Morning Forecast: Wednesday 15 July

Cool CPI lifts stocks as ASML raises its outlook, IBM suffers its worst day ever, and PPI lands today.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

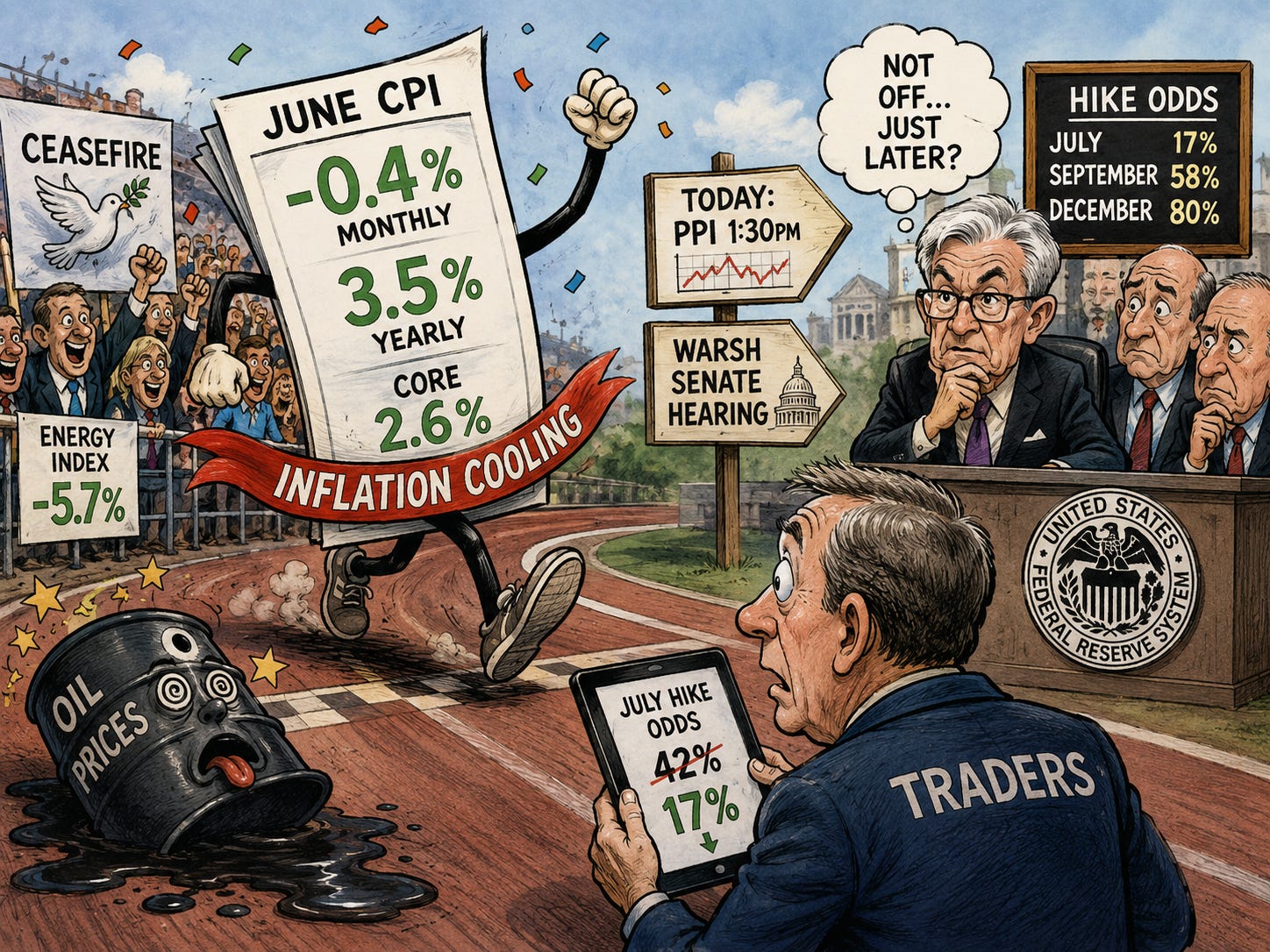

📊 Inflation cools, hike bet collapses: June CPI fell to 3.5% and core held flat, sinking July rate-hike odds to 17% from 42%.

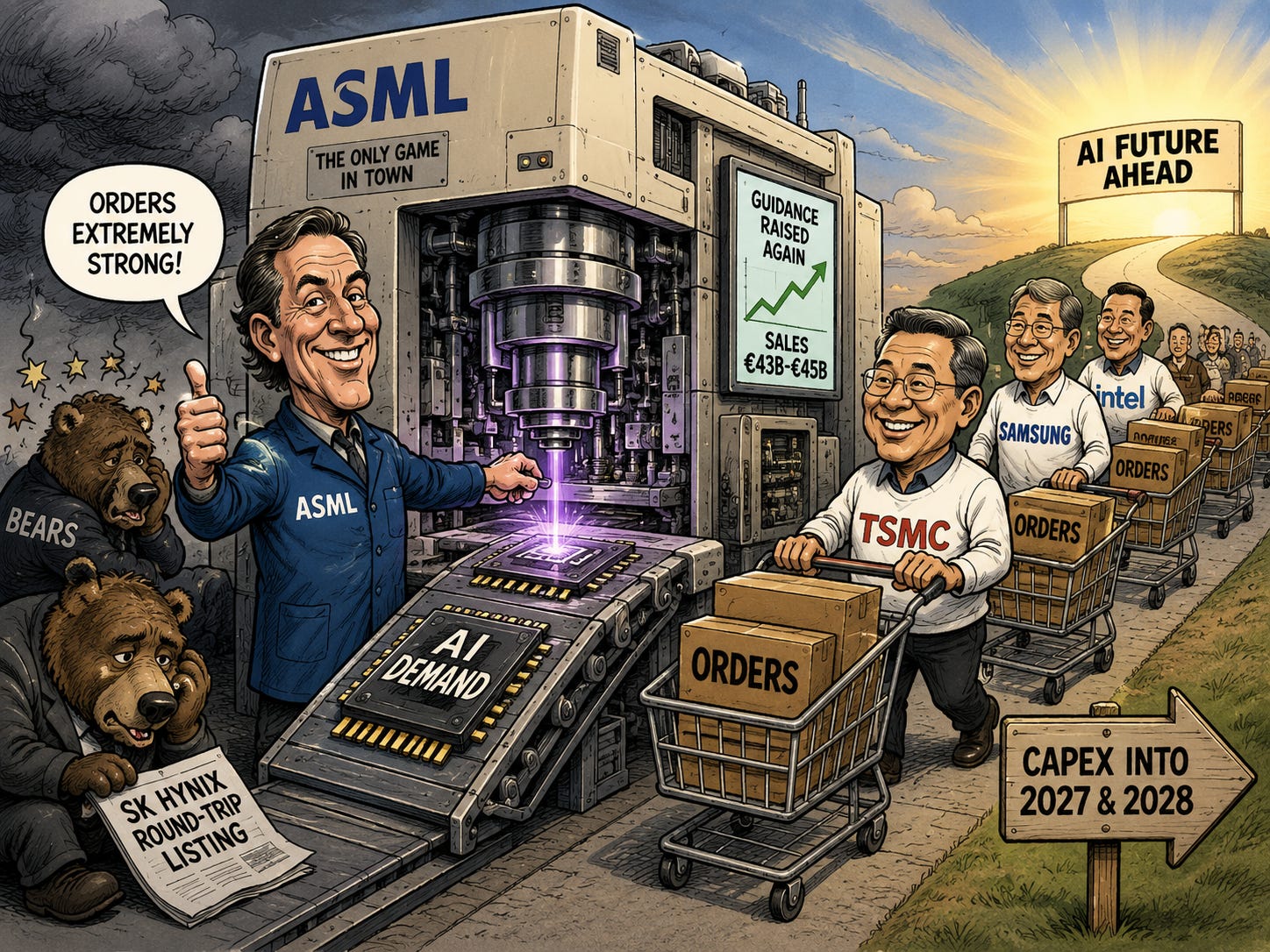

🔬 ASML lifts its outlook: The chip-gear giant beat and raised full-year sales guidance to €45bn, reigniting the AI-hardware trade.

💻 IBM’s worst day ever: Shares cratered 25% after a profit warning as clients diverted budgets to memory and servers, hitting software names.

🏦 Goldman and Citi crush it: Goldman posted a record $20.98 EPS and Citi beat every estimate, capping a blowout bank season.

🛢️ Oil hits a one-month high: Brent topped $85 as US strikes resumed and the blockade returned, though Trump dropped his 20% toll.

🥇 Gold caught in a tug-of-war: Bullion jumped over 2% on the cool CPI, then slipped today as the oil rally revived inflation worry.

₿ Bitcoin waits on the clock: Crypto holds steady as the CLARITY market-structure bill eyes a Senate floor vote the week of 20 July.

🏥 J&J headlines more earnings: Johnson & Johnson and Morgan Stanley report today, with TSMC and Netflix the big reads tomorrow.

🔍 Deep Dive: A full PPI Day Playbook on today’s producer-price print, why the pipeline matters more than the headline, and the levels to watch.

🧠 One Big Thing

June’s inflation number cooled hard, but look at where the cooling came from. The energy index fell 5.7%, its steepest drop since 2020, because June was the ceasefire month for oil. The genuinely good news sits in core, which was flat on the month, the first real sign that underlying price pressure is easing rather than spreading. The catch is that oil is already back above $85, a one-month high, so the energy relief that flattered the headline is reversing in real time. That puts the weight on today’s PPI and on core holding. Watch the wholesale energy read and Warsh’s tone for whether this relief has legs.

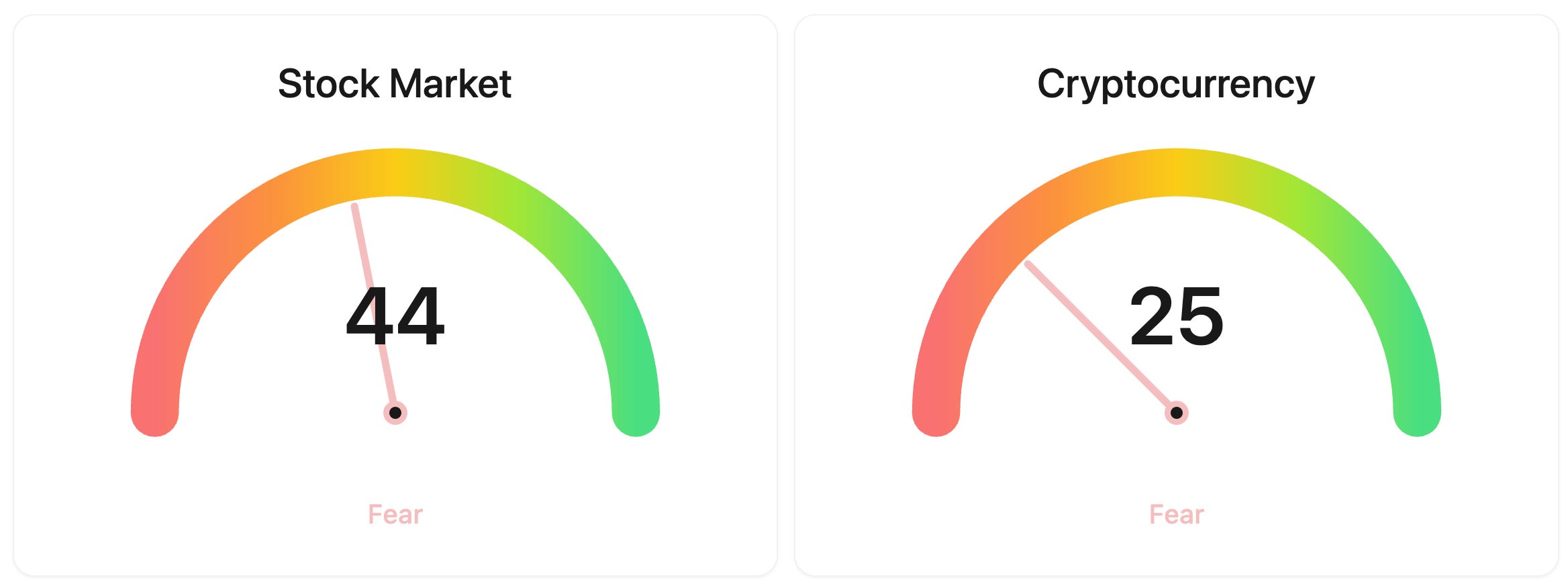

⚖️ Fear & Greed

📉 The Number That Matters

17%

The odds of a July rate hike now, down from 42% a day earlier, after June inflation cooled far more than expected and core prices held flat.

⚔️ Winners vs Losers

Winners

AEHR 0.00%↑: Aehr Test Systems surged after fiscal Q4 earnings beat expectations and management guided fiscal 2027 revenue to $130 million to $150 million, implying roughly 160 to 200 percent growth on the back of record bookings and AI-driven burn-in demand.

PYPL 0.00%↑: PayPal jumped on a report that Stripe and Advent International submitted a joint bid to acquire the company for $60.50 per share, valuing it at more than $53 billion, about a 28 percent premium to Tuesday’s close.

WEAV 0.00%↑: Weave Communications moved higher in pre-market on a low-float, thin-volume push with no specific catalyst identified.

BLK 0.00%↑: BlackRock rose as it reported second quarter results before the open, with investors positioned for another quarter of record assets under management and continued iShares and private-markets inflows.

BABA 0.00%↑: Alibaba extended its multi-session rally as investors kept rotating into Chinese technology on the strength of its Alibaba Cloud and Qwen AI story, with no fresh company-specific catalyst behind today’s move.

ASML 0.00%↑: ASML gained after second quarter sales and margins came in above guidance and the company raised its full-year 2026 outlook for a third time, citing accelerating AI-driven demand for advanced logic and memory chips.

Losers

PNR 0.00%↑: Pentair tumbled after preliminary second quarter sales landed near $930 million, down about 17 percent versus prior guidance, and the company slashed its full-year outlook on pool channel inventory destocking while naming an interim CFO.

PXED 0.00%↑: Phoenix Education Partners fell after fiscal third quarter revenue came in flat and below estimates and full-year guidance disappointed, with margins pressured by higher advertising spend and costs tied to adapting recruitment to AI-driven search.

EVO 0.00%↑: Evotec dropped as its US-listed shares caught up to a steep Frankfurt selloff after the company cut full-year 2026 revenue and earnings guidance, blaming delayed high-margin partnership milestones now pushed into 2027.

ELV 0.00%↑: Elevance Health declined after reporting second quarter results this morning, with the market focused on continued pressure in Health Benefits margins from elevated Medicaid and ACA medical costs.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $64,578 (▼0.58%)

Ethereum (ETH): $1,874 (▼0.79%)

XRP: $1.11 (▼0.44%)

Equity Indices (Futures):

S&P 500: 7,606 (▲0.19%)

NASDAQ 100: 29,938 (▲0.49%)

FTSE 100: 10,495 (▲0.20%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.61% (▲0.50%)

Oil (WTI): $80 (▲0.60%)

Gold: $4,028 (▼0.62%)

Silver: $57.98 (▼1.23%)

Data as of: UK: 11:30 am BST / US: 6:30 am EDT / Asia (Tokyo): 7:30 pm JST

✅ 5 Things to Know

📊 Inflation cools hard as the hike scare fades

June CPI came in far softer than forecast. Consumer prices fell 0.4% on the month, the sharpest drop in years, pulling the annual rate down to 3.5% from 4.2% in May. The relief was broad: the energy index sank 5.7%, its biggest fall since April 2020, as June’s Middle East ceasefire let petrol prices unwind, while core prices, which strip out food and energy, were flat on the month and eased to 2.6% on the year. Traders reacted fast, cutting the odds of a July Fed rate hike to 17% from 42% the day before (CNBC).

The read matters because it reframes the whole summer. A hot core into rising oil was the nightmare setup, and core coming in flat is the first hard sign that underlying pressure is easing rather than spreading. The market has not called the all-clear, though: it pushed the hike bet out rather than off, still pricing roughly a 58% chance by September and about 80% by December. Today keeps the story live. June producer prices land at 1:30pm, a wholesale read after May’s hot 1.1% jump, and Warsh returns for a second day, this time before the Senate (CNBC).

Sensei’s Insight: The headline will get the cheers, but core flat is the line that actually matters, because nobody can blame it on the ceasefire ending. I am watching whether today’s PPI backs it up or flags oil creeping back in.

🔬 ASML beats, lifts guidance, and revives the AI trade

ASML, the Dutch company with a near monopoly on the machines that print the most advanced chips, beat estimates and lifted its outlook for the second time this year. Second-quarter net sales came in at €9.3 billion with a 54% gross margin and net income of €2.9 billion, all ahead of forecasts. More important was the guidance: ASML now sees full-year sales of €43 billion to €45 billion, up from €36 billion to €40 billion, and called orders “extremely strong” through the first half as customers rushed to expand capacity. The shares rose about 4% (CNBC).

For a market rattled by SK Hynix’s round-tripped listing, this is the cleanest signal yet that AI-hardware demand is still accelerating, not fading. ASML sits at the base of the chip supply chain, so its order book is a forward read on what every foundry and memory maker plans to build. Management pointed to strong logic and DRAM investment and order visibility running into 2027 and 2028, with Intel now using its High-NA machines in production. The next confirmation comes fast: TSMC, the world’s leading foundry, reports tomorrow. Watch whether its capital-spending plans echo ASML’s confidence.

Sensei’s Insight: When the one company nobody can bypass raises guidance twice in a year, the AI-capex debate is largely settled at the hardware layer. The question is no longer whether the spend is real, it is which links in the chain capture it.

💻 IBM suffers its worst day on record

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.