Morning Forecast: Tuesday, 27 January

From Shutdown Risks to $117 Silver: Navigating the Most Volatile Week of 2026.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🏛️ Shutdown risks loom over shooting: Minnesota’s shooting triggers a DHS funding clash and potential government closure.

🤝 EU-India trade deal finalized: New agreements slash tariffs to counter volatility from US economic policies.

🇰🇷 Trump threatens South Korean tariffs: Proposed duties target imports to force legislative progress on investment bills.

🇿🇦 South African gold sector revives: Record prices turn aging mines into profitable, high-margin cash machines.

🏦 Fed maintains current interest rates: Chair Powell defends bank independence while facing a DOJ criminal investigation.

🪙 Miners poised for valuation surge: Record gold prices create gaps as analysts underestimate corporate earnings.

🧠 One Big Thing

A massive valuation gap has emerged between record-high precious metals prices and the lagging share prices of the companies mining them. While gold trades near $5,100, most analyst models remain anchored to a $3,200 baseline, causing a significant undervaluation of mining equities. This disconnect creates explosive operating leverage because extraction costs remain relatively fixed while profit margins have essentially doubled. Institutional investors are now positioning for a major "re-rating" cycle as upcoming earnings reports force analysts to upwardly revise profit estimates. If gold maintains levels above $4,000, these miners transition from speculative commodity plays into massive free-cash-flow machines. The upcoming February earnings season will likely serve as the primary catalyst for the market to price in this unprecedented margin expansion.

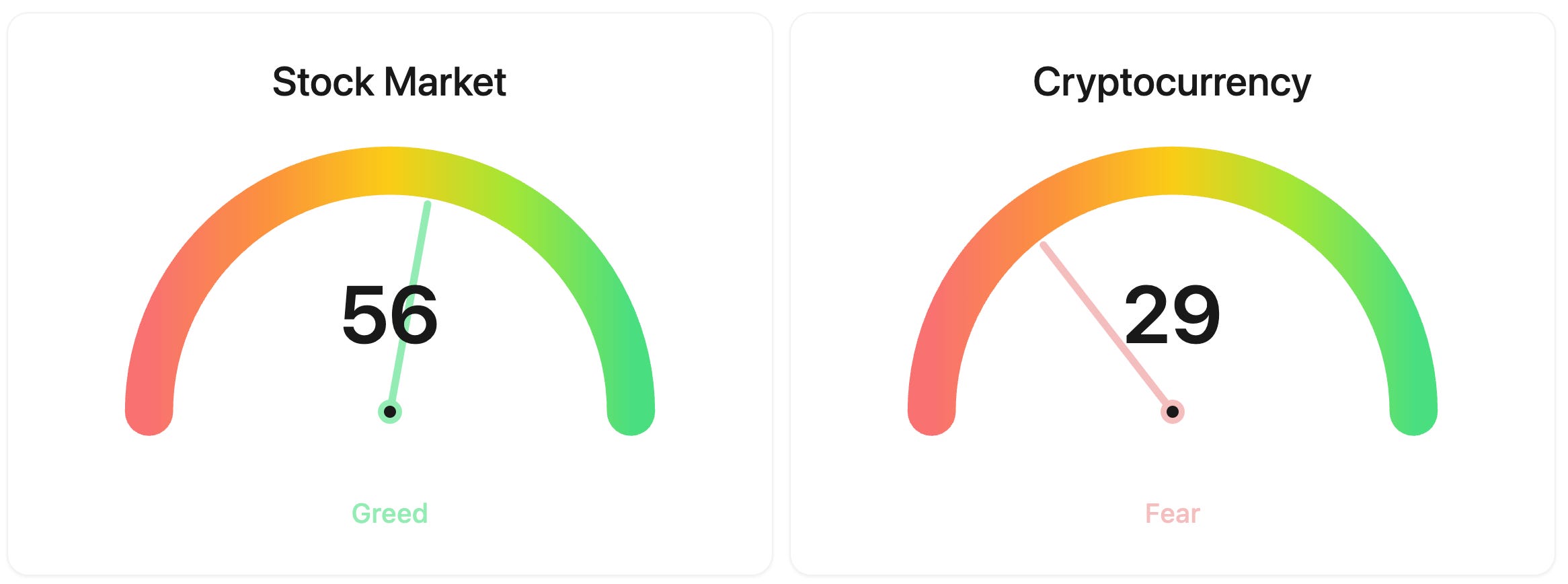

⚖️ Fear & Greed

📉 The Number That Matters

97%

Markets price a 97% probability that the Fed will hold rates at 3.50% to 3.75% tomorrow. However, internal dissent grows as Core PCE stalls at 2.8%, while a DOJ probe into Chair Powell threatens central bank independence.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $87,899 (▼ -0.41%)

Ethereum (ETH): $2,914 (▼ -0.46%)

XRP: $1.89 (▼ -0.80%)

Equity Indices (Futures):

S&P 500: $6,972 (▲ 0.37%)

NASDAQ 100: $26,037 (▲ 0.73%)

FTSE 100: £10,188 (▲ 0.32%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.22% (▲ 0.14%)

Oil (WTI): $61 (▼ -0.39%)

Gold: $5,079 (▲ 1.37%)

Silver: $111.55 (▲ 7.37%)

Data as of UK (GMT): 12:01 pm / US (EST): 7:01 am / Asia (Tokyo): 9:01 pm

✅ 5 Things to Know Today

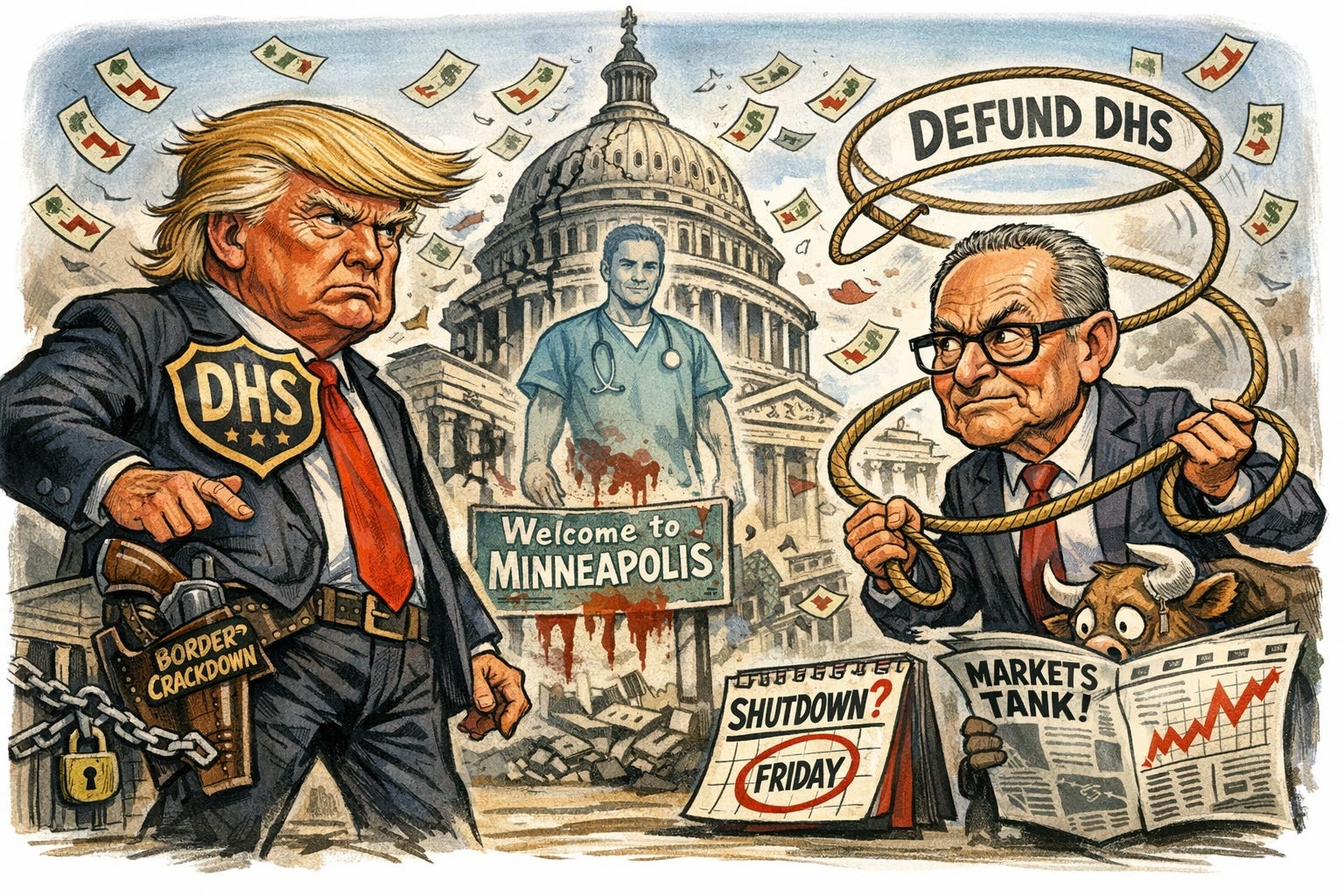

🏛️ Shutdown risks rise after Minnesota federal shooting

A potential government shutdown is looming as President Trump and Senate Democrats clash over Department of Homeland Security (DHS) funding. The flashpoint is the January 24 shooting of Alex Pretti, a 37-year-old ICU nurse and U.S. citizen, by Border Patrol agents during an immigration enforcement surge in Minneapolis. While DHS officials initially claimed Pretti was “violently resisting,” bystander video appears to show him being pepper-sprayed and pinned before being shot multiple times, including in the back. Senate Democratic Leader Chuck Schumer is now threatening to block all DHS funding unless the administration pulls federal agents out of Minnesota cities, creating a high-stakes standoff just weeks after the record-long 43-day shutdown ended in November (Bloomberg).

This isn’t just a local tragedy: it’s a massive hurdle for fiscal stability. For retail investors, the timing is terrible. We just exited a 43-day shutdown in November that rattled the markets, and another lapse in funding could signal a period of prolonged legislative gridlock. Republicans, led by Senate Majority Leader John Thune, are resisting the Democratic demand to defund the Minnesota operations, while the White House remains committed to its immigration crackdown. If neither side blinks, the resulting shutdown may impact everything from federal contracts to broader consumer confidence, which is already sensitive after the previous autumn’s volatility.

Sensei’s Insight: Watch the DHS funding deadline closely. If Schumer holds the line on the Minnesota withdrawal, the risk of a technical default or a prolonged shuttering of non-essential services increases significantly.

🤝 The “Mother of All Deals”: EU and India Pivot Away from US Tariffs

India and the European Union just finalized a massive free trade agreement (FTA) in New Delhi, creating an economic zone of 2 billion people that accounts for roughly 25% of global GDP. The deal is a direct response to geopolitical volatility, specifically the 50% US tariffs currently squeezing Indian exports. Under the new terms, India will slash its legendary 110% auto tariffs down to 10% over five years, while the EU will eliminate or sharply reduce duties on over 99% of Indian goods. This isn’t a “day one” flip, however: the agreement involves a tiered implementation schedule starting as early as January 2027, covering everything from olive oil and wine to machinery and textiles.

This deal signals a major structural shift as both blocs seek alternatives to US-centric trade. For India, it’s a lifeline for labor-intensive sectors like textiles and gems that are currently suffocating under Washington’s trade policies. For the EU, it’s a long-awaited “win” for carmakers and spirit exporters who have been locked out of the world’s most populous market by protectionist walls. While the long-term outlook is structuraly positive, the immediate market reaction was actually negative: the Nifty Auto index slipped 2% on fears that domestic giants like Mahindra & Mahindra will lose their “moat” to cheaper European imports. Investors may want to look past the current FII selling, totaling roughly $4.8 billion this month, and focus on the mid-term boost to India’s pharmaceutical and specialty chemical sectors, which gain a massive cost advantage over Chinese rivals in the European market (Reuters).

Sensei’s Insight: Watch the “implementation gap.” While the headlines are historic, the actual earnings boost for Indian exporters won’t hit until 2027. Expect short-term volatility in Indian auto stocks as they re-price for real competition.

🇰🇷 Trump’s 25% Tariff Salvo: Leverage or Law?

President Trump rattled the trade cages on Monday evening, threatening to jack up tariffs on South Korean imports from 15% to 25%. In a Truth Social post, he targeted automobiles, lumber, and pharmaceuticals, accusing the South Korean National Assembly of dragging its feet on a $350 billion investment deal agreed upon last July. Even though the White House hasn’t filed an official executive order, Trump is citing the International Emergency Economic Powers Act to skip the usual congressional hurdles. The KOSPI index initially dipped but surprisingly rallied to end 2.7% higher, suggesting many institutional desks think this is more of a shakedown than a shift in policy (Bloomberg).

The real friction here is Seoul’s internal gridlock over five investment bills that are currently gathering dust in committee. For investors, the auto sector is the main event since vehicles make up 27% of South Korea’s $122.9 billion in annual shipments to the US. A 25% tariff would be a gut punch to Hyundai, potentially dragging its operating margins down from 9.7% to a measly 6.3%. But don’t ignore the recovery. The market is basically calling Trump’s bluff, betting that South Korean lawmakers will likely cave and pass the bills by the end of February to restore the 15% rate.

Sensei’s Insight: Watch the February legislative deadline in Seoul. If the investment bill passes, expect the tariff threat to evaporate, but any further delay may signal a painful, structural shift for Korean exporters.

🇿🇦 South Africa’s Gold Mining Revival

South Africa’s gold sector is staging an improbable comeback as bullion prices shatter records, recently settling above $5,100 per ounce. This 64% surge in 2025 represents the metal’s largest annual gain since 1979, fueled by central bank buying and geopolitical jitters. The windfall is breathing life into projects like West Wits Mining’s Qala Shallows, which struggled to find backers in 2021 when investors “just didn’t like South Africa.” Fast forward to today: the project secured $100 million in funding and is eyeing its first gold pour in March 2026. With a break-even cost of $1,291 per ounce, the mine sits on a massive cushion compared to the current $5,100+ spot price, signaling a radical shift in the country’s mining viability (Wall Street Journal).

This isn’t just a lucky break for one mine: it’s a fundamental reset of the sector’s profitability. For years, South Africa’s industry was crippled by aging, ultra-deep mines and high costs, but modern mechanized equipment and astronomical prices have flipped the script. Major players are moving fast: Harmony Gold is pouring $410 million into its Mponeng mine, and Sibanye-Stillwater is reviving its Burnstone project. For investors, the takeaway is the massive margin expansion. The gap between production costs and selling prices has widened to nearly $3,300 per ounce for some, turning former laggards into free-cash-flow machines that may support dividends through 2027.

Sensei’s Insight: Watch the $5,200 level for gold. If central bank demand stays at 60 tonnes monthly, even high-cost “marginal” producers could become the market’s new cash cows.

🏦 The Fed’s High-Stakes Hold and the Powell Probe

The Federal Reserve meets tomorrow, January 28, for its first policy showdown of 2026. While a rate hold at 3.50% to 3.75% looks like a 97 percent lock, the underlying friction isn’t exactly calm. Inflation has hit a plateau with Core PCE stalling at 2.8 percent, which is stubbornly above the 2 percent target. The Cleveland Fed’s nowcast suggests this trend isn’t reversing soon, projecting Core PCE at 2.76 percent for the first quarter. Meanwhile, the labor market looks frozen: December added only 50,000 jobs as both hiring and layoffs declined simultaneously. This stalemate is fueling rare internal divisions. Three FOMC members formally dissented in December, highlighting a committee torn between sticky prices and cooling employment (Federal Reserve Board).

This meeting is overshadowed by an unprecedented clash between the central bank and the White House. Chair Jerome Powell recently released a video defending the Fed’s independence against a Department of Justice criminal investigation into his past Senate testimony regarding office renovations. With Powell’s term ending in May 2026 and the Supreme Court currently weighing whether President Trump can legally fire Governor Lisa Cook, markets are pricing in a leadership vacuum. Gold has already surged past $5,100 as the dollar weakens, reflecting fears that institutional stability is cracking. Watch for Powell to use his press conference to reassert the Fed’s autonomy, even if it means delaying rate cuts to prove he isn’t yielding to political pressure.

Sensei’s Insight: The rate decision is just noise. The real signal is Powell’s tone on independence and June’s cut odds. If he sounds defensive, expect dollar volatility to accelerate as May’s term expiration approaches.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: 🪙 The Great Disconnect: Precious Metals Miners in January 2026

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.