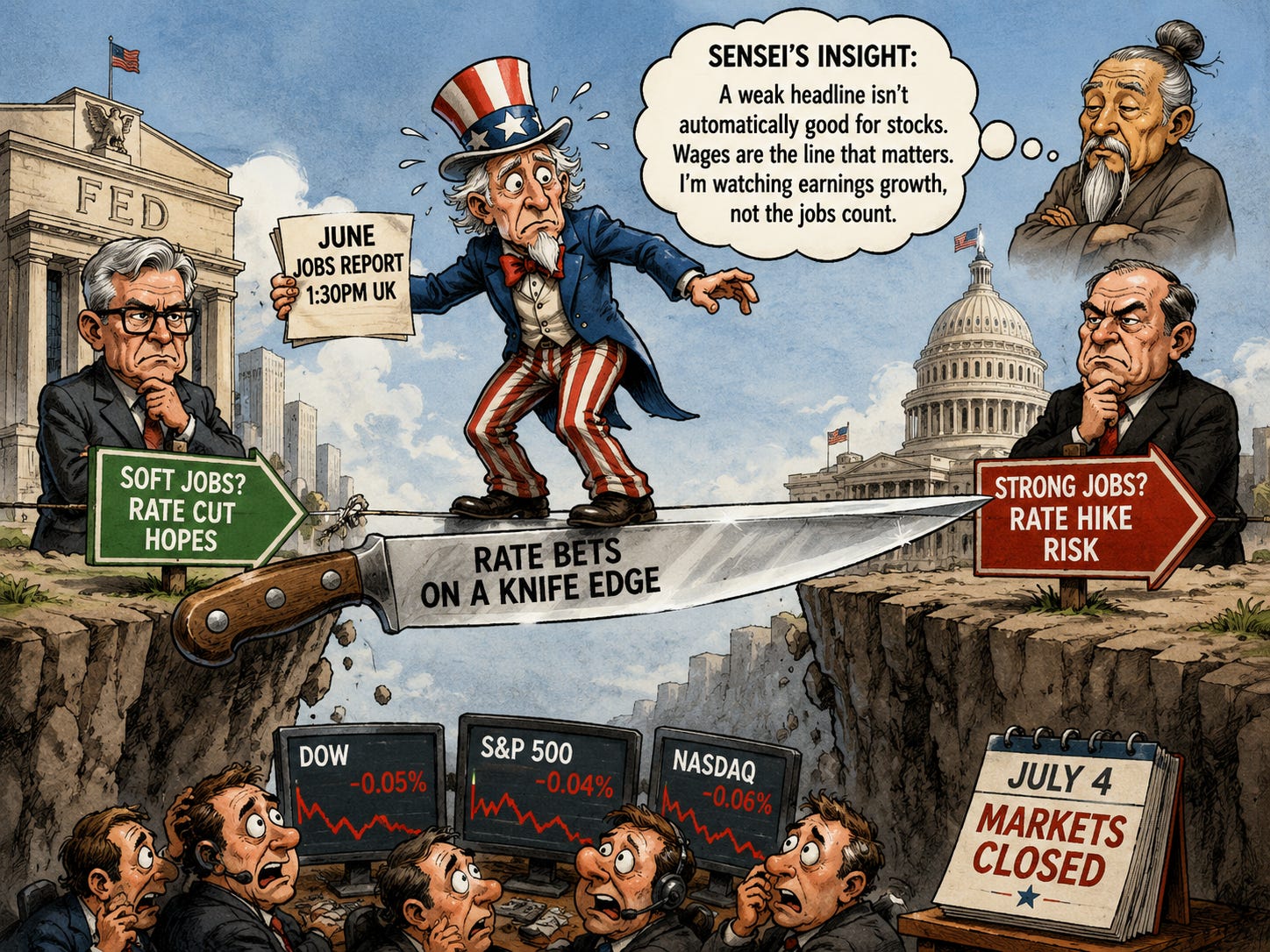

💼 Jobs day is here: June payrolls land at 1:30pm with a 115,000 bar and rate bets on the line.

☁️ Meta’s $179 billion pop: Meta will rent out its spare AI computing power, and the stock jumped 10%.

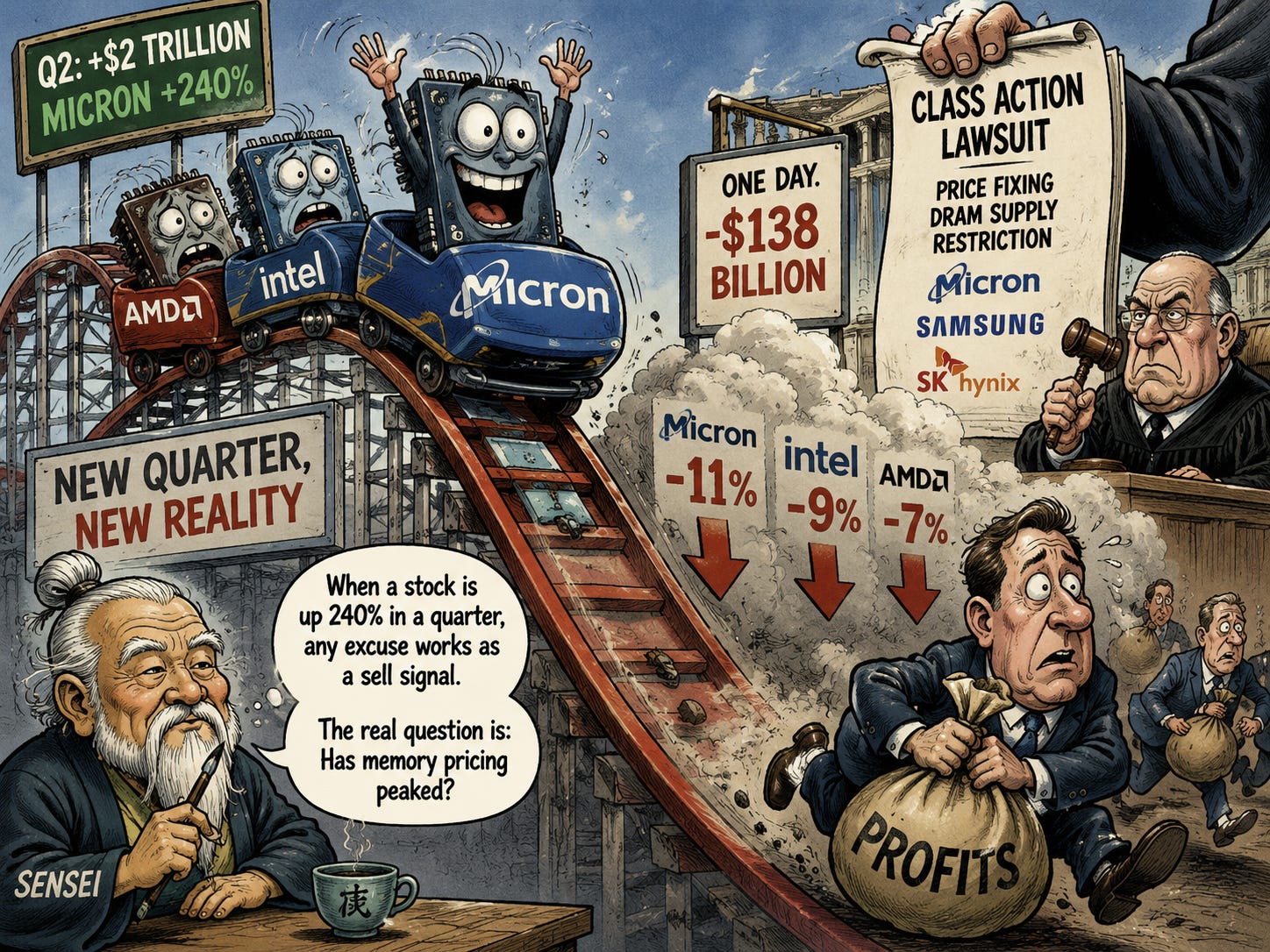

💾 Chips start Q3 with a thud: Micron shed $138 billion in a day as the H1 winners got sold.

🚗 Tesla’s number due today: Wall Street wants roughly 406,000 deliveries, with estimates unusually far apart.

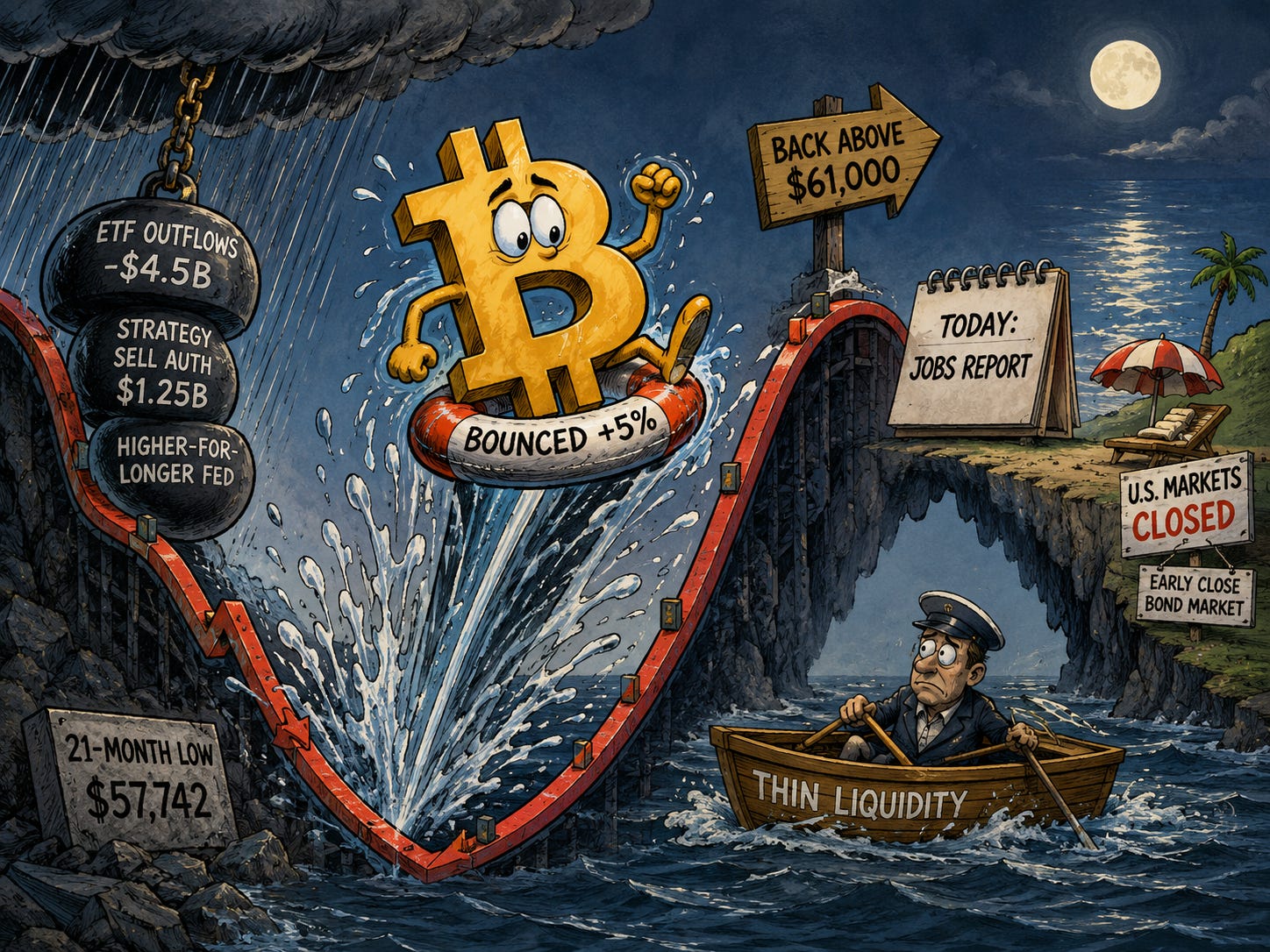

₿ Bitcoin’s 21-month low: BTC touched $57,742 yesterday, its lowest since September 2024, before bouncing back above $61,000.

🎮 PlayStation goes disc-free: Sony ends physical discs for new games from January 2028.

🪙 Ripple joins Open USD: A Visa and Mastercard-backed stablecoin picked the XRP Ledger as a launch rail.

🔍 The Jobs Day Playbook: A cheat sheet for the 1:30pm print: every number, scenario and likely reaction.

🧠 One Big Thing

Meta announcing it will sell its spare AI computing power added $179 billion to its market value in a day. The same session, the companies that build and rent that computing power fell hard: Nebius lost almost 12%, CoreWeave around 10%, Nvidia about 2%. That is the message hiding inside both moves. When the biggest AI spenders start renting out excess capacity, computing power stops being scarce and starts being a commodity, and the profit shifts from the companies selling the shovels to the platforms that already own them. Watch rental pricing at the specialist cloud firms; if it softens, the AI capex boom has found its ceiling.

+

The June jobs report lands at 1:30pm UK into the thinnest market of the year: the bond market shuts early today and everything closes tomorrow. The warm-up act already wobbled, with ADP’s private hiring count coming in at 98,000, its first sub-100,000 reading since March. A weak number is no longer simply good news for stocks. With inflation above 4% and the Fed leaning away from cuts, a soft print revives easing hopes, but a very soft one reads as a growth scare, and a hot one puts a rate rise straight back in play. Watch the two-year yield’s first move, not the equity open.

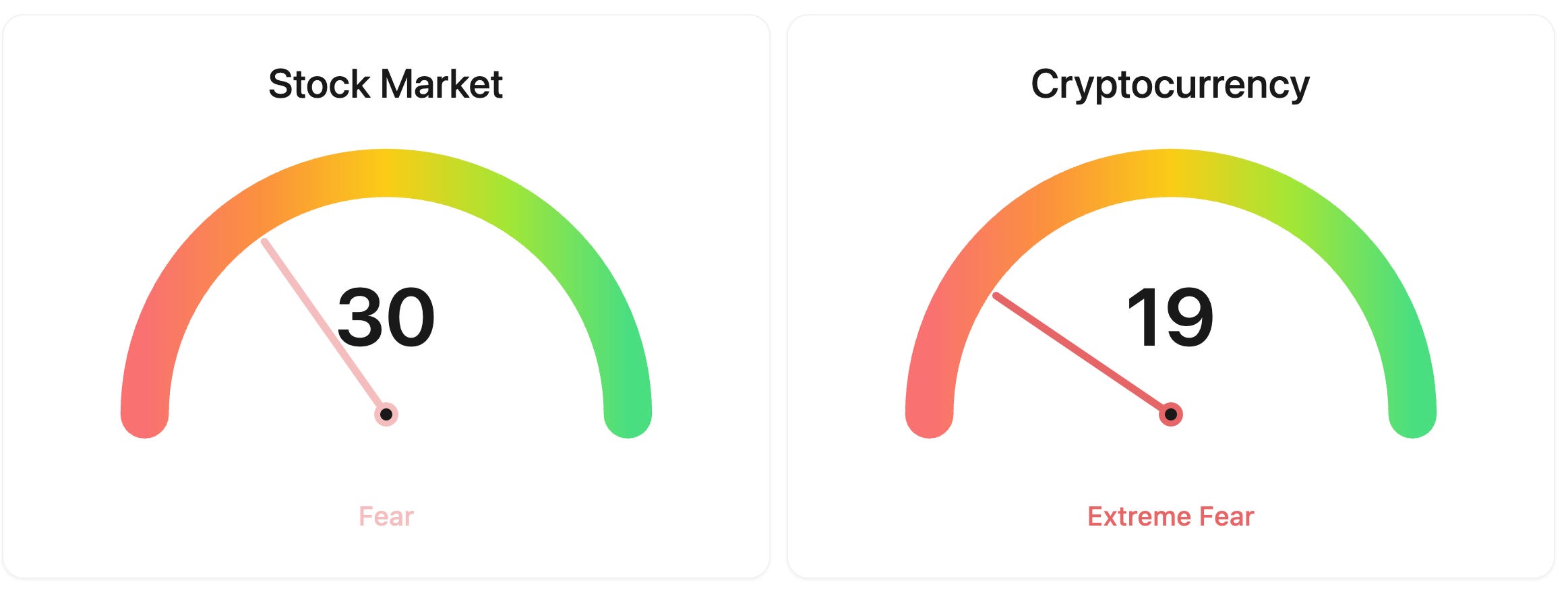

⚖️ Fear & Greed

📉 The Number That Matters

$179 billion

The market value Meta added in one session on its plan to sell spare AI computing power

⚔️ Winners vs Losers

Winners

MSTR 0.00%↑: Strategy Inc is climbing after unveiling a new Digital Credit Capital Framework that authorizes up to two billion dollars in common and preferred stock buybacks, establishes a formal cash reserve policy, and lifts its STRC preferred dividend to twelve percent, with Citi reaffirming a buy rating on the overhaul. The revamped capital plan has driven a sharp bounce off last week’s lows.

HOOD 0.00%↑: Robinhood Markets is rising after launching the public mainnet of Robinhood Chain, its AI-native Ethereum layer-two network built for tokenized stock trading, alongside a run of analyst price-target increases that includes a fresh raise from Deutsche Bank.

PLTR 0.00%↑: Palantir Technologies is extending its rally after the US Army selected its Foundry platform as the data backbone for the Next Generation Command and Control program, a deal worth up to ten billion dollars, and the company announced a partnership with Nvidia to run secure AI models for government agencies.

Losers

FC 0.00%↑: Franklin Covey shares are sliding after the leadership-training company posted third-quarter revenue and earnings that missed expectations and cut its full-year revenue guidance, pointing to a large enterprise contract timing shift, a state education budget reduction, and weakness across international markets.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $61,188 (▲ 2.10%)

Ethereum (ETH): $1,644 (▲ 2.32%)

XRP: $1.08 (▲ 2.56%)

Equity Indices (Futures):

S&P 500: 7,537 (▼ 0.09%)

NASDAQ 100: 29,938 (▼ 0.52%)

FTSE 100: 10,515 (▲ 0.49%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.49% (▲ 0.22%)

Oil (WTI): $68 (▼ 0.75%)

Gold: $4,064 (▲ 0.83%)

Silver: $59.82 (▲ 1.27%)

Data as of: UK: 11:40am BST / US: 6:40am EDT / Asia (Tokyo): 7:40pm JST

✅ 5 Things to Know

💼 Jobs day arrives with rate bets on a knife edge

The June jobs report lands today at 1:30pm UK time, pulled forward because US markets close tomorrow for Independence Day. Economists expect around 115,000 new jobs, a clear step down from May’s 172,000, with unemployment holding at 4.3%. The warm-up act already disappointed: ADP’s private payrolls count came in at 98,000 yesterday, short of the 110,000 expected and the first reading below 100,000 since March. Stock futures are wavering this morning, with the Dow, S&P 500 and Nasdaq all hovering just below the flatline as traders wait (CNBC).

The stakes are unusually lopsided. Fed chair Kevin Warsh gave nothing away at Sintra yesterday, saying only that “prices are too high” while noting inflation risks have eased in recent weeks, and repeating that his Fed will not signal its rate path in advance. That leaves this print to do the talking: a soft number could revive the cut hopes the White House keeps pushing, while a strong one with steady unemployment likely hardens the case for a rise. The reaction plays out in a shortened session, with the bond market closing at 7pm UK and everything shut tomorrow (CNBC).

Sensei’s Insight: A weak headline is not automatically good for stocks any more. With the Fed leaning hawkish, wages are the line that matters: cool pay growth lets Warsh stay patient, hot pay growth puts a hike straight back on the table. See the deep dive below for the cheat sheet.

☁️ Meta turns its AI bill into a cloud business

Meta jumped around 10% yesterday, adding roughly $179 billion in market value, after reports it plans to sell access to its spare AI computing power. The effort, developing inside an internal unit called Meta Compute, would take the enormous data-centre capacity Meta has been building for its own AI models and rent the excess to outside customers, both as raw computing power and as access to AI models hosted on Meta’s infrastructure. It is a straight shot at turning the company’s biggest cost into a second business (Yahoo Finance).

The history rhymes: Amazon built server capacity for its shop, rented the spare to outsiders, and AWS became the most profitable part of the company. Investors clearly like the echo. The losers tell the other half of the story, because the specialist AI-cloud firms that exist purely to rent computing power sold off hard on the news, with Nebius down almost 12% and CoreWeave around 10%, while Nvidia slipped about 2%. Every hyperscaler that rents out spare capacity is new supply competing against them, and Meta is the biggest new landlord yet.

Sensei’s Insight: The market just paid Meta $179 billion for a business that does not exist yet. The real signal is what it did to the rental firms: if the giants start leasing out spare AI capacity, computing power becomes a commodity, and commodity margins go one way over time.

💾 Chip stocks open the second half with a $138 billion dent

The stocks that carried the first half fell hardest on the first day of the new quarter. Micron dropped 11% yesterday, erasing about $138 billion of market value just days after touching an all-time high of $1,255, while Intel fell 9% and AMD lost 7%. The three had added roughly $2 trillion in combined value during a second quarter in which Micron alone rose more than 240%, so the pullback follows a rally with very few precedents. Funds locking in profits and rebalancing at the half-year turn did much of the damage (CNBC).

There is a second thread: a class-action lawsuit filed in a California federal court alleges Micron, Samsung and SK Hynix deliberately restricted supply of ordinary DRAM memory chips while shifting production to the high-bandwidth memory that AI servers need, helping push DRAM prices up roughly 700% in four years. The claim attacks the exact mechanism behind Micron’s extraordinary quarter, in which revenue more than quadrupled and gross margin hit 84.9%. Whether a court ever agrees, the suit gives nervous holders a reason to take the money (Yahoo Finance).

Sensei’s Insight: When a stock is up 240% in a quarter, any excuse works as a sell signal. The lawsuit reads as headline risk, since memory-price cases have a long history of settling small. The real question is whether memory pricing itself has peaked, and this suit does not answer it.

🚗 Tesla’s delivery number lands this afternoon

The wait ends today: Tesla reports second-quarter deliveries this afternoon UK time, and the goalposts are unusually far apart. The company’s own compiled consensus from 22 analysts sits at 406,024 vehicles, but the Bloomberg consensus is closer to 396,000, Goldman Sachs sees 420,000, and at least one bull argues for 450,000. The middle of that range would mean a jump of roughly 11% on a weak first quarter while landing just short of the 410,831 Tesla delivered a year earlier (Yahoo Finance).

Where the sales come from matters as much as the total. Analysts see Europe and international markets doing the heavy lifting while US sales decline, a mix that feeds directly into margins ahead of the full results on 22 July. The quieter number to watch is energy storage, where analysts expect deployments near 13.8 gigawatt hours, well above the 8.8 gigawatt hours of the first quarter, as the Shanghai Megafactory ramps up. With US markets shut tomorrow, any surprise in either direction could move the stock sharply in a thin session.

Sensei’s Insight: A 396,000 to 420,000 spread means somebody is badly wrong today. I care less about the total than the US-versus-international mix, because that decides margins into the 22 July report. A beat built on discounted European volume would be a hollow one.

₿ Bitcoin bounces off a 21-month low into the jobs print

Bitcoin fell as much as 1.5% to $57,742 in Asian trading yesterday, its lowest level since September 2024, before snapping back above $61,000 today, a bounce of more than 5% off the low. The pressure that drove it there came from familiar places: US spot Bitcoin ETFs just closed their worst month since launching, with roughly $4.5 billion of net June outflows, and Strategy’s new authorisation to sell up to $1.25 billion of its Bitcoin still hangs over sentiment. Growing bets that the Fed’s next move is a rise rather than a cut have squeezed every liquidity-sensitive asset, and crypto sits at the front of that queue (Bloomberg).

Today’s jobs report is the next catalyst, and crypto faces it with a structural quirk: Bitcoin trades around the clock while the US bond market closes early today and every US market is shut tomorrow. Any payrolls surprise will still be moving crypto prices long after equities have gone dark, in the thinnest liquidity of the year. Europe’s MiCA deadline, the other event this week, came and went with barely a ripple in price, which says the selling is macro-driven rather than regulatory. Whether the bounce can hold $60,000 through the long weekend is the cleanest test of how exhausted the sellers are.

Sensei’s Insight: A 5% snap off the low with sentiment this stretched is how cycle bottoms have historically started, but one bounce is not a trend, and a hot jobs number into a holiday weekend is exactly the setup for an air pocket back lower. I am watching the weekend, not the print: crypto will be the only market open, and thin tape cuts both ways.

Stories You Might Have Missed

🎮 Sony pulls the plug on PlayStation discs

Sony will stop producing physical discs for new PlayStation games from January 2028, making every new release digital-only through the PlayStation Store and retail code sales. Games released before the cutoff will stay available on disc, but the direction is final, and Sony called it a natural step given digital already accounts for around 80% of the full games it sells, with physical software down to roughly 3% of revenue. Game retailers reacted angrily, since new-release discs remain a pillar of their trade, and the move lands just after Grand Theft Auto 6 went digital-only. For investors the shift means higher-margin sales for Sony and one more squeeze on physical games retail (CNBC).

🪙 Ripple joins a Visa and Mastercard-backed stablecoin

Ripple has signed on as a day-one integration partner for Open USD, a new consortium stablecoin backed by Visa, Mastercard, Stripe, BlackRock, Coinbase, Google and more than 140 other companies, with no single firm in control. The coin is free to mint, hands its reserve earnings back to partner companies after a small fee, and is aimed squarely at the profit engines of Tether and Circle, whose USDT and USDC dominate the market. For XRP holders the relevant part is the rails: Ripple is putting the XRP Ledger forward as one of the blockchains Open USD runs on, which would route institutional stablecoin traffic across the network when the coin goes live later this year (Yahoo Finance).

🔍 Deep Dive: The Jobs Day Playbook

Today’s Deep Dive is a cheat sheet, because the only story that matters this afternoon is the one that has not happened yet. The June jobs report lands at 1:30pm UK time, squeezed in before the long weekend, and it arrives with the usual logic flipped: with inflation above 4% and the Fed leaning toward a rise rather than a cut, a strong number is bad news for markets and a soft one is relief, unless it is weak enough to read as recession. The playbook below walks through every release dropping at 1:30pm, what each number means in plain English, the scenarios that could play out, and how stocks, crypto, gold and the dollar have typically reacted to each one. Read it before the print, not after.

Here is the cheat sheet, click the PDF to open it:

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.