Morning Forecast: Tuesday 30 June

XRP’s quiet reset: Leverage has drained out and network usage jumped 72%, even as a strong dollar keeps the price stuck just above $1.

👀 Today’s Stories at a Glance

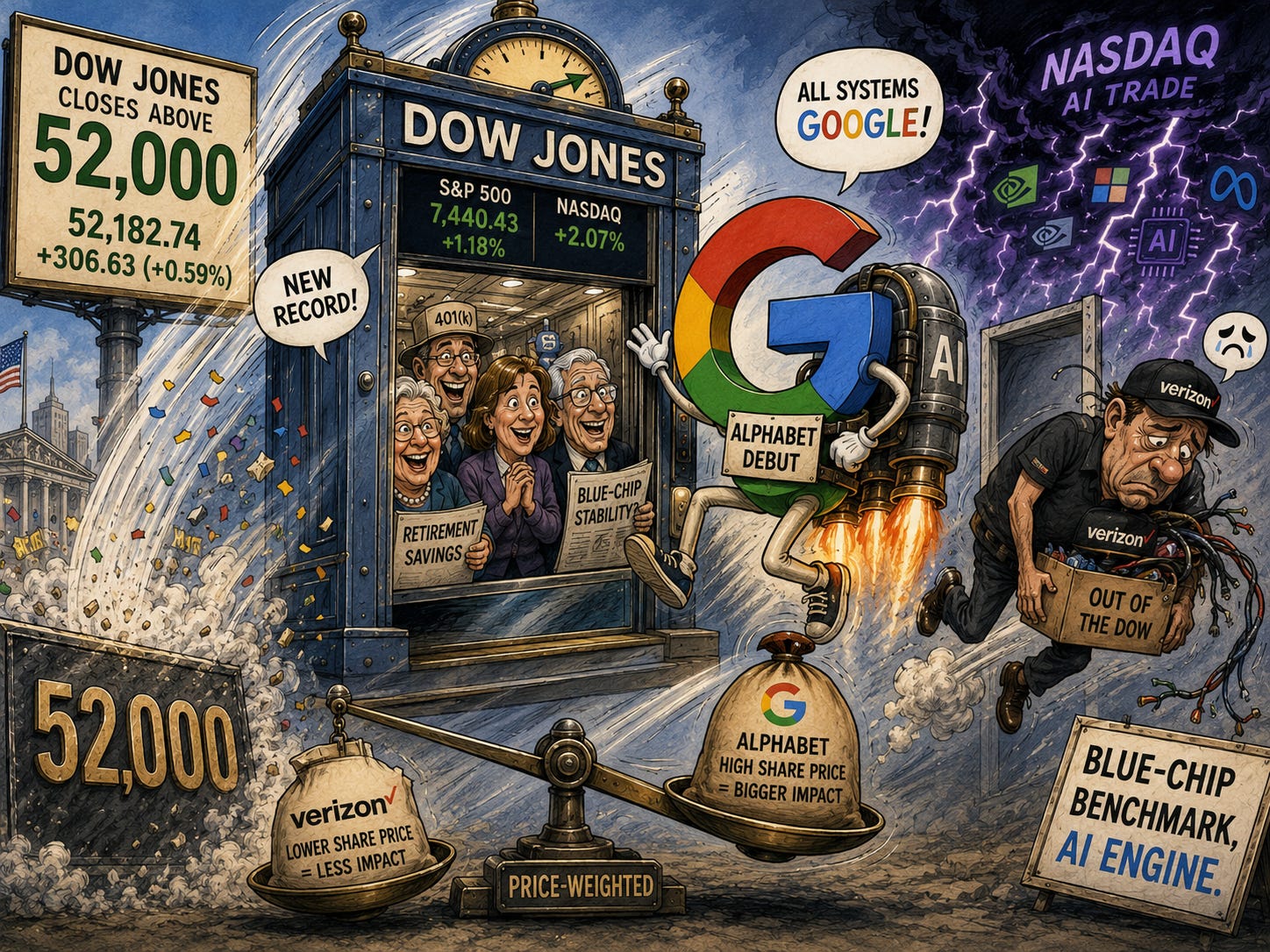

📈 The Dow tops 52,000 with a new face: Alphabet replaces Verizon in the blue-chip index on the day it first closes above 52,000, tying the Dow tighter to the AI trade.

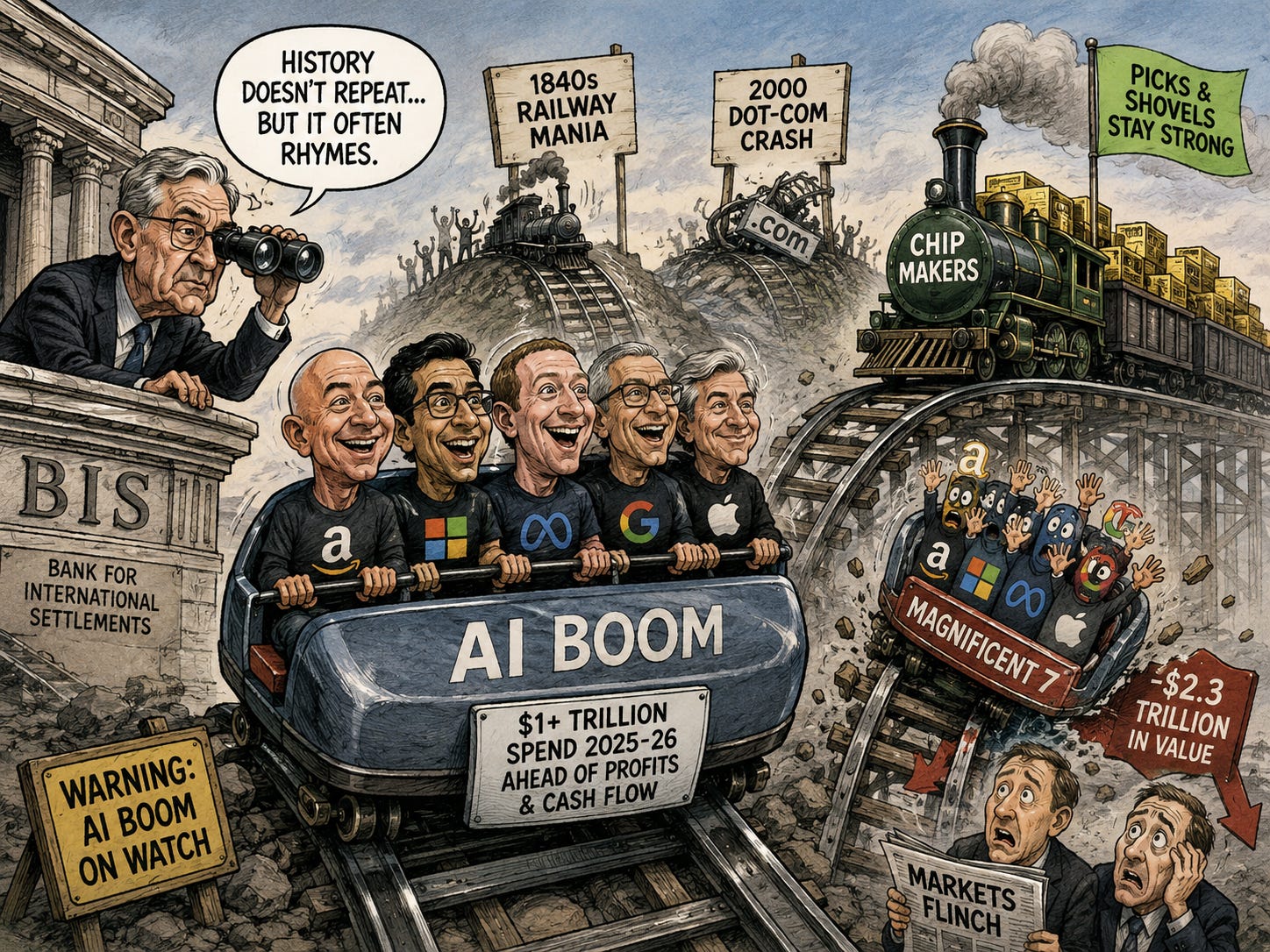

🤖 AI’s watchdogs sound the alarm: The central bank of central banks warns a $1 trillion AI spending boom could end in a crash, just as the Mag 7 sheds $2.3 trillion.

🏛️ Supreme Court walls off the Fed: Justices block Trump from removing Governor Lisa Cook for now, defending central-bank independence even as they widen his firing power elsewhere.

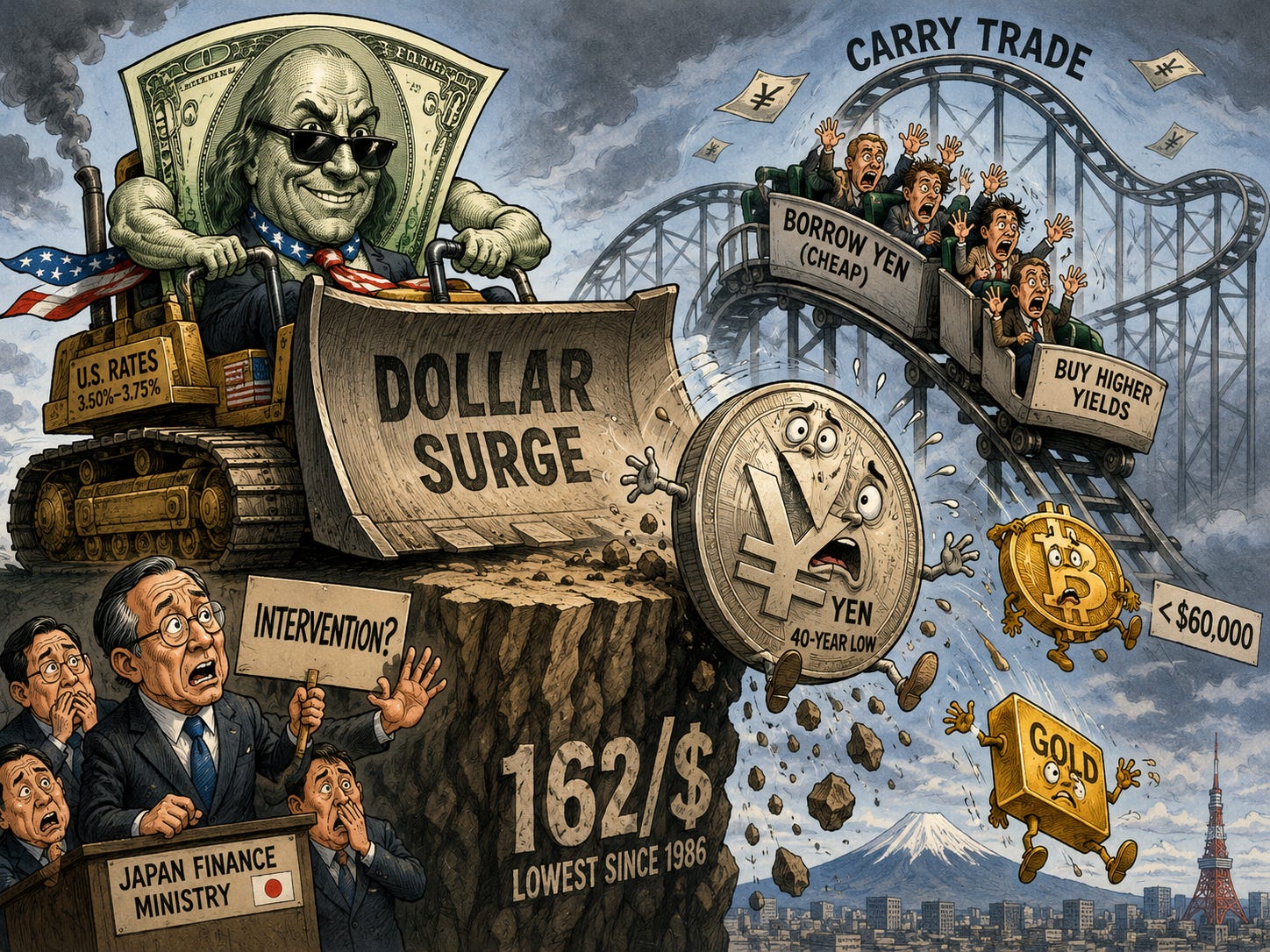

💵 Yen sinks to 1986 lows: A surging dollar drives the Japanese yen past 162, its weakest in 40 years, keeping a lid on crypto and risk despite Tokyo’s warnings.

🍺 Constellation pours its numbers tonight: The Corona and Modelo brewer reports after the close, with soft beer sales, aluminium tariffs and its full-year outlook all in focus.

💻 Taiwan raids Super Micro: Prosecutors search the server maker over alleged Nvidia chip smuggling into China, and the shares fall as much as 9%.

🇰🇷 South Korea bets $518 billion on chips: Samsung and SK Hynix anchor a vast new push into AI memory, though investors fret that fresh capacity could bring oversupply.

🛢️ Oil heads for its worst quarter since 2020: Brent near $73 caps a brutal three months, down more than 20%, as the US and Iran resume talks in Doha.

🔍 Deep Dive: XRP’s quiet reset: Leverage has drained out and network usage jumped 72%, even as a strong dollar keeps the price stuck just above $1.

📈 Chart of the Day: Sensei’s chart and the key levels worth watching.

🧠 One Big Thing

The day’s two biggest stories are really one. Alphabet’s entry into the price-weighted Dow ties the index that anchors a lot of retirement money far tighter to the AI trade, on the very day the Bank for International Settlements warns that the $1 trillion AI spending boom could end in a crash. So the safest-sounding benchmark in finance is leaning into AI exactly as the people who police bubbles lean away from it. For investors the takeaway is concentration: more of your passive money now rides on a handful of AI names, in the Dow as well as the Nasdaq. Watch whether Warsh picks up the BIS worry when he speaks at Sintra tomorrow.

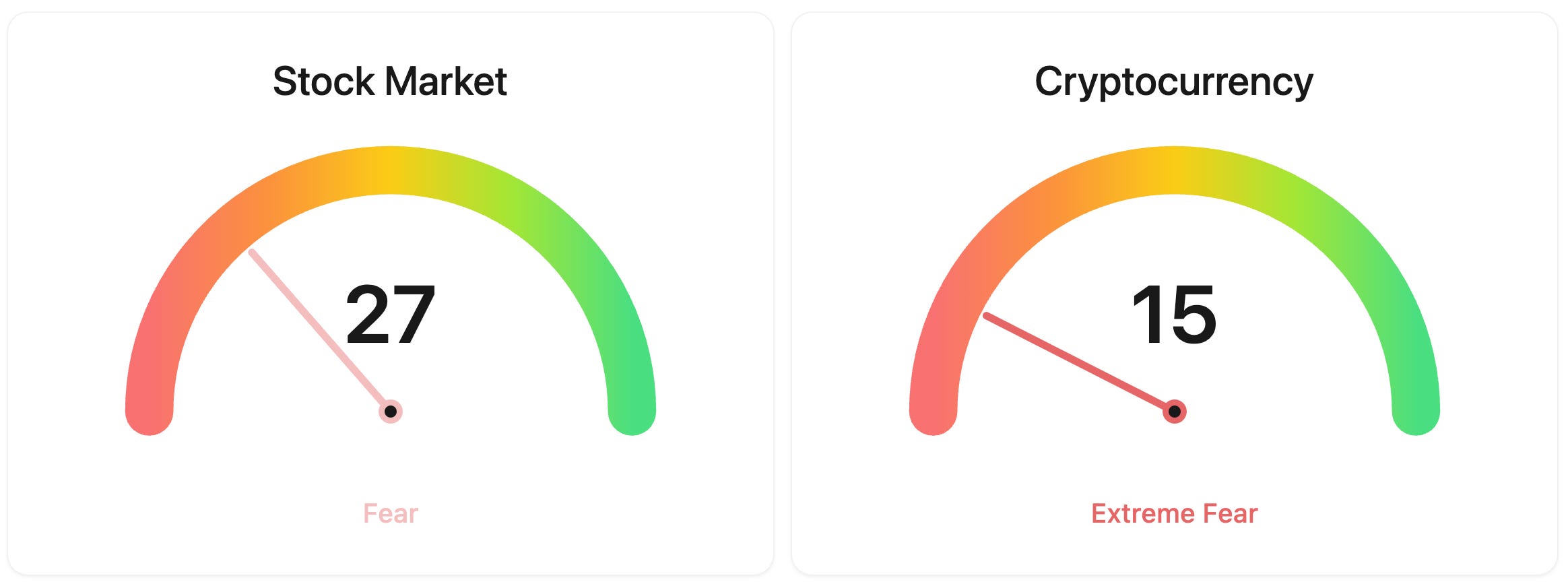

⚖️ Fear & Greed

📉 The Number That Matters

$2.3 trillion

The value erased from the Magnificent 7 as investors question the payoff from heavy AI spending, even as money keeps flowing into the chipmakers underneath them.

⚔️ Winners vs Losers

Winners

AVAV 0.00%↑: AeroVironment shares surged after the drone maker reported fiscal Q4 results that crushed estimates, posting record revenue of $641.6 million and adjusted EPS of $1.84 against roughly $1.47 expected, with backlog growing to $1.2 billion. Management framed defense demand as unprecedented heading into the next two years, even as it flagged that free cash flow may stay negative until after fiscal 2027.

BOT 0.00%↑: RoboStrategy, the newly listed closed-end fund that gives public investors exposure to private robotics and physical-AI companies such as Figure AI and Apptronik, extended its post-listing momentum run as enthusiasm for the robotics theme and a steady cadence of capital raises kept demand running ahead of its small public float.

ENPH 0.00%↑:Enphase Energy led a broad residential-solar rally as installers raced to lock in projects before the July 4 commercial investment tax credit safe-harbor deadline, pulling demand forward across the inverter makers. Fellow inverter maker SolarEdge ($SEDG +11.48%) moved in lockstep on the same catalyst.

NRGV 0.00%↑: Energy Vault caught the clean-energy bid alongside solar peers, helped by battery storage’s exemption from the looming solar tax-credit deadline and by the imminent July 1 start of Phase 1 operations at its first fully owned storage asset.

JACK 0.00%↑: Jack in the Box rallied on forced index buying tied to its inclusion in several FTSE Russell benchmarks during the June reconstitution, building on a stock that had already been running on short-covering and meme-driven momentum the prior week.

Losers

UNCY 0.00%↑: Unicycive Therapeutics collapsed after disclosing a second Complete Response Letter from the FDA for its kidney-disease drug oxylanthanum carbonate, again tied to unresolved deficiencies at a third-party manufacturing vendor rather than the drug’s safety or efficacy, with no facility re-inspection having taken place during the review.

CNXC 0.00%↑: Concentrix slid after the customer-experience services firm cut its full-year outlook alongside Q2 results, guiding fiscal 2026 adjusted EPS to roughly $11 at the midpoint against about $12 expected and trimming its revenue forecast, overshadowing in-line quarterly numbers and a jump in AI-driven bookings.

NVCT 0.00%↑: Nuvectis Pharma dropped after launching an underwritten public stock offering, a dilutive capital raise that landed just days after an ex-China licensing deal with Haisco had sent the shares sharply higher and prompted a string of analyst price-target increases.

VSH 0.00%↑: Vishay Intertechnology extended its pullback from a parabolic run that had lifted the passive-components and discrete-semiconductor maker more than 200% over the past year, as a high-beta unwind and a more hawkish Fed repricing weighed on rate-sensitive chip names.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $59,222 (▼ 1.57%)

Ethereum (ETH): $1,580 (▼ 1.87%)

XRP: $1.04 (▼ 1.71%)

Equity Indices (Futures):

S&P 500: 7,514 (▲ 0.18%)

NASDAQ 100: 30,148 (▲ 0.32%)

FTSE 100: 10,605 (▲ 0.87%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.38% (▲ 0.18%)

Oil (WTI): $71 (▲ 0.85%)

Gold: $4,031 (▲ 0.39%)

Silver: $58.97 (▲ 1.21%)

Data as of: UK: 12:52pm BST / US: 7:52am EDT / Asia (Tokyo): 8:52pm JST

✅ 5 Things to Know

📈 Alphabet joins the Dow as it tops 52,000

The Dow Jones Industrial Average closed above 52,000 for the first time yesterday, up about 0.6% on the day, and it did so with a new member: Alphabet, Google’s parent, took its place in the 30-stock index, replacing Verizon. Alphabet jumped around 5% on its debut as a Dow component, and its arrival capped a broad rebound, with the S&P 500 up 1.2% to 7,440 and the Nasdaq adding about 2%, both snapping a five-day losing streak after a rough run for technology shares (Yahoo Finance).

The swap matters more than the milestone. The Dow is price-weighted, so a stock’s pull on the index comes from its share price, not the company’s size. Alphabet trades in the mid-$330s against Verizon’s far lower share price, which hands it roughly 4% of the index versus Verizon’s 0.5%, instantly making it one of the Dow’s biggest movers (CNBC). That ties the blue-chip benchmark, which a lot of retirement money tracks, far tighter to the same AI trade that drives the Nasdaq. With Alphabet in, the five most valuable US tech names now all hold Dow seats, and the index rises and falls with AI sentiment more than it ever has.

Sensei’s Insight: The Dow used to be where you hid from tech. Not any more. A price-weighted quirk means Alphabet now swings it about eight times harder than Verizon did, so the benchmark behind a lot of pension money just became an AI bet in disguise.

🤖 The world’s central banks put the AI boom on watch

The Bank for International Settlements, the institution that acts as a bank for the world’s central banks, used its annual report this week to warn that the boom funding artificial intelligence could end in a market crash. It singled out the five largest cloud companies, on track to spend more than $1 trillion on AI across 2025 and 2026, an outlay now running ahead of their combined profits and free cash flow. The Basel-based body compared the moment to the railway mania of the 1840s and the dot-com crash of 2000, each a genuine breakthrough that drew in more money than returns could ultimately justify (Fortune).

The warning lands as the market is already flinching. AI and financial stability is a panel topic at the European Central Bank’s Sintra forum today, and Fed Chair Kevin Warsh shares that stage tomorrow, so the institutions that usually wait for a bubble to burst are flagging this one early. The strain is visible in prices: the Magnificent 7, the megacap group that drives roughly a third of the S&P 500, has shed about $2.3 trillion in value as investors question whether the AI spending will pay off, even as money keeps flowing into the chipmakers selling the picks and shovels (CNBC).

Sensei’s Insight: When the BIS reaches for railway-mania and dot-com comparisons, it is flagging the mechanism, not the timing. What I am watching is the split: if chip names hold while the megacaps wobble, the market is repricing AI’s bill, not walking away from the trade.

🏛️ The Supreme Court draws a line around the Fed

The Supreme Court ruled yesterday that President Trump cannot remove Federal Reserve Governor Lisa Cook for now, letting her keep her seat while the legal fight over her firing plays out. Trump had moved to dismiss her over mortgage-fraud allegations she denies. The decision was procedural rather than final: by 5-4, the justices refused to lift a lower-court order protecting Cook, so the case continues without settling whether a president can ever remove a Fed governor. The majority crossed the usual lines, with Chief Justice John Roberts and Justice Brett Kavanaugh joining the three liberal justices, while on the same day the Court let Trump dismiss a Federal Trade Commission member, singling out the Fed as the exception (CNBC).

For markets, the question all along was whether the White House could get its hands on interest-rate policy. Had Cook been removed, the President could have moved toward a friendlier majority on the Fed’s seven-seat board, so the ruling shuts that door for now and stands as the firmest signal yet that the courts will guard central-bank independence. Bonds barely moved, because traders had largely expected this, with Treasury yields holding steady. That throws the focus back onto the data, starting with the jobs report later this week, as the next real driver of where rates go.

Sensei’s Insight: The same Court that just widened the President’s power to fire agency heads drew one line, and it drew it around the Fed. Rate policy stays walled off from the White House for now. The market saw it coming, which is why bonds shrugged rather than rallied.

💵 The dollar’s surge drives the yen to a 40-year low

The Japanese yen fell past 162 per dollar today, its weakest level since 1986, as a powerful dollar overran repeated warnings from Tokyo. It broke through 161.95, the line that triggered direct intervention by Japanese authorities back in July 2024, and finance ministry officials again said they stood ready to act against speculative moves. The gap driving it is simple: the Bank of Japan lifted its rate to 1% this month, the highest since 1995, while US rates sit at 3.50% to 3.75%, leaving the yen the favoured funding currency for global carry trades (Yahoo Finance).

A dollar this strong is a headwind for almost everything priced against it. Bitcoin has slipped back below $60,000, pressured by the same surge even as US spot ETFs keep bleeding cash, and gold sits well off its highs. The risk that reaches everyone is the carry trade: investors borrow cheap yen to buy higher-yielding assets worldwide, and a sudden snap-back in the currency can force them to sell all at once, as it did in August 2024. Watch whether Tokyo moves from words to actual intervention, because that is the trigger that could ripple far beyond Japan.

Sensei’s Insight: The yen is the market’s quiet pressure gauge. While the dollar grinds higher, crypto and gold struggle to rally on their own merits, no matter how good their internals look. A move to real intervention from Tokyo is the wildcard that could loosen that grip.

🍺 Constellation Brands pours its numbers after the close

Constellation Brands, the US company behind Corona, Modelo and Pacifico, reports first-quarter results after the market closes today, and the print doubles as a read on the American consumer. Imported beer is the engine, so the tariffs on Mexican imports that squeezed margins last quarter sit firmly in view, alongside whether management holds its full-year guidance. Analysts expect earnings of about $3.28 a share, up 1.9% from a year ago, on revenue near $2.4 billion, a fall of roughly 3.9% as beer sales soften and the wine and spirits arm struggles (Yahoo Finance).

The figure to watch is depletions, the rate at which beer actually sells through to drinkers, because it shows real demand rather than shipments into warehouses. Softer recent sales have been pinned on higher fuel costs and poor weather, with the summer selling season and the 2026 World Cup expected to help. For investors the bigger question is guidance: a company this exposed to imported beer and aluminium is a live test of whether import duties land on companies or on customers. A confident outlook would calm nerves, while a cut would suggest the consumer is starting to pull back.

Sensei’s Insight: Beer is a defensive business until tariffs hit the can. Constellation is one of the cleanest gauges of where import duties are landing, so the guidance matters far more than the quarter just gone. I am watching the full-year number, not the headline beat.

Stories You Might Have Missed

💻 Taiwan raids Super Micro in a chip-smuggling probe

Super Micro shares fell as much as 9% yesterday after Taiwanese prosecutors raided the server maker’s local offices, widening an investigation into whether its machines were used to route restricted Nvidia AI chips into China. The Keelung District Prosecutors Office also searched three affiliated firms and six homes, alleging a scheme to funnel about $2.5 billion of Nvidia-equipped servers through shell companies in Southeast Asia, the latest turn after US charges against a Super Micro co-founder earlier this year. The company says it is cooperating and has not been charged. The probe lands on an already-shaky stock, with quarterly earnings due early in August, and it is a reminder that the export controls around AI chips are now being enforced hard (Bloomberg).

🇰🇷 South Korea bets $518 billion on the chip race

South Korea unveiled an 800 trillion won plan, about $518 billion, to expand its semiconductor and AI industry, anchored by new Samsung Electronics and SK Hynix fabrication plants and announced alongside President Lee Jae Myung. The two firms produce roughly two-thirds of the world’s memory chips, including the high-bandwidth memory that AI systems depend on, so the build-out matters for the whole AI hardware chain, from Nvidia down to the data centres. The market reaction was wary rather than celebratory: investors worry that too much new capacity arriving at once could tip the memory market back into oversupply, just as today’s chip prices are booming (CNBC).

🛢️ Oil heads for its worst quarter since 2020

Brent crude slipped toward $73 a barrel and US crude trades near $70, leaving oil on course to end the quarter down more than 20%, its steepest quarterly fall since the 2020 demand collapse, as supply floods back through the Strait of Hormuz. Cheaper crude is a relief for drivers and a quiet drag on inflation, but the calm rests on a fragile ceasefire, and any flare-up near Hormuz could send prices straight back up. US and Iranian officials are due to resume technical talks in Doha today, part of a 60-day roadmap toward a final deal, even after fresh weekend clashes showed how easily it could unravel (CNBC).

🔍 Deep Dive - XRP’s Quiet Reset: Falling Leverage, Rising Usage, and a Price That Has Not Caught Up

XRP looks boring on the chart, stuck just above $1 after a 19% slide on the month. Underneath that flat price, two things moved hard in opposite directions. The leverage that powered the rally and then the selloff has drained out, and real network usage jumped 72% in two weeks. When speculation deflates while actual usage climbs, you are usually looking at a base being built, even if the candles do not show it yet.

What actually happened

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.