Morning Forecast: Thursday 9 July

SK Hynix lands the second-biggest US listing ever as war fears cool and oil slips back.

👀 Today’s Stories at a Glance

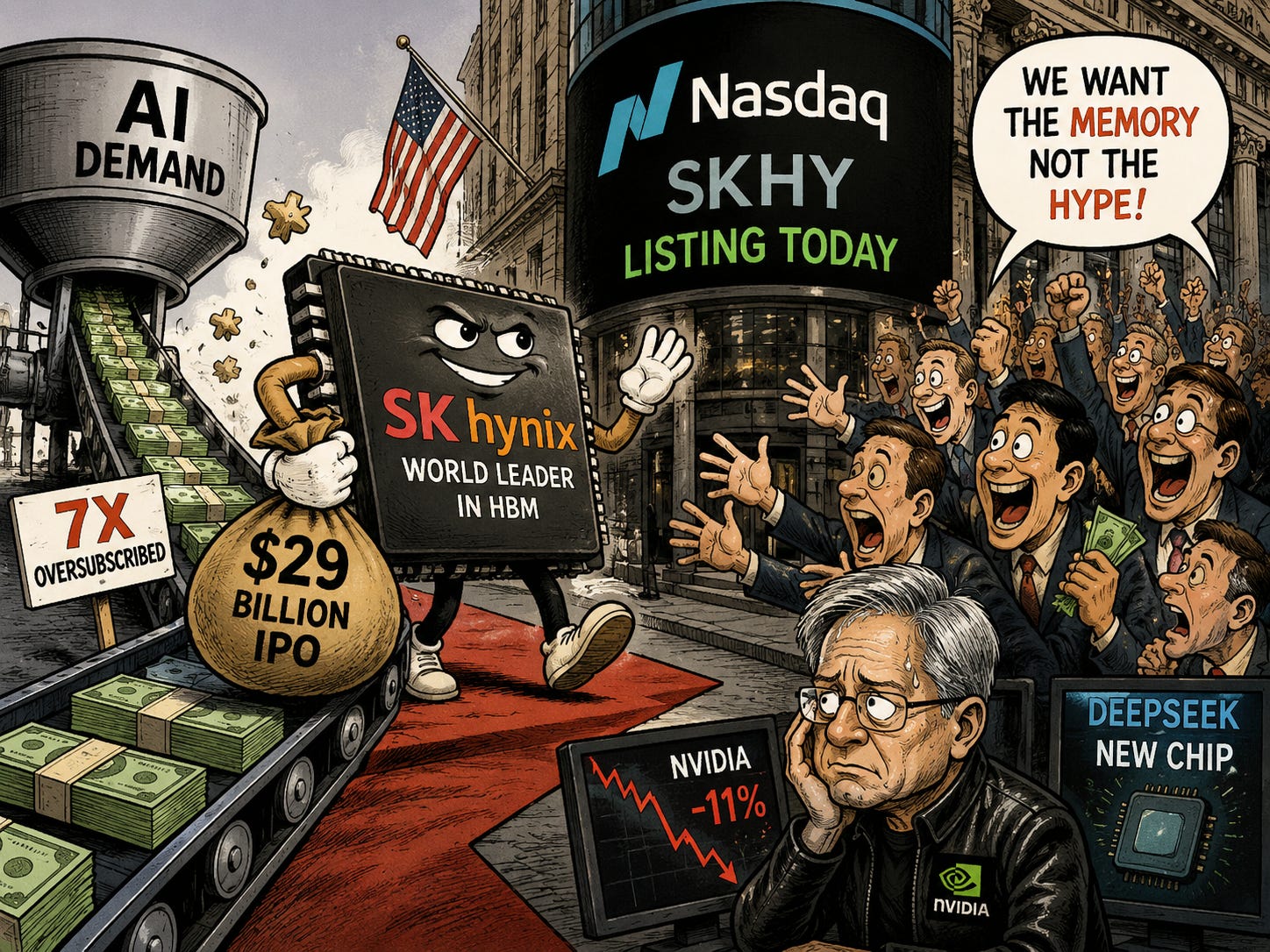

💾 SK Hynix lands mega listing: The memory maker’s roughly $29bn US debut is the second-biggest ever, with demand running near seven times the shares.

⚔️ Iran fears cool, oil slips: Trump said he expects no full war and oil to fall, steadying markets after yesterday’s Middle East selloff.

🏛️ Fed minutes lean hawkish: A few officials wanted a June hike, and inflation now worries policymakers more than the softening jobs market.

🥤 PepsiCo opens earnings season: Sales beat at $24bn as strong overseas demand offset weak North American volumes, and the guidance held.

₿ Bitcoin’s real story is the exodus: US spot ETFs have bled cash for eight straight weeks, the longest run ever, as the price drifts.

✈️ Delta reports before the open tomorrow: Wall Street sees profit down sharply on fuel costs, even as summer travel demand runs hot.

📊 Jobless claims in focus: The weekly count is due at lunchtime, the freshest labour read after last week’s soft payrolls, seen near 218,000.

🥇 Gold slides toward $4,060: The metal fell as hawkish minutes lifted the dollar and yields, capping haven demand despite the Iran tension.

🔍 Deep Dive: Nvidia now trades cheaper than the average S&P 500 stock, and what that rare de-rating says about the AI trade.

📈 Chart of the Day: Nvidia has reclaimed $200, and I break down the trendline, the key levels, and what I’m watching next.

🧠 One Big Thing

The market changed its whole mind in under a day, and that is the signal. Yesterday an Iran shock sent oil toward $80 and knocked the Dow almost 600 points, with gold and bonds failing as havens. This morning, after Trump said he did not expect a full war and predicted oil would fall, futures turned green and the talk moved straight back to AI and the SK Hynix debut. A crowd that can swing from war-fear to chip-greed this fast is trading headlines, not fundamentals, so positioning is thin and reactive. Watch whether the risk-on turn survives contact with the Fed minutes and today’s claims.

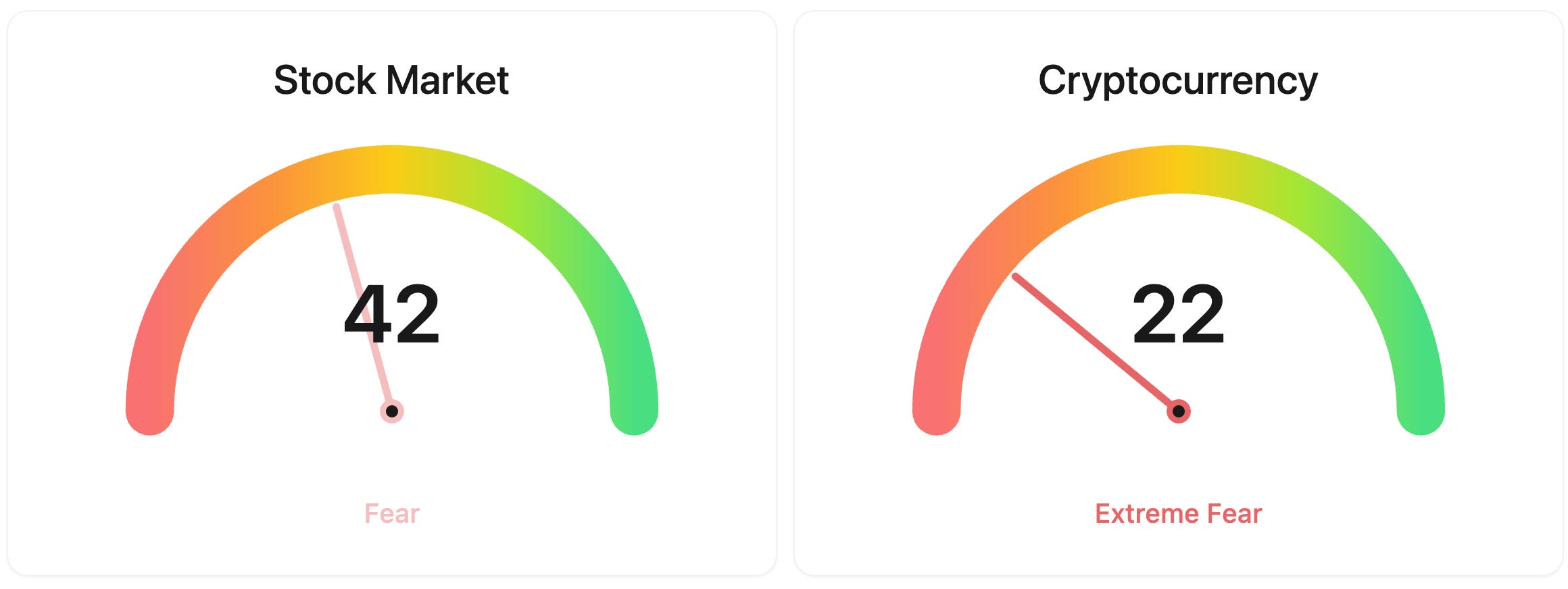

⚖️ Fear & Greed

📉 The Number That Matters

$29 billion

SK Hynix is raising about $29 billion in its US listing, the second-biggest first-time share sale on record after SpaceX, with orders running near seven times the stock available.

⚔️ Winners vs Losers

Winners

AP 0.00%↑: Ampco-Pittsburgh Corporation jumped after reporting first-half 2026 customer orders of roughly $268 million, up 32% year over year, with tariff-driven demand lifting both its forged and cast products and its air and liquid processing segments.

ALNY 0.00%↑: Alnylam Pharmaceuticals rallied after rival Ionis reported that its eplontersen CARDIO-TTRansform trial failed in ATTR cardiomyopathy, removing a looming competitive threat to Alnylam’s approved heart drug Amvuttra.

BBIO 0.00%↑: BridgeBio Pharma climbed on the same Ionis trial failure, which clears a near-term competitor from the ATTR cardiomyopathy market where BridgeBio sells its approved therapy Attruby.

AOSL 0.00%↑: Alpha and Omega Semiconductor advanced alongside a broad rally in AI power and chip stocks, with no company-specific news behind the move.

CBRS 0.00%↑: Cerebras Systems rose after announcing a major expansion of its European infrastructure, with its first data center capacity on the continent set to come online by the end of 2026.

AMAT 0.00%↑: Applied Materials rose as chip-equipment stocks extended a rally fueled by surging AI memory demand and rising analyst targets ahead of TSMC and ASML earnings next week.

LRCX 0.00%↑: Lam Research Corporation advanced on the same wave of chip-equipment strength, supported by expectations for record wafer fabrication equipment spending tied to the AI buildout.

Losers

AFJK 0.00%↑: Aimei Health Technology tumbled after terminating its long-pending merger agreement with United Hydrogen Group, leaving the blank-check company once again searching for a deal.

IONS 0.00%↑: Ionis Pharmaceuticals plunged after its eplontersen CARDIO-TTRansform Phase 3 trial failed in ATTR cardiomyopathy, wiping out a cornerstone of the company’s 2026 growth outlook and its main opportunity to expand the drug beyond its existing approval.

NOAH 0.00%↑: Noah Holdings fell as shares traded ex-dividend on the record date for its combined final and special dividend of about $1.38 per share, a mechanical drop rather than a reaction to news.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $62,739 (▲ 0.79%)

Ethereum (ETH): $1,746 (▲ 0.23%)

XRP: $1.09 (▲ 0.07%)

Equity Indices (Futures):

S&P 500: 7,538 (▲ 0.12%)

NASDAQ 100: 29,619 (▲ 0.51%)

FTSE 100: 10,401 (▼ -0.84%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.58% (▲ 0.04%)

Oil (WTI): $74 (▼ -1.03%)

Gold: $4,104 (▲ 0.62%)

Silver: $58.91 (▲ 1.16%)

Data as of: UK: 12:13 BST / US: 07:13 EDT / Asia (Tokyo): 20:13 JST

✅ 5 Things to Know

💾 SK Hynix Brings a $29 Billion Memory Bet to Wall Street

SK Hynix is pricing its US listing this week, a sale of about $29 billion that is set to begin trading on Nasdaq under the ticker SKHY and stands as the second-biggest first-time share sale on record, behind only SpaceX’s $85.7 billion float last month. The offer is 177.9 million American depositary shares, each representing a tenth of a Korean share, and demand is reported to be running at roughly seven times the stock on offer. The company is the world’s leading maker of high-bandwidth memory, the specialised chips that sit beside Nvidia’s processors in AI servers, and it holds about 56.4% of that market. Its Korea-listed stock has climbed 770% over the past year even after a 20% pullback from its June peak (Yahoo Finance).

So is this an IPO, and can you actually buy it? Not in the usual sense. SK Hynix is already a public company in South Korea; what is new is the US listing, where it sells American depositary shares, receipts that let US investors own a slice of a foreign company and trade it on Nasdaq in dollars like any other stock. Pricing runs this week and trading is expected to begin tomorrow under the ticker SKHY, so from then anyone with an ordinary brokerage account can buy it. Because orders are running near seven times the stock available, demand far outstrips supply, which often produces a jump on the first day but also means smaller investors rarely get stock at the set offer price and usually buy once it opens instead, wherever that turns out to be.

The debut matters far beyond one stock because it is a clean read on whether investors still believe the AI build-out has room to run. It arrives in a jittery week, with DeepSeek unveiling its own chip and Nvidia sliding to its cheapest valuation since before the boom, so a heavily oversubscribed sale would say big money still wants exposure to the memory bottleneck rather than the crowded compute names. History urges some caution: marquee listings often price near a peak in enthusiasm, and SpaceX itself has drifted back toward its float since joining the Nasdaq-100. Watch where the shares open against the offer and how the other chip names trade around it (Bloomberg).

Sensei’s Insight: Seven times covered for a memory maker tells you the AI trade is rotating, not dying. The money is leaving the priciest compute names and paying up for the scarce input instead. A strong open would say the theme still has believers with cash.

⚔️ Iran Fears Cool, Oil Slips and Stocks Steady

The panic that gripped markets yesterday eased overnight after Trump softened his tone on Iran. Speaking in Ankara, he said he did not believe the two sides would return to full-scale war and predicted oil would fall as tankers keep leaving the Strait of Hormuz, adding that the flare would “end very quickly.” That reversed some of the fear that had driven a hard risk-off session, when the Dow dropped 576.76 points, or 1.09%, to 52,348.39 and Brent jumped about 5% to settle near $78 after briefly topping $80. This morning US futures pointed higher, with the Nasdaq 100 up about 0.5%, and WTI, which had closed at $73.52, pared its earlier gain (Yahoo Finance).

For retail investors the lesson is how quickly a geopolitical spike can unwind when the words change. The strait still carries about a fifth of the world’s crude, so any fresh strike on shipping would send oil straight back up, and a sustained move higher would land on US inflation data due next week. For now the market is treating the episode as contained rather than the start of a wider war, which is why equities and oil both stepped back from their extremes. Watch tanker traffic through Hormuz and whether Tehran answers the latest US strikes, the two triggers that could reprice the calm (CNBC).

Sensei’s Insight: One press conference reversed a war scare, which tells you how much of yesterday’s move was fear rather than fact. The oil market is still one headline from another spike, so the calm is real but fragile. The tankers, not the rhetoric, are the thing to watch.

🏛️ The Fed Minutes Show a Committee Itching to Tighten

The record of the Fed’s June meeting, the first under Chair Kevin Warsh, showed a central bank leaning toward higher rates even as it held steady at 3.50% to 3.75%. Only a few officials actively made the case for a hike in the room, fewer than the nine of nineteen who pencilled at least one increase into their projections, a sign the immediate push to move was narrower than the dot plot had implied. What united the committee was the balance of risk: officials judged that the danger of inflation staying high now outweighs the danger of the jobs market weakening, a clear shift in emphasis. Warsh withheld his own rate forecast and trimmed the statement to about 130 words, dropping the easing bias that had survived earlier meetings (Bloomberg).

The timing complicates it, and it cuts both ways. These minutes were written before last week’s soft payrolls report of 57,000, so they may read more hawkish than the committee now feels, yet this week’s oil spike pushes inflation risk the other way. Markets took the message and ran with it: the dollar and Treasury yields rose, with the 10-year at a two-week high, and traders still put about a 76% chance on no change at the next meeting while pricing roughly a 40% chance of a hike by December. The next test is inflation data on 14 July, then the decision on 28 to 29 July. Watch the 2-year yield for the cleanest read on hike odds (CNBC).

Sensei’s Insight: My read is no cuts and no hikes for the rest of the year, and it turns on oil. Below $75 a barrel the hawks lose their best argument and the doves have nothing weak enough to cut into. Brent back above $85 is what revives the hike talk.

🥤 PepsiCo Opens Earnings Season With a Mixed Quarter

PepsiCo kicked off the second-quarter reporting season before the open with a split result. Revenue rose 6.4% to $24.18 billion, ahead of the roughly $23.97 billion Wall Street expected, helped by strong demand for its snacks and drinks overseas. Adjusted earnings came in at $2.20 a share, a shade under the $2.21 consensus, as its North American food and beverage arms stayed soft. Globally, food volumes rose 3% and beverage volumes 2%, but in North America food volume was flat and beverage volume fell 4%, a sign that budget-conscious US shoppers are pulling back. The company held its full-year forecast unchanged (CNBC).

The read matters because PepsiCo is an early window on the US consumer, and the message is one of resilience abroad masking strain at home. Snack and drink giants have leaned on price rises for two years, and flat-to-falling North American volumes suggest that lever is close to spent as households trade down. The stock had lagged into the print, up about 8% over the year against the S&P 500’s 22%, so the low bar helps. The heavier tests come next, with Delta tomorrow and the big banks from 14 July. Watch whether other consumer names echo the same soft US demand (Yahoo Finance).

Sensei’s Insight: Overseas strength is doing the heavy lifting while the American shopper quietly pulls back, and a 4% drop in US drink volumes is the number to sit with. Two years of price hikes have finally met their limit. Keeping the full-year forecast unchanged says management still thinks the wider business holds.

₿ The Bigger Bitcoin Story Is the ETF Exodus

Bitcoin hovered around $62,700, with Ether near $1,750, but the number that actually matters sits underneath the price. US spot Bitcoin ETFs have now bled money for eight straight weeks, the longest outflow streak since the funds launched in early 2024, with more than $8 billion pulled over the run and roughly $6 billion of that in the past month alone. The daily candles are being shoved around by Iran headlines and the hawkish Fed minutes, but the steady withdrawal by big institutional holders is the structural story the price noise keeps hiding (CoinDesk).

For retail investors the point is what those flows represent: the ETFs were sold as the bridge that would bring pension funds and wealth managers into crypto, and for two months that bridge has carried traffic the other way. The next real test is not a headline but a calendar. Washington faces a hard deadline of 18 July for six agencies to finalise the first federal rules for dollar-backed stablecoins under the GENIUS Act, and the day before that, lawmakers hold a public hearing on the wider CLARITY Act, the bill that would split crypto oversight between the securities regulator and the commodities regulator. The stablecoin rules are the concrete catalyst; the hearing is a step, not a vote, since that bill still faces a long path through the Senate. Until the flows turn, rallies keep running into sellers. Watch whether the outflow streak finally breaks around that mid-July window (Yahoo Finance).

Sensei’s Insight: The price is the sideshow. Eight straight weeks of ETF outflows, the longest run on record, says institutions have been quietly heading for the exit while retail fixates on the daily move. The mid-July stablecoin and market-structure deadlines are the first real chance to change that.

Stories You Might Have Missed

✈️ Delta Kicks Off Airline Earnings Tomorrow

Delta Air Lines reports second-quarter results before the open tomorrow, the traditional curtain-raiser for the airline season, and expectations have fallen sharply. Analysts now see earnings of about $1.48 a share on revenue near $18.78 billion, with the profit estimate cut roughly 26% over the past three months as higher fuel costs bite, driven partly by this year’s oil swings. The counterweight is demand: Delta has run at record load factors through the summer and guided to strong revenue growth, so the report is a clean test of whether robust travel bookings can outrun the fuel bill. The stock sits near its highs into the print, leaving little room for a miss (Yahoo Finance).

📊 Jobless Claims Give the Freshest Labour Read

Weekly jobless claims land at 1:30pm BST, the first look at the labour market since last week’s soft payrolls report and the day after the Fed’s hawkish minutes. Economists expect about 218,000 new filings, barely changed from 215,000 the week before, with continuing claims seen near 1.82 million. Claims have stayed historically low even as monthly hiring has cooled, which makes them the cleanest weekly check on whether the slowdown in jobs is turning into actual layoffs. A jump toward 250,000 would sharpen the slowdown story and complicate the Fed’s inflation focus, while another low print would say firms are still holding on to staff. Watch the four-week average, which smooths the weekly noise (Yahoo Finance).

🥇 Gold Slides Toward $4,060 as the Dollar Firms

Gold eased toward $4,060 an ounce, near a one-week low, as the hawkish Fed minutes lifted the dollar and pushed Treasury yields to a two-week high, both of which weigh on a metal that pays no yield. The pressure came despite the Iran tensions that would normally send buyers into gold, a sign that the rates story is winning the tug-of-war for now. As long as the Fed keeps a hike on the table, the dollar and yields stay firm and gold’s upside is capped, though a hot inflation print on 14 July or a fresh Middle East shock could quickly flip the balance. The metal remains well below its January record (Reuters).

🔍 Deep Dive: Nvidia Is Now Cheaper Than the Average S&P 500 Stock. What Is Going On?

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.