Morning Forecast: Wednesday, 16 March

Australia Is Hiking Rates. The Fed Can't. Inflation Cheat Sheet

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

🪓 Oracle Eyes Massive AI Layoffs: 30,000 jobs face cuts to fund expensive infrastructure and mounting debt.

🐻 Short Seller Targets SoFi Shares: Muddy Waters alleges hidden debt; shares fell as retail investors reacted.

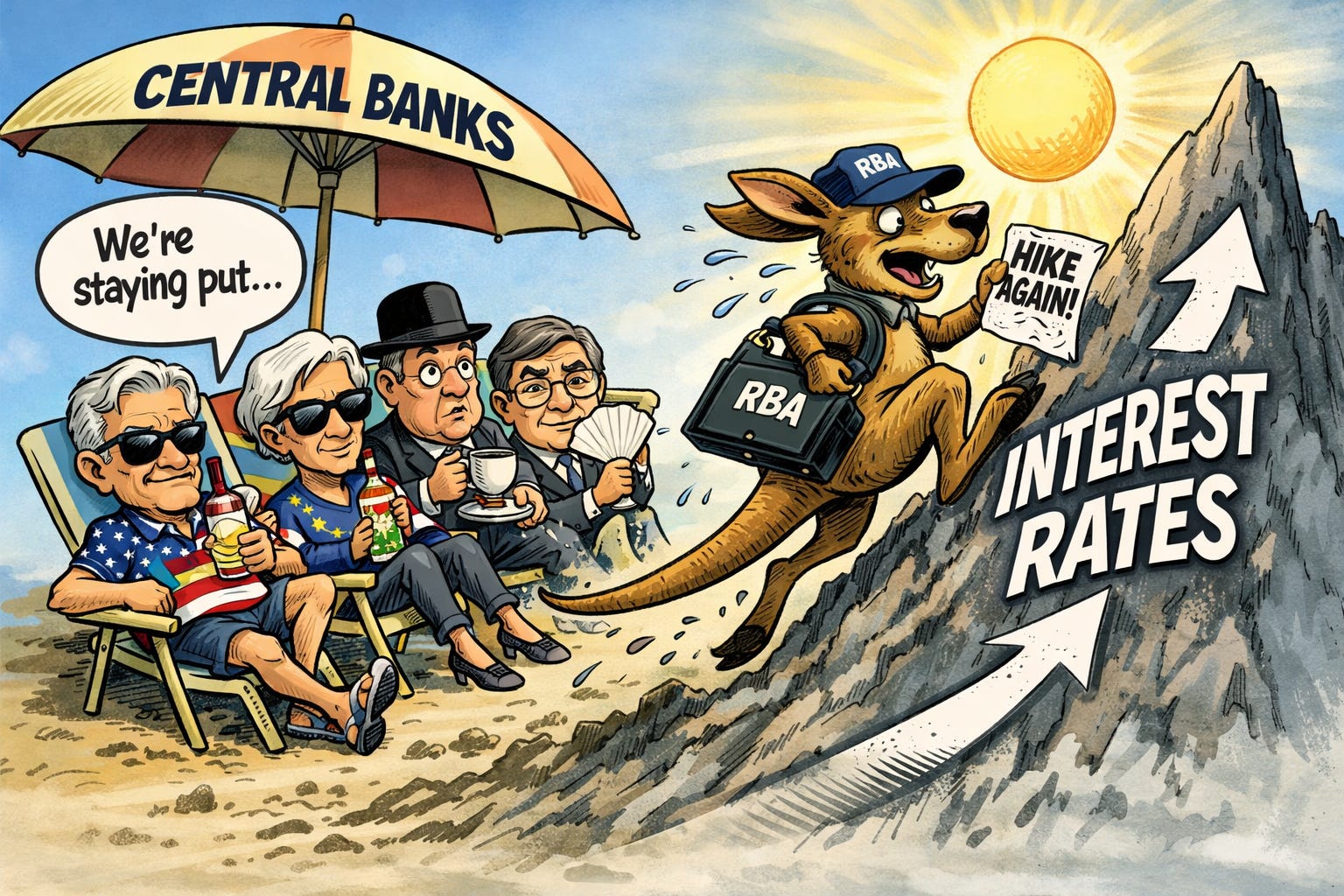

🦘 Australia Hikes Interest Rates Again: The central bank raised rates as sticky inflation outpaces global peers.

🛢️ Iraq Bypasses Blocked Oil Strait: A new pipeline deal allows crude exports via Turkey; avoiding Hormuz.

✈️ Shutdown Disrupts National Airport Operations: Unpaid TSA staff shortages may force closures as the shutdown continues.

🔍 Wholesale Inflation Data Drops Today: Markets await February producer prices before upcoming war and tariff shocks.

🧠 One Big Thing

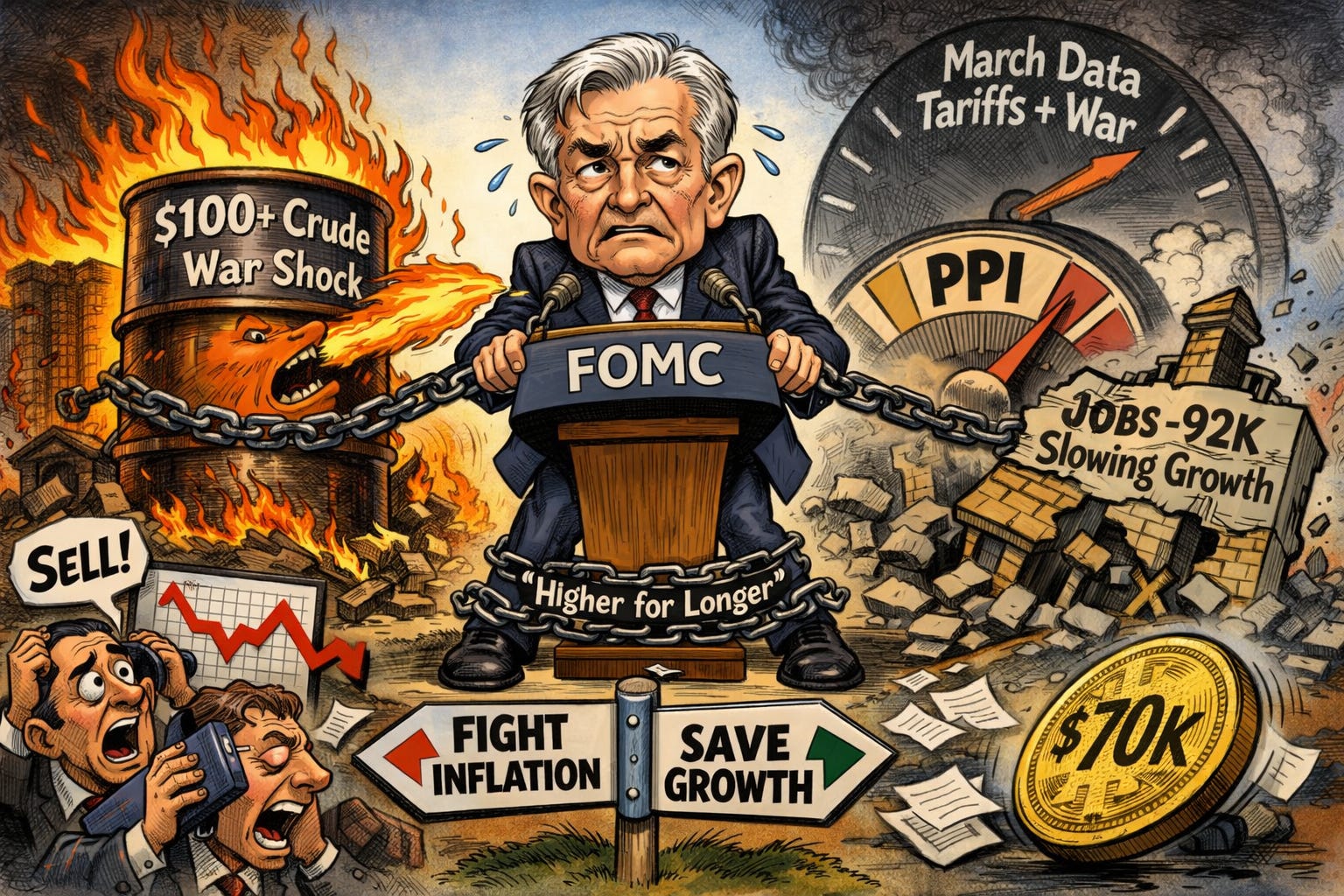

The Fed’s Dueling Mandate

Today’s FOMC meeting concludes as the Federal Reserve navigates a strategic deadlock between surging energy costs and a weakening labor market. While officials plan to keep the benchmark interest rate unchanged, the military conflict in Iran has pushed oil prices higher, threatening to entrench five years of elevated inflation. This price shock arrives just as a sudden decline in February payrolls signals potential economic fragility. Policymakers are now divided on whether to prioritize cooling prices or supporting employment. For investors, the focus shifts to new economic projections to determine if the Fed will maintain its path toward rate cuts. The decision hinges on how domestic stability withstands these mounting global risks.

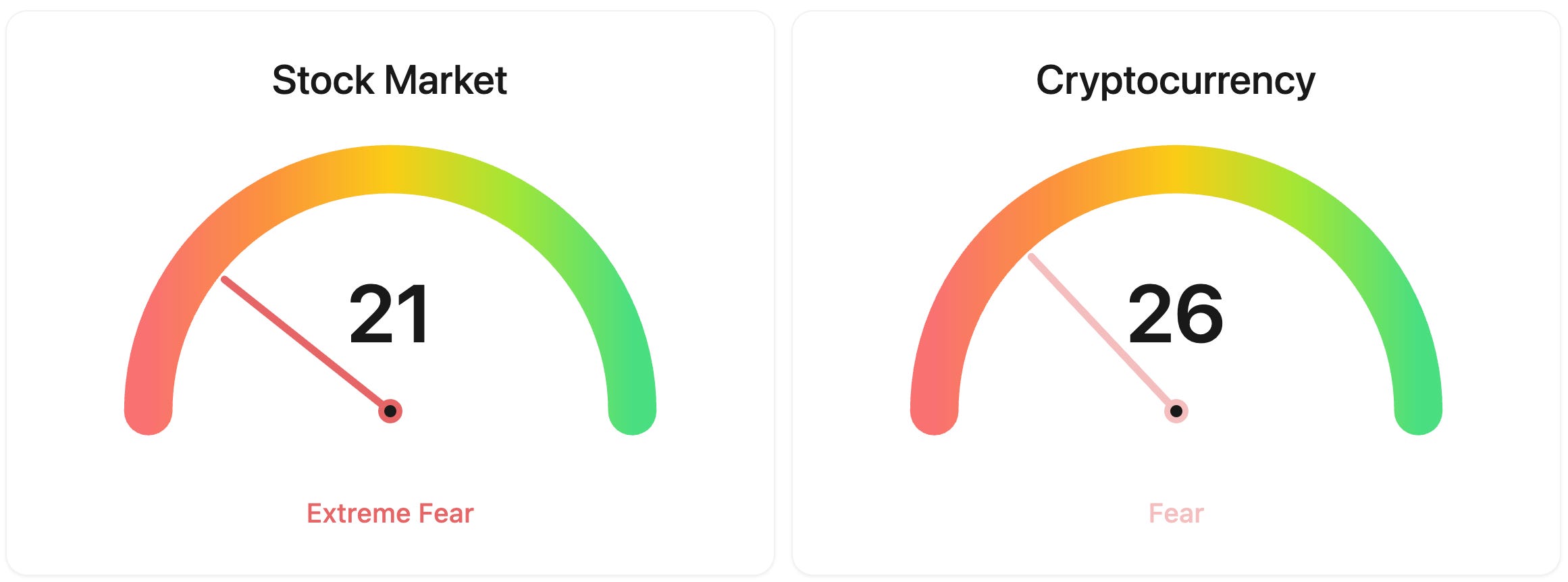

⚖️ Fear & Greed

📉 The Number That Matters

0.8%

Investors are bracing for February PPI data (being released today) following January’s +0.8% core inflation surge. This baseline reading serves as the final inflation gauge before the Iran conflict’s oil shock and new 10% global tariffs hit the domestic supply chain (more in the deep dive).

⚔️ Winners vs Losers

Winners

OVID 0.00%↑: Ovid Therapeutics Inc. surged ahead of its Q4 earnings report scheduled for today, with investors anticipating updates on its OV329 epilepsy drug program heading into a Phase 2a trial and the oral KCC2 activator OV4071 nearing clinical stage.

KC 0.00%↑: Kingsoft Cloud Holdings Limited continued its rally on sustained momentum in Chinese AI and cloud infrastructure stocks, with the company’s AI gross billings growing over 120% year-over-year last quarter as it prepares to report Q4 2025 results on March 25.

DVLT 0.00%↑: Datavault AI Inc. climbed after announcing its Q4 and full-year 2025 earnings call for tomorrow, with investors positioning ahead of results following the company’s raised 2026 revenue guidance to at least $200 million on tokenized asset deal momentum.

HIT 0.00%↑: Health In Tech, Inc. jumped after announcing a strategic collaboration with Ciklum, an AWS Advanced Tier Services Partner, to optimize its self-funded stop-loss health insurance marketplace with AI-driven quoting, financial reporting, and analytics capabilities.

VNET 0.00%↑: VNET Group, Inc. extended gains following strong Q4 2025 earnings reported on March 16, with revenue beating estimates at $389 million (up 26% year-over-year) and ambitious 2026 guidance projecting 16-19% revenue growth driven by surging wholesale data center demand.

Losers

GEMI 0.00%↑: Gemini Space Station, Inc. continued to slide ahead of its March 19 earnings report, weighed down by ongoing fallout from triple C-suite departures, a 25% workforce reduction, its exit from the UK, EU, and Australia, and weakening crypto trading volumes.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $74223 (▲ 0.43%)

Ethereum (ETH): $2332 (▲ 0.65%)

XRP: $1.52 (▲ 0.13%)

Equity Indices (Futures):

S&P 500: $6754 (▲ 0.52%)

NASDAQ 100: $24971 (▲ 0.68%)

FTSE 100: £10434 (▲ 0.60%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.18% (▼ -0.40%)

Oil (WTI): $94 (▼ -1.81%)

Gold: $4982 (▼ -0.49%)

Silver: $79.73 (▲ 0.56%)

Data as of: UK (GMT) 10:30 / US (EST): 06:30 / Asia (Tokyo): 19:30

✅ 5 Things to Know Today

🪓 Oracle May Cut 30,000 Jobs to Pay for Its AI Gamble

Oracle is preparing what could be the largest tech layoff event of 2026. TD Cowen estimates the company may eliminate up to 30,000 positions, roughly 18.5% of its 162,000-person workforce, freeing $8 to $10 billion in cash flow. Oracle has not confirmed that figure, but its own Securities and Exchange Commission (SEC) filings tell the story: the company raised its fiscal 2026 restructuring budget to $2.1 billion and stated that AI-generated code has allowed it to reorganise product development teams into “smaller, more agile and productive groups.” The cuts are expected to span multiple divisions and could begin as early as this month (Reuters).

The layoffs are not about a struggling business. Oracle’s most recent quarter delivered $17.2 billion in revenue, up 22% year on year, with cloud infrastructure revenue surging 84%. The problem is the cost of its AI pivot. Capital expenditure has ballooned to a guided $50 billion for fiscal 2026, up from $6.9 billion just two years earlier. Free cash flow turned negative $10 billion in the most recent quarter. Total debt now exceeds $108 billion, and Moody’s rates Oracle at Baa2, just two notches above junk and lower than every other major tech company. The stock trades around $156, down roughly 55% from its September 2025 all-time high (Financial Times).

Sensei’s Insight: The pattern is worth naming: record revenue growth and mass layoffs happening inside the same company at the same time. Oracle is not cutting because AI replaced these roles. It is cutting because AI chips and data centres cost more than the business currently generates, and debt markets are starting to notice.

🐻 Muddy Waters Takes Aim at SoFi, One of Retail’s Favourite Stocks

Prominent short-seller Muddy Waters Research disclosed a short position in SoFi Technologies (SOFI) yesterday, publishing a report that accused the fintech of being “a financial engineering treadmill, not a healthy origination business.” The firm alleges SoFi’s true personal loan charge-off rate, the percentage of loans written off as losses, sits at 6.1%, more than double the 2.89% the company reports. Muddy Waters also claims SoFi’s 2025 adjusted EBITDA (earnings before interest, taxes, depreciation, and amortisation) of $1,054 million is inflated by roughly 90%, with what it calls a “truer figure” of just $103 million. The report flagged $312 million in apparent unrecorded debt from JPMorgan Chase and $194 million in capitalised marketing expenses that bypass the income statement.

SoFi shares dropped as much as 6% intraday on volume of 157.5 million shares, about 167% above the daily average, before recovering to close down 1.47% at $17.37. SoFi is one of the most heavily retail-owned stocks in the market, which makes this report especially relevant for this audience. Muddy Waters has a significant track record: its short report on Luckin Coffee in 2020 led to a fraud revelation and eventual delisting. That does not mean the same outcome applies here, and SoFi has not yet issued a formal response. But the allegations are specific enough, and the accuser credible enough, that anyone holding the stock should watch closely for management’s rebuttal.

Sensei’s Insight: The most telling number is not the charge-off discrepancy but the EBITDA gap. If Muddy Waters is even directionally right that $1 billion in earnings is really closer to $100 million, the stock’s valuation framework changes entirely. Management’s response will need to address the methodology, not just dismiss the messenger.

🦘 Australia Hikes Rates Again While Everyone Else Holds

The Reserve Bank of Australia (RBA) raised its cash rate by 25 basis points to 4.10% yesterday, the second consecutive monthly increase and the first back-to-back hike since mid-2023. The decision was razor-thin at 5 to 4, the narrowest possible margin and the first non-unanimous vote since July 2025. Australia now stands alone among major central banks in actively tightening while the Federal Reserve, the European Central Bank (ECB), the Bank of England (BoE), and the Bank of Japan are all expected to hold rates this week (Reuters).

Governor Michele Bullock pointed to inflation that remains stubbornly above target. Headline Consumer Price Index (CPI) inflation sits at 3.8% year on year, well above the 2 to 3% target band. Housing costs are climbing 6.8% annually, electricity surged 32.2% as state rebates expired, and inflation expectations hit 5.2%, the highest since July 2023. All four major Australian banks passed the full increase through to variable home loans immediately, adding roughly $181 per month to a $600,000 mortgage compared to the start of the year. All four now expect another hike in May, which would fully unwind the entire 2025 easing cycle (Reuters).

Sensei’s Insight: The RBA cut rates three times in 2025, bringing the cash rate down to 3.60%. It has now reversed two of those three cuts in just two months. Watch whether other central banks follow Australia’s lead on pre-empting energy-driven inflation rather than waiting it out, particularly after the Fed and BoE decisions later this week.

🛢️ Iraq Finds a Way Around the Strait of Hormuz

Iraq and the Kurdistan Regional Government (KRG) struck a deal yesterday to resume oil exports through the Kirkuk-Ceyhan pipeline, sending crude north to Turkey’s Mediterranean port and bypassing the Strait of Hormuz entirely. Shipments are expected to begin today at an initial rate of around 250,000 barrels per day. Oil prices dipped on the news, with Brent falling below $101 a barrel after gaining more than 3% the previous session (Bloomberg).

The deal required political concessions on both sides. The KRG had refused to allow crude through its pipeline infrastructure until Baghdad agreed to lift customs restrictions imposed in January that had strangled trade into the region. The pipeline itself, largely idle since 2014 after sustaining heavy damage during the Islamic State’s advance through northern Iraq, can handle 250,000 barrels per day with potential to scale to 450,000. For context, Iraq was producing over 4 million barrels per day before the war and has since slashed output to roughly 1.4 million as the Hormuz closure filled every available storage tank. The pipeline restores a fraction of lost capacity, but it is the first meaningful workaround since the strait effectively closed over two weeks ago.

Sensei’s Insight: The pipeline matters less for its barrels and more for its signal. Saudi Arabia and the UAE already have bypass infrastructure; Iraq was the only major Gulf producer with zero alternatives. Other producers watching Hormuz will read this as evidence that overland routes can be activated under pressure, which may start to erode the risk premium baked into crude since the war began.

✈️ Airports May Start Closing as the DHS Shutdown Hits Day 32

The partial US government shutdown entered its 32nd day yesterday with no resolution in sight, and the Transportation Security Administration (TSA) is running out of options. Acting Deputy TSA Administrator Adam Stahl warned that if the standoff continues, smaller airports may have to “quite literally shut down.” Some 50,000 TSA officers have been working without pay since the Department of Homeland Security (DHS) lost funding in mid-February, and 366 have quit. Callout rates, the percentage of officers not showing up for shifts, hit 55% at Houston’s Hobby Airport on a single day and have averaged around 20% at major hubs including Atlanta, JFK, and Houston throughout the shutdown (CNN).

The standoff is over immigration policy, not aviation, but aviation is absorbing the damage. Travellers at some airports faced security lines stretching past three hours over the weekend, right as spring break travel hit full swing. Airline CEOs have called for a quick resolution, and Delta Air Lines raised its first-quarter revenue guidance yesterday on strong bookings, even as the operational environment deteriorates. The shutdown has forced the suspension and restart of the Global Entry programme and triggered food bank donations at airports in Denver, Seattle, Portland, and Baltimore for TSA workers who cannot afford groceries. The previous full government shutdown last autumn lasted 43 days and forced the Federal Aviation Administration (FAA) to cut flights by 10%. This time air traffic controllers are funded, but TSA staffing is the bottleneck (CNBC).

Sensei’s Insight: The shutdown has been treated as political background noise, but the market impact is starting to compound. Airlines are guiding higher while the infrastructure supporting their operations frays, consumer confidence takes another hit during spring break, and the political standoff shows no sign of resolution. Watch airline stocks closely if any airport actually closes a terminal.

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_live_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

🔍Deep Dive: FEBRUARY PPI CHEAT SHEET

Producer Price Index | Wednesday March 18, 2026 | 8:30 AM ET / 12:30 PM GMT

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.