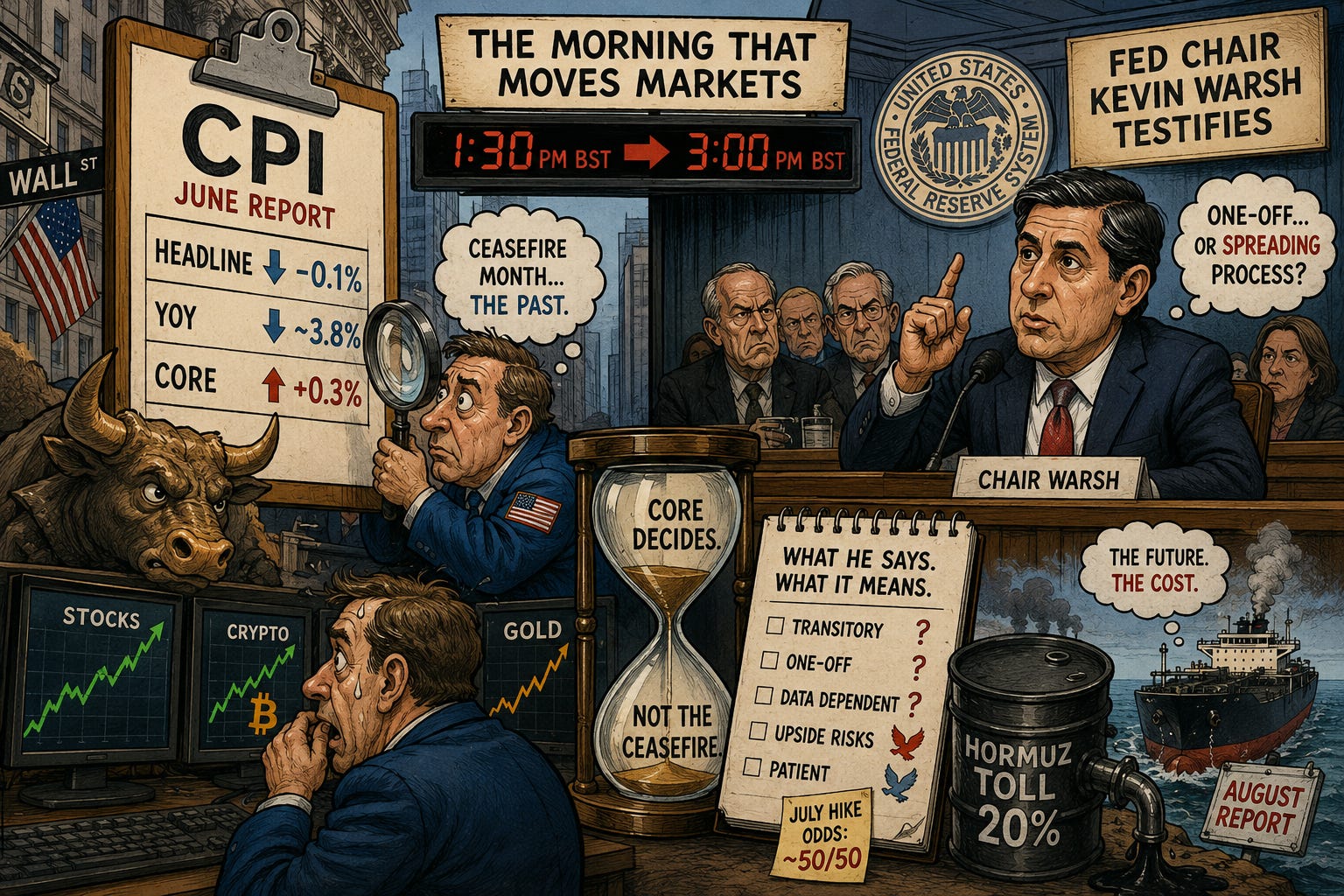

Morning Forecast: Tuesday 14 July

A 20% Hormuz toll, June CPI, and the new Fed chair’s first testimony all land today!

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🛢️ Hormuz toll ignites oil: Trump sets a 20% fee on all Strait cargo and blockades Iranian ports, lifting Brent past $86, a one-month high.

📊 CPI then the Fed chair: June inflation lands at 1:30, with Warsh’s first testimony 90 minutes later and a July hike near a coin flip.

🏦 Banks smash estimates: JPMorgan posts a record profit on a $6bn trading haul, with BofA and Wells Fargo also beating.

💾 SK Hynix keeps sliding: The memory giant gives back more of its record listing, down toward $152 from a $168 debut as valuations reset.

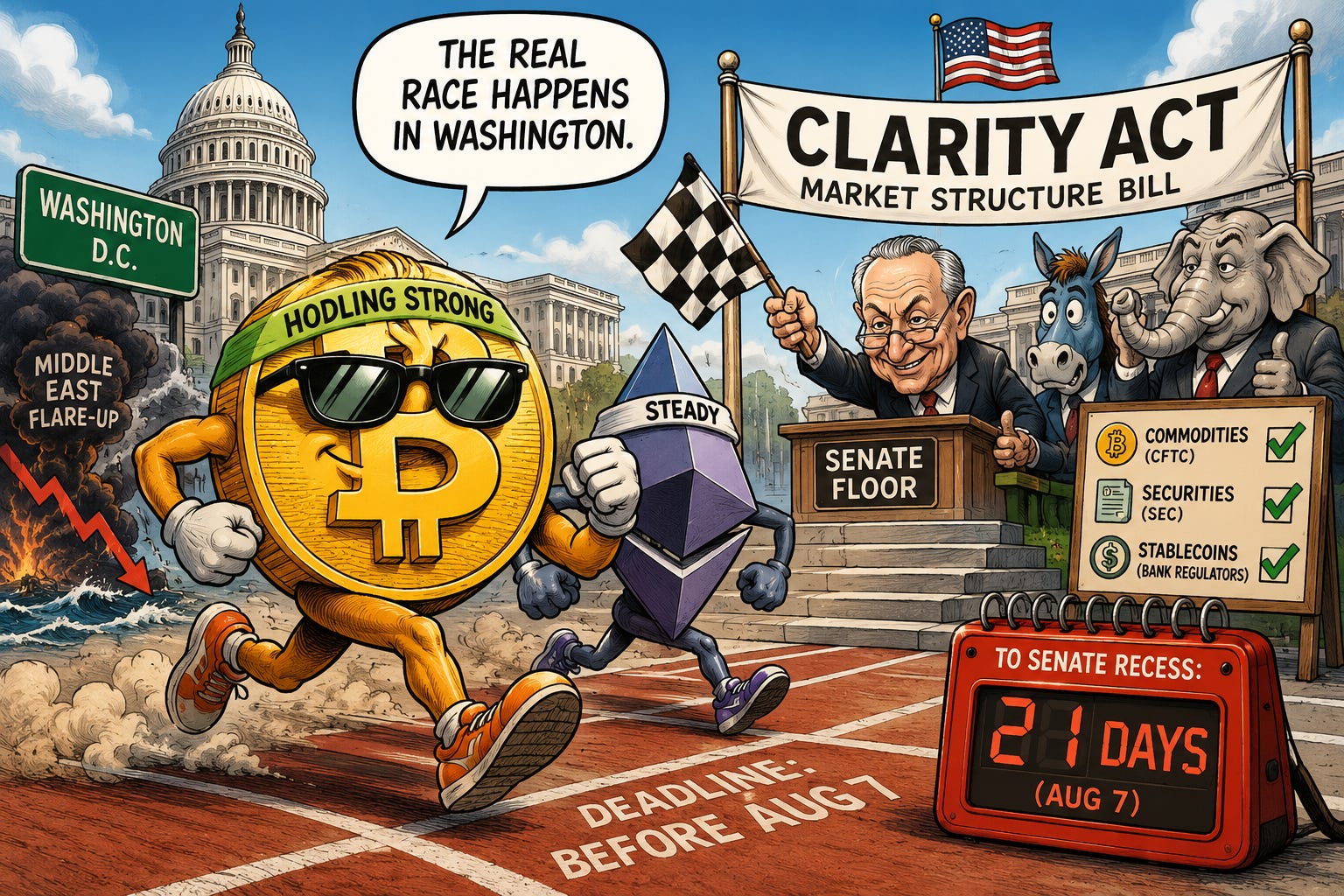

₿ Bitcoin waits on Washington: BTC holds near $63,000 as the CLARITY market-structure bill could reach the Senate floor within days.

🥇 Gold loses its haven bid: Bullion shed about 3% toward $4,000, its worst day in a month, as rate-hike fears outweighed the war premium.

🖥️ Chip earnings could steal focus: ASML reports tomorrow and TSMC soon after, a live read on AI-hardware demand after SK Hynix’s round trip.

🔍 Deep Dive: Two playbooks for the day, a full CPI Day guide and a Warsh Hearings guide, are below.

📈 Chart of the Day: Oil, and the price zones that decide whether a July rate hike stays on the table.

🧠 One Big Thing

For the first time this year, the biggest inflation print and the start of bank earnings arrive the same morning, with an oil shock layered on top. That is three separate reads on the same question landing within hours. CPI shows what prices did, the banks show what credit and the consumer are actually doing, and oil shows what is coming next. The tension is whether they agree. A firm CPI with cautious bank guidance whispers stagflation; a soft print with solid loan books lets the rally breathe. Watch whether the data and the boardroom tell the same story today.

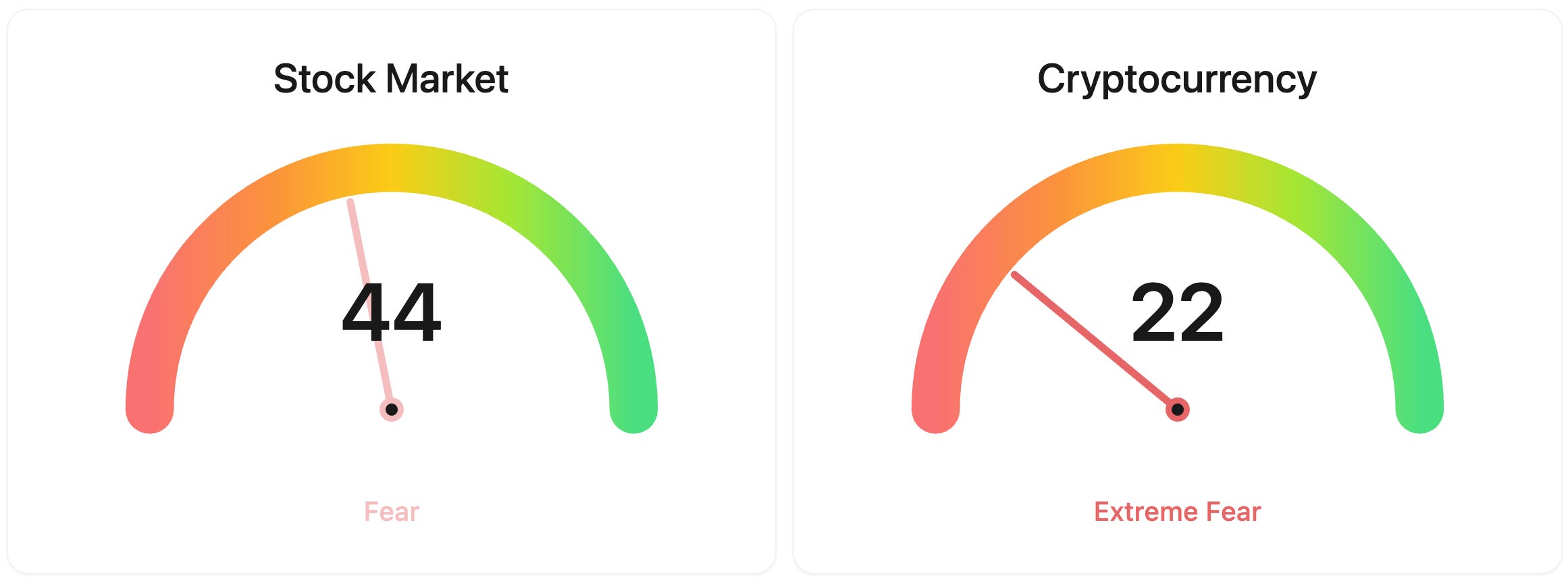

⚖️ Fear & Greed

📉 The Number That Matters

20%

The fee Trump set on all cargo crossing the Strait of Hormuz, the first time Washington has taxed the world’s most important oil chokepoint, a cost that builds into inflation through the summer.

⚔️ Winners vs Losers

Winners

TSEM 0.00%↑: Tower Semiconductor Ltd. surged after announcing a roughly $3 billion dual-track expansion of its 300mm silicon photonics, silicon germanium and advanced packaging capacity in Japan, backed by about $1 billion in grants from Japan’s METI, alongside raised 2028 targets.

Losers

EVO 0.00%↑: Evotec SE extended its slide after the drug discovery group slashed 2026 guidance late Monday, cutting revenue to 570 to 610 million euros from 700 to 780 million and swinging its adjusted EBITDA forecast to a loss of 70 to 105 million euros from a projected profit. The Frankfurt line fell around 30% to its lowest level in a decade.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $62,724 (▲ 0.69%)

Ethereum (ETH): $1,792 (▲ 0.93%)

XRP: $1.07 (▲ 0.17%)

Equity Indices (Futures):

S&P 500: 7,556 (▼ 0.09%)

NASDAQ 100: 29,589 (▲ 0.38%)

FTSE 100: 10,441 (▼ 0.50%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.62% (▼ 0.04%)

Oil (WTI): $81 (▲ 3.53%)

Gold: $4,018 (▲ 0.42%)

Silver: $57.87 (▲ 0.44%)

Data as of: UK: 11:45am BST / US: 6:45am EDT / Asia (Tokyo): 7:45pm JST

✅ 5 Things to Know

🛢️ Washington puts a toll on the Strait of Hormuz

President Trump has moved to reinstate a blockade of Iranian ports near the Strait of Hormuz and to charge a fee “at the rate of 20% on all cargo” crossing the waterway, with US Central Command saying the blockade takes effect at 4pm ET today. It is the first time Washington has taxed the world’s most important oil chokepoint, through which about a fifth of the world’s seaborne crude passes. Brent has surged past $86, its highest in a month and up nearly 13% over two sessions, after tanker traffic through the strait fell to roughly a third of normal, about 13 transits against a 33-a-day average (CNBC).

The move drove yesterday’s broad selloff, but the bigger point is structural: a standing 20% tax on a fifth of the world’s seaborne oil is a cost, not just a scare, and it feeds shipping, insurance, and fuel prices through the summer. It will not show up in today’s June inflation number, because June was the ceasefire month, so the effect builds into August and beyond. Citi warned the plan materially raises the risk of further escalation. For now the market is pricing disruption, not closure, so watch whether the 4pm ET deadline passes without incident and how Iran answers.

Sensei’s Insight: Every Hormuz flare-up this year has faded within days, and the market has learned to fade them too. The part I am not fading is the toll: a standing 20% tax on the world’s most important oil route is a structural cost, not a scare.

📊 CPI lands, then the new Fed chair testifies

June’s Consumer Price Index arrives at 1:30pm BST, the most watched inflation report of the year after an energy spike lifted May’s annual rate to 4.2%, a three-year high. Consensus sees headline prices slipping about 0.1% on the month, easing the annual rate toward 3.8% as June’s ceasefire-month petrol drop of roughly 10% washes through, while core, the Fed’s preferred gauge, is seen firm near a 0.3% monthly gain. Ninety minutes later, new Fed chair Kevin Warsh gives his first testimony to Congress, with a July rate hike now priced at roughly a coin flip, up from about a third a week ago (Yahoo Finance).

The catch is timing. June was the calm month, so today’s headline is a photograph of the ceasefire, and the fresh Hormuz toll will not land until the August report. That puts the weight on core, and it makes Warsh’s afternoon the real event, because the market wants to know whether he calls the oil shock a one-off or a spreading process. There is a lot to read across the two, so I have built a full playbook for each, both in today’s Deep Dive below. The CPI guide walks through what every headline-versus-core combination would do to stocks, crypto and gold, and the oil levels that keep a hike alive. The Warsh guide decodes the phrases that read as hawkish or patient, who he is, and where the sparks will fly. If you read two things before the open, read those. Watch core, and watch Warsh’s language around the word “transitory.”

Sensei’s Insight: The year’s oddity in one morning: the headline will flatter, the core decides, and core is the one line nobody can blame on the ceasefire ending. I am not trading the first candle; the toll and the testimony own the summer.

🏦 The banks post blowout profits, but Dimon warns

JPMorgan opened earnings season with the highest quarterly profit in its history, powered by a record $6.03 billion stock-trading haul that jumped 86% on the year and beat even the most bullish analyst estimate, lifting total trading revenue to an all-time high of $12.1 billion. A long-held Visa stake added $4.6 billion, investment-banking fees rose 30% to $3.28 billion as dealmaking thawed, and the bank raised its full-year net interest income outlook to about $105.5 billion. Even so, CEO Jamie Dimon struck a wary tone, warning that geopolitical tension, sticky inflation, and elevated asset prices are “shifting below the surface like tectonic plates” (Bloomberg).

The strength ran across the group. Bank of America’s traders set their own record, with equity-trading revenue up 70% to $3.6 billion and earnings of $1.21 a share topping the $1.12 expected, while its investment bank and a 68% jump in advisory fees rode the same dealmaking revival that SpaceX’s record June IPO helped ignite. Wells Fargo beat too, lifting net income 17% to $6.4 billion, or $2 a share against a $1.71 estimate, on stronger wealth-management and investment-banking fees. Volatile markets and a reawakening in deals, rather than plain old lending, did the heavy lifting (Bloomberg).

The reaction told the real story. Despite the records, JPMorgan shares slipped about 1.4% in early trading, because a volatility-fuelled trading boom is not the same as durable growth, and because the same morning’s rate-hike bets are lifting bond yields and setting a jumpy tone into the CPI print. The banks did confirm that the consumer is holding up and credit is calm, which steadies the question of how strong the economy really is. But Dimon’s tectonic-plates warning echoes the oil-and-inflation backdrop, and blockbuster profits were not enough to lift the wider market while yields climb.

Sensei’s Insight: When the banks print records and the stock still falls, the good news was already in the price and the worry is what comes next. Dimon just named it. I am watching credit costs and the yield move, not the size of the beats.

💾 SK Hynix hands back more of its record debut

SK Hynix’s US-listed shares slid toward $152, down from a $168 debut, extending a sharp reversal that has now unwound most of the pop from one of the year’s marquee listings. The stock sank more than 10% in Asian trade, with its Seoul-listed line weak alongside it, as investors wrestled with how to value the newly US-listed shares against the Korean stock and took profits after the debut spike. The memory maker led the semiconductor slide that dragged the Nasdaq down 1.55% yesterday (Yahoo Finance).

The listing itself raised $26.5 billion, the largest first-time share sale by a foreign company in US history, so the round trip in a matter of sessions is a real referendum on how much investors will pay for AI memory. SK Hynix supplies more than half the world’s high-bandwidth memory, the chips that feed AI accelerators, which ties its fate to the demand reads coming this week. ASML reports tomorrow and TSMC soon after, both treated across markets as live gauges of AI-hardware appetite. Watch memory and foundry names into those prints.

Sensei’s Insight: A debut that doubles then gives it all back in days tells you the float was priced for perfection, not that demand vanished. The clean read comes tomorrow: if ASML’s order book is strong, this was positioning, not a verdict on memory.

₿ Bitcoin steadies as its Washington moment nears

Bitcoin is holding near $63,000 after dipping below $62,000 over the weekend on the Middle East flare-up, with Ethereum steadier alongside it. The bigger story is in Washington: the CLARITY Act, the market-structure bill that would finally define which digital assets are securities and which are commodities, could reach the Senate floor as early as 17 July. The bill is running on a hard four-week runway before the Senate breaks for its summer recess on 7 August, and prediction markets put its chances of passing this year at roughly 60% to 70% (Yahoo Finance).

The bill would sort tokens into three buckets: commodities like Bitcoin overseen by the CFTC, fundraising tokens under the SEC, and payment stablecoins supervised by banking regulators, which would lift one of the largest regulatory overhangs on the sector. It is still snagged on ethics language and the split of authority between agencies, and a miss before the recess would push the catalyst out for months. A House field hearing in New York on 17 July is a talking shop rather than a vote, so watch the Senate floor calendar for the real signal.

Sensei’s Insight: Crypto is trading the calendar now, not the charts, and the four-week clock to recess is the whole game. A floor vote before 7 August is the catalyst the rally wants; a slip past it hands the summer back to the macro tape.

Stories You Might Have Missed

🥇 Gold loses its haven bid as rates fears bite

Gold shed about 3% yesterday, its biggest daily drop in more than a month, sliding toward $4,000 before steadying near $4,014 this morning. That is a striking move on a day oil climbed and the US tightened a blockade, the sort of backdrop that usually sends money into bullion. Instead, ramped-up expectations of higher interest rates and a firmer dollar did the opposite: higher rates dull the appeal of an asset that pays no yield, so investors chose Treasuries over the metal even as the war premium built. Gold now sits well below its January record near $5,595, and its direction from here leans on today’s CPI and Warsh’s tone (CNBC).

🖥️ Chip earnings this week could steal the show

The memory rout has raised the stakes for a run of chip results that markets treat as real-time reads on AI demand. ASML, which makes the machines that print the most advanced chips, reports tomorrow, with new bookings watched as a gauge of how much hardware the AI buildout still needs. TSMC, the foundry that manufactures the world’s leading silicon, follows soon after with its own capital-spending plans. After SK Hynix round-tripped its record debut in days, these prints offer the cleanest test yet of whether the AI-hardware trade is cooling or simply repricing. A strong order book would steady the semis; a soft one would deepen the doubt (CNBC).

🔍 Deep Dive

Two special playbooks for today’s double event, so you can read the inflation print and the new Fed chair like a pro.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.