Morning Forecast: Tuesday, 17 March

Diesel at $5, Five Credit Funds Frozen, and the Fed Can't Fix Either One.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

⛽ War Spirals as Inflation Bites: Diesel costs surge while Iran leadership falls, leaving the Fed stuck.

🚀 Nvidia Debuts Trillion Dollar Superchip: The new Vera Rubin platform targets massive orders by boosting performance.

⚖️ Judge Blocks RFK Vaccine Cuts: A Boston ruling restores childhood immunizations and reverses controversial policy changes.

🤖 Meta Cuts Staff for AI: Thousands lose jobs as the company shifts billions into massive infrastructure.

🇬🇧 Trump Slams UK War Stance: The President threatens trade consequences after Starmer refuses military support.

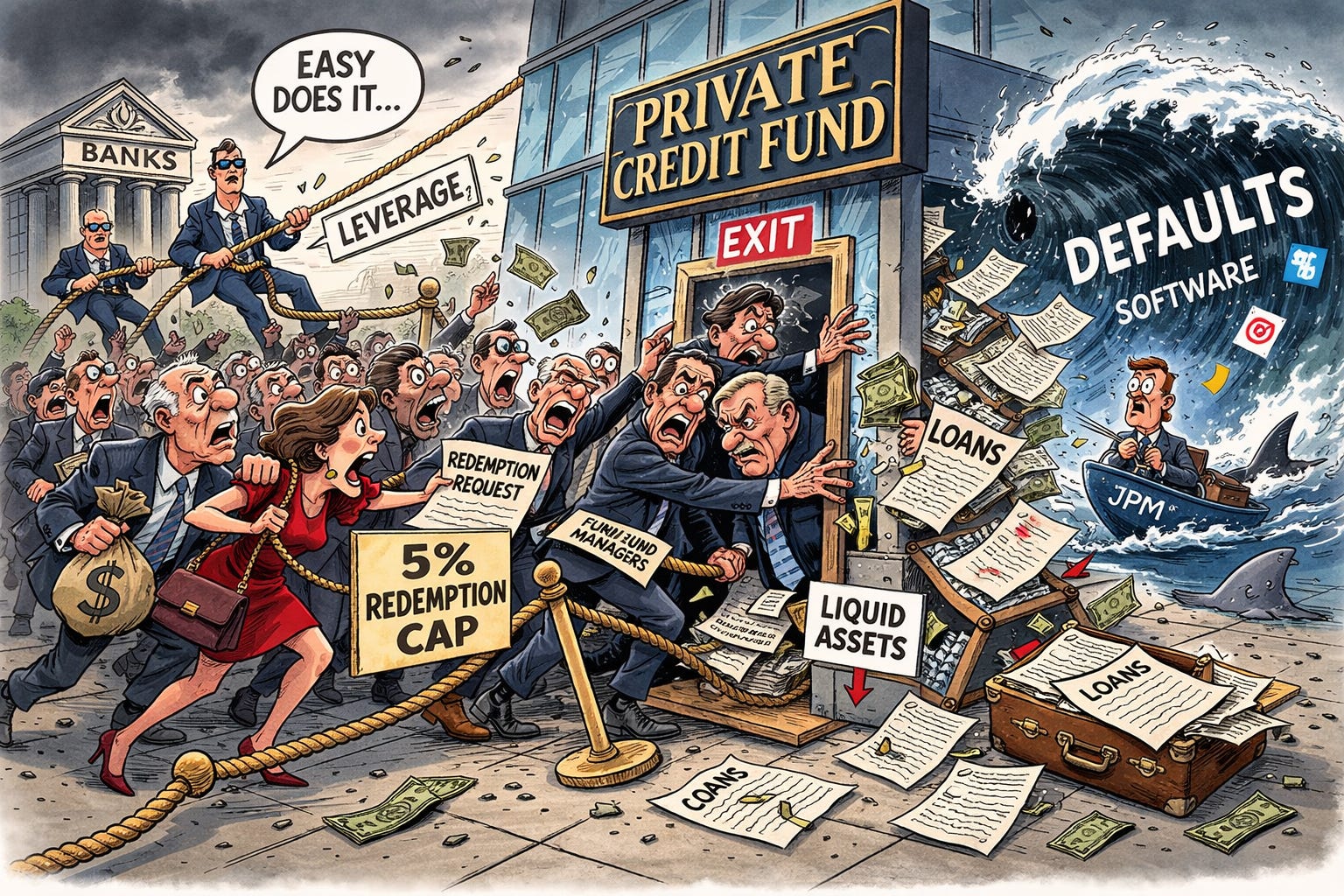

🔍 Private Credit Faces Liquidity Crisis: Major funds freeze withdrawals as banks mark down collateral, sparking fear.

🧠 One Big Thing

The Fed’s Stagflation Trap

The Federal Reserve faces a tightening stagflationary bind as escalating energy costs from the Iran conflict clash with a deteriorating labor market. National diesel prices exceeding five dollars are fueling inflation while domestic growth and consumer sentiment reach historic lows. This volatility prevents the central bank from cutting interest rates to support the economy without risking persistent price hikes. Investors are consequently repricing assets for an environment with fewer anticipated rate reductions through 2026. Historical data suggests these energy spikes frequently precede global recessions. The core tension lies in the Fed’s inability to address falling growth while energy-driven inflation remains uncontained.

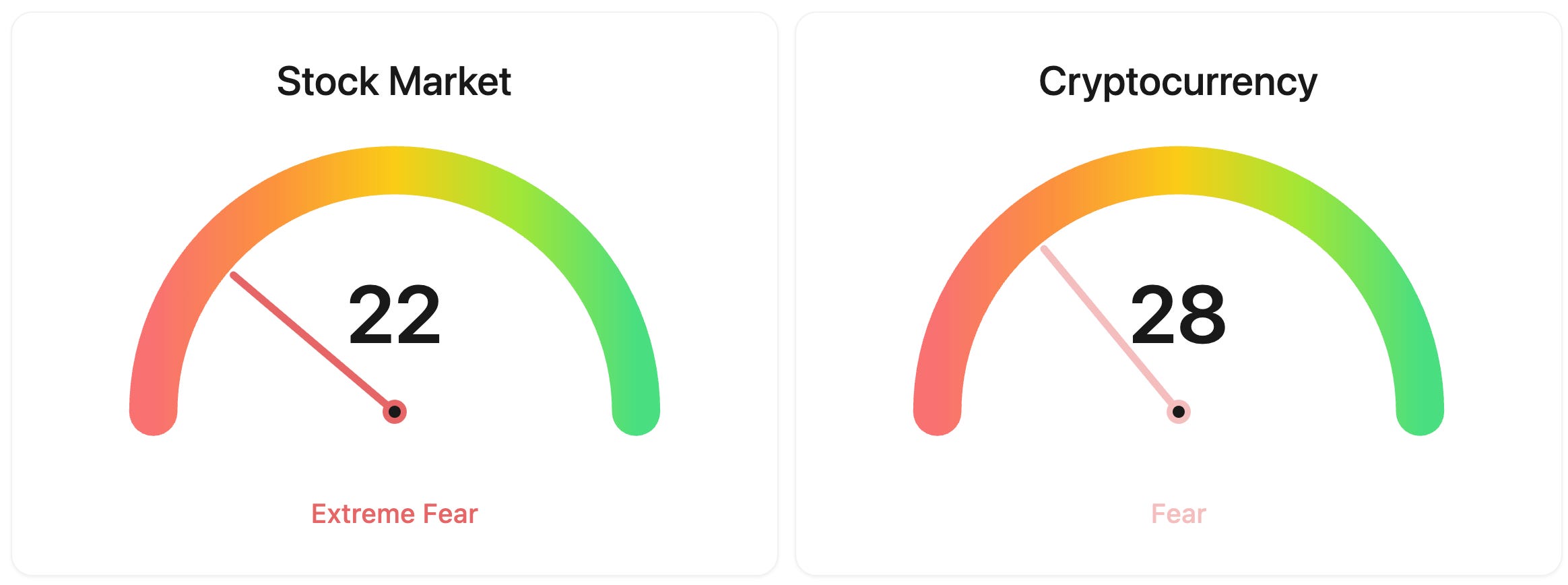

⚖️ Fear & Greed

📉 The Number That Matters

$265 BILLION

$265 BILLION in market capitalization has evaporated from alternative managers as private credit redemptions freeze. Today’s deep dive examines how this $2 trillion sector faces a structural reckoning driven by back-leverage and rising software-sector defaults.

⚔️ Winners vs Losers

Winners

KNDI 0.00%↑: Kandi Technologies Group moved sharply higher in pre-market with no specific catalyst identified.

STIM 0.00%↑: Neuronetics, Inc. is rallying ahead of its Q4 2025 earnings release and conference call scheduled for this morning, following strong preliminary results reported in February showing Q4 revenue of $41.8M (up 86% as reported) and the company’s first quarter of positive operating cash flow.

PLBY 0.00%↑: Playboy, Inc. surged after reporting a Q4 earnings beat yesterday, posting EPS of $0.03 versus the $0.01 consensus and revenue of $34.9 million that topped the $33.52 million estimate, marking a return to quarterly profitability.

CING 0.00%↑: Cingulate Inc. continues to climb as investors position ahead of the May 31, 2026 PDUFA date for its lead ADHD candidate CTx-1301, with no specific catalyst today.

LMND 0.00%↑: Lemonade, Inc. is bouncing after shares sank 40% in February following a Q4 report that disappointed investors despite strong revenue growth, with the stock still well off its 52-week high.

PURR 0.00%↑: Hyperliquid Strategies Inc. extended its recent rally, buoyed by analyst upgrades including a target price increase from Cantor Fitzgerald on the digital asset treasury company focused on accumulating the HYPE token.

Losers

MVST 0.00%↑: Microvast Holdings, Inc. plunged after reporting a dismal Q4, with revenue of $96.4 million down 15% year over year and gross margin collapsing to 1.0% from 36.6% due to $29.0 million in impairment charges. Full-year revenue of $427.5 million also missed the company’s $450-475 million guidance.

LNSR 0.00%↑: LENSAR, Inc. cratered after announcing it reached an agreement with Alcon to terminate their merger agreement, as the FTC intended to seek to block the acquisition and regulatory approval was unlikely to be met by the deadline.

HFFG 0.00%↑: HF Foods Group Inc. sold off following its Q4 report yesterday, where the company posted modest results with net revenue of $1.23 billion, up just 2.2%, and offered only low single-digit growth guidance for 2026.

AXTI 0.00%↑: AXT Inc. is pulling back after a parabolic run driven by indium phosphide demand for AI infrastructure, with CEO Morris Young selling 37,905 shares worth $1.93 million and a director also offloading stock near the 52-week high.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $73673 (▼ -1.64%)

Ethereum (ETH): $2313 (▼ -1.72%)

XRP: $1.51 (▼ -2.18%)

Equity Indices (Futures):

S&P 500: $6687 (▼ -0.12%)

NASDAQ 100: $24604 (▼ -0.20%)

FTSE 100: £10376 (▲ 0.28%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.23% (▲ 0.14%)

Oil (WTI): $97 (▲ 2.43%)

Gold: $5002 (▼ -0.11%)

Silver: $80.44 (▼ -0.37%)

Data as of: UK (GMT) 10:39 / US (EST): 06:39 / Asia (Tokyo): 19:39

✅ 5 Things to Know Today

⛽ Diesel Hits $5, Iran’s Security Chief Killed, and the Fed Has No Good Options

The Iran war entered its 18th day with no off-ramp in sight and the economic damage now landing squarely on American consumers. US diesel crossed $5 a gallon for the first time since December 2022, reaching a national average of $5.04 according to the American Automobile Association (AAA). Regular gasoline hit $3.72, up nearly 80 cents in a month. Diesel powers the trucks, trains, ships, and farm equipment that move almost everything in the US economy, meaning the price spike will ripple into food, freight, and construction costs for months. Brent crude traded above $105 a barrel after Iran set the Shah natural gas field in the United Arab Emirates (UAE) ablaze with a drone strike, the first time Iran has hit an upstream oil or gas facility in the UAE during the conflict. The key port of Fujairah, the UAE’s only crude export route that bypasses the Strait of Hormuz, suspended oil loadings after a separate attack. Israel claimed overnight that it killed Ali Larijani, the secretary of Iran’s Supreme National Security Council and widely considered the country’s de facto leader since the assassination of Supreme Leader Khamenei on the war’s first day. Iran has not confirmed the claim (Bloomberg).

The Federal Open Market Committee (FOMC), the Federal Reserve’s rate-setting body, begins its two-day meeting today with markets pricing a 97% chance it holds rates steady at 3.50-3.75%. But the statement language will be scrutinised intensely. The economy lost 92,000 jobs in February against expectations of 50,000 gained, fourth-quarter gross domestic product (GDP) was revised down to just 0.7% annualised, and the University of Michigan consumer sentiment index fell to 55.5, a reading in the 2nd percentile of the survey’s entire history, meaning Americans haven’t felt this pessimistic about the economy in decades. On the other side, core Personal Consumption Expenditures (PCE), the Fed’s preferred inflation gauge, sits at 3.0-3.1%, well above the 2% target, and analysts project headline Consumer Price Index (CPI) inflation could spike to 3.8-4.5% by the second quarter as energy costs feed through. Ed Yardeni of Yardeni Research has raised his probability of 1970s-style stagflation, the toxic combination of rising prices and falling growth, to 35% (CNBC).

The Larijani assassination, if confirmed, removes the most prominent remaining figure in Iran’s wartime leadership and deepens the question of who, if anyone, has the authority to negotiate an end to this conflict. Iraq said today it is in contact with Iran to allow some oil tankers through the Strait of Hormuz, offering a sliver of hope for partial relief. But no country has committed warships to help reopen the waterway despite Trump’s public appeals to allies and China alike. The 10-year Treasury yield has surged to 4.26-4.28% from roughly 4.00% before the war, gold sits near $5,009 an ounce, and the 30-year yield is approaching the psychologically important 5% threshold. Every significant oil price spike in modern history, including 1973, 1978, and 2008, has been followed by some form of global recession (Reuters).

Sensei’s Insight: The Fed’s paralysis is now the story within the story. Each week it holds rates while oil stays elevated, inflation expectations risk becoming embedded in wage demands and pricing decisions. Markets previously priced three 2026 rate cuts; they now price one to two. Watch whether tomorrow’s statement formally acknowledges the stagflation bind, because that language shift alone could reprice bonds and equities sharply.

🚀 Nvidia Unveils Its Next Superchip and Projects $1 Trillion in Orders

Nvidia chief executive Jensen Huang took the stage at the company’s annual GPU Technology Conference (GTC) in San Jose yesterday and delivered what may be the most ambitious product announcement in the company’s history. The centrepiece was Vera Rubin, a new platform comprising seven chips now in full production and five rack-scale systems designed to function as a single giant artificial intelligence (AI) supercomputer. Huang projected that purchase orders for the current Blackwell generation and the incoming Vera Rubin systems would reach at least $1 trillion through 2027, double the $500 billion he projected last year. The headline chip, the Vera Rubin NVL72, uses 72 GPUs and 36 CPUs with 1.3 million components, liquid-cooled by 45-degree water, and Nvidia claims it delivers 10 times more performance per watt than the current Blackwell generation at 10 times lower cost per token, the fundamental unit of AI computation (CNBC).

The second major reveal was the Groq 3 Language Processing Unit (LPU), the first product from Nvidia’s roughly $20 billion acquisition of Groq, which closed in December 2025. The chip targets inference, the process of running AI models at scale rather than training them, and delivers up to 35 times higher throughput per megawatt when paired with Vera Rubin. Samsung will manufacture it, with shipments expected in the third quarter. Huang also outlined the 2028 Feynman roadmap, the next-generation GPU architecture, and confirmed Amazon Web Services (AWS) has committed to deploying more than one million Nvidia GPUs. Separately, Amsterdam-based Nebius Group announced a $27 billion, five-year deal with Meta to provide AI infrastructure, including one of the first large-scale Vera Rubin deployments. Nebius shares surged 15% to $129.85 on the news (Bloomberg).

Sensei’s Insight: The Groq acquisition is the move worth watching most closely. Nvidia is now building dedicated hardware for inference, the segment where competition from Google’s TPUs, Amazon’s Trainium chips, and custom silicon has been strongest. If Groq delivers on its throughput claims, it closes the one gap competitors were trying to exploit. That consolidation of the full AI stack, from training to inference, could make Nvidia’s ecosystem even harder to leave.

⚖️ Federal Judge Blocks RFK Jr.’s Vaccine Overhaul in Sweeping Ruling

A federal judge in Boston issued a preliminary injunction yesterday blocking key parts of Health and Human Services (HHS) Secretary Robert F. Kennedy Jr.’s effort to reshape US childhood vaccine policy. Judge Brian E. Murphy’s ruling was sweeping: it struck down the Centers for Disease Control and Prevention (CDC) memo that had reduced routinely recommended childhood vaccines from covering 17 diseases to 11, stripping vaccines for rotavirus, meningococcal disease, hepatitis A, hepatitis B, influenza, COVID-19, and RSV of their universal recommendation. Murphy also stayed the appointments of all 13 members Kennedy had installed on the Advisory Committee on Immunization Practices (ACIP), the expert body whose recommendations determine which vaccines insurers must cover at no cost, after Kennedy fired all 17 prior independent members in June 2025. Every vote taken by the reconstituted committee was reversed, including a December decision to eliminate the universal hepatitis B birth dose (Reuters).

The ruling’s legal basis centred on the Administrative Procedure Act (APA), the law that governs how federal agencies make policy changes. Murphy found the CDC’s January memo was “arbitrary and capricious” because it abandoned decades of established practice without adequate explanation. The ruling came at roughly 3:45 PM Eastern yesterday, near market close, meaning the full stock reaction plays out today. Pfizer makes Prevnar 20 (roughly $6.5 billion in annual revenue) and the RSV vaccine Abrysvo. Merck makes Gardasil 9 for HPV and RotaTeq for rotavirus, one of the vaccines removed from the schedule. Sanofi’s RSV treatment Beyfortus generated 1.8 billion euros in revenue. Moderna’s mResvia targets RSV. All had products directly affected by the schedule reduction, and the ruling restoring the prior schedule preserves those revenue streams. Moderna is already up 66% year-to-date and 123% from its November 2025 lows (CNBC).

Sensei’s Insight: The legal win preserves the demand architecture, but the damage to vaccine confidence from a year of Kennedy’s public messaging won’t be reversed by a court order. US vaccine sales have declined across the board for every major manufacturer. Watch whether pharma companies begin guiding for volume recovery on earnings calls, because until uptake rates actually improve, restored recommendations on paper don’t translate to restored revenue.

🤖 Meta Plans Massive Layoffs While Doubling Down on AI Spending

Meta Platforms is planning layoffs that could eliminate 20% or more of its roughly 79,000-person workforce, approximately 15,800 jobs, to offset its surging AI infrastructure spending. The company has earmarked $115 to $135 billion in capital expenditure for 2026, roughly double what it spent in 2025, almost entirely directed at AI data centres and compute. A Meta spokesperson called the reporting “speculative reporting about theoretical approaches.” Wall Street rewarded the news: Meta shares rose roughly 2.3% yesterday, with investors interpreting the cost cuts as margin-positive. Jefferies analysts noted that if Meta is willing to reduce headcount at this scale while accelerating AI investment, it signals a broader shift where AI is increasingly replacing, rather than supplementing, human productivity (Reuters).

Meta is not alone. Block recently cut 40% of its staff and Atlassian cut 10%, both citing AI-driven efficiencies. Over 12,000 US job cuts in 2026 have been linked specifically to AI displacement. The pattern emerging across big tech is consistent: grow headcount aggressively during the zero-interest-rate era, then use AI as the justification for structural workforce reductions that improve margins permanently. For investors, the question is whether these cuts reflect genuine productivity gains from AI tools or simply provide convenient cover for overdue downsizing. The answer likely varies by company, but the market is clearly rewarding the strategy regardless, treating each AI-linked layoff announcement as a signal of operational discipline rather than distress.

Sensei’s Insight: The $135 billion capex figure is worth sitting with. Meta is simultaneously firing people and spending more on infrastructure than most countries spend on defence. The bet is that AI compute generates more value per dollar than human employees. If that thesis proves correct, it reshapes margin structures across the entire tech sector. If it doesn’t, Meta is building the most expensive white elephant in corporate history. Watch the revenue-per-employee trend over the next two quarters for early evidence of which way this goes.

🇬🇧 Trump Calls UK Approach “Terrible” in Sharpest US-UK Rift in Decades

President Trump publicly attacked British Prime Minister Keir Starmer yesterday, calling the UK’s stance on the Iran conflict “terrible” after Starmer declared from Downing Street that Britain “will not be drawn into the wider war.” Trump recounted asking Starmer directly to deploy two aircraft carriers and minesweepers to help reopen the Strait of Hormuz, and expressed frustration that Starmer wanted to consult his team before responding. The sharpest line came with a veiled threat: “Whether we get support or not, I can say this, and I said it to them: we will remember.” The UK has participated only in defensive operations, with Royal Air Force (RAF) jets intercepting Iranian drones over Jordan and Qatar, but Starmer refused to let the US use British bases for offensive strikes and denied the carrier request. No major US ally has agreed to send warships into the Strait during active hostilities (CNBC).

The trade implications are the critical concern for investors. The US-UK trade deal signed in May 2025 left a 10% baseline tariff on British goods, reduced auto tariffs from 27.5% to 10%, and zeroed out steel and aluminium duties. Total annual goods trade between the two countries runs approximately $148 billion, with UK exports to the US worth roughly $68 billion. Trump’s “we will remember” language and his separate warning that failure to help would be “very bad for the future of NATO” both imply trade consequences. The pound has already been punished, falling to roughly $1.3260, a three-month low, down from above $1.38 earlier in the year. Markets have dramatically repriced Bank of England rate expectations, swinging from two expected rate cuts to a 50%-plus probability of a hike by year-end as energy-cost-driven inflation fears mount. Defence stocks are the standout beneficiary: BAE Systems carries a record order backlog of 83.6 billion pounds and its shares are up roughly 23% year-to-date (Bloomberg).

Sensei’s Insight: The deeper signal here is what’s not happening. Not a single major US ally, not the UK, France, Germany, Japan, or Australia, has committed warships to Hormuz. That unified refusal means the oil supply disruption has no multilateral resolution path, only a bilateral US-Iran one. Until that changes, the energy risk premium stays elevated regardless of what any individual country does.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: The Private Credit Crunch: What’s Going On, Why It Matters, and What Happens Next

The $2 trillion private credit market is facing something it has never experienced at this scale: a genuine crisis of confidence. Over the past six weeks, five major fund managers (Blue Owl, Blackstone, BlackRock, Morgan Stanley, and Cliffwater) have all either frozen, capped, or scrambled to meet investor withdrawal requests from their flagship credit funds. JPMorgan has started marking down the value of loans it holds as collateral from these funds. Deutsche Bank has disclosed $30 billion in exposure to the sector. Morgan Stanley’s analysts now forecast default rates could hit 8%. And regulators are paying attention: the Financial Stability Oversight Council has stood up new working groups on market resilience and non-bank risks that explicitly include private credit.

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.