Morning Forecast: Thursday, 9 April

Three Ships Got Through Hormuz Yesterday. The Normal Number Is 135.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🕊️ Fragile Mideast Truce Under Threat: Israel strikes Hezbollah while the Strait of Hormuz remains largely closed.

🏦 Fed Minutes Signal Potential Hikes: Officials debate raising rates as the committee acknowledges growing stagflation risks.

✈️ Fuel Costs Dampen Delta Gains: Record revenues face a projected two billion dollar fuel price headwind.

🏦 Private Credit Faces Redemption Crisis: Redemptions spike as the Federal Reserve warns of systemic industry contagion.

🌍 Trump Weighs NATO Troop Relocations: The administration suggests moving US troops to more supportive European allies.

🔍 Inflation Pressures Precede Energy Shock: Pre-war data shows high price pressures existed before the global crisis.

🧠 One Big Thing

The Fed’s Hawkish Pivot

The Federal Reserve is pivoting from planning rate cuts to discussing potential interest rate hikes. Internal minutes show a growing consensus that higher borrowing costs may be required if price pressures do not subside. This shift in policy direction occurred even before the Middle East conflict caused oil prices to surge. Economic data indicates that underlying inflation was already trending higher in February regardless of energy market volatility. For investors, this suggests that the central bank will prioritize fighting inflation over supporting growth during the current geopolitical crisis. Market pricing now indicates that borrowing costs will likely stay steady or increase throughout the year.

⚖️ Fear & Greed

📉 The Number That Matters

$100

WTI crude prices rebounded to $100 per barrel as the Strait of Hormuz remained closed despite a fragile ceasefire. Only three ships exited the passage yesterday, compared to the normal daily average of 135 vessels.

⚔️ Winners vs Losers

Winners

STAA 0.00%↑: STAAR Surgical Company surged after reporting preliminary Q1 2026 net sales exceeding $90 million, more than doubling the $42.6 million from the year-ago quarter, driven primarily by strong demand in China and double-digit growth in the Americas.

WSR 0.00%↑: Whitestone REIT jumped after announcing a definitive agreement to be acquired by Ares Management for $19.00 per share in an all-cash deal valued at approximately $1.7 billion, representing a 12.2% premium to the prior close.

Losers

ABUS 0.00%↑: Arbutus Biopharma Corporation drifted lower in pre-market with no specific catalyst identified, as the stock continues to consolidate following its massive rally on the $2.25 billion Moderna patent settlement announced in early March.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $71297 (▲ 0.33%)

Ethereum (ETH): $2191 (▲ 0.05%)

XRP: $1.33 (▼ -0.68%)

Equity Indices (Futures):

S&P 500: $6755 (▼ -0.29%)

NASDAQ 100: $25021 (▼ -0.21%)

FTSE 100: £10575 (▼ -1.04%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.29% (▼ -0.14%)

Oil (WTI): $100 (▲ 3.17%)

Gold: $4742 (▲ 0.48%)

Silver: $74.07 (▼ -0.04%)

Data as of: UK (BST) 12:00 / US (EDT): 07:00 / Asia (Tokyo): 21:00

✅ 5 Things to Know Today

🕊️ Ceasefire Holds on Paper, but Hormuz Stays Shut and Lebanon Burns

The fragile US-Iran truce survived its first full day, but barely. Despite a notable drop in strikes across Arab Gulf states, the two sides spent yesterday accusing each other of violations while the Strait of Hormuz, through which roughly a fifth of the world’s oil and liquefied natural gas flowed before the war, remained largely closed. The White House confirmed Vice President JD Vance will lead a delegation to Islamabad for direct talks with Iran this weekend, joined by special envoy Steve Witkoff and Jared Kushner. Iran’s team is expected to arrive in the Pakistani capital today. Oil rebounded sharply after yesterday’s 16% WTI collapse, the biggest single-day crude drop since April 2020, with Brent trading just below $98 a barrel and WTI at a similar level. The ceasefire had triggered a massive relief rally: the Dow surged 1,325 points, or 2.85%, its best day since April 2025, the S&P 500 jumped 2.51%, and energy was the only sector in the red. But the optimism faded overnight, with Asian shares down 0.9% and US futures slipping 0.3% (Bloomberg).

The biggest obstacle is Lebanon. Israel launched its largest assault on the country since the conflict began, striking more than 100 Hezbollah targets within 10 minutes yesterday. At least 182 people were killed and hundreds wounded, bringing Lebanon’s total death toll to more than 1,730 with over one million people displaced. Vance insisted the US never promised the ceasefire would extend to Lebanon: “we never made that promise, we never indicated that was gonna be the case.” Iran sees it differently. Foreign Minister Abbas Araghchi said in a social media post that the US must choose between “ceasefire or continued war via Israel. It cannot have both.” Parliament Speaker Mohammad-Bagher Ghalibaf cited the Lebanon strikes, an alleged drone incursion into Iranian airspace, and the denial of Iran’s enrichment rights as reasons negotiations are “unreasonable.” Hezbollah responded by firing rockets toward Israel.

On the Strait, ships are inching closer but not yet through. Three Chinese supertankers and a Saudi vessel laden with crude sailed east toward Hormuz yesterday, joining a growing pool waiting to exit. But Iran made a rare reference to sea mines in the area, establishing two designated safe routes and requiring all ships to coordinate with the Islamic Revolutionary Guard Corps (IRGC) before transit. More than 800 freighters remain stranded inside the Persian Gulf. In normal times about 135 vessels cross daily; yesterday just three left. Iran also told mediators it would limit passage to roughly a dozen ships per day and charge tolls, an arrangement the White House has not accepted. Trump posted late yesterday that US military personnel and weaponry would remain in place “until such time as the REAL AGREEMENT reached is fully complied with,” adding that if Iran fails to comply, “the ‘Shootin’ Starts.’” Goldman Sachs warned that if Hormuz stays closed for another month, Brent could average above $100 a barrel through the rest of the year (Barron’s).

Sensei’s Insight: The mine reference changes everything. Mines take weeks to clear even after a deal is signed, and Iran now has a technical excuse to restrict Hormuz indefinitely without violating a ceasefire. The market priced in a clean resolution yesterday. The physical evidence, three ships through versus 135 on a normal day, says the resolution has not even started.

🏦 Fed Minutes Reveal a Committee Frozen Between Rate Hikes and Cuts

The Federal Reserve released minutes from its March 17-18 meeting yesterday, and they show a central bank paralysed by two-sided risk. The Federal Open Market Committee (FOMC) voted 11-1 to hold rates at 3.50% to 3.75%, with Governor Stephen Miran the sole dissenter, preferring a 25 basis-point cut. That is down from two dissenters in January, when Governor Christopher Waller also voted to cut. Waller’s flip back to holding is the most significant individual shift: if even the doves are retreating, internal momentum for easing has stalled. “Most participants” said it was “too early to know” how the Iran war would affect the economy, but the committee formally acknowledged geopolitical risk in its statement for the first time. The staff revised its growth outlook down to “about in line with potential,” down from above potential in January, while inflation forecasts were revised higher for the second consecutive meeting, a combination that one analyst described as “the definition of stagflation risk” (Bloomberg).

The most striking development is the escalation in rate hike language. In January, “several participants” raised rate increases as a hypothetical. In March, “many participants” said hikes could be warranted if inflation stays elevated, and “some participants” pushed for hike language to appear in the official post-meeting statement. Core Personal Consumption Expenditures (PCE) inflation hit 3.1% in January, up from 2.8% in the prior reading, and the staff estimated February at 3.0%. The “vast majority” of officials now believe progress toward the Fed’s 2% target “could be slower than previously expected.” At the same time, the committee acknowledged growing downside risks to employment, reversing the January assessment that those risks had “diminished.” Several officials warned that after five years of above-target inflation, longer-term expectations “could become more sensitive to energy price increases,” a new concern that signals rising de-anchoring risk. Futures markets tell the story: nearly 90% of participants now expect rates to stay unchanged through September, and the probability of at least one hike through early 2027 has risen to about 30%.

Sensei’s Insight: The hike discussion moved from “several” to “many” in one meeting, and a subset now wants it in the official statement. Tomorrow’s March Consumer Price Index (CPI) is the catalyst. If core inflation broadens above 3%, the repricing toward zero cuts or an outright hike accelerates fast. These minutes tell you where the committee was before the ceasefire, and it was closer to hiking than cutting.

✈️ Delta Posts Record Revenue but Warns of a $2 Billion Fuel Hit Ahead

Delta Air Lines kicked off earnings season yesterday with a first-quarter revenue record of $14.2 billion, up 9.4% from a year ago, and adjusted earnings per share of $0.64, a 44% jump from the prior year. The airline beat Wall Street expectations on revenue and met its own January guidance despite a meaningful increase in fuel costs, harsh winter weather, and a healthcare strike that dragged on February payrolls. Premium ticket revenue rose 14% to $5.4 billion, corporate sales hit a quarterly record with double-digit growth across all sectors, and American Express remuneration climbed 10% to more than $2 billion. Shares surged roughly 11% yesterday, riding the double tailwind of strong results and the ceasefire-driven collapse in crude prices (CNBC).

The forward guidance is where it gets complicated. Delta is projecting second-quarter fuel costs of approximately $4.30 per gallon, roughly double the year-ago period, creating a fuel expense increase of more than $2 billion. The airline guided second-quarter earnings between $1.00 and $1.50 per share on an operating margin of 6% to 8%, a wide range that reflects how much uncertainty the Iran war has injected into cost planning. Capacity is being held flat, with management adopting what it called a “downward bias” to protect margins. CEO Ed Bastian told CNBC that demand remains strong, with premium cabin bookings up double digits, but the gap between what the airline can earn and what fuel might cost is the widest it has been since the pandemic. Delta paid an adjusted average of $2.62 per gallon in the first quarter; at $4.30, every route becomes a different calculation.

Sensei’s Insight: Delta is the canary in the fuel-cost mine for every company that moves things, flies people, or ships goods. The $2.62 to $4.30 per gallon jump tells you exactly how fast the war premium flows through to corporate margins. If the ceasefire collapses and Brent stays near $100, that $2 billion headwind becomes the template for guidance cuts across the entire transportation sector this earnings season.

🏦 Private Credit’s Slow-Motion Bank Run Just Got Worse

The wave of investor redemptions sweeping the $1.8 trillion private credit industry intensified this week. Blue Owl Capital disclosed that investors in its $36 billion Credit Income Corp fund requested 21.9% of their shares back in the first quarter, up from 5.2% in the prior period. Its smaller Technology Income Corp fund saw an extraordinary 40.7% withdrawal request, up from 15.4%. Barings followed with an 11.3% redemption request on its $4.9 billion fund, capped at 5%. Across the industry, investors have sought to pull roughly $13 billion from over a dozen funds this quarter, but withdrawal caps mean more than $4.6 billion remains trapped behind gates (Bloomberg).

The pattern is accelerating, not stabilising. BlackRock, Morgan Stanley, Apollo, Ares, and Cliffwater have all restricted withdrawals in recent weeks. The FOMC minutes released yesterday flagged the stress directly, noting “notable increases in redemption requests at several private credit funds” and highlighting the sector’s heavy exposure to software loans vulnerable to artificial intelligence (AI) disruption. The feedback loop is straightforward: capping withdrawals makes it harder to attract new investors, which makes it harder to manage outflows, which increases pressure to sell illiquid loans at a discount. Software remains the single largest sector in most of these portfolios, representing 12.3% of Apollo’s fund alone. For retail investors who poured into these “semi-liquid” products during the boom years expecting bond-like stability with equity-like returns, the exits are getting smaller just as the queue is getting longer.

Sensei’s Insight: The Fed just told you this is a problem. When the FOMC minutes explicitly flag private credit stress, that is not background noise, it is the central bank watching for contagion. If loan defaults rise in a higher-rate environment while redemption queues stay in the double digits, the next step is forced asset sales at steep discounts, and that reprices every private credit vehicle in the market.

🌍 Trump Explores Punishing NATO Allies by Relocating US Troops

The Trump administration is weighing a plan to move American troops out of NATO member countries it considers unhelpful during the Iran war and station them in more supportive allies, the Wall Street Journal reported yesterday. The proposal emerged after a tense meeting between Trump and NATO Secretary General Mark Rutte at the White House, where Trump said “NATO wasn’t there when we needed them, and they won’t be there if we need them again.” Rutte acknowledged Trump was “clearly disappointed” but pushed back, saying the majority of European nations provided basing, logistics, and overflight support for the campaign. White House Press Secretary Karoline Leavitt said allies had “turned their backs on the American people” (Wall Street Journal).

The plan would fall short of a full NATO withdrawal, which would require congressional approval, but the signal to European defence budgets is unmistakable. Secretary of State Marco Rubio said the US would “reexamine the value of NATO for Washington” once the war ends. Trump also revived his Greenland threat in a post after the meeting. For markets, the relevance is in the defence spending acceleration: NATO’s spending floor is rising from 2% of gross domestic product (GDP) to 5% by 2035, and every hostile signal from Trump pushes European governments to accelerate procurement timelines. European defence stocks have already been the standout sector of 2026, and this dynamic has further to run.

Sensei’s Insight: Trump cannot legally leave NATO without Congress, and he knows it. The troop relocation plan is the lower-cost alternative: punish specific countries while keeping the alliance technically intact. The investable signal is the same either way. European governments are now planning as if America will not show up, and defence budgets from Berlin to Warsaw are being rewritten accordingly.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

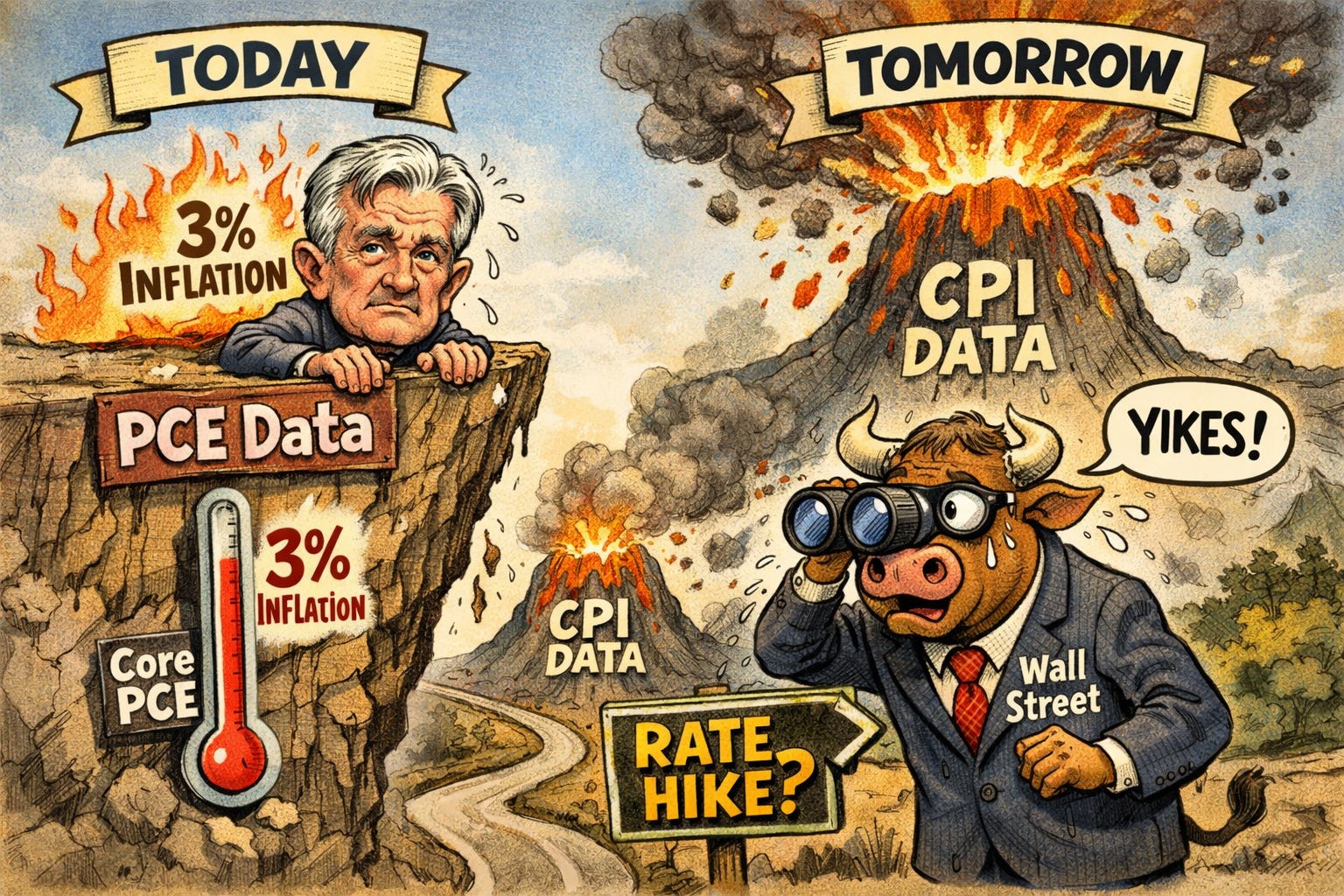

🔍Deep Dive: PCE inflation: the pre-war baseline

The Bureau of Economic Analysis (BEA) releases February Personal Consumption Expenditures (PCE) data at 8:30 AM ET today. This is the Federal Reserve’s preferred inflation gauge, and it is the number that drives interest rate decisions more than any other.

There are two inflation stories playing out right now, and today’s release helps answer one of them. The first story is the Iran war and oil prices. Everyone expects inflation to spike because of that, and it will, but it will show up in tomorrow’s Consumer Price Index (CPI) data, not today. The second story is the one that arguably matters more: even before the war started, was underlying inflation actually coming down, or was it getting worse? Today’s PCE covers February, which means it captures almost none of the energy shock. What it does capture is the state of the economy’s price pressures before the war distorted everything. That is what makes this release so important. If inflation was already running too hot before the oil shock, the Fed has a much bigger problem than just expensive gasoline.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.