Morning Forecast: Tuesday 12 May

Today's inflation number is Powell's last, and markets have already given up on rate cuts in 2026.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🛢️ Oil Buffer Nears Operational Stress: JPMorgan warns global crude inventories could hit the floor by early June as Iran truce collapses.

🇨🇳 Trump-Xi Summit Opens Tomorrow: Two-day state visit covers rare earths, chip licensing, Boeing orders, and the Iran ceasefire.

🚨 Burry’s $1.1B Bubble Bet: Scion holds Nvidia and Palantir puts at roughly 80% of fund, with strikes expiring through December 2027.

⚖️ Meta Faces $7B Scam-Ad Suit: Santa Clara County alleges Meta earned $7 billion annually while throttling fraud controls to protect revenue.

🏠 Spring Housing Recovery Stalls: April sales rose just 0.2% as mortgage rates climbed back to 6.37% on the oil shock.

🇨🇳 China Factory Prices Break Deflation: Producer Price Index rose 2.8% in April, the strongest reading since July 2022.

📈 Lumentum Joins Nasdaq-100 After Beat: Optical-components maker rose 16% on Q3 revenue of $808 million, up 90% year-over-year.

⛏️ McEwen Lines Up $2.4B Copper Loan: Subsidiary mandates lender for Los Azules in Argentina, one of the largest undeveloped copper deposits.

🔍 Powell’s Last Inflation Print Today: Consumer Price Index drops two days before Kevin Warsh takes over the Federal Reserve chair.

🧠 One Big Thing

The single most important sentence in today's edition is JPMorgan's call that global crude inventories approach operational stress by early June. That is not a forecast; it describes a physical floor below which pipelines and terminals stop functioning. Once that floor binds, the marginal balancer is demand destruction, not price. Demand destruction may show up as Asian fuel rationing, emerging market sovereign stress, and producer-price contagion of the kind China's 2.8% April print already telegraphs. The trade rotates from long oil to long the spread between economies with strategic-reserve depth and those without.

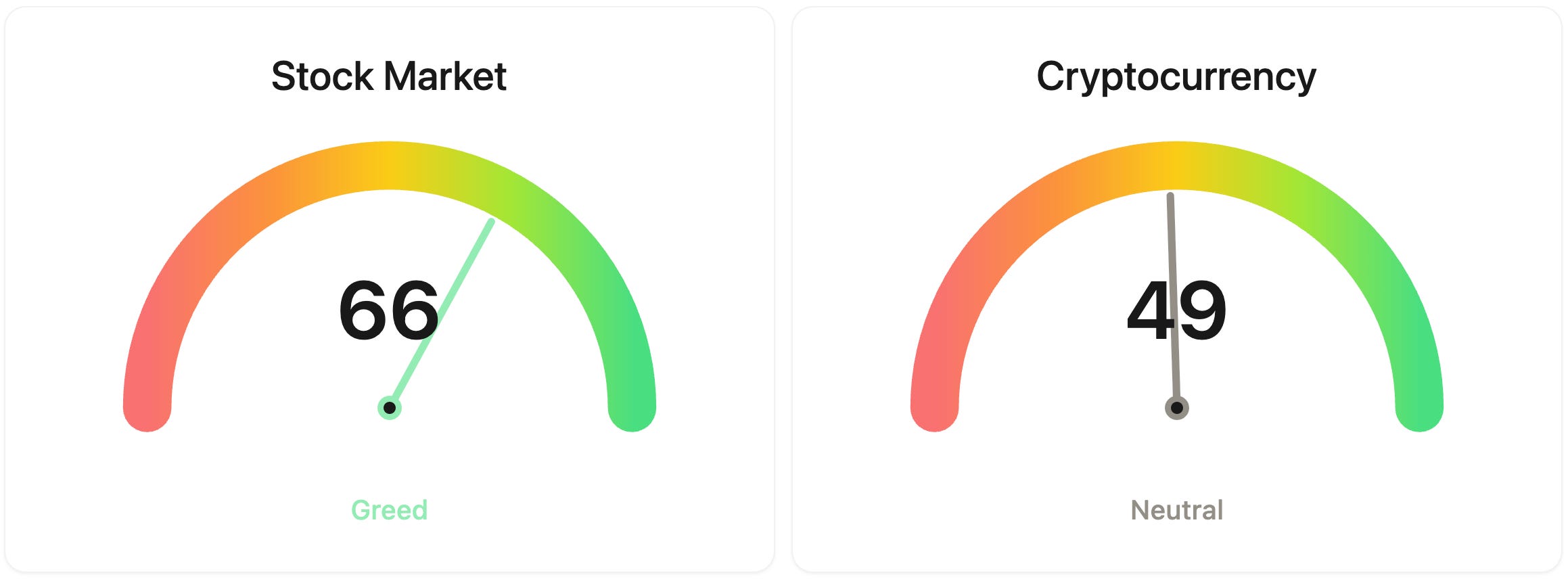

⚖️ Fear & Greed

📉 The Number That Matters

ZERO CUTS

Futures markets now price zero Federal Reserve cuts in 2026, a complete reversal from January when at least one quarter-point cut was on the table. Zero cuts shifts the equity bull case from earnings plus rate relief to earnings alone.

⚔️ Winners vs Losers

Winners

QUBT 0.00%↑ 24.17% Quantum Computing Inc. surged after reporting Q1 2026 revenue of $3.7 million, a sharp jump driven by contributions from its LSI and NuCrypt acquisitions, with the company also beating loss-per-share estimates and outlining Fab 2 planning.

PACS 0.00%↑ 22.26% PACS Group jumped after reporting Q1 net income up 184% year over year, raising its 2026 adjusted EBITDA guidance, and authorizing a new $250 million share repurchase program.

TE 0.00%↑ 17.38% T1 Energy rallied after reporting Q1 2026 revenue of $177.6 million, blowing past the $95.5 million consensus estimate, along with record quarterly net income from continuing operations of $3.9 million and record adjusted EBITDA of $9.1 million.

Losers

MVST 0.00%↑: Microvast Holdings collapsed after Q1 revenue fell 48% to $60.6 million, missing the $99 million estimate, and the company flagged substantial doubt about its ability to continue as a going concern citing geopolitical headwinds and capital repatriation constraints from China.

GTM 0.00%↑: ZoomInfo Technologies tumbled after slashing full-year 2026 revenue guidance to roughly $1.20 billion from $1.26 billion, citing AI-related buyer hesitation, and announcing a 20% workforce reduction along with the closure of its Israeli offices.

PSIX 0.00%↑: Power Solutions International plunged after Q1 adjusted EPS of $0.36 came in less than half the $0.74 consensus and revenue of $128.6 million missed by roughly $32 million, with management guiding Q2 sales to remain soft on weaker oil and gas demand and elevated ramp-up costs in Wisconsin.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $80,645 (▼ -1.35%)

Ethereum (ETH): $2,286 (▼ -2.33%)

XRP: $1.45 (▼ -1.95%)

Equity Indices (Futures):

S&P 500: $7,387 (▼ -0.31%)

NASDAQ 100: $29,201 (▼ -0.76%)

FTSE 100: £10,233 (▼ -0.06%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.43% (▲ 0.34%)

Oil (WTI): $102 (▲ 3.54%)

Gold: $4,694 (▼ -0.83%)

Silver: $83.62 (▼ -2.79%)

Data as of: UK (BST) 12:00 PM / US (EDT): 7:00 AM / Asia (Tokyo): 8:00 PM

✅ 5 Things to Know

🛢️ Iran Truce on “Life Support” as Oil Buffer Empties

The negotiation that’s been pinning oil below $100 just broke. Trump told reporters in the Oval Office yesterday that the US-Iran ceasefire is on “massive life support” with “a 1% chance of living” after rejecting Iran’s latest counter-offer through Pakistani mediators. He also accused Tehran of reneging on a verbal agreement to let US teams extract enriched uranium from the bombed nuclear sites, and warned that any restart of Project Freedom, the Navy’s commercial-shipping escort through Hormuz, would be “much more severe.” WTI rose 3.9% to $99.18 and Brent gained 3.5% to $104.83. Saudi Aramco CEO Amin Nasser told analysts normalization could now slip into 2027. (CNBC)

The harder news arrived from JPMorgan. The bank told clients global crude inventories are on track to fall below 2022 levels and approach “operational stress” by early June, the term for the floor where pipelines and terminals physically stop functioning. That buffer is the only reason oil sits near $100 rather than $200, with record US Strategic Petroleum Reserve drawdowns, de-sanctioned Russian and Iranian flows, and roughly 4.3 million barrels a day of demand destruction filling the gap left by 14 million barrels of Persian Gulf supply offline. Asia is closest to the edge: Pakistan has about 20 days of refined-product reserves, and Japan and India sit at 10-year seasonal lows. (Bloomberg)

The two threads tie together at tomorrow’s Trump-Xi summit, where China’s leverage just grew. Trump told Fox News that Iran said only the US or China could retrieve enriched uranium from the bombed sites, a striking admission that Beijing now has a seat at the diplomatic table whether Washington likes it or not. The US Navy also disclosed an Ohio-class ballistic-missile submarine arrived in Gibraltar on Sunday, a rare public nuclear-posture signal days before the visit.

Sensei’s Insight: Inventory math is now the binding constraint, not diplomacy. Once OECD stocks hit JPMorgan’s operational floor in June, the only marginal balancer left is demand destruction. That means an emerging-market fuel crisis, not a US gasoline crisis, is the real tail risk for portfolios to position around.

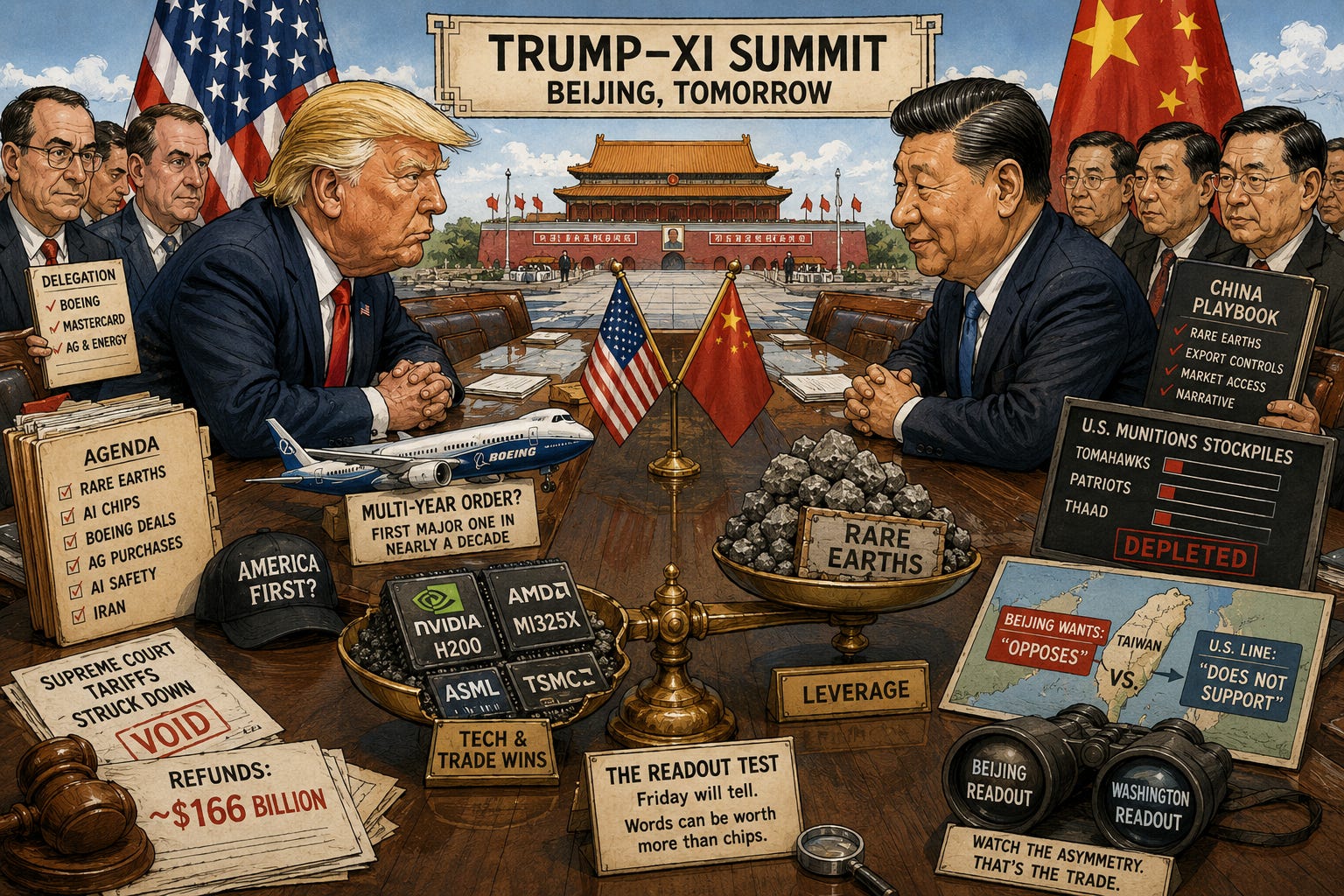

🇨🇳 Trump-Xi Summit Tomorrow Covers Iran, AI Chips, Rare Earths

China’s Foreign Ministry formally confirmed yesterday that Trump’s two-day state visit begins tomorrow, his first to Beijing since November 2017 and the first US presidential state visit in roughly nine years. The agenda is unusually crowded: extending the rare-earth export-control truce that runs out in late October, licensing Nvidia’s H200 and AMD’s MI325X chips for the China market, fresh Boeing and agricultural purchase commitments, a first-ever Trump-Xi conversation on AI safety, and Iran. The delegation reportedly includes Boeing and Mastercard CEOs. (CNBC)

Xi enters with the leverage. The Supreme Court struck down Trump’s emergency-powers tariffs in February, forcing the administration onto a 10% Section 122 global tariff valid only 150 days and triggering roughly $166 billion in projected refunds. China’s October rare-earth export controls drove the Geneva and Busan climbdowns last year, and Defense Secretary Pete Hegseth conceded in April that key US munitions stockpiles, including Tomahawks, Patriots, and THAAD interceptors, have been depleted by the Iran war. (Bloomberg)

For portfolios, the live trades cluster around three deliverables. A rare-earth truce extension and explicit H200 licensing would re-rate Nvidia, AMD, ASML, TSMC, and the EV battery supply chain (Nvidia took a $4.5 billion H20 write-down last quarter). A multi-year Boeing order, China’s first major one in nearly a decade, lifts BA and the aerospace tier. The destabilizing outcome flagged by analysts at CSIS and the German Marshall Fund is any softening of the standard US line from “does not support” Taiwan independence to “opposes,” which Beijing has been pushing hard.

Sensei’s Insight: Watch the two readouts side by side on Friday. If Beijing’s text runs harder on Taiwan than Washington’s, it means Trump traded language for the chip and rare-earth wins. That asymmetry is the real signal, not the choreography in the press conferences.

🚨 Burry Bets 80% of Fund on AI Bubble Echoing 2000

Michael Burry told subscribers on his Substack last Friday that the current AI rally “feels like the last months of the 1999-2000 bubble” and that roughly 80% of Scion Asset Management is now in put options on Nvidia and Palantir. Combined notional value: $1.1 billion. The specific positions, per follow-up reporting: 1 million Nvidia puts at a $110 strike expiring December 2027, plus stacked Palantir puts at $100 (December 2026) and $50 (June 2027). He’s also short the SOXX semiconductor ETF via January 2027 puts and holds QQQ puts. Bloomberg amplified the call yesterday. (Bloomberg)

The setup that prompted him is genuinely unusual. The Shiller cyclically adjusted P/E ratio hit 40.1 on Friday, near the dot-com peak; the Philadelphia Semiconductor Index is up around 65% year-to-date, with a 10% gain in the single week ending May 8; and Friday’s record S&P close at 7,398.93 coincided with the lowest University of Michigan consumer sentiment reading in the survey’s history. John Hussman and David Rosenberg have called the same setup a “great speculative bubble.” Morgan Stanley’s Mike Wilson sits on the other side at 7,800 for the S&P in twelve months. Burry’s Q1 13F filing is due Thursday. (CNBC)

Sensei’s Insight: Look at the strikes. Burry’s Nvidia puts don’t pay until well below the stock’s current trading level, and they expire in December 2027. He’s not calling a June top. He’s positioning for a multi-quarter re-rate that takes through 2026 earnings season. Anyone treating this as a crash call is reading the wrong tape.

⚖️ Meta Sued at Home Over $7B Scam Ad Business

Santa Clara County filed a civil enforcement lawsuit against Meta yesterday in the company’s own backyard, alleging it earned as much as $7 billion a year from “high-risk” scam ads on Facebook and Instagram while internally throttling fraud-reduction efforts that would have cost too much revenue. County Counsel Tony LoPresti filed on behalf of all California residents under the state’s False Advertising and Unfair Competition statutes, seeking restitution, civil penalties of up to $2,500 per violation, and injunctive relief. Outside counsel includes Bernstein Litowitz, the firm best known for securities-class-action work, on contingency. (Bloomberg)

The complaint draws heavily on internal Meta documents first surfaced by Reuters last November showing the company projected roughly $16 billion in scam-ad revenue in 2024 (about 10% of its ad business) and calculated that universal advertiser verification would cost $2 billion and dent revenue by 4.8%. The most striking new allegation is that Meta can “adjust the flood of scam ads it allows on its platforms in order to smooth its earnings or hit specific revenue targets.” META closed at $603.84 yesterday, down 1.3% on a day the S&P 500 set another record. (Fortune)

Sensei’s Insight: The “smooth earnings” line is the tell. That’s not consumer-protection language, that’s SEC-disclosure language. Pair it with Bernstein Litowitz as outside counsel and the contingency structure, and this case reads less like a False Advertising suit than a stalking horse for a securities action.

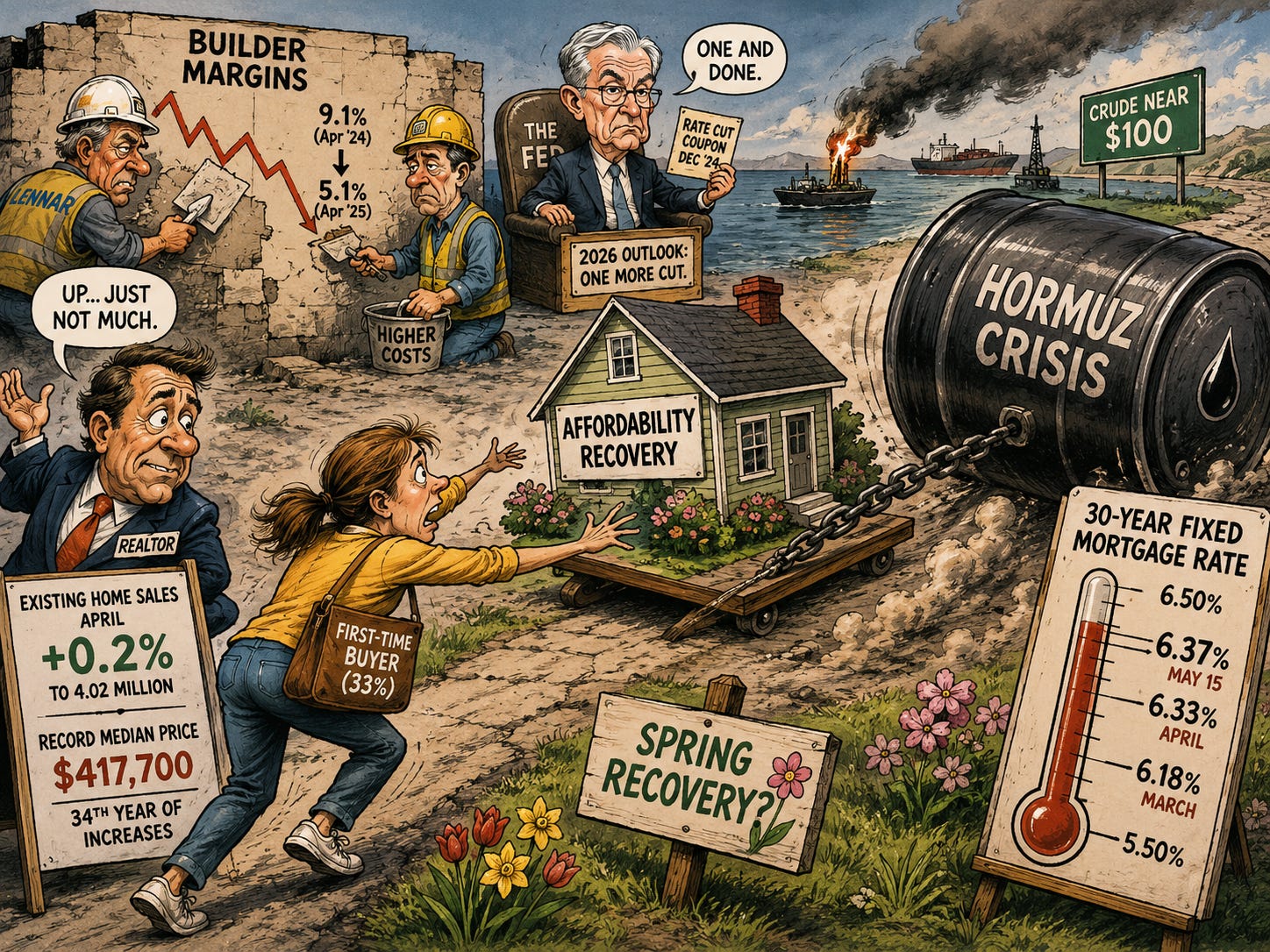

🏠 Home Sales Inch Up but Spring Recovery Loses Steam

Existing US home sales rose 0.2% in April to a 4.02 million annualized pace, missing the 4.05 million consensus but climbing off March’s nine-month low. The median sale price hit a record $417,700, the 34th consecutive year-over-year increase. First-time buyers held at 33% of transactions, well below the roughly 40% considered healthy, and days-on-market lengthened to 32 from 29 a year earlier. The Housing Affordability Index reached 110.6, its strongest reading in years. National Association of Realtors chief economist Lawrence Yun credited lower mortgage rates from a year ago and incomes outpacing price growth. (NAR)

The affordability tailwind is already reversing. Freddie Mac’s 30-year fixed rate climbed from 6.18% in March to 6.33% in April to 6.37% last Thursday, tracking long Treasury yields higher as the Iran war pushed crude back near $100 and revived inflation fears. The Fed delivered one December cut, and the FOMC has signaled only one more for 2026. Builder stocks have noticed: the SPDR S&P Homebuilders ETF closed Thursday at $102.66, down nearly 3% on the day, and Lennar’s last print showed margins compressed to 5.1% from 9.1% a year earlier. (Yahoo Finance)

Sensei’s Insight: April was supposed to be the spring affordability recovery, with mortgage rates falling and incomes finally beating prices. Then Hormuz closed. The same Iran story draining the oil buffer is now resetting the housing clock by another quarter, and the next builder margin print will show it.

Stories You Might Have Missed

🇨🇳 China April PPI Hits 45-Month High on Oil Shock

China’s April Producer Price Index rose 2.8% year-over-year, the highest reading since July 2022 and well above the Reuters poll of 1.6%, the National Bureau of Statistics reported yesterday. CPI also beat at +1.2% versus +0.9% expected. The drivers were unmistakably Iran-war energy costs: retail gasoline up 19.3% year-over-year, non-ferrous metals mining up 38.9%, oil and gas extraction up 28.6%. The print ends a 41-month deflation cycle and shifts the macro narrative from “Chinese deflation risk” to “imported inflation risk.” It also probably keeps the People’s Bank of China on hold through mid-2026, pulling away a stimulus tailwind that Chinese equity bulls had penciled in. (CNBC)

📈 Lumentum Surges 16% on Earnings Plus Nasdaq-100 Promotion

Lumentum Holdings (LITE) rose 16.4% yesterday to a record high after the optical-components maker posted Q3 revenue of $808.4 million, up 90% year-over-year, with non-GAAP EPS of $2.37 and Q4 guidance ($960 million to $1.01 billion) that brackets a billion-dollar quarter. Management said the company is still under-shipping demand by roughly 30% even after a 40% capacity expansion. The kicker arrived Friday, when Nasdaq announced LITE will join the Nasdaq-100 on May 18, replacing CoStar Group and forcing mechanical buying from the $600 billion-plus in QQQ-linked passive funds. The print is the cleanest read yet that the AI capex cycle is moving down the stack from GPUs into optical interconnect, supportive for Coherent, Fabrinet, and Broadcom. Caveat: LITE now trades at roughly 180 times trailing earnings. (Yahoo Finance)

⛏️ McEwen Copper Lines Up $2.4B Loan for Argentina Project

McEwen Copper, a subsidiary of Toronto-listed McEwen Inc. (MUX), has mandated a financial firm to manage the $2.4 billion debt portion of the $4 billion financing for its Los Azules copper project in San Juan province, Argentina, Reuters reported yesterday. Los Azules is one of the world’s 10 largest undeveloped copper deposits, with an after-tax net present value of $2.9 billion at $4.35 per pound (closer to $6.3 billion at current prices), 19.8% IRR, and first production targeted for 2030. The mandate signals Argentina’s RIGI investment regime under Milei is finally pulling project finance, and follows Friday’s news that Rio Tinto is weighing raising its 17.2% stake via Nuton. Copper futures sit at $6.35 per pound, up roughly 38% year-over-year on AI data-center, grid, and EV demand colliding with the Grasberg landslide and Chile’s first-quarter output drop. (Reuters via OneNewsPage)

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: April CPI cheat sheet: the print that defines Warsh’s first week

The Bureau of Labor Statistics releases the April Consumer Price Index at 8:30 AM ET today. After March’s headline jumped to 3.3% year over year, the largest single-month rise since 2022 (BLS), this print arrives in the middle of arguably the most important macro week of 2026: producer prices land tomorrow, the Trump-Xi summit is Thursday, and Friday is Jerome Powell’s final day as Fed chair before Kevin Warsh takes over (Roll Call).

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.