Morning Forecast: Tuesday 7 July

SpaceX joins the Nasdaq-100 as Samsung’s record profit sends its shares lower

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

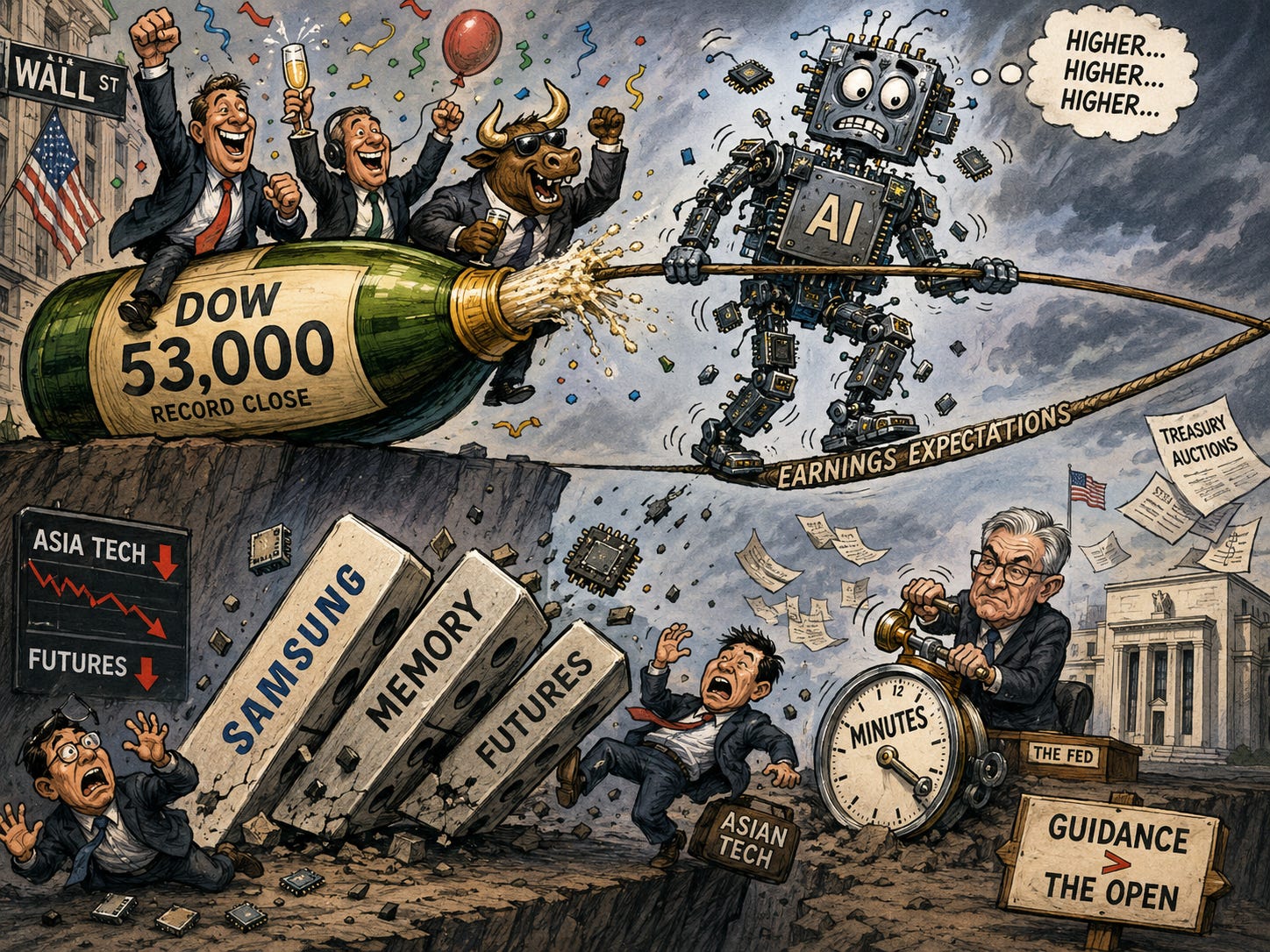

📉 Wall Street’s record wobble: the Dow closed above 53,000 for the first time yesterday, but chip doubt returned overnight and futures slipped before the open.

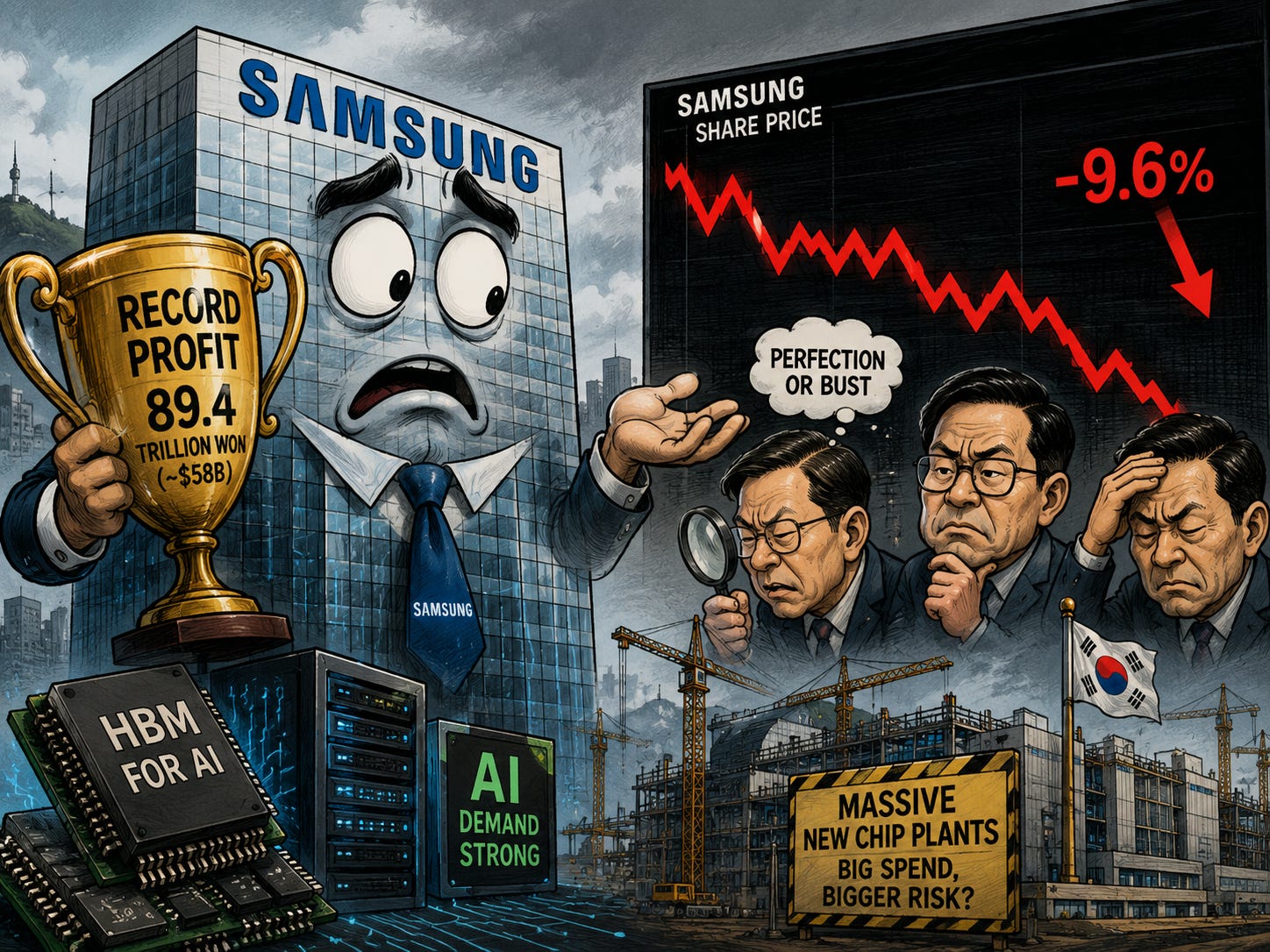

💾 Samsung’s record falls flat: operating profit jumped 1,810% to an all-time high, yet the shares dropped about 9.6% on renewed fears over AI spending.

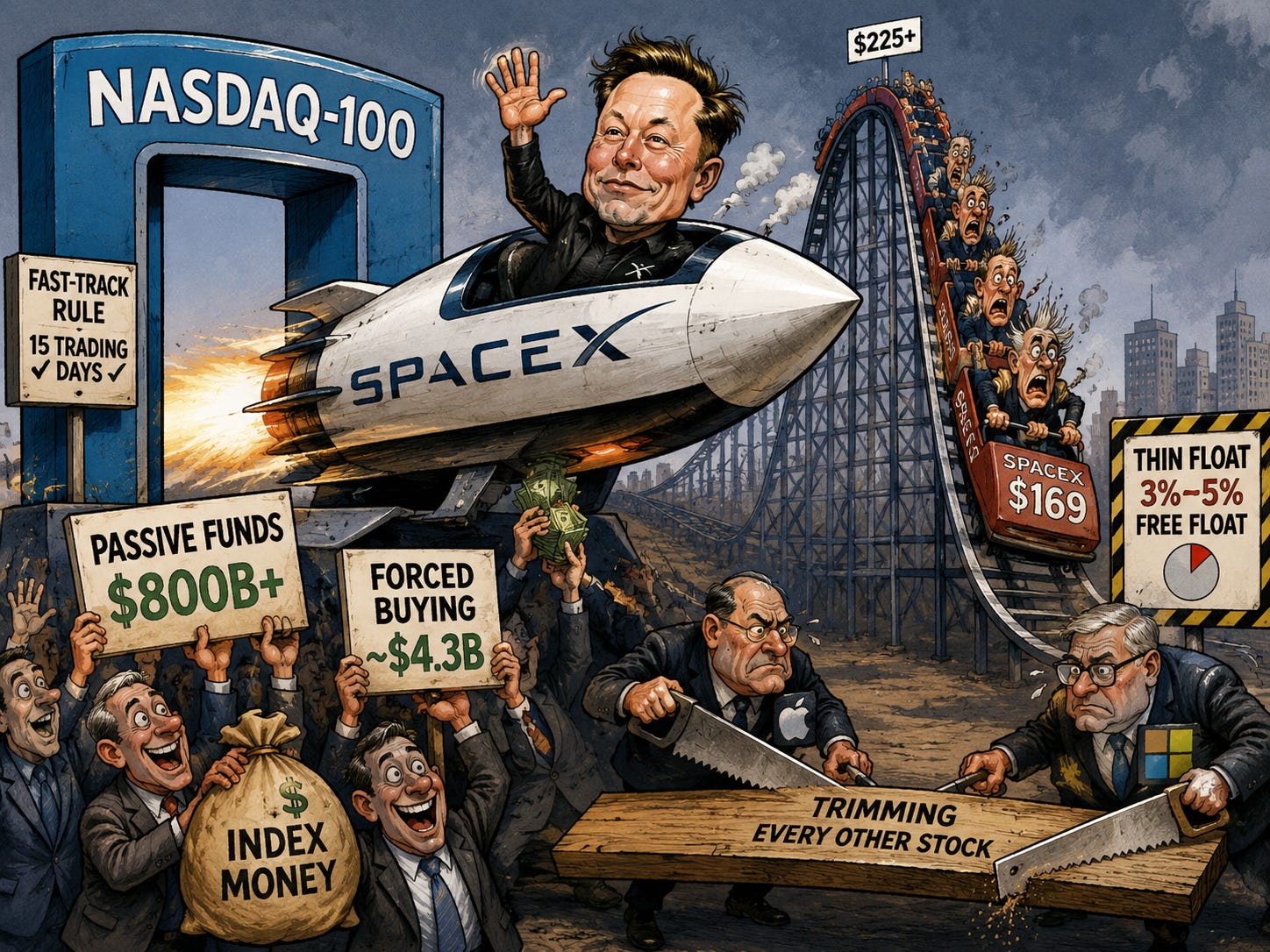

🚀 SpaceX enters the Nasdaq-100: the inclusion takes effect today, forcing roughly $4.3 billion of passive buying, though history warns index entry often marks a peak.

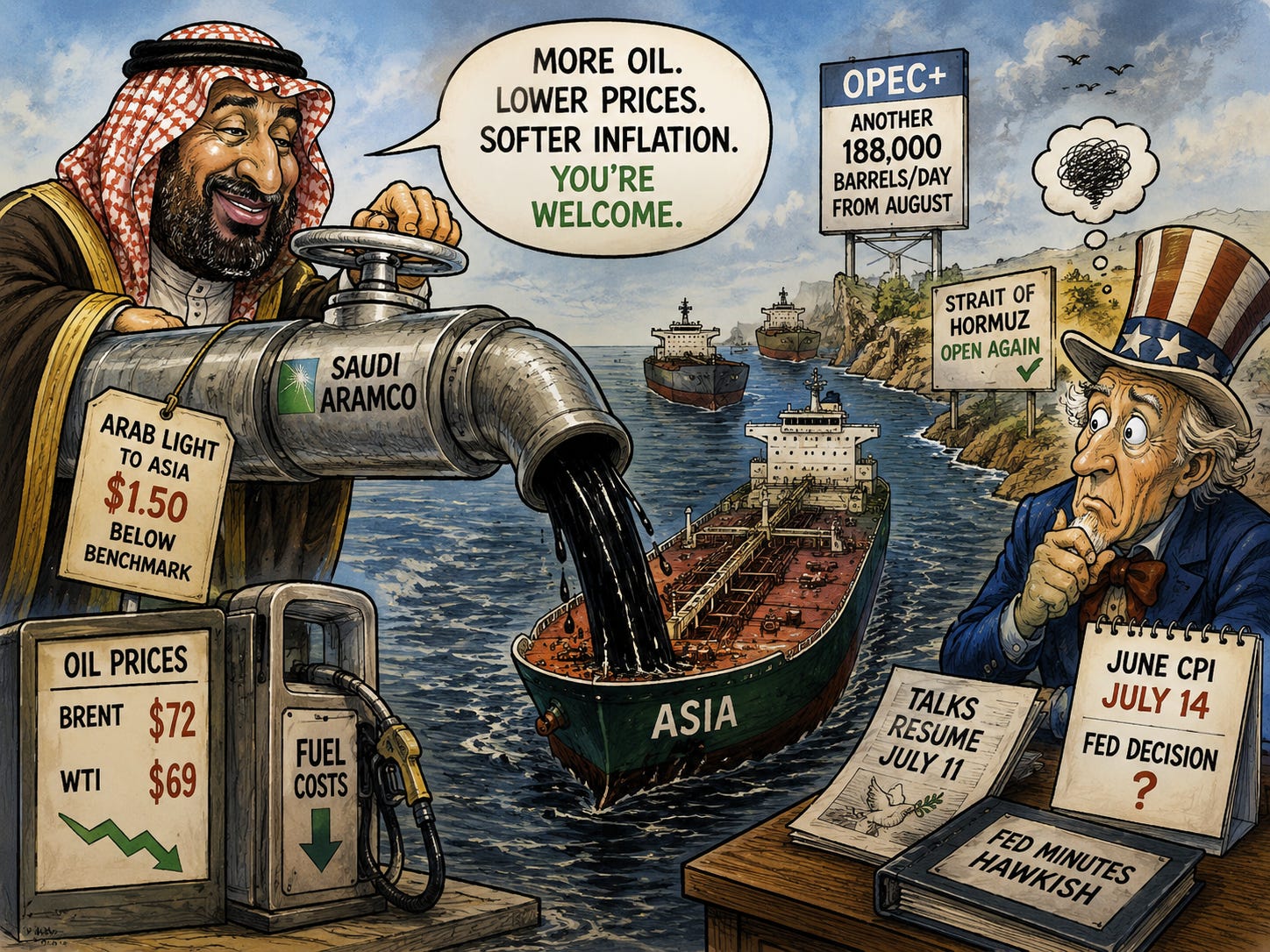

🛢️ Saudi Arabia slashes crude prices: the kingdom cut its August price to Asia by $11 a barrel, its steepest drop in more than two decades.

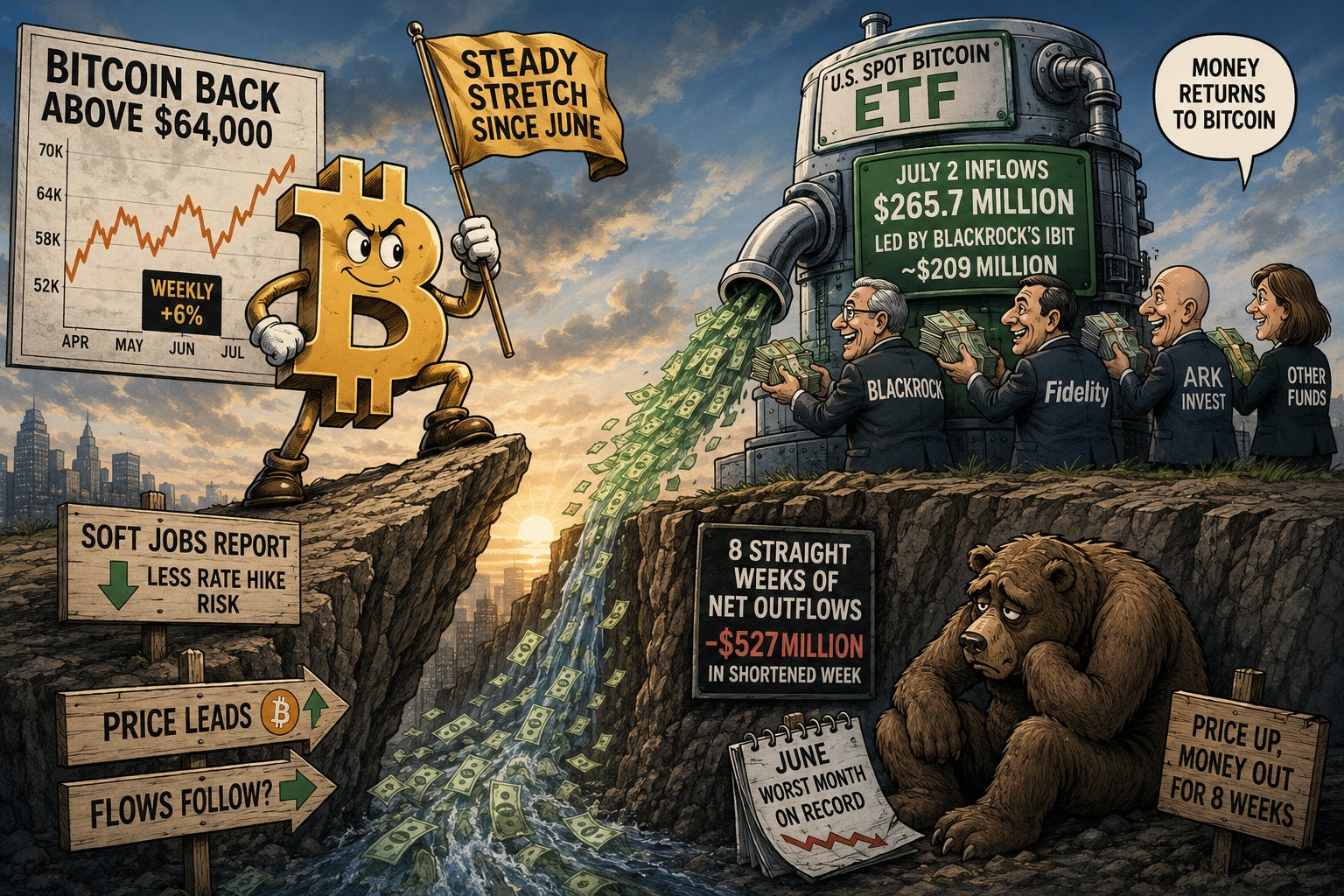

₿ Bitcoin’s flows finally turn: the coin held above $64,000 as spot ETFs drew their biggest daily inflow in a month, denting an eight-week outflow streak.

🏛️ The week’s real test is tomorrow: minutes from Warsh’s first Fed meeting land midweek, with services data steady at 54 and Treasury auctions all week.

🔬 Alphabet backs a fusion bet: Google’s parent and RWE funded German startup Proxima Fusion at a €2.4 billion valuation, chasing power for the AI era.

🥇 Gold slips ahead of the Fed: bullion eased around 0.8% to near $4,133 as traders paused before the minutes, still riding the softer rate outlook.

🧠 One Big Thing

While the market fixates on chips, the quieter force under this week is oil. Saudi Arabia just cut its Asian crude prices by the most in over two decades, OPEC+ keeps adding barrels, and the war premium is draining away with the Strait of Hormuz reopening. Cheaper energy feeds straight into cooler inflation, and it lands a week before June CPI and two weeks before the Fed decides. The minutes tomorrow will sound hawkish, because the meeting predates the weak jobs data, but falling oil may be doing the disinflation work the committee is still resisting. Watch Brent against the CPI print on the 14th.

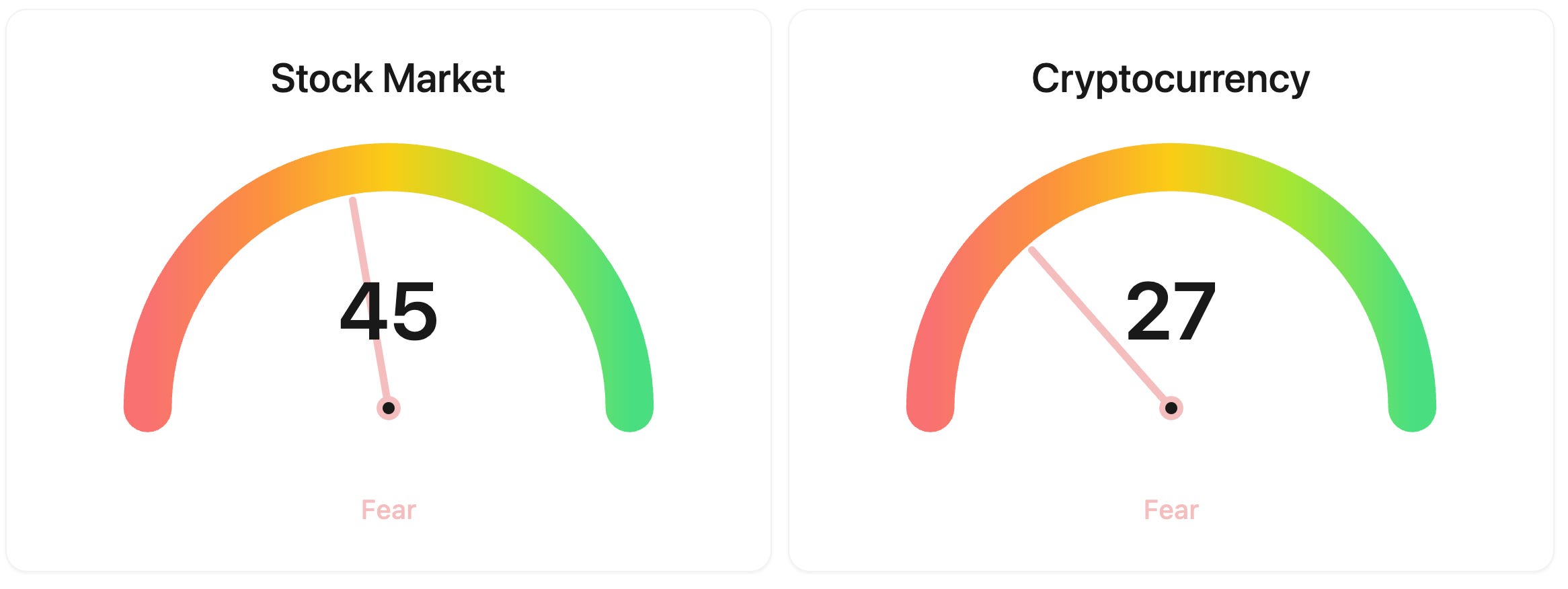

⚖️ Fear & Greed

📉 The Number That Matters

1,810%

Samsung’s operating profit jumped 1,810% from a year ago to a record 89.4 trillion won, yet its shares still fell about 9.6%, a sign the market now needs AI winners to beat expectations, not merely grow.

⚔️ Winners vs Losers

Winners

CRNX 0.00%↑: Crinetics Pharmaceuticals shares nearly doubled after Vertex Pharmaceuticals agreed to acquire the company for $85.00 per share in cash, adding endocrine drugs Palsonify and atumelnant to Vertex’s pipeline.

NOW 0.00%↑: ServiceNow shares rose as investors kept rotating out of semiconductors and into oversold enterprise software, with a recent Guggenheim upgrade to Buy and a run of AI partnership announcements reinforcing the bullish case.

Losers

SNDK 0.00%↑: Sandisk Corporation dropped alongside fellow memory maker Micron as the same semiconductor and memory-cost selloff pressured storage names.

MU 0.00%↑: Micron Technology slid on the sector-wide rotation out of memory and AI chip stocks, extending the group’s recent pullback.

MRVL 0.00%↑: Marvell Technology declined in sympathy with the broader semiconductor selloff.

LRCX 0.00%↑: Lam Research fell as chip-equipment makers were swept up in the same sector rotation.

AMAT 0.00%↑: Applied Materials dropped alongside other semiconductor equipment names on the sector pullback.

KLAC 0.00%↑: KLA Corporation slid with the rest of the chip-equipment group in the broad semiconductor selloff.

TER 0.00%↑: Teradyne fell in line with the sector-wide decline in semiconductor and chip-equipment stocks.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $63,144 (▼ -1.31%)

Ethereum (ETH): $1,775 (▼ -1.25%)

XRP: $1.12 (▼ -1.95%)

Equity Indices (Futures):

S&P 500: 7,574 (▼ -0.24%)

NASDAQ 100: 29,614 (▼ -1.09%)

FTSE 100: 10,677 (▲ 0.13%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.49% (▲ 0.45%)

Oil (WTI): $69 (▲ 0.80%)

Gold: $4,143 (▼ -0.52%)

Silver: $60.97 (▼ -1.82%)

Data as of: UK: 12:25 BST / US: 07:25 EDT / Asia (Tokyo): 20:25 JST

✅ 5 Things to Know

📉 Wall Street’s record runs into fresh chip doubt

The reopen rally carried Wall Street to another record. The Dow Jones Industrial Average closed above 53,000 for the first time yesterday, finishing at 53,055.91, while the S&P 500 added 0.72% to 7,537.43 and the Nasdaq Composite rose 1.12%, as beaten-down chip names rebounded and faith in the AI trade returned. The mood did not survive the night. Asian technology shares reversed sharply, Samsung and other memory makers fell, and US stock futures slipped ahead of the open, with prediction-market traders pricing only a slim chance the S&P 500 would open higher today (Yahoo Finance).

The whipsaw is the story. Nothing fundamental changed between the record close and the overnight reversal, which points to a market trading on positioning rather than news, and to an AI rally where expectations have climbed so high that even strong results struggle to clear them. The next real test is the earnings season that opens on the 9th, when the chip complex has to convert this year’s optimism into numbers. A run of Treasury auctions and tomorrow’s Fed minutes sit in between, so the tape could stay jumpy. The direction of the whole market still rests on one question: whether AI spending keeps compounding.

Sensei’s Insight: Records and reversals inside twelve hours tell you this is a positioning market, not a news one. The level that matters is not the Dow’s, it is the bar earnings have to clear from the 9th. Watch guidance, not the open.

💾 Samsung’s record profit, and a falling share price

Samsung Electronics handed the market a lesson in expectations this morning. The South Korean giant reported preliminary second-quarter operating profit of 89.4 trillion won, about $58 billion, a record that jumped roughly 1,810% from a year earlier and marked a third straight quarter of all-time-high earnings, driven by strong demand for the high-bandwidth memory that feeds AI servers. The stock fell anyway, dropping about 9.6% on the day, as investors focused less on the profit and more on whether memory prices and AI infrastructure spending can keep rising at the pace that produced it (CNBC).

The reaction captures the unease running through the whole chip complex. A profit that large would normally lift a stock, but with memory names having led this year’s rally, the market is now pricing perfection and selling anything that hints the boom is maturing. Samsung’s pledge to build vast new fabrication plants in the south of the country added to the worry, since heavy spending arrives just as investors question future demand. The read carries straight into the memory suppliers, from SK Hynix, which is preparing its own large US listing, to Micron, and sets a cautious tone under this week’s earnings season.

Sensei’s Insight: A 1,810% profit surge met with a 9.6% share drop is the clearest signal going that AI winners are now priced for perfection. The bull case on demand is intact. The bar on valuation is the problem, and this week’s results have to clear it.

🚀 SpaceX joins the Nasdaq-100 today

SpaceX formally enters the Nasdaq-100 before today’s open, and for a company barely a month into public life this is a rapid ascent. It listed on 12 June, raising about $85.7 billion in the largest IPO ever staged, and the shares jumped roughly 50% on their first day. A new listing would normally wait months to qualify for a major index, but a rule introduced in May now fast-tracks the very largest debutants, letting a company that ranks near the top of the market by value join after just 15 trading days. SpaceX cleared that bar with room to spare, and today it takes its place among the hundred stocks that define the index (Yahoo Finance).

Membership is a mechanical event, but the money behind it is real. More than $800 billion sits in funds that track the Nasdaq-100, and every one of them must now hold SpaceX at its roughly 1% weight, an estimated $4.3 billion of forced buying, much of it printed right at yesterday’s close when index funds rebalance. The detail that matters most for price is the float: only about 3% to 5% of SpaceX shares trade freely, with the rest held by insiders and early backers. When a wall of guaranteed demand meets a pool of shares that thin, the stock can lurch hard in either direction, calm one hour and sharp the next. There is a knock-on effect too: to pay for the SpaceX they are compelled to buy, those same funds must shave a sliver off every other member of the index, a quiet sell order landing on the biggest tech names on the same morning.

That thin float cuts both ways, which is why history counsels caution. Index inclusion is one of the most telegraphed events in markets, so the demand is often already in the price by the time the date arrives. Recent marquee additions make the point: Palantir and Strategy both tended to peak around or before they joined, then faded once the passive bid was spent. SpaceX already trades near $169, down from a peak above $225 and roughly a quarter off that high, so some of the air has escaped already. The real test is not today’s buying, which is guaranteed, but how the shares trade in the days after, once the index funds are done and ordinary buyers and sellers set the price (CoinDesk).

Sensei’s Insight: Inclusion buying is mechanical, not a verdict. Funds must own SpaceX today whatever the price. The pattern from Palantir and Strategy is that the pop fades once the passive bid is filled. I am watching what happens after, not the open.

🛢️ Saudi Arabia slashes crude prices for Asia

Saudi Arabia has cut the price of its flagship crude for Asian buyers by the most in more than two decades, a clear signal that the world’s top exporter sees a softening market. State producer Saudi Aramco set the August official selling price for Arab Light to Asia at $1.50 a barrel below the regional benchmark, an $11 cut from the previous month and the lowest since June 2020. The move followed the weekend decision by OPEC+ to add another 188,000 barrels a day of output from August, a fifth straight monthly rise, and came as the United Arab Emirates pushed production above pre-war levels (CNBC).

For households the read is straightforward: more oil is arriving just as the war premium drains away. Brent traded around $72 and US crude near $69, both close to their lowest in four months, ticking up only slightly today. With shipping through the Strait of Hormuz recovering, the extra barrels that sat on paper during the conflict can now reach buyers, and talks between Washington and Tehran are due to resume on the 11th. Cheaper crude feeds directly into softer fuel costs and cooler inflation, which matters with June CPI, the last major price read before the Fed’s decision, landing on the 14th.

Sensei’s Insight: The paper barrels are turning into real cargoes, and Saudi Arabia cutting prices this hard says the demand is not there to absorb them. That is disinflationary, and a soft CPI on the 14th would leave tomorrow’s hawkish Fed minutes a step behind the data.

₿ Bitcoin holds firm as ETF money returns

Bitcoin has climbed back above $64,000, trading around that level after a roughly 6% gain on the week, its steadiest stretch since the sharp June drawdown that dragged it under $58,000. The move still rests on the soft June jobs report, which cut the odds of a Fed rate rise and eased pressure across risk assets. The bigger shift is in the funds that track it. US spot Bitcoin ETFs pulled in about $265.7 million yesterday, their largest daily haul in more than a month, led by roughly $209 million into BlackRock’s IBIT, and the second positive session in three (CoinDesk).

That matters because the flows have pointed the other way for two months. Even with yesterday’s inflow, the funds still shed about $527 million across the shortened holiday week, an eighth straight week of net outflows, after June closed as their worst month on record. The gap between a rising price and institutional money heading out is the tension that has hung over this rally, and yesterday was the first real sign it may be closing. The prints over the rest of the week decide whether it holds, or whether one strong session was another blip inside a still-negative trend.

Sensei’s Insight: One green day does not end an eight-week outflow streak, but it is the first crack in it. Price has been leading the flows for weeks; if the money now follows, this bounce gets a floor. I am watching this week’s ETF prints.

Stories You Might Have Missed

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.