Morning Forecast: Wednesday 20 May

Nvidia reports tonight. Your cheat sheet is inside.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

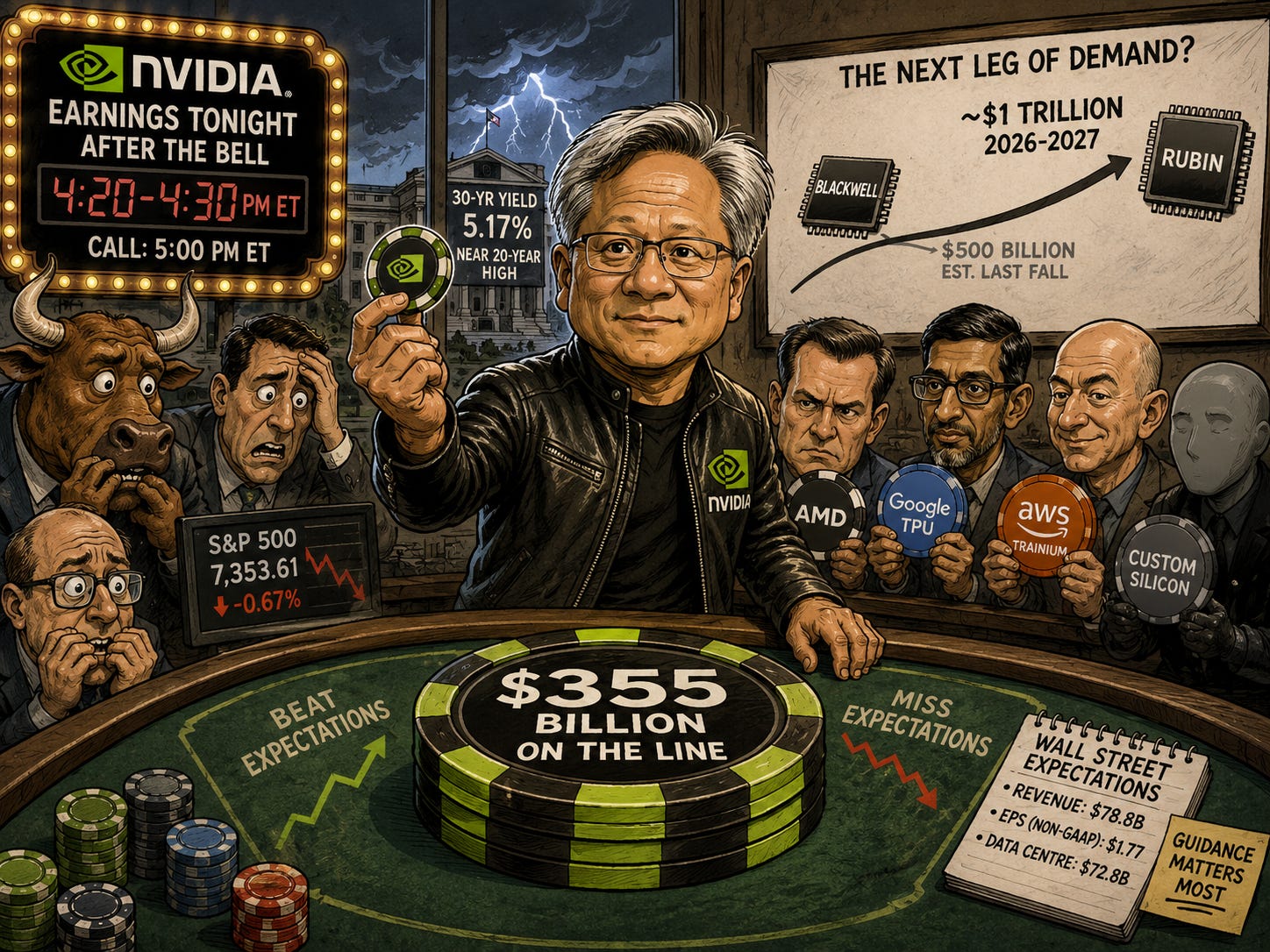

🤖 Nvidia’s $355 Billion Earnings Test: Options price a 6.5% swing on tonight’s print, roughly $355 billion of market value.

🛢️ Britain Opens Russian Fuel Loophole: Open-ended licence permits Russian-derived diesel and jet fuel from third-country refineries, with no expiry.

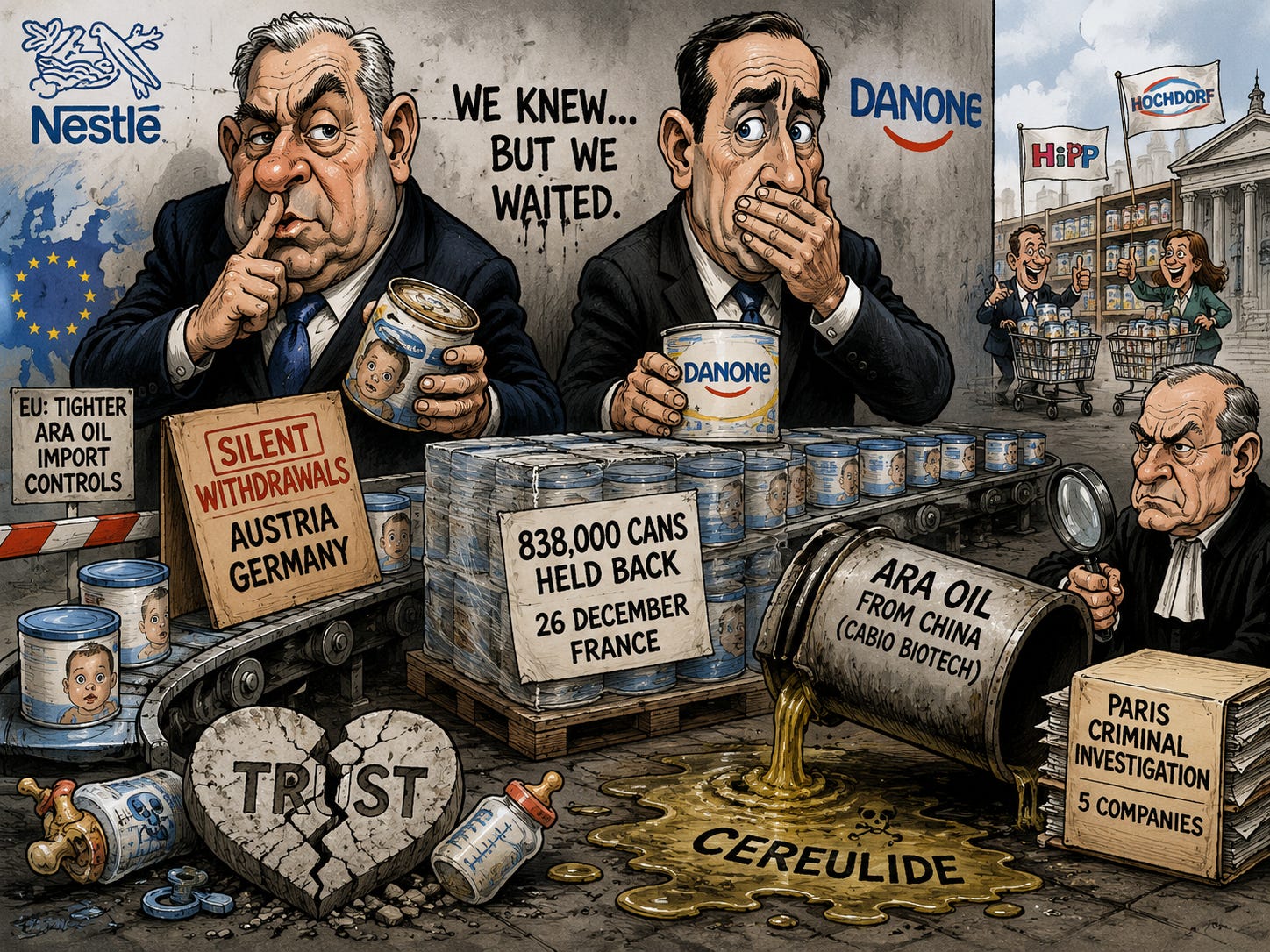

🍼 Nestlé and Danone Face Cover-Up Claims: European broadcasters allege silent withdrawals and held-back stock during the cereulide contamination episode.

💴 Tokyo Issues Fresh Yen Warning: Yen near 159 against the dollar after sixth straight session of losses, edging toward intervention zone.

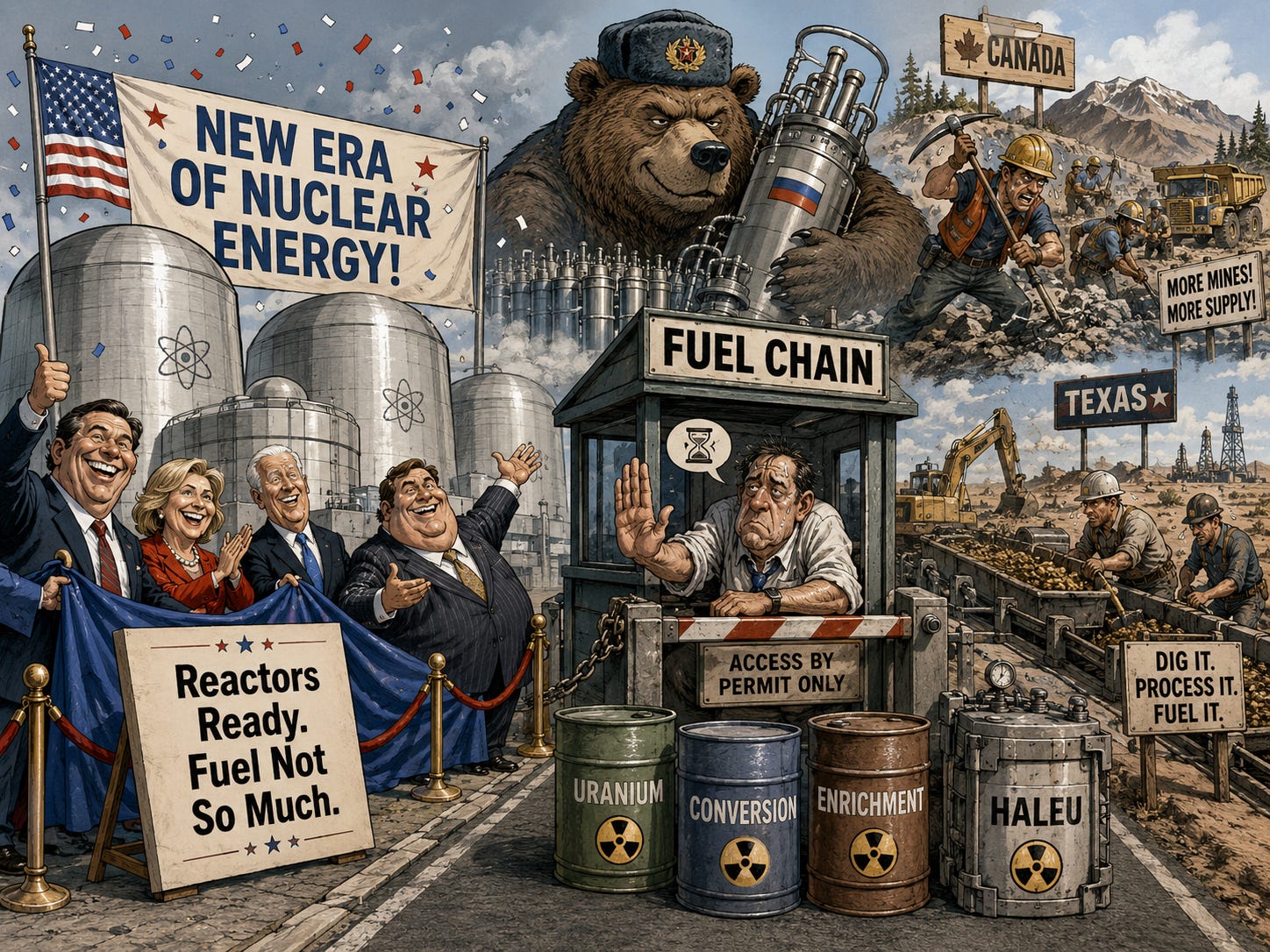

⚛️ Nuclear’s Bottleneck Sits in Fuel: Uranium contract prices reached $90 a pound while Russia still controls roughly 40% of global enrichment.

🏦 Lloyds Eyes Data-Centre Lending: British lender plans push into artificial intelligence (AI) infrastructure financing market dominated by Wall Street.

📊 AI Reshapes Investment-Grade Bond Market: Hyperscaler issuance approached $121 billion in 2025, with AI debt nearing 15% of the investment-grade market.

🛢️ Iran Threatens Retaliation Beyond Region: Revolutionary Guard warns any renewed American or Israeli strikes would trigger response well outside the Middle East.

🧠 One Big Thing

The bond market is now the constraint on the artificial intelligence (AI) trade, not the catalyst. The 30-year Treasury yield closed at 5.17%, the highest since the early 2000s, just as Nvidia heads into a print options price as a $355 billion event. Long-duration equity multiples and long-duration bond yields are no longer moving in opposite directions; the same hyperscaler capital expenditure cycle driving Nvidia revenue has fed $121 billion of new debt issuance in 2025. That feedback loop matters for positioning. A clean Nvidia guide with rates still climbing could narrow the AI rally to revenue winners rather than re-rate the broader sector.

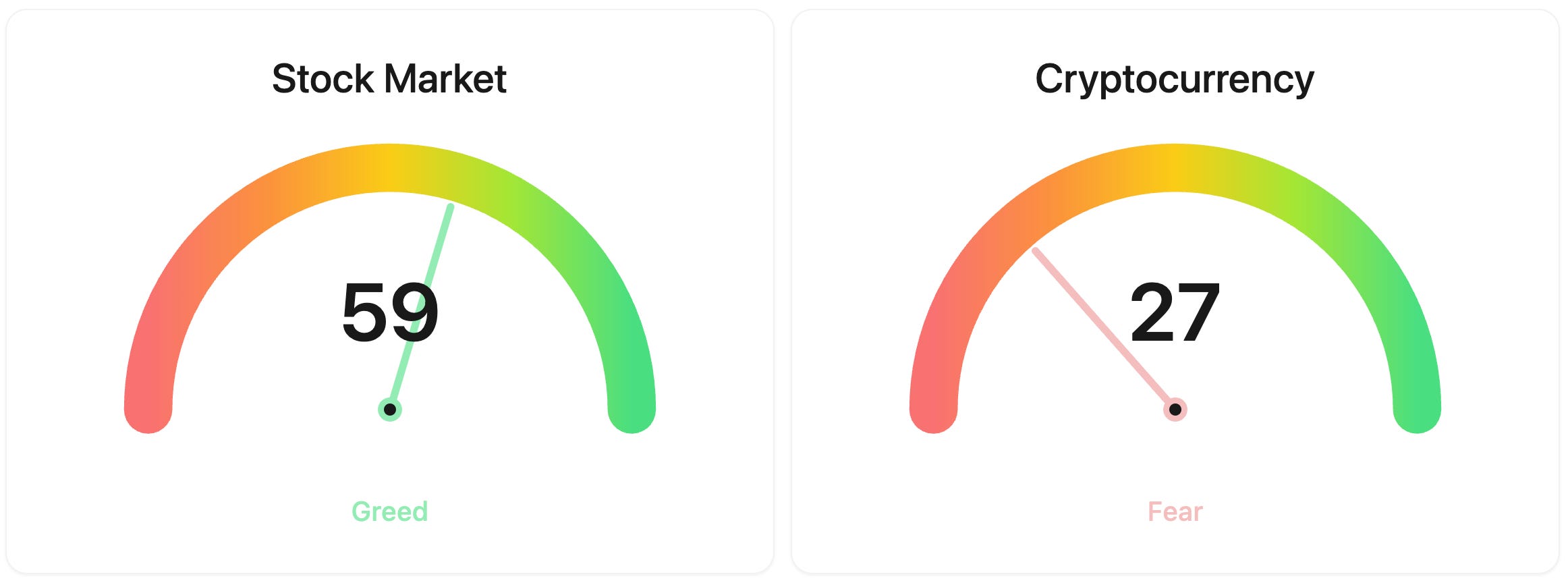

⚖️ Fear & Greed

📉 The Number That Matters

40%

Russia still controls roughly 40% of global uranium enrichment capacity, the choke point reactor pledges have ignored. With Western enrichment expansion not expected until the early 2030s, that 40% gates the supply chain through the rest of the decade.

⚔️ Winners vs Losers

Winners

IMVT 0.00%↑: Immunovant, Inc. jumped after reporting positive preliminary results from its IMVT-1402 trial in difficult-to-treat rheumatoid arthritis, released alongside its Q4 and fiscal year 2026 earnings and business update this morning.

INTC 0.00%↑: Intel Corporation led a semiconductor sector bounce, with chip names extending gains for a second day as investors positioned ahead of Nvidia’s closely watched first-quarter earnings after the bell.

CBRS 0.00%↑: Cerebras Systems Inc. extended its post-IPO rally after S&P Global confirmed the AI chipmaker qualifies for Fast Track IPO Entry, with inclusion in eligible S&P Dow Jones Indices taking effect May 25.

Losers

TGT 0.00%↑: Target Corporation slid despite a Q1 beat with EPS of $1.71 versus $1.35 expected and a raised full-year outlook, as new CEO Michael Fiddelke struck a cautious tone on the macro environment and the work still ahead.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $77,584 (▲ 1.04%)

Ethereum (ETH): $2,134 (▲ 1.10%)

XRP: $1.37 (▲ 0.90%)

Equity Indices (Futures):

S&P 500: $7,385 (▲ 0.46%)

NASDAQ 100: $29,142 (▲ 0.75%)

FTSE 100: £10,349 (▲ 0.56%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.65% (▼ -0.34%)

Oil (WTI): $102 (▼ -2.24%)

Gold: $4,495 (▲ 0.26%)

Silver: $75.49 (▲ 2.52%)

Data as of: UK (BST) 1:58pm GMT / US (EDT): 7:58am EST / Asia (Tokyo): 9:58pm

✅ 5 Things to Know

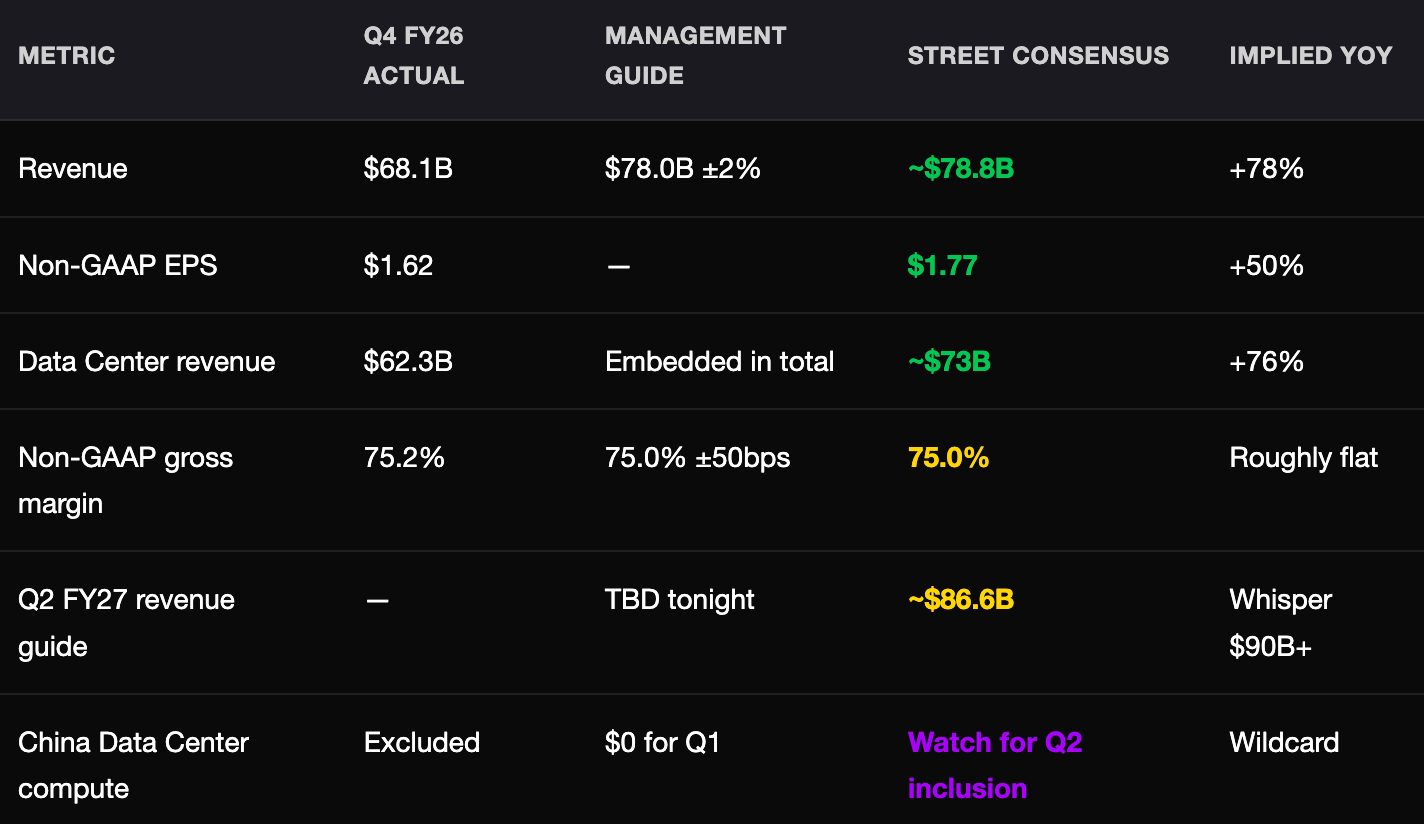

🤖 Nvidia Reports Tonight With $355 Billion on the Line

Nvidia delivers fiscal Q1 2027 results after the US market close today at roughly 4:20 to 4:30 p.m. Eastern, with the call at 5:00 p.m. Options markets are pricing a move of about 6.5% in either direction tomorrow, equivalent to roughly $355 billion of market value given Nvidia’s $5.4 trillion size. Wall Street consensus sits at about $78.8 billion in revenue and $1.77 in non-GAAP earnings per share, with Visible Alpha pointing to $72.8 billion of that from the data-centre segment. Last quarter’s data-centre revenue rose 75% year over year, and gross margins recovered to 75.2% after the H20 China inventory charge. (Reuters)

The bar is high and the read-through is wider than one stock. The S&P 500 closed Tuesday at 7,353.61, down 0.67% for a third straight decline, with the 30-year Treasury yield finishing at a near-20-year high of 5.17%. The market needs a clean Nvidia print to give it a reason to stop bleeding. Beyond the headline numbers, the contested ground is inference: AMD, Alphabet’s TPUs, Amazon’s Trainium and custom silicon are all pushing harder on the workload that is supposed to be the next leg of demand. Jensen Huang said at GTC in March that Blackwell plus the Rubin platform could generate roughly $1 trillion of revenue across 2026 and 2027, up from a $500 billion estimate last fall. Investors will want that number reaffirmed. (S&P Global)

Sensei’s Insight: Go to the Deep Dive below for a full cheat sheet for tonight’s Nvidia earnings.

🛢️ UK Quietly Carves Out Russian Diesel and Jet Fuel

Britain late Tuesday issued an open-ended general trade licence that permits the import of diesel and jet fuel refined in third countries from Russian crude. The licence takes effect today, has no expiry date, and is subject only to record-keeping requirements rather than supply-chain evidence at the border. It exempts those two fuels from the wider third-country processed-oil ban that Whitehall introduced on the same day. Diesel imports under HS codes 2710 19 42 and 2710 19 44 and jet fuel under 2710 19 21 are covered. (Reuters)

This is the energy-security side of the Iran war showing up in sanctions policy. Brent traded around $110 a barrel yesterday, the Strait of Hormuz remains contested, and IEA chief Fatih Birol warned in mid-April that European stockpiles of aviation fuel had roughly six weeks of cover. UK refiners met only 54.9% of road-diesel demand and 28.8% of jet-fuel demand in 2024, and the country relies heavily on imports from India and the Gulf. The US extended its own Russian-oil waiver on Monday for similar reasons. The combined message from London and Washington this week is that sanctions architecture will tighten on paper, but fuel will keep moving while the Middle East crisis runs. For investors, the carve-out reduces the near-term risk of a UK-driven jet fuel squeeze that would have hit IAG, easyJet and Ryanair fuel bills hardest. (Bloomberg)

Sensei’s Insight: The licence is indefinite and reviewable, which means it stays until policy or fuel markets change. The next test is whether the EU pushes back on the UK using its “partner country” status to keep Russian-derived fuel flowing while Brent stays above $100.

🍼 Nestlé and Danone Hit With Fresh Cover-Up Claims

A joint investigation by Radio France, Belgium’s RTBF and Switzerland’s RTS published yesterday accused Nestlé and Danone of delays in alerting European authorities about cereulide contamination in infant formula, including what the broadcasters called silent withdrawals in Austria and Germany from 24 December and 838,000 cans held back at a Nestlé factory in northern France from 26 December. Nestlé called the reports “inaccurate and misleading” and said it acted with full transparency from day one. Danone did not respond. French prosecutors in Bordeaux and Angers have ruled out a link between the recalled product and two infant deaths, with a third still under investigation. (RTÉ)

The story has shifted from a contamination problem to a credibility problem, and that matters for both stocks because brand trust in baby formula does not bend back easily. The toxin was traced to arachidonic acid oil supplied by China’s CABIO Biotech and used across Nestlé, Danone and Lactalis production, exposing how concentrated the upstream ingredient chain had become. Bernstein puts infant formula at roughly 21% of Danone group revenue and about 5% for Nestlé, with Danone’s exposure heaviest in China. Recalls have reached more than 60 countries. Paris prosecutors opened criminal investigations into five companies in February. The next pressure points are the EU’s tighter ARA oil import controls already in place and any new findings from the Paris investigation. Competitors like HiPP and Hochdorf have been picking up shelf share through the disruption. (Reuters)

Sensei’s Insight: Danone carries about four times the formula revenue exposure of Nestlé, and China is where the trust scars run deepest. The criminal probe and any prosecutorial findings on disclosure timing are the catalysts that could move both names again.

💴 Katayama Renews Yen Warning After G7 in Paris

Finance Minister Satsuki Katayama told reporters in Paris on Tuesday that her G7 counterparts understand Japan’s position on the yen and that Tokyo will take bold action as needed. The G7 communique reaffirmed the long-held commitment not to target exchange rates and acknowledged that excess currency volatility can harm economies, language Japanese officials read as cover for further action. The yen has weakened toward 159 against the dollar this week, its sixth consecutive session of losses, and is near the 160 level that triggered actual market intervention in late April. Japan’s official reserves stood at roughly $1.37 trillion at the end of December 2025. (Bloomberg)

The yen is the cheapest funding leg of the global carry trade, so any meaningful rally on intervention forces traders to unwind positions worldwide. That is the channel through which a Tokyo policy story becomes a cross-asset story. The Bank of Japan’s policy rate sits at 0.75% against US fed funds at 3.50% to 3.75%, and that gap is keeping pressure on the currency despite verbal escalation. BoJ board member Kazuyuki Masu said this week that rates should be raised as soon as possible, citing inflation risks from the Iran war. In 2024 Japan spent roughly $100 billion across four interventions, with a single July session hitting $36.8 billion. For investors, the relevant exposures are Japanese exporters like Toyota and Sony if the yen rallies, importers and utilities on the other side, and currency-hedged Japan ETFs versus unhedged peers. (The Japan Times)

Sensei’s Insight: Verbal intervention is the cheap tool. What actually moves the yen for more than a few days is coordinated US-Japan action. Whether Katayama and Treasury Secretary Scott Bessent are aligned again is the next thing to watch, not the rhetoric.

⚛️ Nuclear’s Real Bottleneck Is Fuel, Not Reactors

The nuclear revival has shifted from a policy story to a fuel-chain story. The IEA says more than three-quarters of mined uranium comes from just four countries and that Russia controls roughly 40% of global enrichment capacity. With 78 gigawatts of new reactor capacity under construction across 15 countries and 38 nations pledged at the Paris Nuclear Energy Summit to triple global capacity by 2050, the front end of the fuel cycle is now the gating issue. Long-term U3O8 contract prices reached $90 a pound by the end of the first quarter, the highest since 2008, with spot prices holding at $85 to $87. (IEA)

The investment shift this implies is upstream. Reactor builders make headlines, but uranium miners, converters and enrichers control the actual scarcity. The Trump executive orders target quadrupling US nuclear capacity to 400 gigawatts by 2050, and Orano USA estimates that doing it with domestic fuel would need a twelve-fold expansion of US enrichment capacity. The Department of Energy awarded $900 million each to Centrus Energy, American Centrifuge Operating and Orano Federal Services in January for HALEU production, but new capacity is not expected to be fully operational until the early 2030s. The Russian uranium import ban kicks in in 2028, which is what is putting pressure on the system now. NexGen Energy received final federal approvals for its Rook I project in Saskatchewan last month and Uranium Energy Corp started production at Burke Hollow in South Texas, the first new US in-situ recovery mine in over a decade. (Bloomberg)

Sensei’s Insight: The names with real bottleneck exposure are the enrichers and converters, not the reactor builders: Centrus, Cameco, NexGen and Uranium Energy Corp. HALEU is the harder problem because there are no commercial-scale transport casks yet, which is why the advanced-reactor timelines policymakers want are already at risk of slipping.

Stories You Might Have Missed

🏦 Lloyds Pushes Into US Data-Centre Lending

The Financial Times reported yesterday that Lloyds Banking Group is planning a push into US infrastructure lending with a specific focus on the data-centre market. The strategic point is that a large UK domestic retail lender is trying to diversify away from pure home-market rate exposure into the capital-intensive AI-linked asset class that has been the preserve of Wall Street banks and private credit. Meta’s $13 billion El Paso financing, Oracle’s $14 to $16 billion Michigan packages and the new $25 billion Google-Blackstone joint venture announced on Monday are the kind of deals UK lenders have so far been on the edges of. For Lloyds, this is about earning fee income and lending spreads in a higher-growth segment while UK retail banking flatlines. The broader read is that the AI infrastructure build-out is now reshaping bank strategy globally, not just hyperscaler capex plans. (Financial Times)

📊 AI Debt Now Accounts for 15% of the US Corporate Bond Market

Hyperscalers issued roughly $121 billion in bonds in 2025, more than four times the prior five-year average, and AI-related companies tapped debt markets for at least $200 billion across the year. Morgan Stanley projects $250 billion to $300 billion of issuance in 2026 from hyperscalers and related joint ventures, with JPMorgan forecasting $300 billion in annual AI deals across the next five years. CreditSights projects $602 billion in big-tech AI infrastructure capex in 2026, a 36% rise. The relevance for retail investors is that the AI trade is now showing up in fixed-income portfolios through investment-grade bond funds, with AI debt approaching 15% of the US investment-grade corporate market. A Quinn Emanuel analysis put 2025 AI industry revenue at roughly $60 billion against $400 billion of capex, which is the concentration risk regulators and Democratic senators have begun asking about. (Bloomberg)|

🛢️ Iran vows global retaliation if war resumes

Iran’s Revolutionary Guard warned today that any renewed US or Israeli strikes would trigger retaliation well beyond the Middle East, escalating a standoff that has kept Brent crude trading around $110 a barrel, up roughly 80% this year. President Donald Trump told reporters yesterday he could order fresh attacks within days as he pushes Tehran into concessions over its nuclear programme and the reopening of the Strait of Hormuz to oil and gas tankers. The threats have already rippled into markets, helping fuel a global government bond selloff as traders price in stickier inflation. NATO is separately weighing a mission to escort vessels through Hormuz by early July if the waterway stays blocked.

🔍 NVIDIA Q1 FY27 Earnings: The Cheat Sheet

Everything you need to know before tonight’s print, in one place.

The most-watched print of the quarter lands today. The press release crosses around 4:20 PM Eastern, and the conference call kicks off at 5:00 PM Eastern. NVIDIA closed last week at an all-time high of $236.54 before slipping back to roughly $222 heading in. About 6% of last week’s gains are already gone before management has spoken a word.

The company right now

NVIDIA designs and sells the chips that train and run modern artificial intelligence systems. Its current platform, Blackwell, is in full volume production. The next one, Vera Rubin, started sampling earlier this year and ramps in the second half of 2026.

Four reporting segments exist, but only one really matters. Data Center revenue made up 91% of the total last quarter at $62.3 billion, up 75% year-on-year. Gaming, Professional Visualization, and Automotive together account for less than 10%. The four largest hyperscalers (Alphabet, Amazon, Meta, Microsoft) make up just over half of Data Center revenue, and their combined 2026 capital expenditure is on track to approach $700 billion (CNBC).

The biggest development since the last report: the US cleared roughly ten Chinese firms to buy the H200 chip under a licensing structure that routes 25% of revenue to the US Treasury. No chips have actually shipped yet (CNBC).

What Wall Street expects

NVIDIA’s own Q1 guide of $78 billion was already $5 billion above consensus when it was issued, one of the widest guide-above-Street gaps in mega-cap history (Indmoney).

Why this print is different

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.