Morning Forecast: Tuesday, 28 April

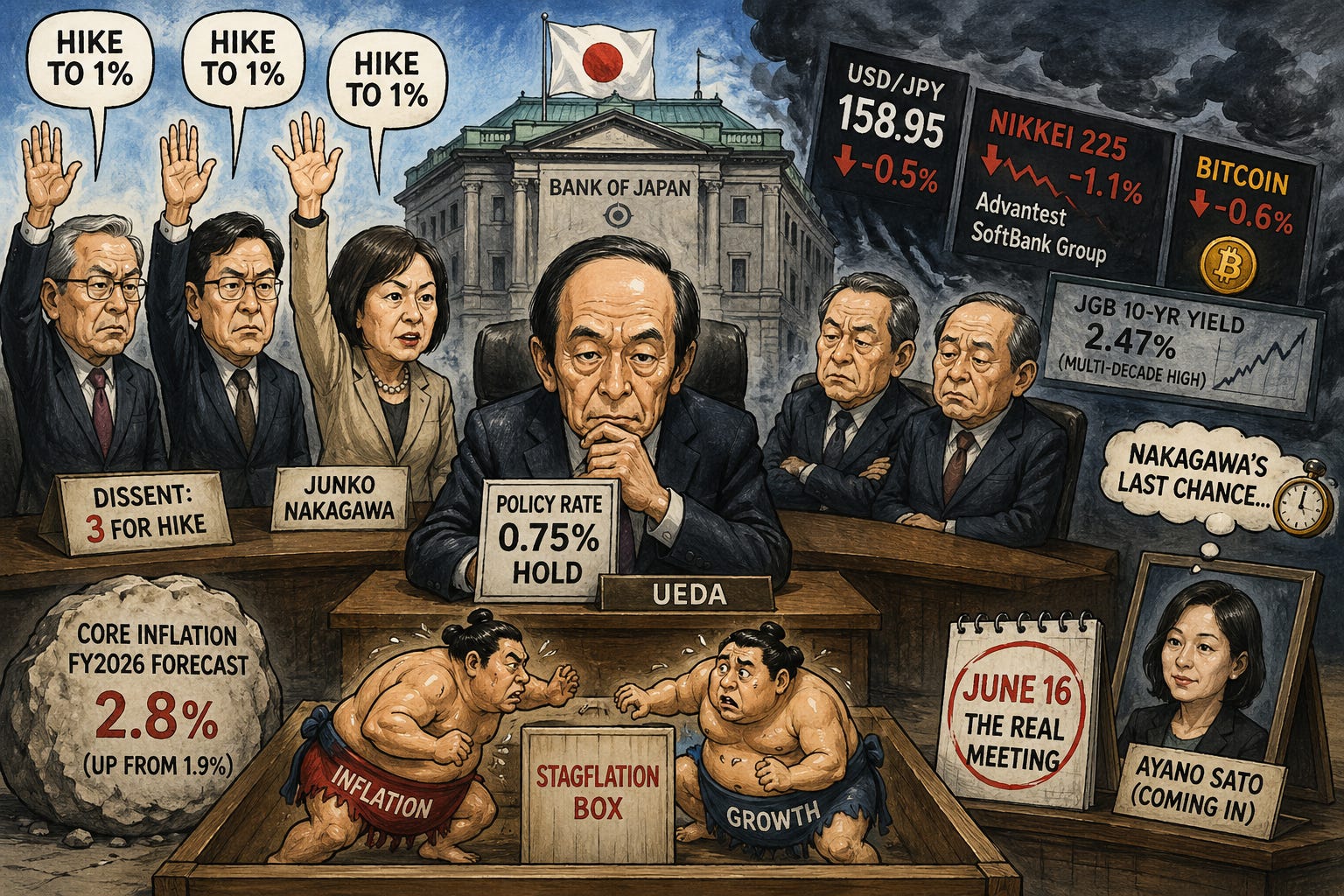

Tokyo held at 0.75%. Three board members wanted 1% now.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🇯🇵 BoJ split signals June hike: Three board members backed an immediate move to 1%, putting June 16 firmly in play.

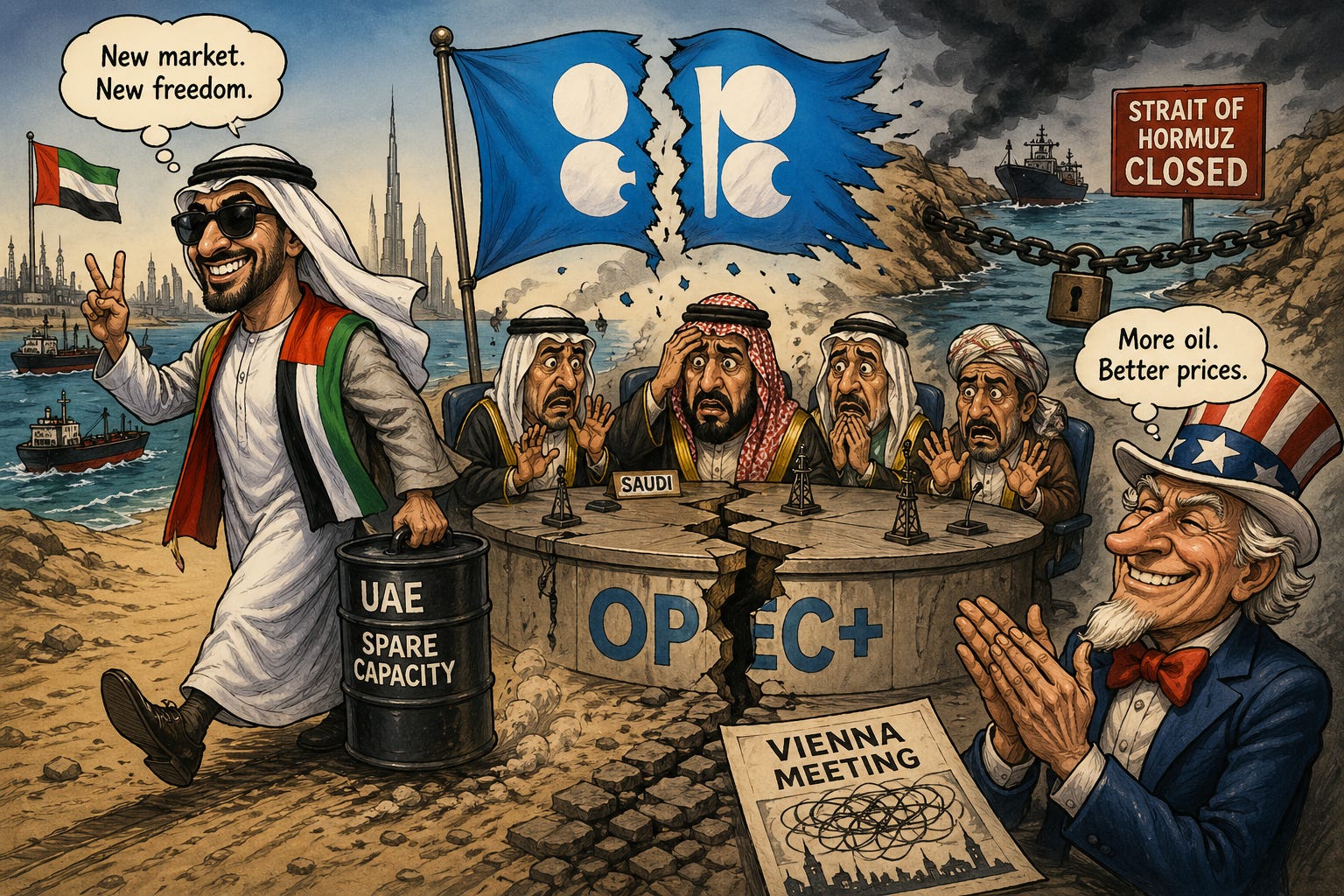

🇦🇪 UAE walks out of OPEC: First major exit since 2019 lands one day before the Vienna meeting opens.

🇪🇺 Brussels targets Gemini’s Android edge: Draft Digital Markets Act rules could force Android open to rival AI assistants.

🛢️ Brent breaks $111, peace stalls: Goldman warns $120 is in play after Iran’s mediated proposal fails to move the market.

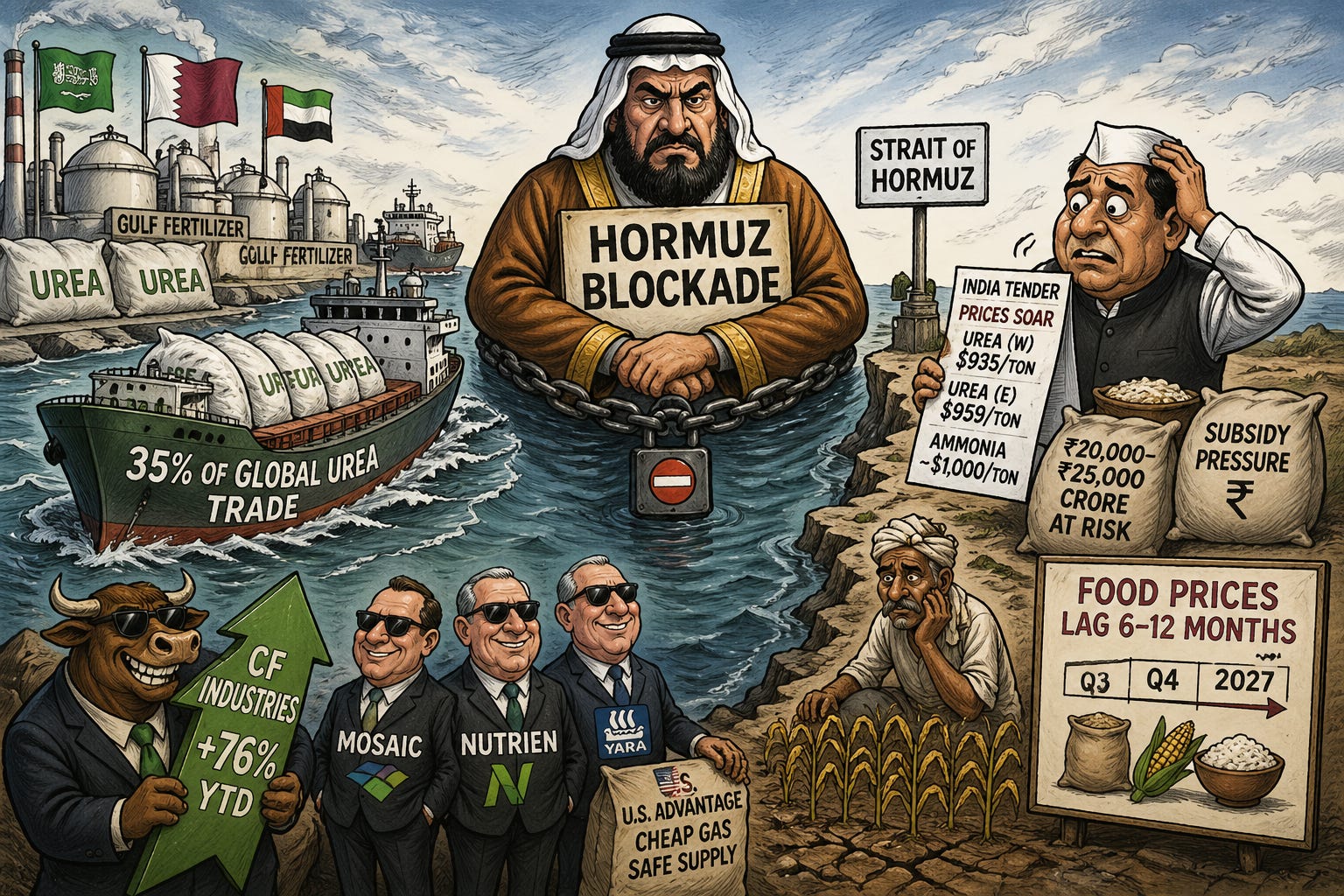

🌾 Hormuz blockade squeezes fertilizer: India paid nearly double for urea as Gulf producers stay locked behind the blockade.

🇻🇪 Big Oil returns to Venezuela: Rigs come out of long-term storage as services commit to the post-Maduro reset.

💰 Kuwait pipeline bids close today: Roughly $7 billion stake draws BlackRock and Brookfield despite Iranian drone damage.

🏦 India tightens bank loss rules: Reserve Bank of India locks the Expected Credit Loss framework for April 2027 rollout.

🧠 One Big Thing

The Bank of Japan held rates at 0.75%, but three of nine board members voted for an immediate hike to 1%, the sharpest hawkish split under Ueda. The bigger move was buried in the outlook: fiscal 2026 core inflation revised up to 2.8% from 1.9%, with growth cut in half. Dissenter Nakagawa's term ends June 29, and her replacement skews dovish, which makes June 16 her last live vote. Money markets repriced that meeting within minutes. Dollar-yen at 158 is the level into Ueda's press conference. Carry trade unwinds get violent when 75 basis points still need to land.

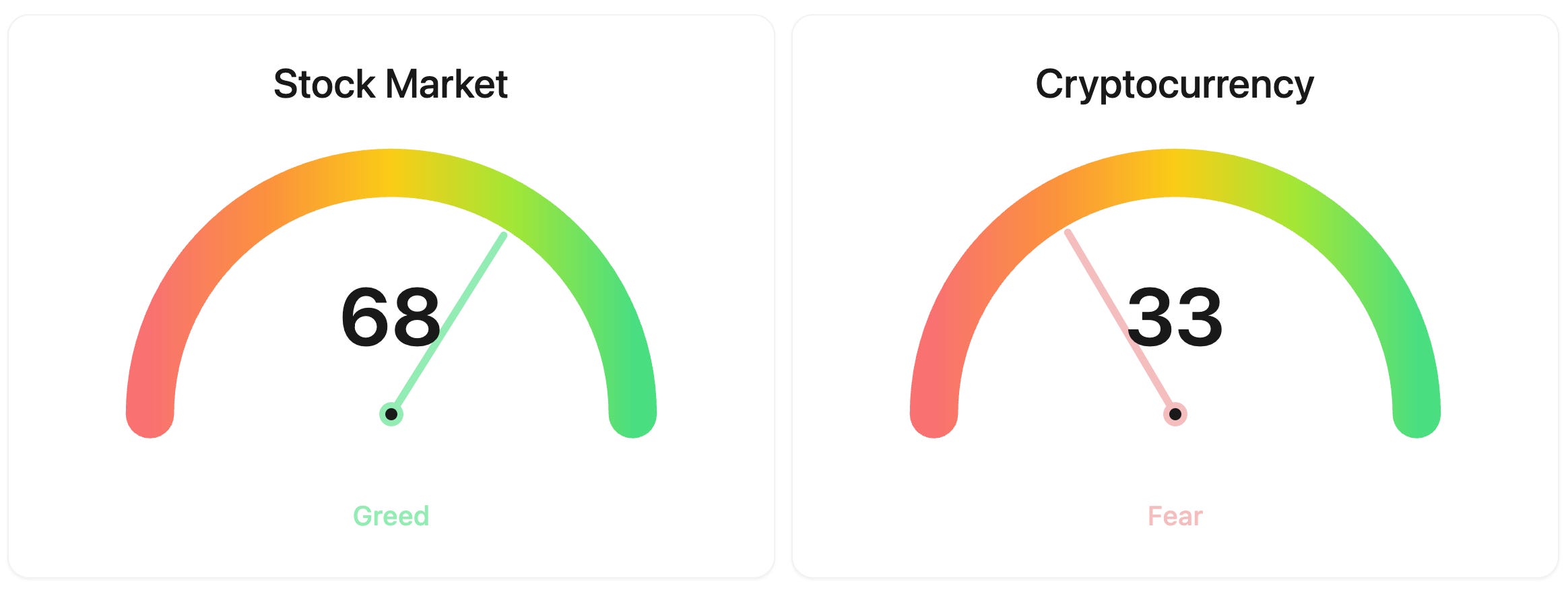

⚖️ Fear & Greed

📉 The Number That Matters

76%

CF Industries stock is up 76% this year, and that 76% gain reflects one simple bet: with Gulf fertilizer cargoes stuck behind Hormuz, US producers like CF own the supply, and traders are paying up early before food inflation flows through.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $76394 (▼ -1.30%)

Ethereum (ETH): $2279 (▼ -1.12%)

XRP: $1.38 (▼ -1.26%)

Equity Indices (Futures):

S&P 500: $7131 (▼ -0.59%)

NASDAQ 100: $27090 (▼ -1.28%)

FTSE 100: £10325 (▲ 0.04%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.37% (▲ 0.60%)

Oil (WTI): $100 (▲ 3.19%)

Gold: $4599 (▼ -1.77%)

Silver: $73.65 (▼ -2.45%)

Data as of: UK (GMT) 13:50 / US (EST): 08:50 / Asia (Tokyo): 22:50

✅ 5 Things to Know Today

🇯🇵 BoJ holds, three votes short of a hike

The Bank of Japan kept its policy rate at 0.75% overnight, but the vote split 6-3, with three board members backing an immediate move to 1%. That’s the most hawkish dissent since Kazuo Ueda took the chair, and the third vote, Junko Nakagawa’s, was the surprise. Dollar-yen fell roughly 0.5% to 158.95, a meaningful move for a major currency on a no-action decision. The Nikkei 225 dropped more than 1%, with Advantest and SoftBank Group leading the slide after their recent rally. Bitcoin slipped 0.6% on the yen strength. Ten-year Japanese government bond yields held flat at 2.47%, already at multi-decade highs. Money markets immediately shifted to price the June 16 meeting as a live event. (CNBC)

The bigger surprise was buried in the quarterly outlook. The Bank of Japan lifted its fiscal 2026 core inflation forecast to 2.8% from 1.9%, a much sharper upward revision than economists expected, citing pass-through from elevated crude prices. It simultaneously cut growth forecasts to 0.5% from 1%, a stagflationary combination that boxes Ueda in. There’s a calendar wrinkle the market just zeroed in on: Nakagawa’s term ends June 29, and her replacement Ayano Sato is materially more dovish. The June 16 meeting is effectively Nakagawa’s last chance to vote for a hike, which makes that decision the real event. Spring wage talks delivered roughly 5% pay rises, the wage-price cycle is running, and the BoJ’s own estimate of neutral rates sits near 1.5%. Seventy-five basis points of tightening still need to land.

Sensei’s Insight: The headline call was the consensus. The real news was the inflation forecast jump and Nakagawa’s last hawkish vote landing in June before her dovish replacement arrives. June 16 is now the live meeting. Watch dollar-yen at 158 through Ueda’s press conference today.

🇦🇪 UAE quits OPEC after nearly 60 years

The UAE announced today it will leave OPEC and the broader OPEC+ alliance on May 1, ending nearly six decades of membership and dealing the most serious blow to the cartel since Qatar’s 2019 exit. The decision was framed by state news agency WAM as a response to changing global demand and a “comprehensive review” of UAE production policy, but the political subtext is harder. UAE diplomatic adviser Anwar Gargash criticized fellow Gulf and Arab states yesterday for failing to defend the country during Iranian attacks during the war, calling their political and military response “the weakest historically.” The statement landed as OPEC+ prepared to meet in Vienna tomorrow. (Bloomberg)

For retail investors, the move cuts both ways. The UAE has built significant idle production capacity that it has long chafed at being unable to fully use under OPEC quotas. Outside the cartel, it’s free to ramp up. That’s potentially price-negative if the war ever ends and that spare capacity hits the market. In the short run, however, it’s destabilizing: Saudi Arabia loses its most important Gulf partner inside the bloc exactly as the Strait of Hormuz remains effectively shut. Trump, who has long accused OPEC of “ripping off the rest of the world” and linked US military protection of the Gulf to oil prices, scored a notable diplomatic win. Tomorrow’s Vienna meeting just got significantly more complicated.

Sensei’s Insight: This is the first real crack in OPEC+ since the bloc was formed in 2016. Outside the cartel, UAE is free to monetize whatever spare capacity it holds. A protracted Saudi-UAE rivalry could mean cheaper oil eventually, but expect chaos first as Vienna scrambles to hold what’s left of the alliance together.

🇪🇺 Brussels takes aim at Gemini’s Android moat

The European Commission yesterday published draft measures forcing Google to give rival artificial intelligence (AI) assistants the same Android privileges that its own Gemini enjoys. That includes system-level voice activation, screen reading, and the ability to act on installed apps to send emails, order food, or share photos. The proposal lands the day before Alphabet reports earnings on Wednesday. Public consultation closes May 13, with a final decision due by end of July. Non-compliance under the Digital Markets Act, the European Union’s competition rulebook for big-platform “gatekeepers,” carries fines of up to 10% of global revenue, which on Alphabet’s $400-billion-plus 2025 base translates to a theoretical $40 billion ceiling. (Bloomberg)

Timing matters because Gemini just completed its takeover as the default AI on more than two billion Android devices last month, replacing Google Assistant. If Brussels gets its way, that distribution moat thins out exactly as Alphabet commits roughly $175 to $185 billion in 2026 capital expenditure to AI infrastructure. The read-across is clean. Any AI rival that scales on Android, including OpenAI, Anthropic, and Perplexity, picks up an addressable market it currently has to fight for app by app. Microsoft, which holds the largest stake in OpenAI, becomes a structural beneficiary if European users get true assistant choice on the device.

Sensei’s Insight: This is the second time in a month Brussels has hit Google, after April’s search data sharing order. The pattern is full-spectrum unbundling of Alphabet’s distribution power. Tomorrow’s earnings call will be the first time Sundar Pichai addresses it on the record.

🛢️ Brent tops $111 as Iran’s proposal falls flat

Brent crude pushed above $111 a barrel this morning, its highest level since March, even after Iran sent the US a fresh proposal through Pakistani mediators offering to reopen the Strait of Hormuz in exchange for deferring nuclear talks. The offer didn’t move the market the way Tehran would have wanted. Trump was reportedly dissatisfied with the terms, and the White House has signaled skepticism while preparing counteroffers in the coming days. Brent is up roughly 13% in a week, after closing below $100 last Tuesday. West Texas Intermediate (WTI) is near $97. Roughly 20 million barrels per day of crude, fuels, and petrochemicals are still affected by the blockade, according to consultancy Lipow Oil Associates. (CNBC)

The Iran-via-Pakistan proposal was the cleanest diplomatic opening in two months, and it failed to ease prices. That tells you something about how the market is now pricing time. Goldman Sachs raised its forecasts on Sunday and warned a worst-case scenario could push Brent to $120. The International Energy Agency still calls this the largest supply shock in oil-market history. Energy producers, oilfield services, and tankers continue to benefit; airlines, chemicals, and consumer-discretionary remain on the wrong side of the trade. American Airlines already cut its full-year guidance last week to a 40-cent loss to $1.10 in earnings per share, down from $1.70 to $2.70 in January.

Sensei’s Insight: When a peace offer pushes oil higher, the market has stopped listening to negotiators. Watch the next 48 hours. Trump’s response will either confirm a deal is close enough to take $5 off the price, or extend the blockade and lock in $110 as the new floor.

🌾 Hormuz blockade squeezes the world’s fertilizer supply

The Strait of Hormuz blockade has crossed from oil into food. Roughly 35% of globally traded urea, the most-used nitrogen fertilizer, comes from the Middle East, and Gulf producers can’t load ships. India, the world’s largest urea importer, just paid $935 per ton on its west coast and $959 on the east in its latest tender, nearly double what it paid two months ago. Yesterday Indian Potash issued a separate tender for 1.6 million tons of phosphate fertilizers (DAP and TSP) on behalf of the country’s whole industry, and an Indian buyer is in the market today for ammonia at prices that recently touched $1,000 a ton. (Bloomberg)

Fertilizer prices feed into food prices on a 6 to 12 month lag, which puts the real exposure on Q4 grain harvests and 2027 consumer staples earnings. CF Industries, the largest US nitrogen producer, is up roughly 76% year-to-date, riding the structural advantage of operating outside the disruption zone with cheap US natural gas. Mosaic, Nutrien, and Yara are similarly placed. The losers are downstream consumer brands and emerging-market governments that subsidize fertilizer; ratings agency Crisil estimates India’s subsidy bill could rise by ₹20,000 to ₹25,000 crore (roughly $2.4 to $3 billion) if disruption persists.

Sensei’s Insight: Oil gets the headlines, but fertilizer is the quiet trade that has already moved real money. CF’s 76% run isn’t speculation. It’s traders pricing in months of structural advantage. If Hormuz stays shut into June, food inflation comes back into the rate-cut conversation.

Stories You Might Have Missed

🇻🇪 Big Oil dusts off rigs as Venezuela reopens

Oilfield service companies are physically pulling drilling rigs out of long-term storage in Venezuela, the strongest signal yet that capital is committing to the country’s post-Maduro reset. At least nine rigs have come out of warehouses in recent weeks, with five more under technical assessment. Venezuela’s oil ministry is targeting 1.37 million barrels per day of production by year-end, up from 1.1 million currently. Chevron has tripled its Venezuelan exports since December and just lifted its Petroindependencia stake to 49%. Halliburton said on its earnings call last week it’s been discussing commercial terms for Venezuela operations; SLB called the country an “exciting growth opportunity.” With the world’s largest crude reserves slowly coming back to market, watch the oilfield services names. (Bloomberg)

💰 Kuwait pipeline bids land amid war damage

Today is the bidding deadline for a roughly $7 billion stake in Kuwait Petroleum Corporation’s crude oil pipeline network. JPMorgan, HSBC, National Bank of Kuwait, and Kuwait Finance House are arranging a $6 billion financing syndicate to back the buyers, with bidders including BlackRock’s Global Infrastructure Partners, Brookfield, EIG, KKR, Macquarie, and Stonepeak. The wrinkle is that Kuwait Petroleum reported “severe material damage” at some operating units after Iranian drone attacks during the conflict. The deadline was already pushed from April 7 after bidders asked for more time to assess war risk. Today’s outcome is a real-time gauge of how seriously global infrastructure capital is taking the Strait of Hormuz risk premium, with Saudi Aramco’s planned $4 billion gas-plant sale teed up next. (Bloomberg)

🏦 India tightens bank loan rules to global standards

The Reserve Bank of India finalized its long-anticipated Expected Credit Loss framework yesterday, with implementation locked in for April 1, 2027. Indian banks will move from setting aside money after losses become visible to estimating future losses upfront across three risk stages. The RBI declined banks’ requests for softer floors, keeping Stage 2 provisions at 5% versus the roughly 0.4% lenders typically book today. State-run banks with thinner contingency buffers face the largest provisioning hit, while private-sector banks like HDFC and ICICI are better positioned. The two-year runway is meant to soften the transition, but expect Indian bank earnings to absorb the impact in fiscal 2027 and 2028. (Bloomberg)

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

📈 Chart of the Day: Crude Oil

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.