Morning Forecast: Wednesday, 1 April

Trump Puts a Clock on the War. Tonight He Tells the Country What's Next.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

Discord Integration is Live

Your private Sensei News channels are now live on Martyn’s Discord server.

If you’re already a Discord member, open a help ticket and send me your Substack email. I’ll verify it and add your newsletter role to unlock your private channels.

If you’re not on Discord yet, you can join here: https://discord.com/servers/martyn-lucas-investor-914375589480259635

You don’t have to pay for anything extra. You just need to go through the onboarding process.

When it asks why you want to join, just say “I want Sensei’s channels” and give your email.

You’ll watch a short safety video, answer a few questions, and then I’ll give you full access to your private newsletter channels, training videos, announcements, live stage events, and community chat

👀 Today’s Stories at a Glance

🪖 Trump Sets Iran War Deadline: The President suggests a three-week timeline as Iran targets Israel and major US companies.

🌍 Trump Threatens NATO Exit: Declaring the alliance a paper tiger, Trump considers withdrawal after allies refuse Hormuz naval support.

🤖 Nvidia Secures Marvell Alliance: A $2 billion stake locks Marvell into Nvidia’s proprietary networking ecosystem to sideline industry competitors.

💰 Massive Tariff Refunds Loom: CBP prepares $166 billion in payouts, though one-third of entries face exclusion from the portal.

📈 Fed Warns of Sticky Inflation: Officials signal 3% inflation may be permanent, contradicting Chair Powell’s view on transitory oil shocks.

💾 Google Breaks Memory Demand: A new compression algorithm threatens HBM demand, erasing a third of Micron’s market value recently.

🧠 One Big Thing

The Mechanical Market Bounce

Wall Street’s massive rally today is a product of technical positioning rather than genuine optimism for peace in Iran. While President Trump signaled a potential end to hostilities within three weeks, major trading desks at Goldman Sachs and JPMorgan report the surge was fueled by hedge funds unwinding bearish short positions and pension funds rebalancing at month-end. This mechanical recovery masks a worsening fundamental backdrop because the IRGC continues to strike energy infrastructure and major US corporations face direct evacuation threats. For investors, the risk remains a violent reversal if tonight’s presidential address fails to deliver a concrete ceasefire. The core tension lies in a market buoyed by temporary technical flows while the physical reality of tight oil storage and a closed Strait of Hormuz persists.

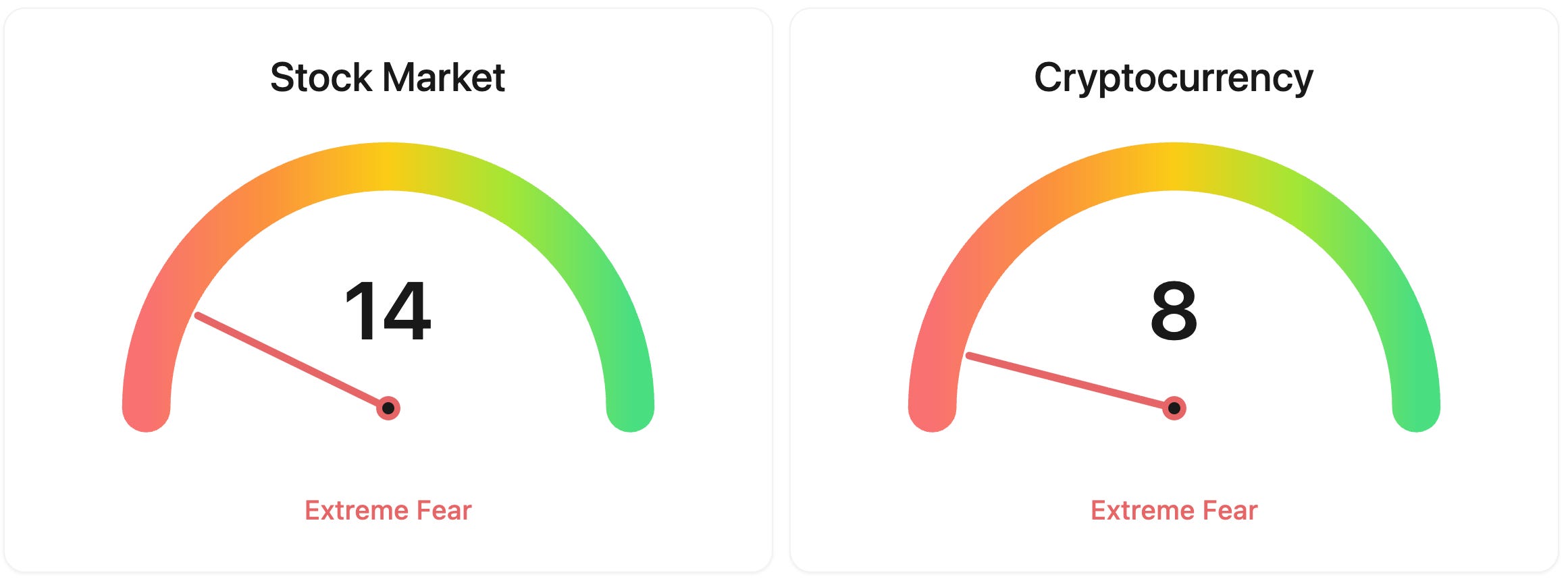

⚖️ Fear & Greed

📉 The Number That Matters

30%

Micron Technology shares plummeted 30% over eight sessions following Google’s release of the TurboQuant algorithm. The new compression technology threatens the high-growth narrative for HBM chips by significantly reducing the memory required for AI inference workloads.

⚔️ Winners vs Losers

Winners

DEFT 0.00%↑: Defi Technologies, Inc. rallied alongside a broader crypto bounce as Bitcoin climbed above $68,000, lifting sentiment across digital asset equities after a prolonged selloff.

TH 0.00%↑: Target Hospitality Corp. continued its upward momentum following a strong Q4 earnings report in March that included 2026 revenue guidance of $320M to $350M, well above the $276M consensus, backed by over $740M in new multi-year contracts tied to data center and power generation workforce housing.

NCNO 0.00%↑: nCino, Inc. surged after reporting Q4 fiscal 2026 results that handily beat estimates, with adjusted EPS of $0.37 versus the $0.21 consensus and record annual contract value bookings up 17% year over year. The company also announced a $100M accelerated share repurchase program.

NG 0.00%↑: Novagold Resources Inc. gained ahead of its Q1 2026 earnings release and investor webcast scheduled for this morning, with gold prices holding firm above $4,700 an ounce and the company advancing its Donlin Gold bankable feasibility study.

MLYS 0.00%↑: Mineralys Therapeutics, Inc. extended recent gains after the FDA accepted its NDA filing for lorundrostat, an aldosterone synthase inhibitor for hypertension, and assigned a PDUFA target date of December 22, 2026. Multiple analysts have reiterated Buy ratings with raised price targets.

Losers

ORIC 0.00%↑: Oric Pharmaceuticals, Inc. sold off sharply after announcing the recommended Phase 3 dose selection for rinzimetostat in combination with darolutamide for its Himalayas-1 prostate cancer trial, with investors apparently unimpressed by the clinical update despite the company framing it as a milestone.

RH 0.00%↑: RH missed Q4 revenue expectations at $842.6M versus the $873.7M consensus and posted adjusted EPS of $1.53, well below the $2.20 estimate. The luxury furniture retailer’s Q1 revenue guidance of $789.5M came in roughly 10% below analyst forecasts, extending concerns about its turnaround timeline.

APTV 0.00%↑: Aptiv PLC’s pre-market decline reflects the completion of its Versigent spin-off, with shares of the newly independent electrical distribution systems business (ticker VGNT) beginning regular trading on the NYSE today. The drop is a mechanical price adjustment rather than a fundamental deterioration.

MSM 0.00%↑: MSC Industrial Direct Co. reported fiscal Q2 earnings this morning that missed on both lines, with EPS of $0.82 versus the $0.84 consensus and revenue of $917.8M falling short of the $941M estimate, as ongoing weakness in manufacturing end markets weighed on demand.

NKE 0.00%↑: Nike, Inc. beat Q3 fiscal 2026 EPS estimates at $0.35 versus $0.28 but guided for a 2% to 4% sales decline in Q4, well below the consensus expectation of nearly 2% growth. The company warned of an expected 20% revenue drop in its Greater China segment this quarter, overshadowing the bottom-line beat.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $68479 (▲ 0.37%)

Ethereum (ETH): $2132 (▲ 1.36%)

XRP: $1.35 (▲ 0.78%)

Equity Indices (Futures):

S&P 500: $6578 (▲ 0.83%)

NASDAQ 100: $24143 (▲ 0.95%)

FTSE 100: £10379 (▲ 0.96%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.29% (▼ -0.74%)

Oil (WTI): $100 (▼ -1.81%)

Gold: $4743 (▲ 1.52%)

Silver: $75.08 (▼ -0.09%)

Data as of: UK (BST) 12:20 / US (EDT): 08:20 / Asia (Tokyo): 21:20

✅ 5 Things to Know Today

🪖 Trump Puts a Clock on the War, Iran Keeps Firing

President Trump told reporters yesterday that the United States could be done with its war in Iran “within two weeks, maybe three,” the first time he has put a specific public timeline on the conflict since it began on 28 February. The White House announced he will deliver a prime-time address to the nation tonight at 9 PM Eastern to provide “an important update on Iran.” The fighting is not slowing down. Iran’s Islamic Revolutionary Guard Corps (IRGC) fired three waves of missiles at Israel this morning alongside Hezbollah and Yemen’s Houthi rebels. Iranian drones hit fuel depots at Kuwait’s international airport, a cruise missile struck an oil tanker in Qatari waters, and the UAE reported nearly 50 projectiles, including its first cruise missile attacks since 11 March. The IRGC also issued an unprecedented threat naming 18 major US companies, including Apple, Microsoft, Nvidia, and JPMorgan Chase, warning employees to evacuate by tonight. Approximately 4,950 people have been killed so far. Secretary of State Marco Rubio told Fox News the US “can see the finish line,” though Iran’s Foreign Minister Abbas Araghchi told Al Jazeera that direct contact with US envoy Steve Witkoff “does not mean that we are in negotiations” (CNN).

Markets surged on the headlines, but the mechanics behind the rally tell a more cautious story. S&P 500 futures crossed 6,600 this morning, extending yesterday’s 2.9% gain, the index’s best session since May. Brent crude fell below $100 a barrel before recovering to around $104. South Korea’s Kospi jumped 7.2%, Japan’s Nikkei rose 4.5%, and European equities climbed 2.4%. But Goldman Sachs and JPMorgan trading desks told clients the rally was driven primarily by unwinding of extremely bearish positioning at quarter-end, not genuine conviction about peace. Hedge funds had been aggressively short, pension funds were rebalancing into stocks, and options dealers’ short gamma pressure rolled off with yesterday’s expiry. Fast money was waiting for any spark. The optimism rests on a Wall Street Journal report that Trump told aides he was willing to end hostilities even if the Strait of Hormuz remains largely closed. Trump dismissed the Strait as someone else’s problem, telling allies to “go get your own oil.” The UAE responded by signalling it is prepared to help open Hormuz by force. The UK announced it will chair a meeting of 35 G-7, European and Gulf allies this week to push for reopening. But floating storage in the Gulf is becoming critically tight, with only 120 of 332 tankers available as empty vessels, raising the risk of production shut-ins that could cause permanent capacity loss. Brent finished March up roughly 55%, its largest monthly gain since the benchmark’s inception in 1988 (Bloomberg).

Sensei’s Insight: Goldman and JPMorgan both flagged that this rally was positioning, not conviction. Hedge funds were short, pension funds were rebalancing, and options dealers needed to cover. That is a mechanical bounce, not a peace trade. If tonight’s address delivers anything less than a concrete ceasefire timeline, the same dynamics that drove stocks up could unwind just as fast. And even if the war ends, Hormuz is a separate problem with no clear solution. Watch tanker traffic, not headlines.

🌍 Trump Threatens to Pull the US Out of NATO

President Trump told Britain’s Daily Telegraph this morning that he is “strongly considering” withdrawing the United States from the North Atlantic Treaty Organisation (NATO). He described NATO as a “paper tiger” and said the decision was now “beyond reconsideration.” Secretary of State Marco Rubio said the US would “reassess the value of NATO” once the Iran war ends. The threat follows weeks of frustration: Trump has demanded allied navies help reopen the Strait of Hormuz, and every major ally has refused. Spain closed its airspace to US jets yesterday, Italy denied US military aircraft landing rights in Sicily, and Poland refused to relocate Patriot missile batteries to the Middle East. Trump called NATO’s response a “test” and said he would “remember” which allies cooperated (Bloomberg).

The legal path to withdrawal is murky. The National Defence Authorisation Act of 2024, co-sponsored by Rubio himself, requires a two-thirds Senate supermajority or an act of Congress to leave NATO. Trump has dismissed this. Even without a formal exit, the threat is forcing European governments to accelerate defence spending. NATO’s spending floor is rising from 2% of gross domestic product (GDP) to 5% by 2035. The UK’s response was notable: Prime Minister Keir Starmer said bluntly “this is not our war” but simultaneously announced Britain would chair a 35-nation meeting on reopening Hormuz. That is Europe hedging: refusing to fight but stepping up to manage consequences, because America’s commitment to the alliance can no longer be assumed. For retail investors, European defence stocks could see sustained demand growth as governments rearm independently, while US defence contractors that rely on NATO procurement face risk if the relationship fractures.

Sensei’s Insight: The real story is not whether Trump actually leaves NATO. It is that European governments are now planning as if he will. Defence budgets across the continent are being rewritten in real time. Companies like Rheinmetall, BAE Systems, and Leonardo could be the long-term beneficiaries of an alliance that no longer assumes America will show up.

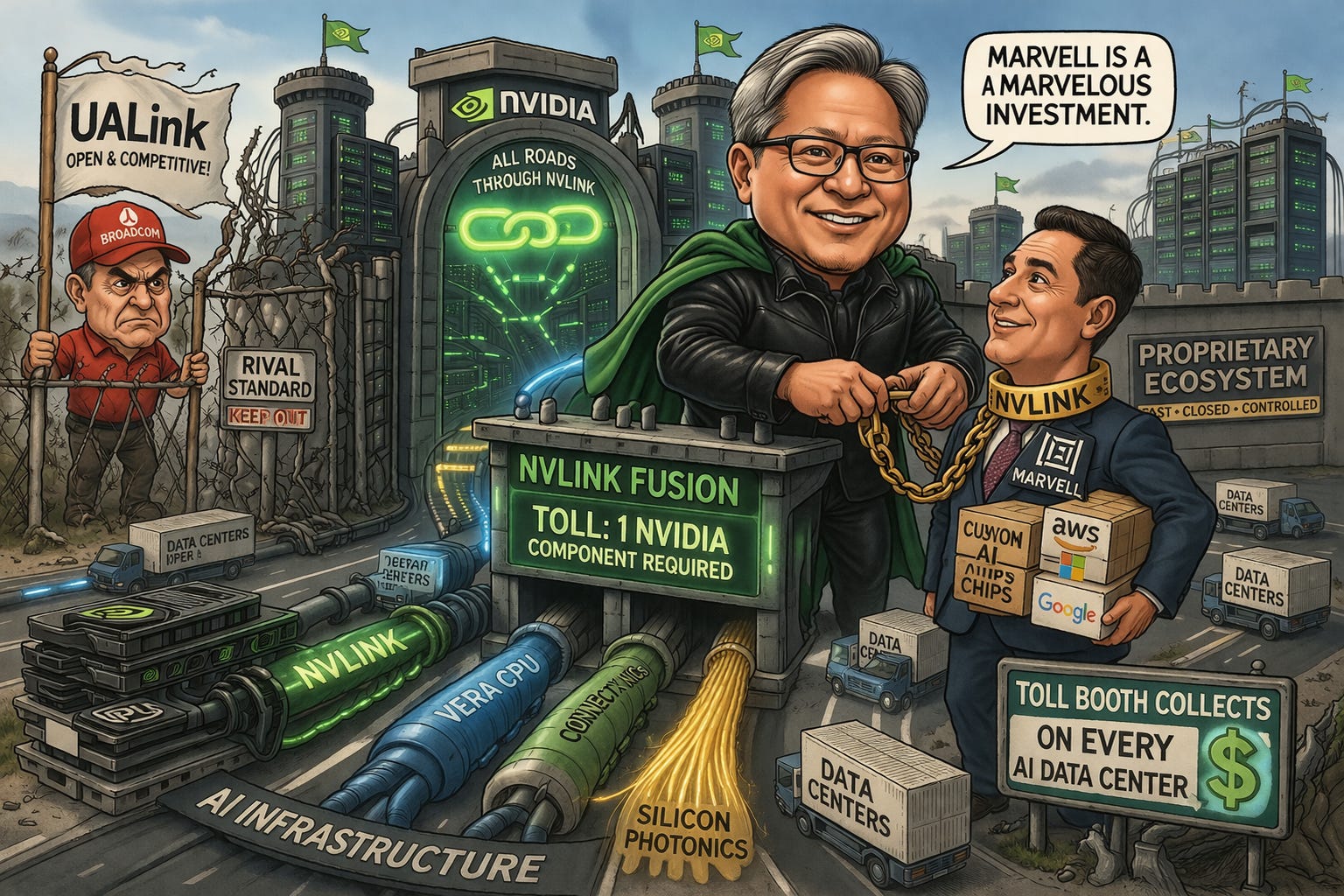

🤖 Nvidia Locks Marvell Into Its AI Empire for $2 Billion

Nvidia announced a $2 billion direct equity stake in Marvell Technology yesterday, paired with a strategic partnership built around Nvidia’s proprietary NVLink Fusion interconnect platform. The deal gives Nvidia approximately a 2.5% ownership stake. Under the agreement, Marvell will supply custom XPUs (application-specific AI accelerators) and NVLink Fusion-compatible networking gear, while Nvidia provides its Vera central processing units (CPUs), ConnectX network interface cards, and NVLink high-speed interconnects. The two companies will also collaborate on silicon photonics, the technology needed to connect thousands of graphics processing units (GPUs) using light instead of copper wire. Marvell shares surged roughly 13%, while Nvidia rose approximately 5% (CNBC).

Rather than simply selling GPUs, Nvidia is building a proprietary ecosystem where every component in an artificial intelligence (AI) data centre connects through its NVLink standard. Every NVLink Fusion platform requires at least one Nvidia component. By locking in Marvell, which designs custom AI chips for Amazon Web Services, Microsoft, and Google, Nvidia ensures that even chips built to compete with its own GPUs still depend on its infrastructure. This is a competitive move against Broadcom, which holds roughly 70% of the custom AI chip design market and backs the rival open UALink standard. The deal follows a pattern of $2 billion investments Nvidia has made in Synopsys, CoreWeave, Coherent, Lumentum, and Nebius Group (Bloomberg).

Sensei’s Insight: The investment is not about Marvell’s stock price. It is about who controls the plumbing. If NVLink Fusion becomes the default standard for connecting AI chips, Nvidia collects a toll on every data centre built, even the ones using competitors’ processors. That is a platform monopoly being assembled in plain sight.

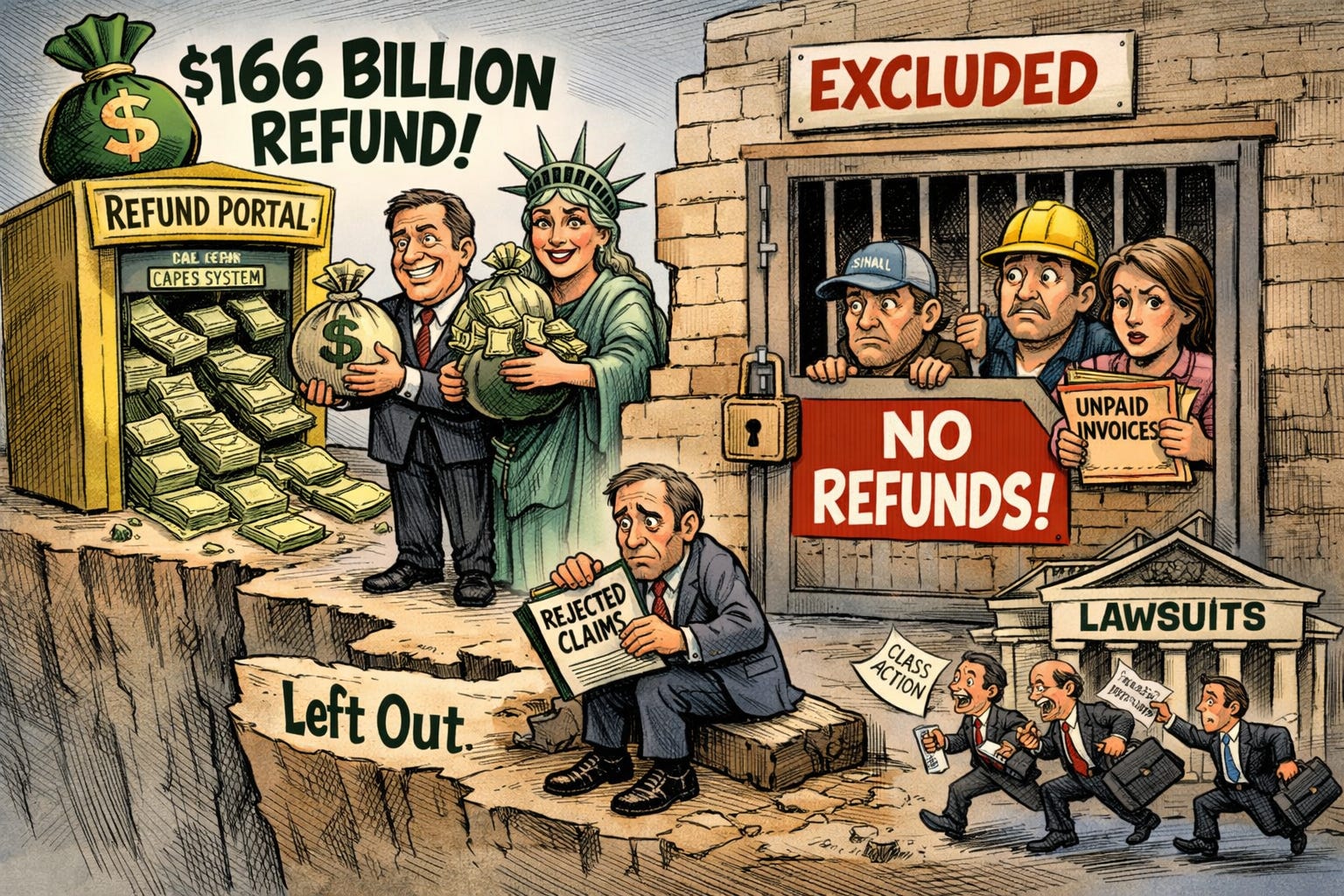

💰 A $166 Billion Refund Is Coming, But a Third of Importers Are Shut Out

United States Customs and Border Protection (CBP) filed its third progress report yesterday on the CAPE system (Consolidated Administration and Processing of Entries), the automated portal being built to refund approximately $166 billion in tariffs the Supreme Court ruled unconstitutional on 20 February. The portal’s claim module is 85% complete, with a likely launch around 20 April. But roughly one-third of the 53 million affected import entries will be excluded at launch, including shipments subject to antidumping orders, entries in bonded warehouses, and entries with drawback claims. Approximately 27,000 importers have registered so far, covering about $120 billion. Tens of thousands of smaller importers may not know they are entitled to refunds (Reuters).

Interest on the unlawful duties is accruing at $650 to $700 million per month. Companies that absorbed tariff costs will receive one-time windfalls when refunds arrive, potentially boosting Q2 and Q3 earnings. But the system is not automatic: importers must proactively submit claims via CSV upload. Class action lawsuits are targeting retailers that passed tariff costs to consumers, with FedEx and Costco already named as defendants. Judge Richard Eaton of the Court of International Trade has pushed CBP hard: “The Supreme Court told you what your position is. Your position is we’re going to refund this money.” Trump replaced the struck-down tariffs with a 10% global tariff under Section 122 of the Trade Act of 1974, set to expire 24 July, creating a policy cliff for trade-sensitive sectors.

Sensei’s Insight: The one-third exclusion is the number to watch. Smaller importers without legal teams are the ones most likely to fall through the cracks. If the portal launches on time, it could quietly lift earnings for import-heavy retailers. If it stalls, the $650 million in monthly interest becomes a taxpayer liability that grows every day.

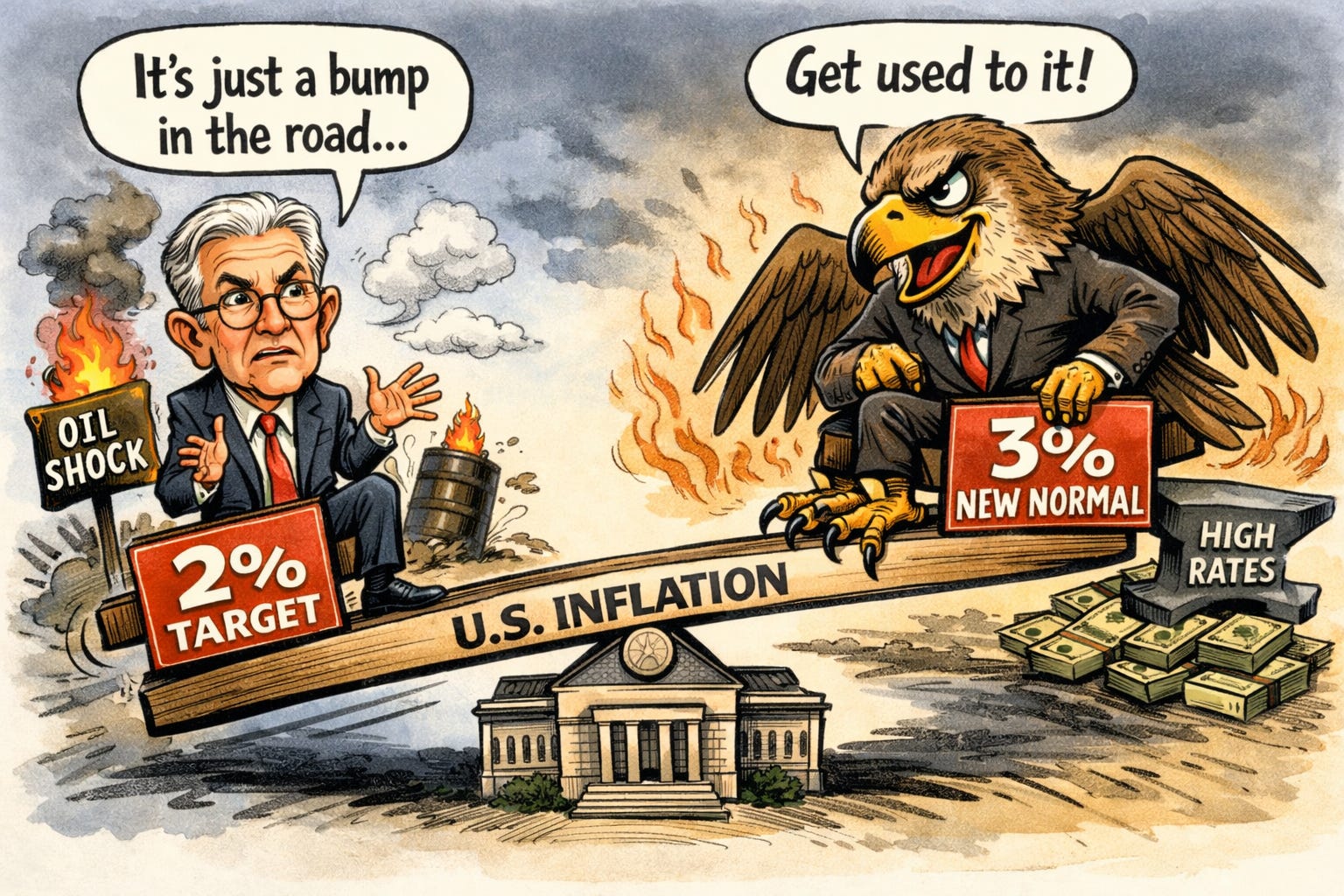

📈 The Fed’s Biggest Hawk Says 3% Inflation Is the New Normal

Kansas City Fed President Jeff Schmid, the most hawkish voice on the Federal Open Market Committee (FOMC), warned yesterday: “There is a real risk inflation will get stuck closer to 3%.” Speaking to the Rotary Club of Oklahoma City, he added: “This oil shock comes at a time when inflation already has been too high for too long. Now is not the time to assume that the inflation from higher oil prices will be transitory.” The comments directly contradict Fed Chair Jerome Powell, who one day earlier at Harvard University said “the tendency is to look through any kind of a supply shock.” Powell’s appearance was dramatic: market odds of a rate hike by December collapsed from above 50% to just 2.2%, and Treasury yields dropped 10 basis points across the curve (Bloomberg).

The data supports Schmid’s concern. Core Personal Consumption Expenditures (PCE), the Fed’s preferred inflation gauge, sits at 3.06% year-over-year, more than a full point above the 2% target. The three-month annualised rate is running at 3.66%, suggesting the trajectory is worsening. CME FedWatch shows a 77% probability that rates do not move in 2026, up from expectations of two cuts before the war. Schmid dissented against both the October and December 2025 rate cuts, and his speech yesterday is the first time a sitting Fed official has warned that the oil spike could make inflation permanently stickier. Nomura economist Rob Subbaraman reinforced the point, noting there is no pent-up demand or fiscal space this time, and central banks “have learnt their lesson to not assume inflation will be transitory.” If Schmid is right, anything financed with debt faces a fundamental repricing.

Sensei’s Insight: Powell and Schmid are publicly disagreeing on the most important question in markets: is this oil shock temporary or structural? Powell’s term ends in May. His successor Kevin Warsh has stated a preference for lower rates. But if inflation is still running at 3% when Warsh takes the chair, his options will be as constrained as Powell’s rhetoric suggests they are not.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.