Morning Forecast: Thursday, 26 March

One Rejected Peace Plan. $580 Million a Day in Airline Losses. A Fed That Can't Move.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

⚔️ Iran Rejects US Peace Proposal: Stocks fell after Tehran dismissed Washington’s plan, as oil prices surged.

💰 Circle Shares Sink on Yield Ban: Leaked rules targeting stablecoin interest caused a 20% stock price crash.

⚖️ Meta, Google Lose Addiction Trial: A jury awarded $6 million after finding social platforms were addictive.

🤖 Arm Debuts First AI Chip: Shares gained 15% after the firm announced its first in-house processor.

✈️ White House Blocks Musk Pay: Federal law stopped Musk from paying TSA workers during the shutdown.

🔍 Claims Data Tests Economic Narrative: This report highlights stagflation risks as fuel prices remain high.

🧠 One Big Thing

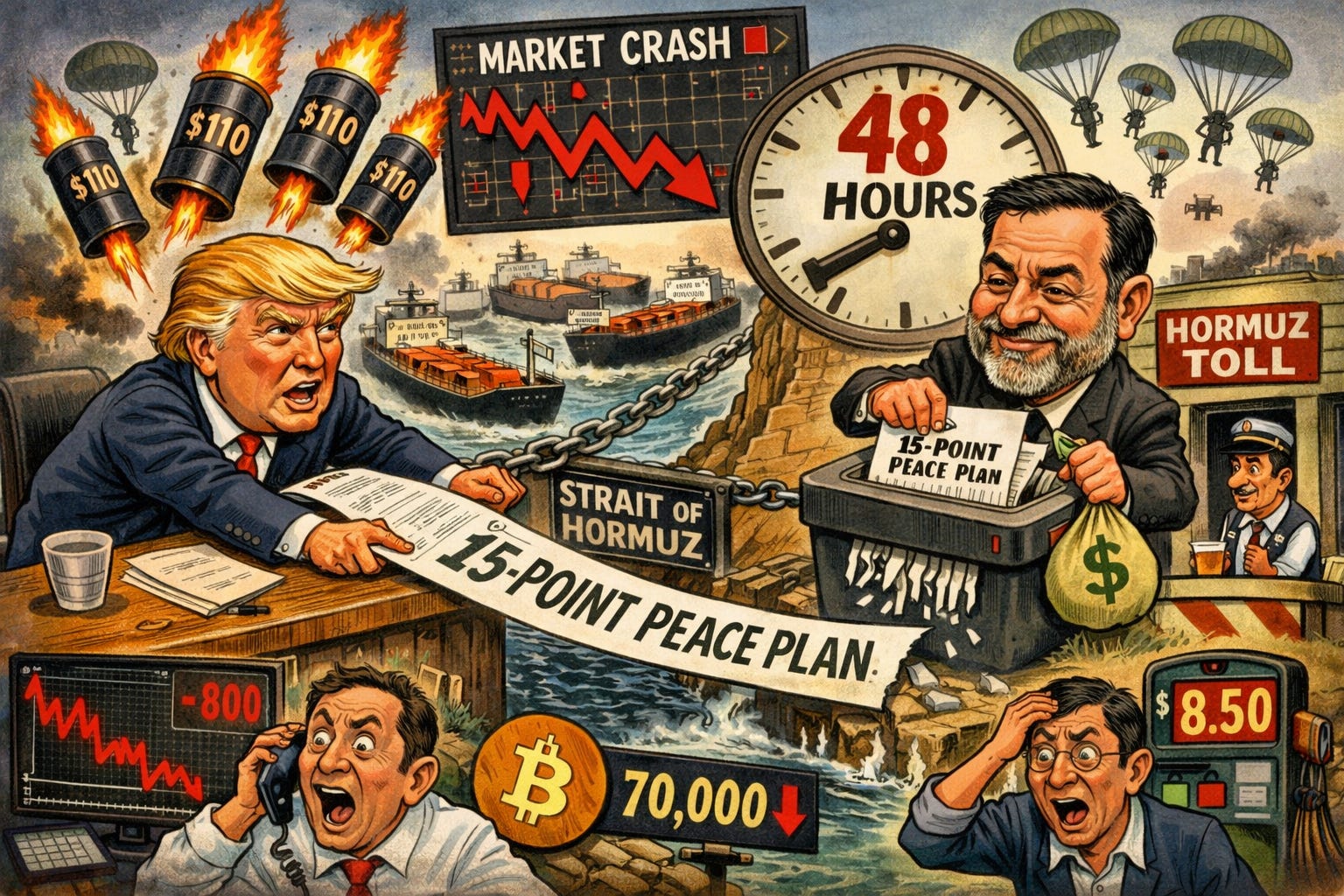

The Hormuz Stagnation Trap

The collapse of diplomatic negotiations between Washington and Tehran has solidified a blockade of the Strait of Hormuz. This closure restricts twenty percent of global oil flow and pushes energy prices toward record highs. Investors are facing a stagflationary environment where surging inflation coincides with a decelerating economy. The tension centers on an expiring deadline for American military strikes against Iranian energy assets. These conditions trap the Federal Reserve by preventing interest rate cuts despite evidence of a weakening labor market. Portfolios must now absorb the combined impact of higher operating costs and slowing consumer growth.

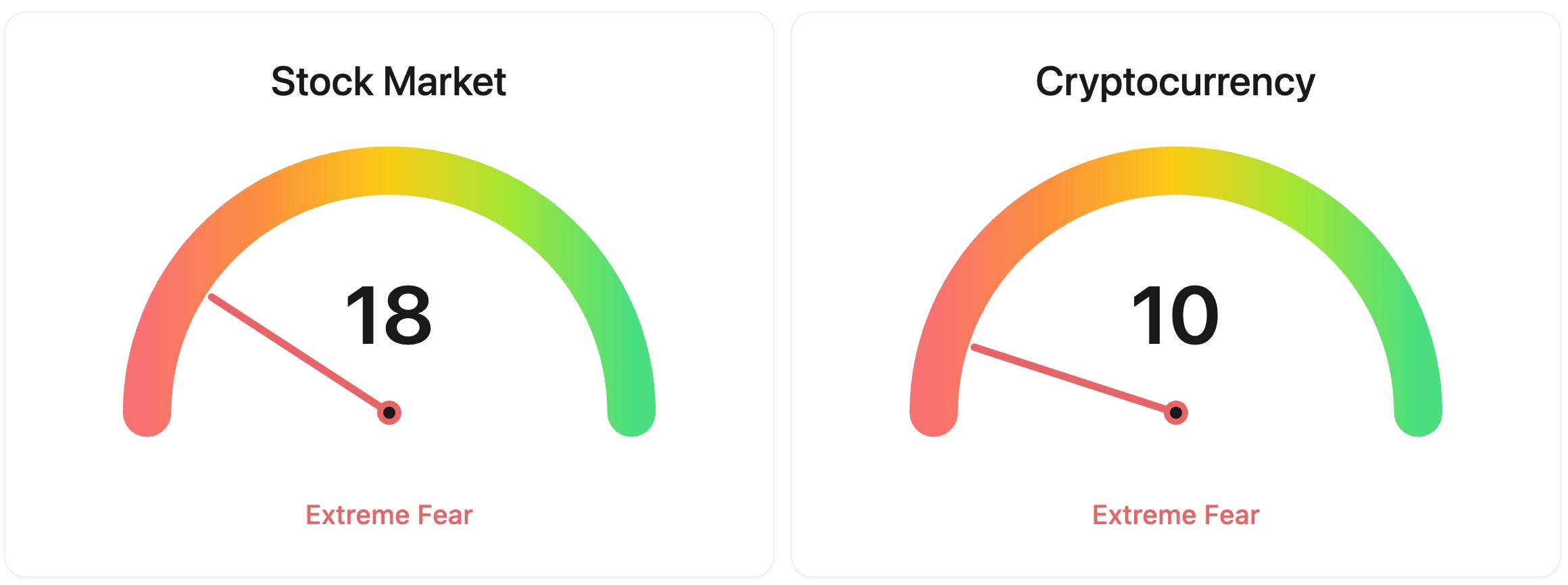

⚖️ Fear & Greed

📉 The Number That Matters

210,000

Market consensus for today’s initial jobless claims is 210,000. Traders are watching for a break in the "no hire, no fire" trend as the U.S. economy balances a weakening labor market against persistent stagflationary pressures.

⚔️ Winners vs Losers

Winners

OLPX 0.00%↑ +50.38% Olaplex Holdings surged after announcing a definitive agreement to be acquired by Germany’s Henkel for $2.06 per share in an all-cash deal valued at approximately $1.4 billion, representing a 55% premium to its prior close.

KOD 0.00%↑: Kodiak Sciences jumped on positive topline Phase 3 GLOW2 results for its retinal drug Zenkuda, which met its primary endpoint with 62.5% of patients achieving meaningful improvement versus 3.3% for sham, and the company said it plans to accelerate its BLA submission.

NAVN 0.00%↑: Navan rallied after reporting Q4 fiscal 2026 revenue of $177.9 million, well above the $162.2 million consensus, with full-year revenue up 31% to $702 million and the company guiding for fiscal 2027 revenue of $866 million to $874 million alongside its first year of positive non-GAAP operating income.

PGEN 0.00%↑: Precigen climbed after reporting Q4 results that highlighted an accelerating commercial launch of its RRP therapy Papzimeos, with management guiding for Q1 2026 revenue exceeding $18 million and projecting a path to cash flow breakeven this year.

Losers

TASK 0.00%↑: TaskUs shares are trading ex-dividend today following a $3.65 per share special cash dividend paid on March 25, funded by a new $500 million credit facility, with the stock price adjusting down by the dividend amount.

MLKN 0.00%↑: MillerKnoll fell after missing Q3 fiscal 2026 estimates, posting revenue of $926.6 million versus the $942 million consensus and adjusted EPS of $0.43 versus $0.45 expected, while next-quarter guidance of $975 million in revenue and $0.52 in EPS also came in below Street forecasts.

WS 0.00%↑: Worthington Steel tumbled after reporting fiscal Q3 earnings of $0.27 per share on revenue of $769.8 million, sharply missing expectations of $0.46 per share and $882.95 million in revenue.

APP 0.00%↑: AppLovin Corporation continued its 2026 slide, with shares down over 35% year to date amid an ongoing SEC investigation and broader investor concerns about AI-driven competition in the ad tech sector eroding the company’s margins.

SNDK 0.00%↑: Sandisk Corporation extended yesterday’s selloff after announcing a $1 billion strategic equity investment in Taiwan’s Nanya Technology, with investors questioning the capital allocation decision alongside concerns raised by Google’s new TurboQuant memory compression technology for AI workloads.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $69625 (▼ -2.36%)

Ethereum (ETH): $2080 (▼ -4.06%)

XRP: $1.38 (▼ -2.68%)

Equity Indices (Futures):

S&P 500: $6548 (▼ -0.66%)

NASDAQ 100: $24173 (▼ -0.80%)

FTSE 100: £9995 (▼ -1.08%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.38% (▲ 1.15%)

Oil (WTI): $93 (▲ 2.12%)

Gold: $4445 (▼ -1.34%)

Silver: $68.20 (▼ -4.18%)

Data as of: UK (GMT) 11:04 / US (EST): 07:04 / Asia (Tokyo): 20:04

✅ 5 Things to Know Today

⚔️ Markets Hit Reverse as Iran Rejects Peace Plan

S&P 500 futures dropped 0.6% this morning after Iranian state media confirmed Tehran had rejected Washington’s 15-point peace proposal, delivered through Pakistani intermediaries earlier this week. The plan demanded Iran dismantle its nuclear sites, halt enrichment, end ballistic missile development, and reopen the Strait of Hormuz, the chokepoint that normally handles roughly 20% of global oil supply but has been effectively closed since early March. Iranian Foreign Minister Abbas Araghchi told state television that no negotiations are taking place, and a diplomatic source dismissed the proposal as “maximalist” and “unreasonable,” directly contradicting President Trump’s claim that Iran “wants a deal so badly.” European stocks snapped a three-day winning streak, Brent crude climbed back above $104 a barrel, and Bitcoin dropped 1.3% below $70,000 to $69,943, dragging Ethereum and XRP down 2.1% and 2.6% respectively. It was a sharp reversal from yesterday, when the S&P 500 gained 0.54%, the Dow rose 0.66%, and Brent fell around 7% to $97.26 on hopes the peace plan could gain traction. Goldman Sachs has since raised its near-term Brent forecast to $110, warning prices could exceed 2008 records if Hormuz remains at minimal capacity for 10 weeks (Bloomberg).

The diplomatic picture is now considerably darker, with less than 36 hours until Trump’s self-imposed pause on strikes against Iranian energy infrastructure expires. Tehran countered with its own five-point proposal that includes war reparations, recognition of Iran’s sovereignty over Hormuz, protection for its regional proxy groups including Hezbollah and the Houthis, and guarantees against future attacks. Iran’s parliament is also working on a draft bill to formalise a toll system for vessels passing through Hormuz, charging up to $2 million per ship, a move that would legally codify what the shipping industry has already been reporting as an informal arrangement. The White House insists talks are ongoing, with Press Secretary Karoline Leavitt warning that Trump “does not bluff and is prepared to unleash hell.” Vice President JD Vance may travel to Pakistan for face-to-face talks this weekend, but both sides are publicly miles apart. A Reuters/Ipsos poll conducted this week found 61% of Americans disapprove of the military strikes, adding domestic pressure to the White House’s push for visible diplomatic progress. Meanwhile, the US is deploying more than 1,000 paratroopers from the 82nd Airborne Division alongside 5,000 Marines trained in amphibious assaults, and Axios reported that the Pentagon is preparing options for a “final blow” including ground forces and a major bombing campaign (Wall Street Journal).

BlackRock President Robert Kapito warned today that investors may be underestimating how badly the conflict could hit portfolios, telling a symposium in Melbourne that growth could take a two-percentage-point hit while inflation may rise by a similar margin, even if the war ends soon. Brent crude is on pace for its biggest monthly gain since 1990, having surged from below $70 at the start of the conflict to a peak of $119 earlier this month. Iran, paradoxically, has been one of the war’s economic beneficiaries: its crude is selling at the slimmest discount to Brent in over 10 months, and as the only major exporter still able to ship through Hormuz, its Kharg Island terminal has actually seen activity increase. Across Asia, the fuel crisis is deepening. Japan has begun releasing oil from its national reserves, Thailand hiked gasoline prices 14% to 22% overnight, and India’s state-owned refiners purchased liquefied petroleum gas (LPG) from Iran for the first time in nearly eight years after shortages forced some households to cook with firewood. The Pentagon is even considering diverting weapons originally intended for Ukraine to the Middle East, a sign the conflict’s resource demands are straining American military capacity on multiple fronts (Bloomberg).

Sensei’s Insight: The 82nd Airborne doesn’t deploy for theatre. If Friday’s deadline passes without a deal, this shifts from an air campaign to something far more expensive and unpredictable. Meanwhile, Asia’s fuel crisis is accelerating by the day, and every hour Hormuz stays closed teaches Tehran just how much leverage it holds over global energy. Watch Friday’s close.

💰 Circle Suffers Worst Day on Record After Stablecoin Yield Ban Surfaces

Circle Internet Group (NYSE: CRCL), the company behind the USDC stablecoin, saw its shares crater 20% earlier this week after a leaked draft of the Digital Asset Market Clarity Act revealed plans to ban yield payments on stablecoin holdings. The proposed language prohibits platforms from offering interest “directly or indirectly” for simply holding a stablecoin, or in any way “economically equivalent to interest.” That strikes at the core of Circle’s business. A remarkable 95% of Circle’s Q4 2025 revenue, totalling $770 million and up 77% year on year, came from US Treasury bill interest earned on USDC’s $75.3 billion in reserve assets. The selloff wiped billions from Circle’s market cap and dragged Coinbase down roughly 10% alongside it (CNBC).

Circle bounced approximately 7% yesterday as investors digested that the legislation remains in draft form and still needs 60 Senate votes before becoming law. Analysts are divided on the damage. Clear Street’s Owen Lau called the drop “an overreaction,” while Bitwise CIO Matt Hougan argued that stablecoin adoption has been driven more by payments and settlement utility than yield. But the timing was especially painful: on the same day, rival Tether announced it had hired a Big Four accounting firm for its first-ever full audit, potentially narrowing USDC’s key transparency advantage. The stock remains up 27% year to date and 11 of 12 covering analysts still rate it a Buy, with an average target of $127.61, but the revenue model that underpins that consensus is now under direct legislative threat (CoinDesk).

Sensei’s Insight: The Clarity Act may ultimately strengthen Circle’s hand against Coinbase. If yield rewards disappear, Coinbase loses high-margin stablecoin revenue and Circle gains leverage in their August 2026 distribution renegotiation. Watch the bill’s progress, but also watch the power dynamics between issuer and distributor shifting underneath the headlines.

⚖️ Jury Hands Meta and Google a $6 Million Verdict in Social Media’s “Big Tobacco Moment”

A Los Angeles jury yesterday found Meta and Google liable on all counts in the first social media addiction trial to reach a verdict, ordering the companies to pay $6 million in total damages to a 20-year-old woman identified as K.G.M. The breakdown: $3 million in compensatory damages, split 70/30 between Meta and Google, plus an additional $3 million in punitive damages ($2.1 million from Meta and $900,000 from Google). Jurors concluded that Instagram and YouTube were deliberately designed to be addictive and that executives knew their platforms harmed minors. Internal Meta documents shown during the seven-week trial included one stating, “If we wanna win big with teens, we must bring them in as tweens” (NPR).

The dollar amount is meaningless for companies worth trillions. The precedent is not. This was a bellwether trial selected to guide resolution of approximately 1,500 to 2,000 pending lawsuits by parents, school districts, and individuals, with more than 10,000 individual cases and roughly 800 school district claims pending nationwide. A federal trial is set for this summer in Oakland. The verdict landed one day after a separate New Mexico jury ordered Meta to pay $375 million for violating consumer protection laws related to child exploitation. The legal strategy that proved effective here focused on platform design flaws, such as infinite scroll, autoplay, and algorithmic amplification, rather than content, which allowed plaintiffs to sidestep Section 230 immunity protections. Meta and Google both plan to appeal (Bloomberg).

Sensei’s Insight: The legal playbook that won here, targeting design choices rather than content, could apply far beyond social media. Any platform that uses algorithmic engagement loops to retain users is now on notice. The financial risk is not this verdict. It is the signal it sends to the 1,500 cases behind it and the potential for aggregate settlements that could reach the billions.

🤖 Arm Makes History With First In-House Chip as Stock Surges 15%

Arm Holdings (NASDAQ: ARM 0.00%↑) announced its first-ever in-house chip, the AGI CPU, at an event in San Francisco earlier this week, sending shares up 15% yesterday in the stock’s largest single-day gain in nearly a year. After 35 years of licensing its chip designs to companies like Apple, Nvidia, and Amazon, Arm is now making physical silicon. The AGI CPU is a data centre processor optimised for artificial intelligence (AI) inference, built on Arm’s Neoverse architecture and manufactured by Taiwan Semiconductor Manufacturing Company (TSMC) on its 3-nanometre process. Meta is the lead customer, with OpenAI, Cloudflare, SAP, and more than 50 other ecosystem partners committed (CNBC).

The financial ambition is striking. CEO Rene Haas said the AGI CPU alone is expected to generate $15 billion in annual revenue by 2031, with total company revenue reaching $25 billion and earnings per share (EPS) of $9. For context, Arm generated $4 billion in revenue in fiscal 2025. CFO Jason Child said the chip will sell at roughly 50% gross margin, significantly expanding Arm’s profit opportunity beyond its traditional royalty model. Arm’s pitch to data centre operators is efficiency: up to 64 AGI CPUs, containing approximately 8,700 cores, fit in a single air-cooled rack, delivering what Arm claims is twice the performance per watt of competing x86 architecture from Intel and AMD. The move puts Arm in direct competition with some of its own licensees for the first time (Bloomberg).

Sensei’s Insight: Arm is essentially building the AMD playbook of 2017, moving from IP licensor to silicon competitor, except it starts with more than 99% smartphone market share and the entire AI ecosystem already built on its architecture. The risk is alienating licensees. The reward is a revenue base six times its current size.

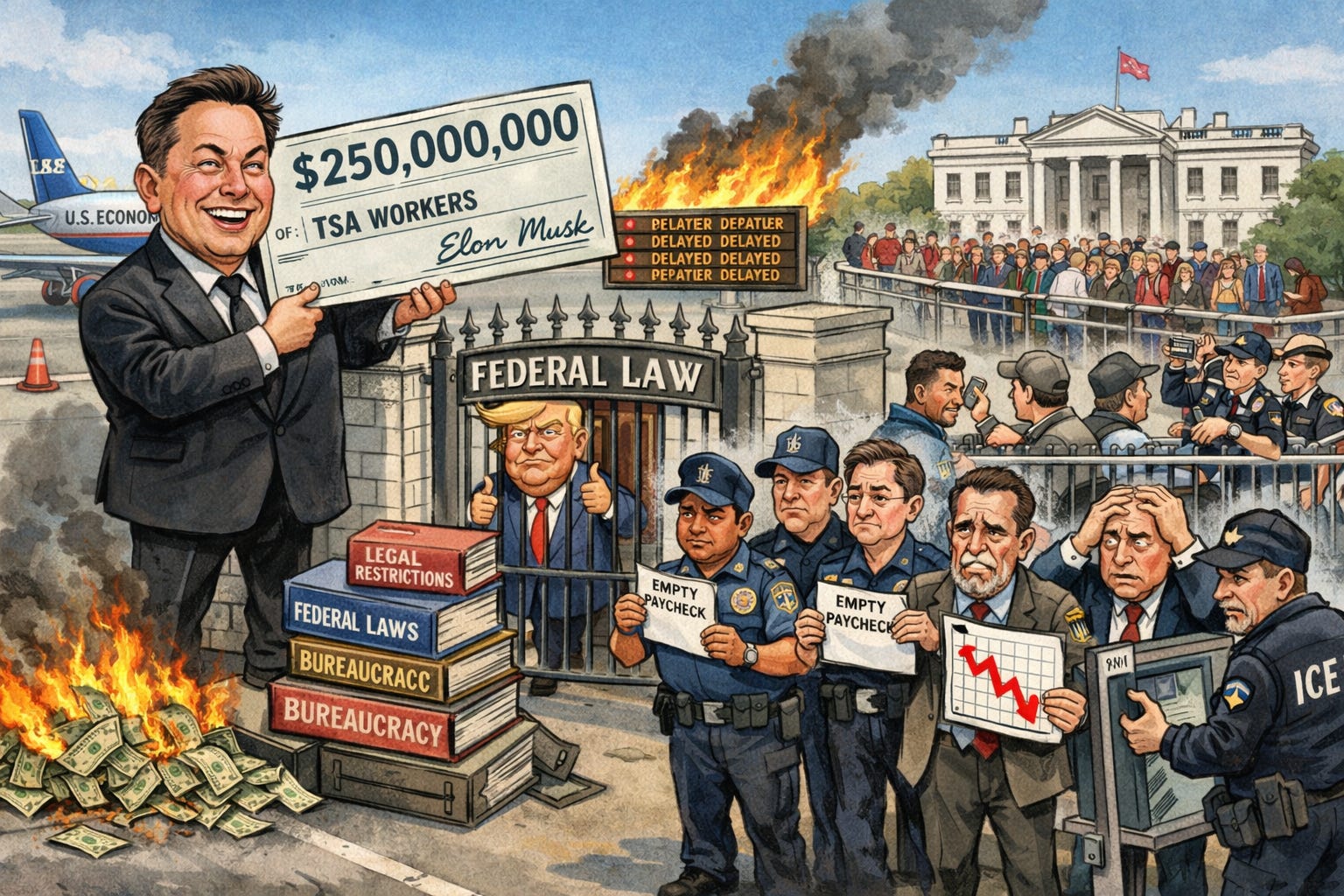

✈️ White House Rejects Musk’s $250 Million Offer to Pay TSA Workers

Elon Musk posted on X last week offering to personally cover the salaries of Transportation Security Administration (TSA) officers during the ongoing Department of Homeland Security (DHS) funding shutdown, an offer estimated at roughly $250 million. President Trump initially reacted positively, but the White House ultimately rejected the proposal, citing legal barriers: federal law prohibits outside individuals from directly paying government employees. The DHS shutdown, now in its 40th day and the second in six months, has left approximately 50,000 TSA officers working without pay, with many about to miss their second full paycheck. More than 300 officers have resigned since the shutdown began, and call-out rates have exceeded 50% in Houston and 30% in New Orleans and Atlanta (Reuters).

The airline industry is bleeding. Delta estimated a $200 million pretax profit hit, United recorded a $250 million loss, and American Airlines projected a $325 million revenue shortfall. The industry warns of $580 million in daily economic losses if the gridlock persists through peak spring break travel, when 171 million passengers are projected. Security wait times at major airports have ballooned to two to three hours. Senate negotiators say they have “narrowed remaining disputes” on a bipartisan deal, but no resolution has been reached. Trump deployed hundreds of Immigration and Customs Enforcement (ICE) agents to 14 airports this week to assist with screening, though they lack formal TSA training (CNBC).

Sensei’s Insight: Airline stocks are caught in a compounding crisis: the DHS shutdown plus Iran-driven fuel costs hitting simultaneously. Any bipartisan deal would provide immediate relief, but the longer this drags, the more permanent the damage becomes as experienced TSA officers leave for good. Watch for a resolution this week. If it doesn’t come, expect airline earnings guidance to start getting pulled.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: WEEKLY JOBLESS CLAIMS CHEAT SHEET

Thursday, March 26, 2026 | 12:30 PM GMT / 8:30 AM ET

Initial and Continuing Jobless Claims drop today at 8:30 AM Eastern. In a normal cycle, this is a mid-tier weekly release. Right now, it is one of the most important data points in markets. The labour market is the last pillar holding the “no fire” narrative together, and today’s print either reinforces it or cracks the foundation at the worst possible time: inflation is reaccelerating, the Fed is boxed in, and the economy just lost 92,000 jobs in February.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.