Morning Forecast: Tuesday, 24 February

The Man Who Survived 2008 Just Named the Next Sector to Blow Up

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

📉 Treasury Yields Signal Debt Crisis: Rising long-term forward rates confirm investor fears over ballooning federal deficits rather than simple inflation.

🏠 Home Depot Beats Earnings Estimates: Surprise sales growth and lower mortgage rates boosted shares despite a frozen, low-turnover housing market.

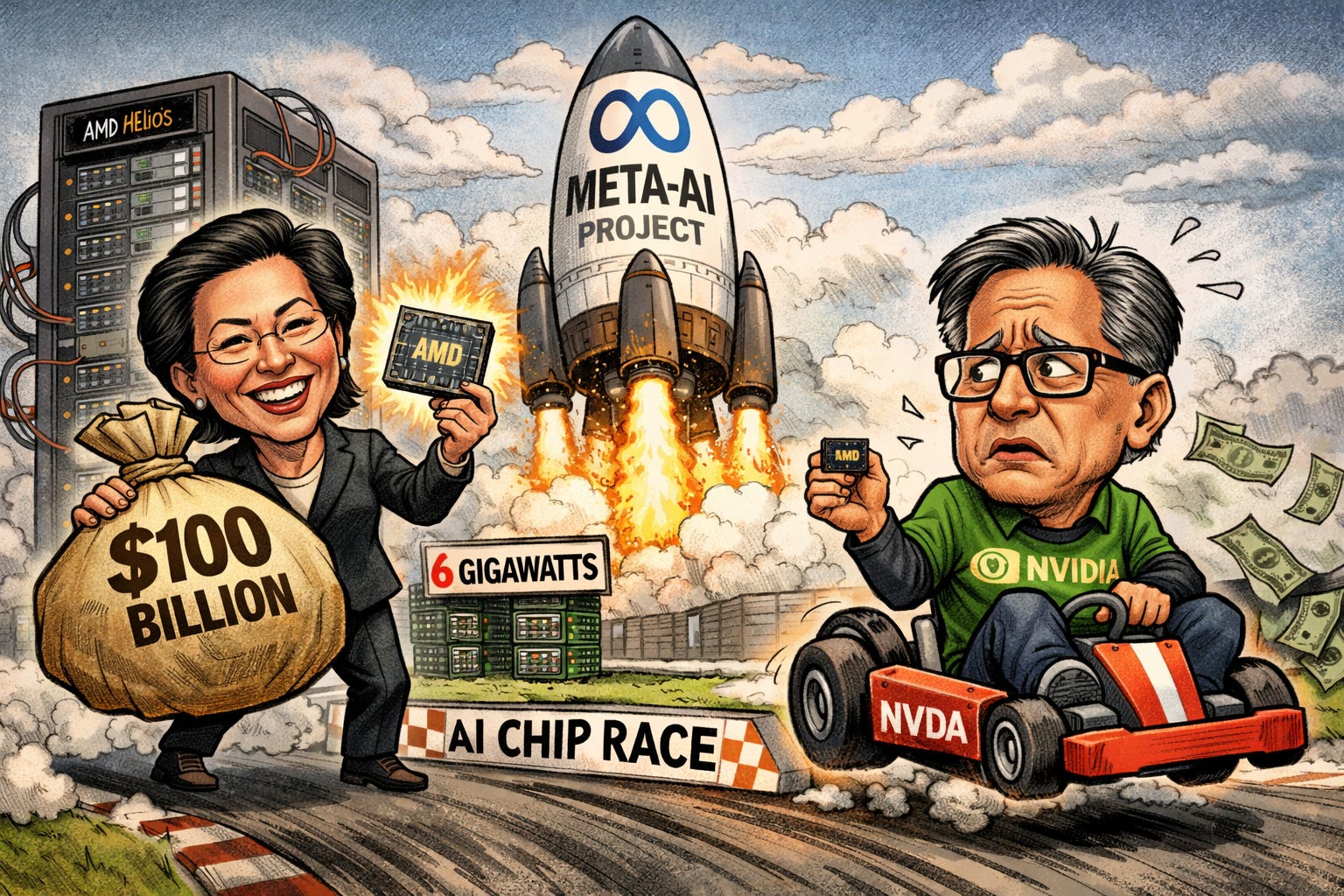

🔥 AMD Lands Massive Meta Deal: A $100 billion partnership for AI data centers positions AMD as a major custom silicon competitor.

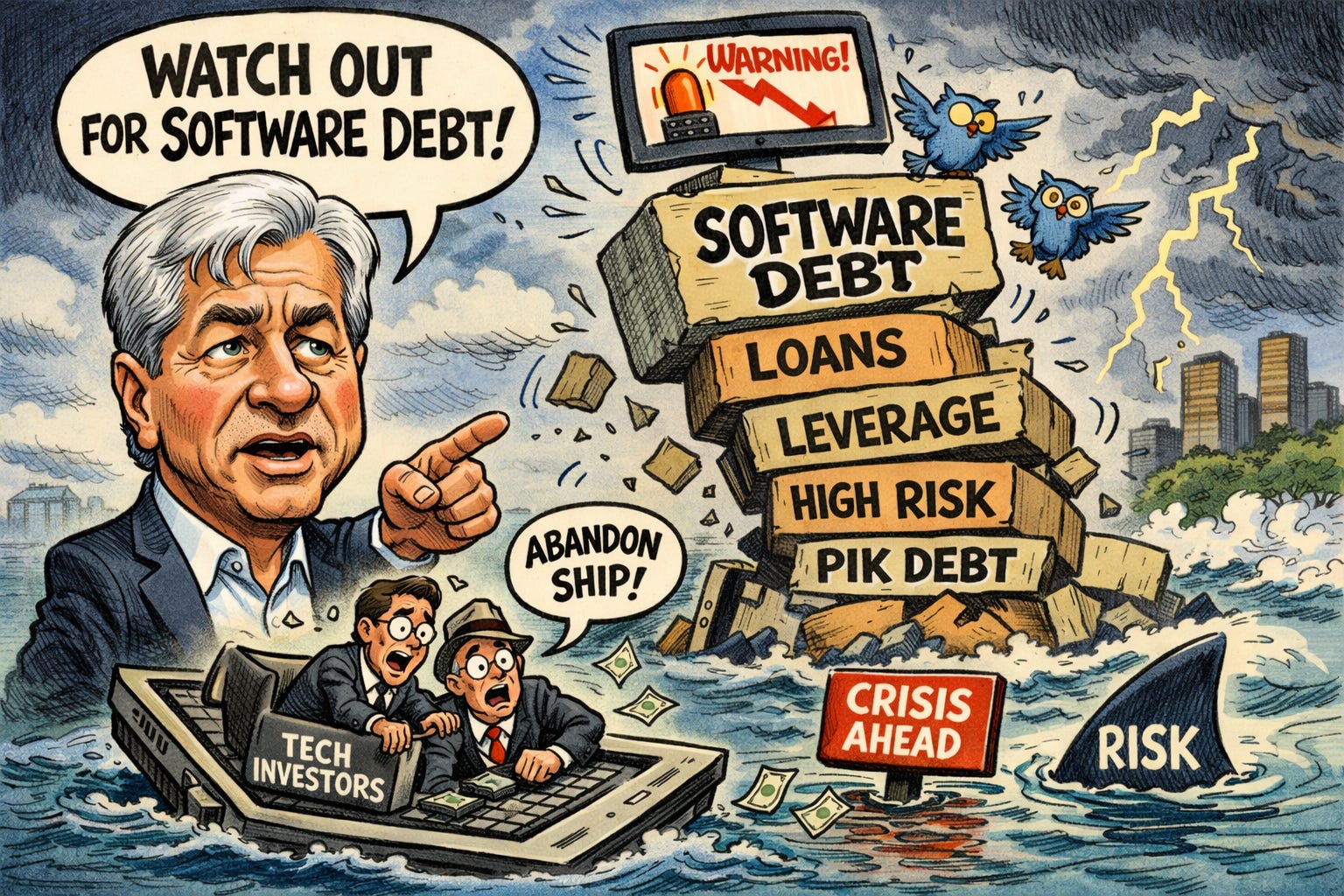

⚠️ Dimon Warns of Software Risk: JPMorgan’s CEO flagged enterprise software lending as a potential credit crisis trigger amidst record-low spreads.

₿ Bitcoin Drops Below $64,000: Crypto fell as the “digital gold” narrative weakened, showing high correlation with struggling speculative software stocks.

🔍 Trump’s State of the Union: Tonight’s speech addresses new 10% stopgap tariffs and military tensions with Iran following Supreme Court setbacks.

🧠 One Big Thing

A Forced Strategic Reset

Tonight’s address marks a forced strategic reset after the Supreme Court dismantled the administration’s primary tariff framework. The White House has responded with a 150-day emergency trade stopgap that faces a hard legal expiration this summer. This policy instability coincides with a massive military mobilization in the Middle East before a critical diplomatic deadline on Thursday. Investors now face heightened uncertainty as gold hits record highs while domestic growth slows. The speech will reveal if the President seeks legislative compromise or persists with temporary executive workarounds. Any signal of military escalation or trade defiance will likely intensify existing market volatility.

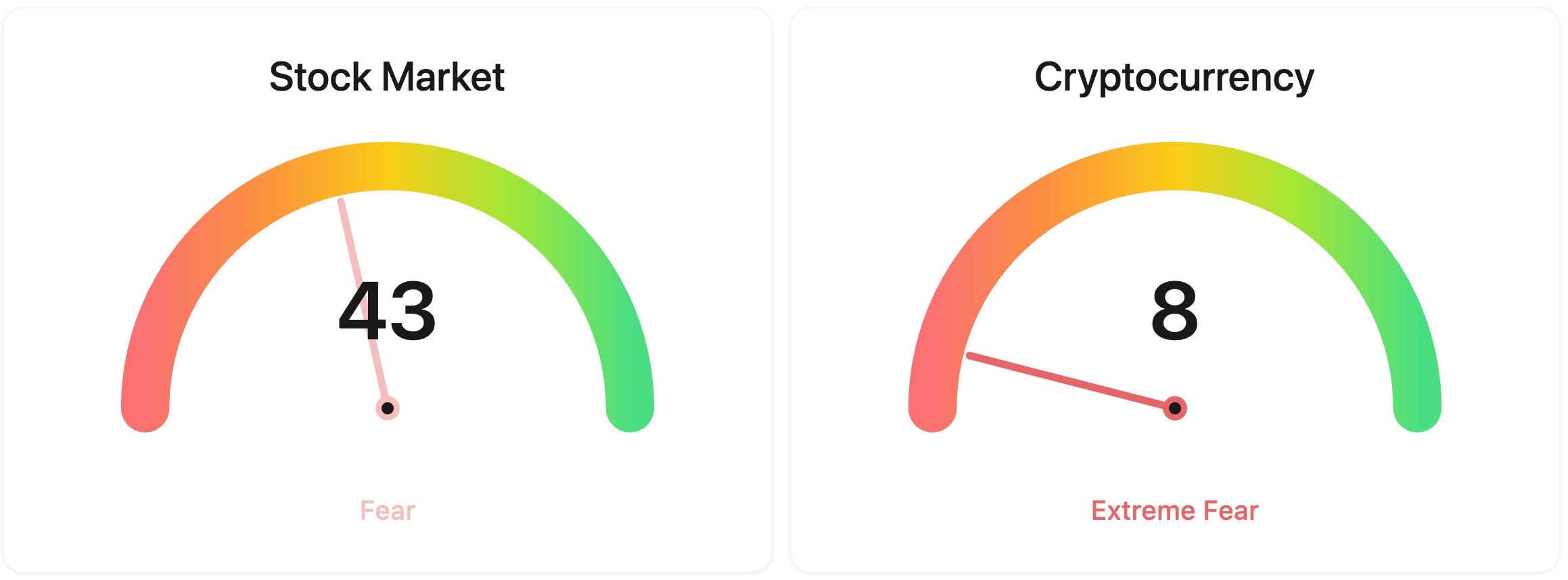

⚖️ Fear & Greed

📉 The Number That Matters

2.9%

US high-yield credit spreads sit at 2.9%, mirroring levels seen immediately before the 2008 financial crisis. Jamie Dimon has warned of "hidden leverage" and potential systemic risks within the enterprise software lending sector as asset prices remain inflated.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $63,436 (▼ -1.85%)

Ethereum (ETH): $1,832 (▼ -1.28%)

XRP: $1.34 (▼ -1.17%)

Equity Indices (Futures):

S&P 500: $6,844 (▲ 0.00%)

NASDAQ 100: $24,912 (▲ 0.60%)

FTSE 100: £10,705 (▲ 0.16%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.04% (▲ 0.22%)

Oil (WTI): $67 (▲ 0.33%)

Gold: $5,124 (▼ -1.94%)

Silver: $87.01 (▼ -1.29%)

Data as of UK (GMT): 3:04 PM / US (EST): 10:04 AM / Asia (Tokyo): 12:04 AM

✅ 5 Things to Know Today

📉 The Bond Market Is Flashing a Warning Most Investors Can’t See

The 10-year Treasury yield fell to 4.04% on Monday, its lowest in three months, and on the surface that looks reassuring. But a lesser-known metric is telling a very different story. The 10-year-10-year forward rate, which captures what markets expect the 10-year yield to be a decade from now, has surged 53.5 basis points to 5.62% since Trump’s inauguration. A Federal Reserve staff paper published February 12 confirmed the driver: growing concerns about federal deficits and the risk of future supply shocks, not inflation expectations. In other words, the Fed still has credibility on prices, but the market sees a debt problem it can’t fix.

The Congressional Budget Office (CBO) outlook published February 11 spells out why. The fiscal year 2026 deficit is projected at $1.9 trillion, or 5.8% of gross domestic product (GDP), ballooning to $3.1 trillion by 2036. Debt held by the public will hit 101% of GDP this year and 120% by 2036, surpassing the World War II record around 2030. Interest payments alone are set to more than double from $1.0 trillion to $2.1 trillion over the decade, eating nearly a fifth of all federal spending. Meanwhile, the Supreme Court’s February 20 ruling striking down presidential tariffs under the International Emergency Economic Powers Act (IEEPA) added a new wrinkle: long-dated yields initially rose on Friday as investors priced in lower tariff revenue making the deficit even worse. Refund estimates for already-collected IEEPA tariffs range from $85 billion to $175 billion, though some analysts doubt consumers will ever see that money.

Sensei’s Insight: Neither rate cuts nor tariff revenue can outrun a debt trajectory this entrenched. The CBO's projections assume no recession and no new spending. Reality will almost certainly be worse.

🏠 Home Depot Snaps Its Losing Streak as Mortgage Rates Hit a Three-Year Low

Home Depot delivered its first earnings beat in four quarters on Tuesday, with adjusted earnings per share (EPS) of $2.72 against a consensus estimate of $2.52 to $2.54, a surprise of roughly 7 to 8%. Same-store sales rose 0.4% where analysts had expected a 0.4% decline, and revenue of $38.2 billion edged past estimates despite a shorter 13-week quarter compared with 14 weeks a year ago. Average ticket size climbed 2.4%, and big-ticket transactions above $1,000 grew 1.3%, signs that the professional contractor business is finding its footing. Shares jumped 4.2% to $392.81, adding $15.1 billion in market capitalisation.

The backdrop remains challenging. Chief Financial Officer Richard McPhail said on CNBC that the housing market has been “frozen” for three years, with turnover stuck around 3% of units versus a long-term average of 4.1%. Homeowners locked into sub-3% pandemic-era mortgages have little incentive to sell into a 6% rate environment. But the 30-year fixed mortgage rate at 5.99%, its lowest since 2022, and over $11 trillion in tappable home equity suggest demand could start to thaw. Home Depot reiterated fiscal 2026 guidance of flat to 2% comparable sales growth and adjusted EPS of roughly $14.69 to $15.28. More than half of its products are sourced domestically, giving it a buffer against tariff pressure. Lowe’s, which trades at a notably cheaper 19 times forward earnings versus Home Depot’s 24 to 25 times, reports Wednesday.

Sensei’s Insight: A beat is a beat, but fewer customers walking through the door while the housing market stays frozen isn’t a recovery story yet. Lowe’s reports Wednesday at 19x forward earnings. That comparison could be telling.

🔥 AMD Lands a $100 Billion Meta Deal and Reshapes the AI Chip Race

AMD announced a partnership with Meta to deploy 6 gigawatts of data centre infrastructure powered by AMD processors over five years, starting in the second half of 2026. CEO Lisa Su described the value as “double-digit billions” per gigawatt, putting the total deal in a range of $60 billion to over $100 billion. AMD will supply custom MI450 Instinct GPUs designed for Meta’s inference workloads alongside two generations of EPYC CPUs, using AMD’s Helios rack-scale architecture developed through the Open Compute Project. The level of customisation is a key differentiator. Analyst Ben Bajarin of Creative Strategies noted there is no indication Nvidia is offering comparable bespoke designs. AMD shares surged as much as 15% in premarket trading before settling around 9 to 11% higher during the session.

The deal comes with unusual financial engineering. Meta receives warrants to purchase 160 million AMD shares at $0.01 per share, roughly 10% of outstanding stock, with tranches vesting as GPU shipments scale from 1 gigawatt toward 6, and a final tranche requiring AMD’s stock to reach $600 versus Monday’s close of $196.60. This is identical in structure to AMD’s October 2025 deal with OpenAI, meaning the two partnerships combined could dilute existing shareholders by approximately 320 million shares, or 20%, if fully vested. Critics have called this vendor financing reminiscent of the dot-com era, though bulls point out Meta generates hundreds of billions in operating cash flow, making it a fundamentally different counterparty. Nvidia reports earnings Wednesday, where 68% revenue growth expectations will test whether the AI chip market is large enough for a genuine number two player.

Sensei’s Insight: AMD isn’t trying to out-Nvidia Nvidia. It’s betting inference becomes the bigger market and that custom silicon wins those contracts. Nvidia’s earnings Wednesday will show whether the pie is growing fast enough for both.

⚠️ Jamie Dimon Says “Watch Out” and Names the Sector Nobody Expects

JPMorgan CEO Jamie Dimon delivered his most pointed credit cycle warning in years at the bank’s annual investor event on Monday. Responding to a question from Wells Fargo analyst Mike Mayo, Dimon drew a direct comparison to the years before the financial crisis: the rising tide was lifting all boats, everyone was making money, and some lenders were “doing dumb things” to generate net interest income (NII). Then he named the sector he thinks could deliver the surprise blow this time around: software. Enterprise software has been the preferred lending category for private credit since 2020, with firms like Blue Owl Capital holding over 70% of their loan books in the sector. Software debt in the leveraged loan market trades at roughly 91 cents on the dollar, and the iShares Software ETF is down 15% in February alone, its worst month since 2008.

The warning already has a real-world example. On February 19, Blue Owl restricted withdrawals from its retail-focused OBDC II fund, reversed plans to resume redemptions, and sold $1.4 billion of direct-lending investments across three funds. Redemption requests in its tech-focused OTIC fund jumped to roughly 15% of net asset value (NAV), and Blue Owl shares have lost over 50% in the past year. Across the broader credit market, US high-yield spreads sit at approximately 2.9%, near the all-time low of 2.4% set in 2007. Leveraged loan spreads for BB and B-rated credits are at their lowest levels this century. Moody’s has flagged “hidden leverage” building through payment-in-kind debt and NAV lending. Dimon did not predict when the turn comes, but was unequivocal about where he stands: “I’m not assuaged by the fact that asset prices are high. In fact, I think that adds to the risk”.

Sensei’s Insight: High-yield spreads near 2.9% are practically identical to 2007 levels. The market is pricing in perfection at the exact moment the man who survived 2008 is telling you to worry. That gap between price and caution is worth watching.

₿ Bitcoin Plunges Below $64,000 as the “Digital Gold” Narrative Shatters

Bitcoin fell to roughly $63,100 to $63,500 on Tuesday, down approximately 3 to 3.6% in 24 hours and extending a decline that has erased 29% of its value year-to-date. The total crypto market capitalisation has shed roughly $750 billion in 2026, dropping from $2.97 trillion to $2.22 trillion. Bitcoin now sits nearly 50% below its all-time high of $126,210, reached in October 2025. The immediate trigger was a viral report from Citrini Research titled “The 2028 Global Intelligence Crisis,” a fictional scenario in which AI drives US unemployment to 10.2% as automation hollows out middle-class jobs. The post racked up 24.4 million views on X, and Michael Burry amplified it with bearish commentary. Bitcoin spot exchange-traded funds (ETFs) have recorded $3.8 billion in outflows over five consecutive weeks, with BlackRock’s IBIT alone losing $2.13 billion.

The deeper problem is what Bitcoin is not doing. Gold has surged roughly 20% year-to-date while Bitcoin has fallen 25%, blowing a hole in the “digital gold” thesis that underpinned much of the institutional case for crypto. Jim Bianco of Bianco Research posted a chart showing Bitcoin and the software stock index moving in near-perfect lockstep, concluding they are essentially the same trade. The 30-day correlation between Bitcoin and the S&P 500 stands at 60.5%. The Crypto Fear and Greed Index hit 5 out of 100 on February 23, a reading labelled “Extreme Fear” at levels not seen consistently since the 2018 bear market. Paradoxically, the regulatory environment has never been friendlier: the GENIUS Act on stablecoins is being implemented, the CLARITY Act passed the House, the Securities and Exchange Commission (SEC) dropped Biden-era enforcement actions, and XRP and Solana ETFs are now trading. None of it has mattered against the macro headwinds.

Sensei’s Insight: A 60.5% correlation with the S&P 500 means Bitcoin is a risk-on bet, not a hedge. That said, a Fear and Greed reading of 5 has historically been a terrible time to panic. The question isn’t whether Bitcoin bounces, but what it bounces as.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: Trump’s State of the Union: What Investors Need to Know

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.