Morning Forecast: Thursday 28 May

The Fed's inflation number drops this morning, and we've broken down every line in today's cheat sheet.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🤖 Marvell raises, lifts AI trade: Record quarter and a bigger guide point to chip capex accelerating into 2027.

🛢️ Brent swings on Iran strikes: A second round of US strikes lifts crude even as a ceasefire framework circulates.

✈️ Boeing wins 47-jet clearance: Regulators sign off on a higher MAX rate, the cleanest production upgrade in two years.

💰 Dimon flags trading boom, exuberance: JPMorgan eyes its second-best trading quarter, then warns the backdrop echoes past tops.

🍽️ One in ten short on food: New York Fed research shows food insecurity has doubled, signalling the lower consumer is cracking.

🧑💻 OpenAI commits $250M to workers: The non-profit’s first big spend targets retraining and wage support for displaced workers.

⛽ Gas tax holiday gains traction: Two competing bills aim to suspend the federal levy as pump prices hit four-year highs.

📊 PCE print lands today: The Fed’s preferred inflation gauge could front-run hike risk if core runs hot.

📈 Bitcoin drifts toward flag support: Trading near 73,000 in a downtrend, a break below 70,000 could open 60,000.

🧠 One Big Thing

The market is leaning on one engine. The index is at records, but it is standing on a single leg. Marvell's raise and the hyperscalers' roughly $725 billion capex guide are doing the work rate cuts normally would, holding stocks up while the rest of the picture weakens. The New York Fed's food data, the 44.8 sentiment print and Dimon's exuberance warning all point the other way. So the rally rests on AI spending while the broad consumer cracks underneath. Broadcom on June 3 is the next test, and a soft guide could knock the one leg out from under a tiring tape.

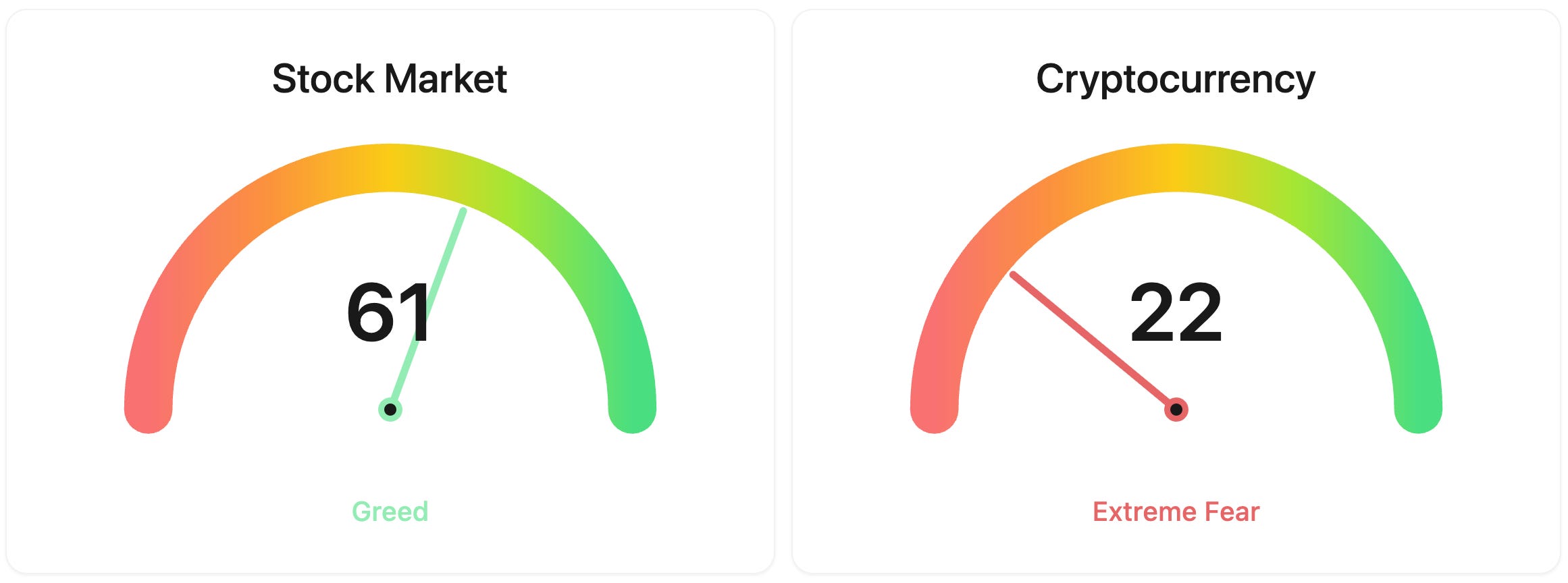

⚖️ Fear & Greed

📉 The Number That Matters

10%

Some 10% of US households said they lacked enough food in February, up from 4% in mid-2020, a doubling that signals the lower-income consumer is cracking even with unemployment near record lows.

⚔️ Winners vs Losers

Winners

SNOW 0.00%↑: Snowflake Inc. soared after reporting fiscal Q1 product revenue of $1.33 billion, up 34% and its strongest sequential dollar growth ever, and raising full-year product revenue guidance to roughly $5.84 billion, lifting expected growth from 27% to 31%. The report also featured surging AI demand, the Natoma acquisition, and an expanded AWS deal.

UMAC 0.00%↑: Unusual Machines, Inc. jumped after its partner Powerus was selected for Phase II of the Pentagon’s $1 billion Drone Dominance Program, with the rally amplified by reports that the Trump administration is in talks to fund domestic drone makers through a mix of debt and equity.

CRSR 0.00%↑: Corsair Gaming, Inc. extended a multi-day rally on enthusiasm for its new CORSAIR PRO line of AI workstations and servers built on Nvidia Grace Blackwell technology, building on a strong Q1 earnings beat and elevated short interest that has added fuel to the move.

PHR 0.00%↑: Phreesia, Inc. climbed after fiscal Q1 revenue rose 13% to $130.9 million and management reaffirmed full-year revenue guidance of $510 million to $520 million, pointing to momentum in its AccessOne business and new provider marketing offerings.

RCAT 0.00%↑: Red Cat Holdings, Inc. rose after H.C. Wainwright initiated coverage with a Buy rating and a $20 price target, with sentiment further boosted by a contract to supply 173 Black Widow drones to Japan’s Ground Self-Defense Force and its acquisition of wireless-power firm Quaze Technologies.

NCNO 0.00%↑: nCino, Inc. gained after fiscal Q1 revenue of $159.4 million beat estimates and grew 11%, with adjusted operating margin expanding sharply, prompting the company to lift its full-year revenue outlook.

DLTR 0.00%↑: Dollar Tree, Inc. rallied after reporting Q1 results with net sales up 7.2%, comparable store sales up 3.5%, and adjusted EPS up 38% to $1.74, well ahead of expectations, while raising its full-year adjusted EPS outlook to $6.70 to $7.10.

NBIS 0.00%↑: Nebius Group N.V. advanced after Situational Awareness LP disclosed a 5.6% stake of more than 12.4 million shares, a passive position with no activist intentions that the market read as a vote of confidence in the AI infrastructure firm.

NOW 0.00%↑: ServiceNow, Inc. moved higher with no specific overnight catalyst identified, appearing to ride a software sector rally sparked by Snowflake’s blowout results alongside continued optimism from its Knowledge 2026 AI announcements and recently raised guidance.

Losers

P 0.00%↑: Everpure, Inc., the data storage company formerly known as Pure Storage, fell despite beating on fiscal Q1 revenue and earnings and raising full-year guidance, a sell the news reaction after shares had run up sharply into the report and as the next-quarter outlook implied a steep sequential revenue decline.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $73,456 (▼ -1.20%)

Ethereum (ETH): $1,992 (▼ -1.52%)

XRP: $1.29 (▼ -1.12%)

Equity Indices (Futures):

S&P 500: $7,526 (▼ -0.19%)

NASDAQ 100: $29,921 (▼ -0.42%)

FTSE 100: £10,394 (▼ -0.92%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.50% (▲ 0.38%)

Oil (WTI): $91 (▲ 1.60%)

Gold: $4,386 (▼ -1.57%)

Silver: $72.95 (▼ -2.26%)

Data as of: UK (BST) 11:47 BST / US (EDT): 06:47 EDT / Asia (Tokyo): 19:47

✅ 5 Things to Know

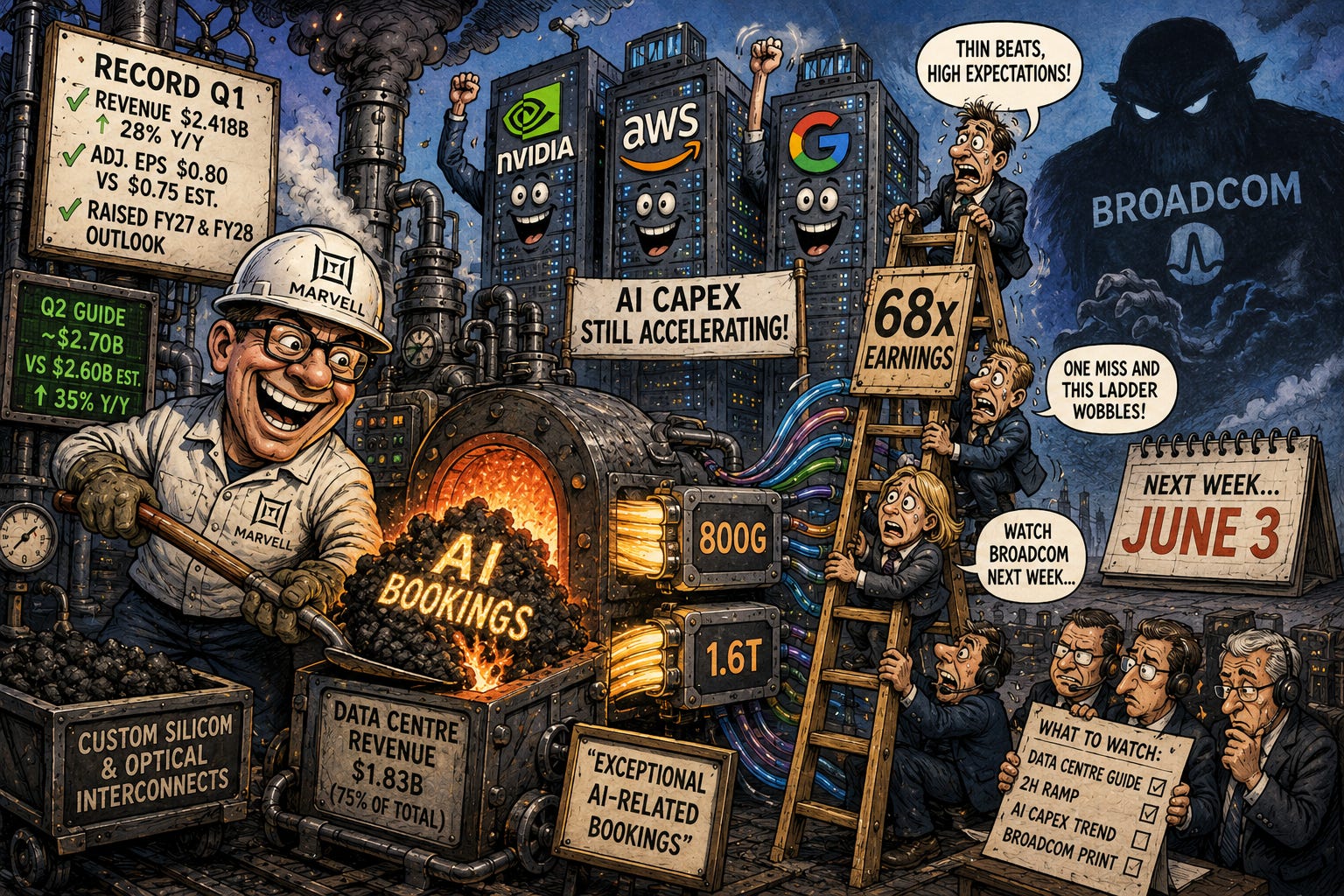

🤖 Marvell Beats and Raises, AI Trade Catches a Bid

Marvell Technology reported record fiscal first-quarter results after the close yesterday and lifted its full-year outlook for both fiscal 2027 and 2028, giving the AI infrastructure trade fresh ammunition for today’s open. Revenue came in at $2.418 billion, up 28% year on year and just ahead of the $2.40 billion analysts expected. Adjusted earnings per share landed at $0.80 against $0.75 estimated. The bigger move was the guide: Marvell sees second-quarter revenue around $2.70 billion, well above the $2.60 billion consensus and pointing to 35% year-on-year growth. The stock gained roughly 5% to 7% in extended trading after a 145% run year to date. (Bloomberg)

Marvell sits at the centre of the picks-and-shovels trade powering this year’s chip rally. It sells the custom silicon and optical interconnects that move data between processors inside hyperscaler data centres, and CEO Matt Murphy pointed to “exceptional AI-related bookings” as the reason for the raise. Data centre revenue hit a record $1.83 billion last quarter, three-quarters of the business, and the company is shipping 800G and 1.6 terabit optical modules into Nvidia, Amazon and reported Google projects. The next read on the AI capex cycle is Broadcom on June 3, the largest direct comparable and the bigger market-mover. (Yahoo Finance)

Sensei’s Insight: The headline beats were thin, but the raised full-year outlook says AI capex is still accelerating into 2027, not peaking. Marvell trades near 68 times earnings, so even a clean print can be sold if Broadcom disappoints next week. Watch the implied second-half ramp on tonight’s data centre commentary from the call.

🛢️ US Strikes Iran Again Even as a Deal Nears

The United States struck targets in southern Iran again overnight, the second round of strikes this week, even as President Trump insists a deal to reopen the Strait of Hormuz is close. US Central Command said the strikes hit a military site and that it shot down Iranian drones it said threatened American forces and shipping near the strait, the chokepoint that carried about a fifth of the world’s seaborne oil before the war. Crude swung on the news. Brent, the global benchmark, rose about 2% to around $96 a barrel today, clawing back part of a steep drop earlier in the week when Trump said talks were “proceeding nicely.” (CNBC)

The whipsaw captures the bind traders are in: a framework is on the table, but the fighting has not stopped. The outline under discussion runs to a 60-day ceasefire that would reopen Hormuz with no tolls, see Iran clear the mines it laid, and lift the US blockade in stages while nuclear talks continue. Iranian state media floated a version of it this week, and the White House dismissed that account as a fabrication. The hard items left unresolved are Iran’s enriched-uranium stockpile and billions in frozen Iranian assets. Brent is down roughly 13% over the past month on deal hopes but still sits far above pre-war levels, and Trump’s cabinet met at Camp David to weigh next steps. (Axios)

Sensei’s Insight: Every $10 move in Brent shifts US inflation by about two-tenths of a percentage point, and the Federal Reserve’s preferred price gauge for April lands this morning. A signed ceasefire would cool energy costs fast. Another round of strikes could send them straight back up.

✈️ Boeing Cleared to Build 47 MAX Jets a Month

Boeing has the green light from the Federal Aviation Administration to lift 737 MAX production from 42 jets a month to 47, the strongest sign yet that the company’s two-year quality overhaul is translating into output. CEO Kelly Ortberg told the Bernstein Strategic Decisions Conference yesterday that Boeing has “passed the capstone review” for the higher rate and is “off and rolling” on the new pace, with the line expected to stabilise over the next couple of months. He reiterated a target of 52 jets a month early next year through a fourth assembly line in Everett, Washington, and an aspirational rate of 63 longer term. Boeing shares climbed about 3.6% intraday on the comments. (CNBC)

The certification of the smaller MAX 7 and longer MAX 10 is the other shoe still to drop, and both look on track for this year. More than 80% of certification flight testing is complete, FAA Administrator Bryan Bedford has said publicly he sees no obstacle to approval by year-end, and Southwest Airlines CEO Bob Jordan expects the MAX 7 cleared by August. Together those two models cover more than 1,700 aircraft on order, with Southwest holding around 90% of the MAX 7 book. Each extra jet a month is roughly $50 to $60 million of revenue, and a higher rate flows directly into Spirit AeroSystems, RTX, GE Aerospace and Howmet. (Yahoo Finance)

Sensei’s Insight: This is the first time in two years Boeing’s production guidance has moved up without an asterisk. The capstone review was the regulator’s structural sign-off, which means the next ramp to 52 is an execution question, not an FAA question. The MAX 7 and MAX 10 certifications are the next catalyst.

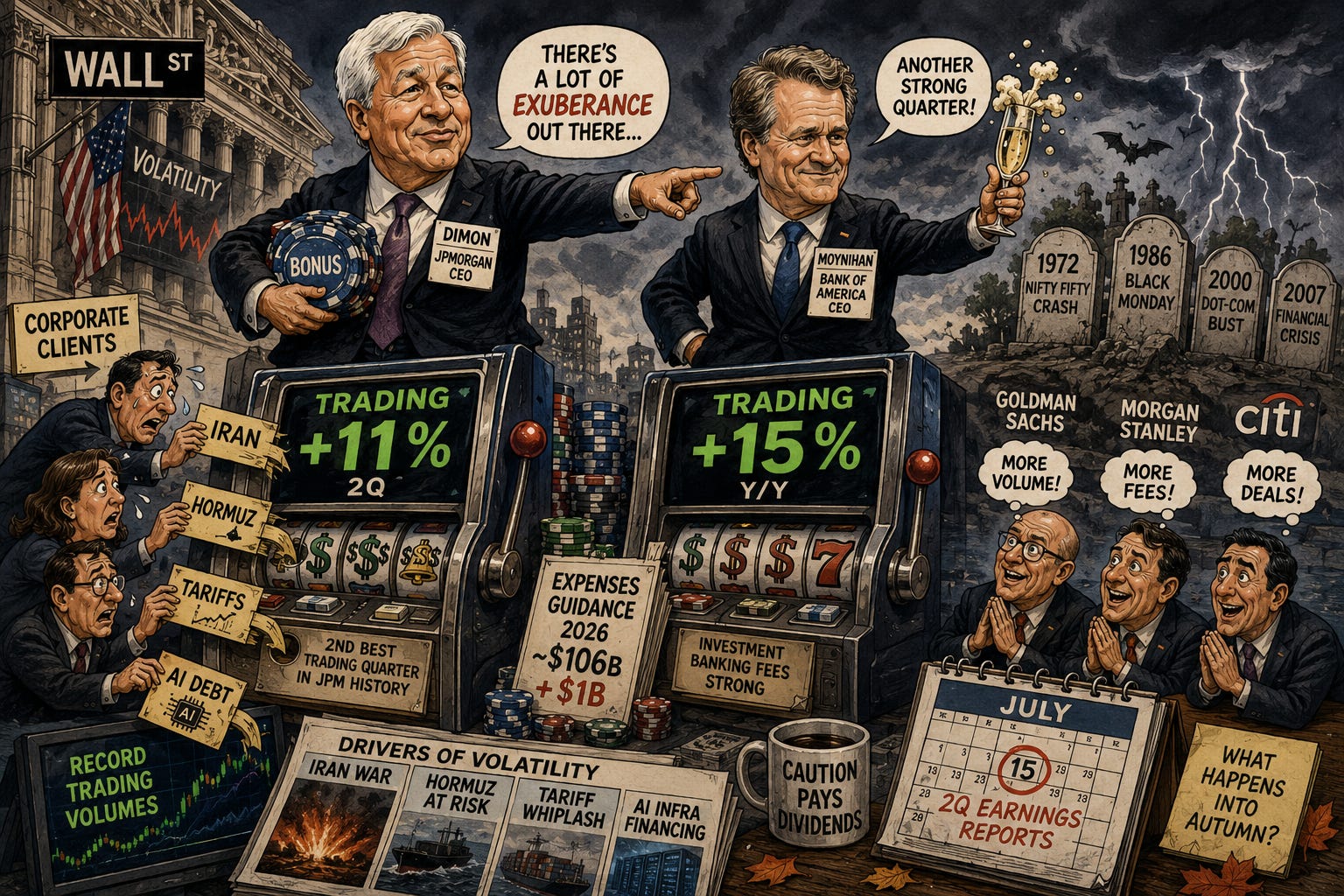

💰 Dimon Sees Trading Up 11%, Then Warns of “Exuberance”

The two most-watched US bank CEOs took the stage at Bernstein’s conference yesterday and delivered the same message: trading desks are having an extraordinary quarter. Jamie Dimon said JPMorgan’s markets revenue could rise about 11% in the second quarter, which would make it the second-best trading quarter in the bank’s history. An hour later, Bank of America CEO Brian Moynihan said BofA expects sales and trading up roughly 15% year on year with investment banking fees up “strong.” Dimon also raised JPMorgan’s 2026 expense guidance by about $1 billion to roughly $106 billion, citing higher variable compensation tied to the trading boom. JPMorgan shares slipped nearly 3% intraday on the expense raise before paring losses. (Yahoo Finance)

The volatility driving these numbers is the same set of stories making everyone else nervous: the Iran war, Hormuz, tariff shifts and AI infrastructure financing. Corporate clients are hedging more, banks earn fees on the volume, and the result is a near-record quarter. Dimon was blunt about what comes next: “There’s a lot of exuberance out there, so yeah, right now, it’s good, but it was in ‘72, ‘86, 2000, 2007. That doesn’t give me comfort.” The read-through is positive for Goldman Sachs, Morgan Stanley and Citi, all of which run capital-markets businesses tied to the same volume surge. (Bloomberg)

Sensei’s Insight: Dimon listing 1972, 1986, 2000 and 2007 is the closest thing to a public warning a sitting bank CEO will issue while still telling shareholders trading is booming. Both can be true. The confirming print is second-quarter earnings in July; the worry is what corporate dealmaking does into the autumn.

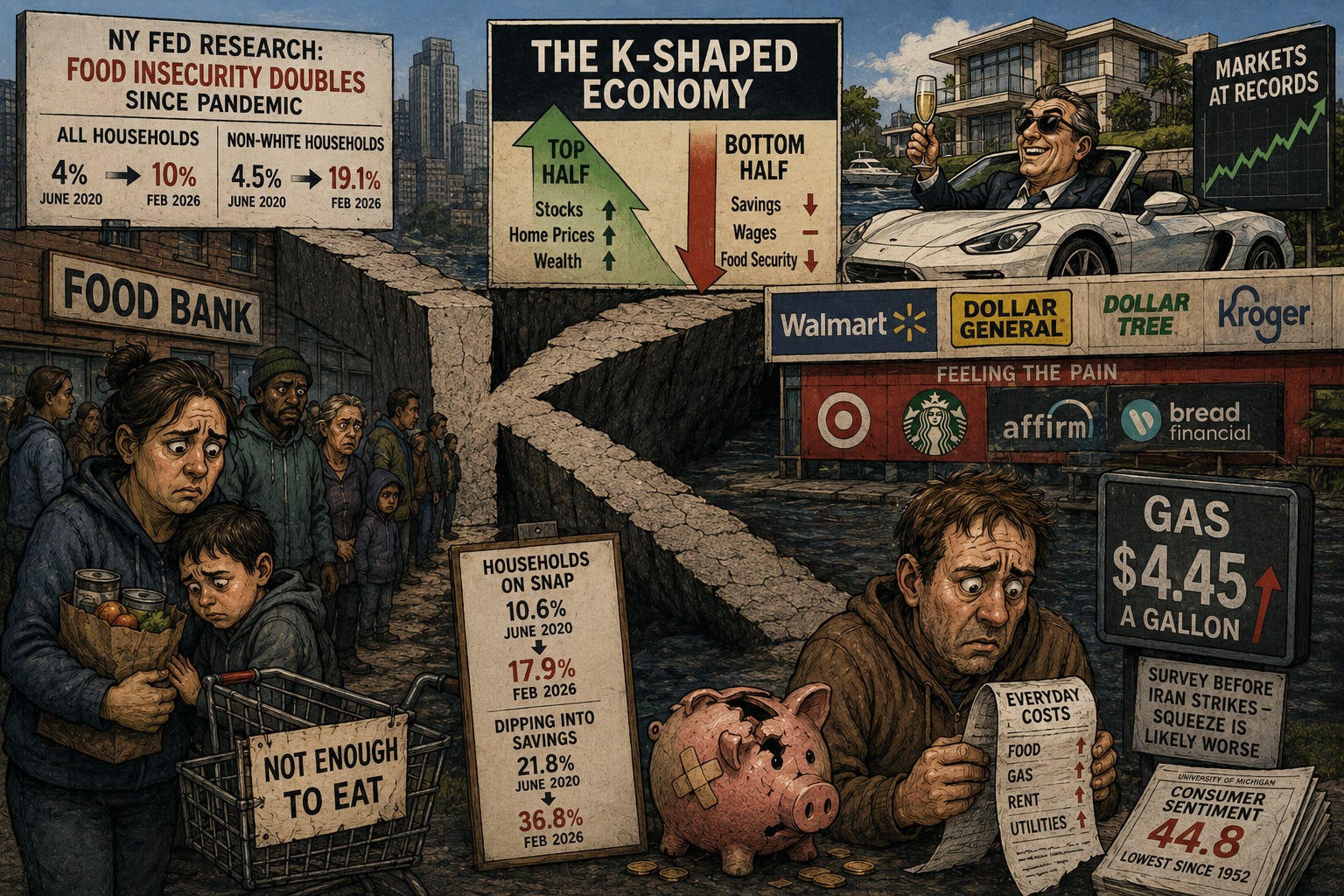

🍽️ One in Ten Americans Now Short on Food

The New York Federal Reserve published research yesterday showing food insecurity among US households has more than doubled since the start of the pandemic. Drawing on its Survey of Consumer Expectations, the bank found that 10% of households said they did not have enough food in February 2026, up from 4% in June 2020. Among non-white households the figure climbed to 19.1% from 4.5%. The share on SNAP food stamps rose to 17.9% from 10.6%, and 36.8% of households reported dipping into savings to cover everyday expenses, against 21.8% in 2020. Fed researchers called the increase “remarkable” and concentrated in lower-income and lower-educated households with young children. (CNBC)

The Fed tied the jump explicitly to a “K-shaped” economy, where wealthier households are gaining from stock and house prices while lower-income ones are running down savings and turning to food aid. The data was collected before US strikes on Iran pushed retail gasoline to $4.45 a gallon, which means the actual squeeze is likely worse than the survey shows. The University of Michigan consumer sentiment index hit 44.8 last week, the lowest reading since the survey began in 1952. For retail investors, the trade-down runs through staples and dollar-store names like Walmart, Dollar General, Dollar Tree and Kroger, with the pain felt by discretionary mid-tier (Target, Starbucks) and subprime credit (Affirm, Bread Financial). (CNN)

Sensei’s Insight: This is the cleanest signal yet that the bottom half of the consumer is breaking even with unemployment near record lows. The Fed has another reason to wait on cuts. Retailers tied to lower-income spending have another reason for caution, even as the high-end keeps holding up.

Stories You Might Have Missed

🧑💻 OpenAI Pledges $250M for Workers AI Displaces

The OpenAI Foundation, the non-profit that controls OpenAI, said yesterday it will commit $250 million in grants, partnerships and direct programs to help workers and economies disrupted by artificial intelligence. The pledge is the first specific spend from the foundation since its restructuring closed last October and is structured around three priorities: studying how AI is reshaping the economy, supporting workers through near-term disruption (including wage-loss insurance and retraining), and exploring longer-term ideas, including shifting taxation from labour toward capital and sovereign-wealth-fund-style distribution models. The foundation owns 26% of OpenAI Group, valued at around $130 billion, implying an OpenAI valuation near $500 billion. The political question now is whether other AI labs match the commitment or push back on the tax direction OpenAI is floating, particularly as Block and Standard Chartered cite AI efficiency for recent layoffs. (Yahoo Finance)

⛽ Gas Tax Holiday Push Picks Up in Washington

With US retail gasoline at a four-year high of $4.45 a gallon, two competing bills to suspend the federal gas tax are now live in Congress: Senator Josh Hawley’s 90-day Republican version with a Highway Trust Fund bailout, and the Gas Prices Relief Act from Senators Mark Kelly and Richard Blumenthal that runs the holiday until October 1. President Trump said yesterday he supports a suspension but wants states to move first. The economics are settled, even if the politics are not. The federal gas tax is 18.4 cents a gallon, unchanged since 1993; the best peer-reviewed work puts the consumer pass-through at 79%, meaning roughly a fifth of any cut goes to refiners. The Bipartisan Policy Center estimates pump savings of 10 to 16 cents a gallon, or about $8.90 a month for the average driver, against a fiscal cost of around $21 billion for a six-month holiday. Refiners (Valero, Marathon Petroleum, Phillips 66) tend to capture a portion of the pass-through; aggregates names (Vulcan, Martin Marietta) face a small headwind if Trust Fund capacity erodes. (Bloomberg)

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

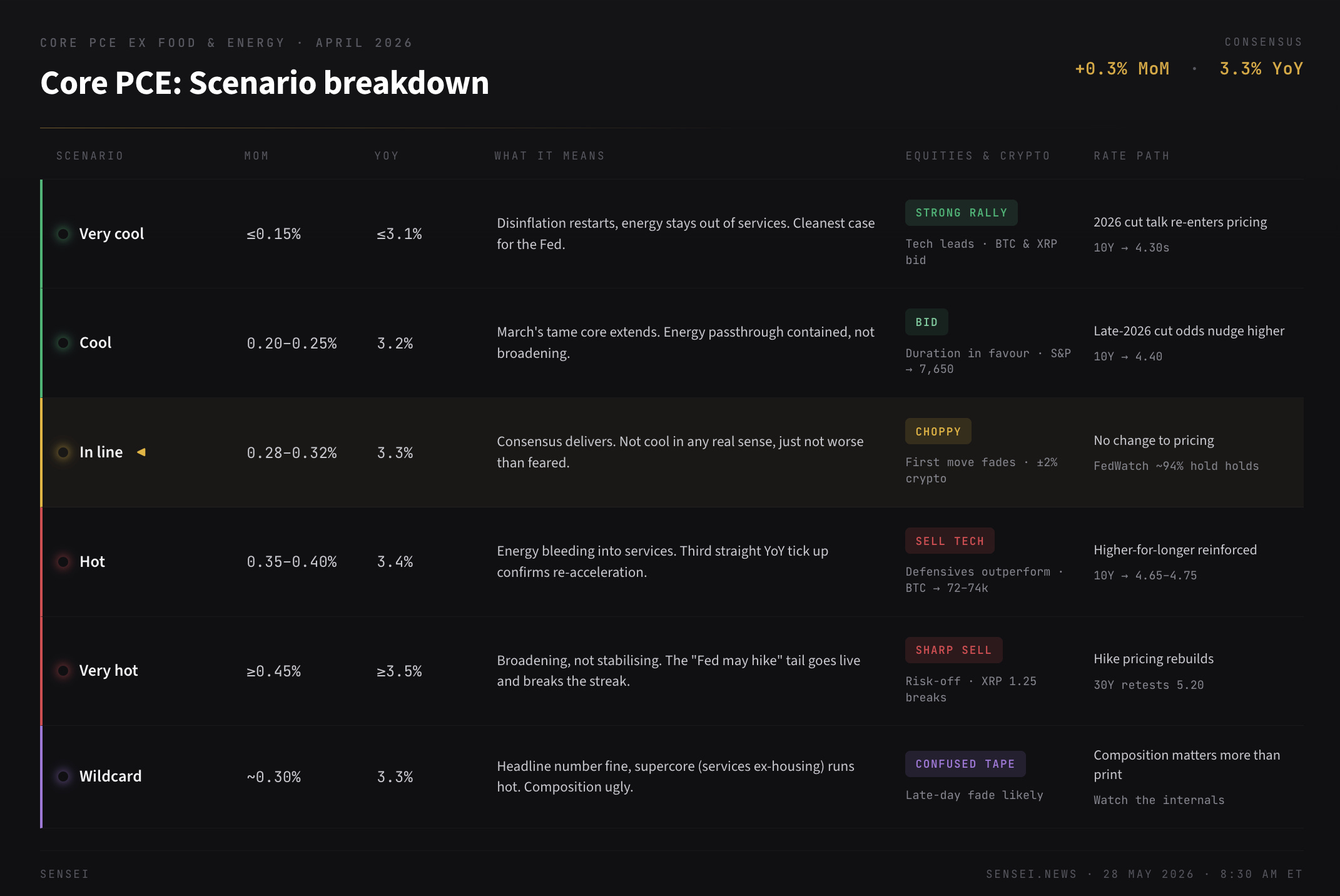

📊 PCE Day: The Cheat Sheet

At 1:30pm UK the Bureau of Economic Analysis drops April PCE, the Fed’s preferred inflation gauge, at the same minute as the second estimate of Q1 GDP and a batch of activity data. Fifteen US lines hit the wire together, so the first move can be noisy. The market walks in from record highs and an eight-week win streak, the longest since December 2023, with the VIX near 16. PCE sets the tone, so we start there, then work through the rest of the slate.

The main event: PCE

PCE is the number the Fed actually targets, and three things make this one heavier than a routine data day. First, the target is 2% headline PCE over the long run, and a 2% trend is only about 0.17% a month. A 0.3% core reading compounds to roughly 3.7% annualised, so the 0.3% consensus is not cool, it is just not worse than feared. Second, the committee has turned hawkish: the Fed held at 3.50 to 3.75% in April on an 11 to 1 vote, with four total dissents, the most since 1992 [CNBC], and the minutes showed many members saying hikes could become appropriate if inflation stayed hot. Third, Kevin Warsh took over as Chair in May, and early messaging from Jefferson and Cook has leaned toward inflation risk, not rescue. CME’s FedWatch now puts June at around 94% hold, and a Reuters poll found most economists no longer expect a cut this year, with rate futures at one point pricing a hike rather than a cut as the next move [Reuters]. So a hot print does not just delay cuts, it pulls hike risk forward.

Core strips out food and energy and is the cleaner trend read. At 0.2% month-on-month or below the market can call it progress, 0.3% is survivable, 0.4% or higher becomes a policy problem.

Headline includes energy, and this cycle the inflation scare is an energy story, so it carries more weight than usual. Headline and core are best read together, which is what the matrix table below shows.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.