Morning Forecast: Wednesday 8 July

Trump says the Iran ceasefire is “over,” and oil jumps toward $79 a barrel.

This content is for informational and educational purposes only and does not constitute financial advice. Always do your own research. Not financial advice (NFA).

👀 Today’s Stories at a Glance

⚔️ Trump calls the Iran truce over: The president called the ceasefire a “waste of time” after overnight US strikes, sending Brent up about 6% toward $79 a barrel.

💻 DeepSeek chip rout hits Asia: China’s DeepSeek is building its own chip, and the selloff dragged Samsung and SK Hynix, pushing Korea’s Kospi into a bear market.

🏛️ Warsh’s first Fed minutes land: The June record publishes later today, showing how close a 2026 rate hike really is, as bond yields hit a four-week high.

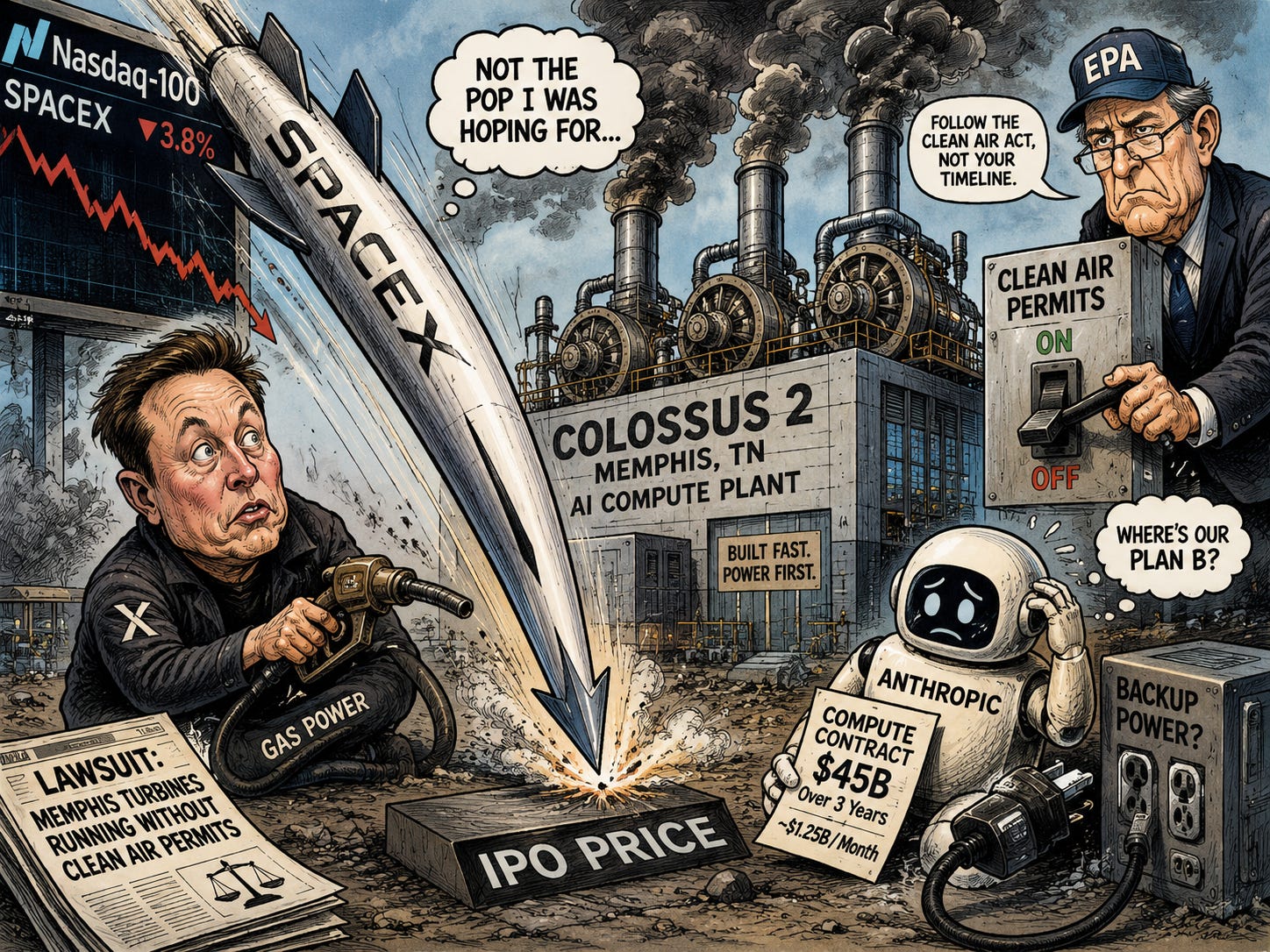

🚀 SpaceX slides on its debut: The stock fell toward its float price on its first Nasdaq-100 day as a permit fight clouds its $45 billion Anthropic deal.

₿ Bitcoin slides toward $62,000: The coin fell about 2.6% as the Iran escalation hit risk assets, giving back much of its jobs-report bounce before today’s Fed minutes.

💊 Vertex buys Crinetics for $10bn: The drugmaker agreed an $85-a-share cash takeover, sending the target near double as big biotech deals return this year.

🎮 Xbox cuts 3,200 jobs: Microsoft is laying off staff and selling five studios in its biggest gaming overhaul, admitting its margins trail rival platforms by a wide gap.

🥤 PepsiCo opens earnings season: The snacks-and-drinks giant reports before the open tomorrow, with volumes the test of whether shoppers are still absorbing higher prices.

🔍 Deep Dive: Keep an eye out later today, when I’ll break down the Fed minutes in full, plus a dedicated newsletter on them for premium members only.

📈 Chart of the Day: WTI crude has jumped around 11% in two days, filling the price gap left when the Iran war began in March, then bouncing off that low.

🧠 One Big Thing

The market’s reaction to the Iran shock is the real signal. A war flare usually sends money into gold and government bonds, yet today both fell while oil and yields rose. Investors are treating the escalation as an inflation problem that keeps the Fed leaning hawkish, not a growth scare that brings rate cuts closer. That is why equities, crypto and gold sold off together rather than splitting. Into today’s minutes, the risk is a central bank already minded to tighten now facing a fresh energy-price impulse. Watch the 2-year yield and Brent for the cleaner read.

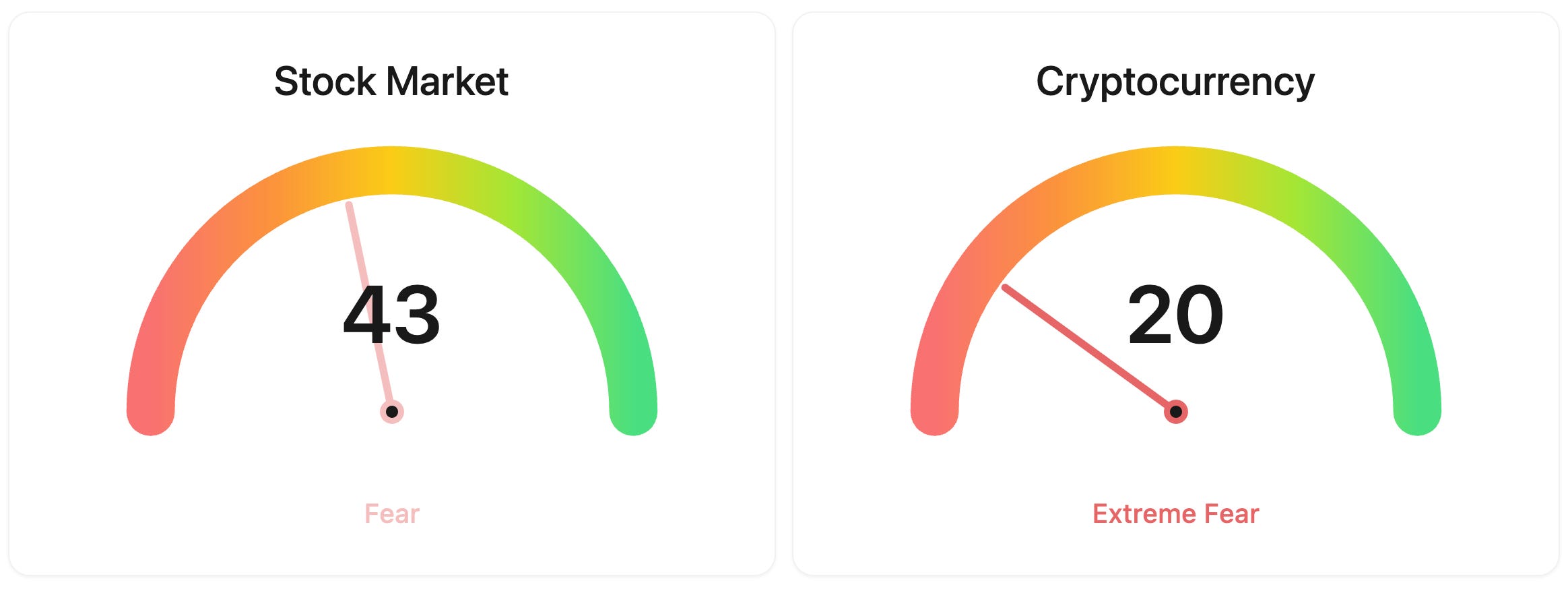

⚖️ Fear & Greed

📉 The Number That Matters

$79

Brent crude jumped about 6% toward $79 a barrel after Trump called the Iran ceasefire over, unwinding a month of calm that had pulled oil back toward its pre-war level.

⚔️ Winners vs Losers

Winners

MAAS 0.00%↑: Maase Inc. extended its powerful multi-month rally as the thinly traded, heavily insider-owned Chinese AI name kept drawing momentum buyers behind its pivot to full-stack AI computing.

BABA 0.00%↑: Alibaba Group Holding Ltd. jumped after its Hong Kong shares posted their biggest gain since September, as investors rotated into beaten-down Chinese internet names and turned optimistic ahead of the company’s upcoming earnings.

Losers

FCEL 0.00%↑: FuelCell Energy Inc. tumbled after announcing a $200 million public stock offering to fund manufacturing expansion, a dilutive raise that landed on top of profit-taking from its recent data-center-driven run.

SNDK 0.00%↑: Sandisk Corporation slid as the memory and storage complex extended its selloff, with profit-taking accelerating after disappointing Samsung earnings rattled a group that has posted enormous gains in 2026.

WDC 0.00%↑: Western Digital Corporation fell alongside the broader memory pullback as traders trimmed exposure to the year’s most extended semiconductor winners.

GLW 0.00%↑: Corning Incorporated dropped as weakness spread across AI-infrastructure and optical names caught in the broader electronic-technology pullback.

HOOD 0.00%↑: Robinhood Markets Inc. pulled back as high-beta fintech names gave back gains, unwinding part of the rally that followed the company’s early-July blockchain and tokenized-stock launch.

MRVL 0.00%↑: Marvell Technology Inc. fell as the semiconductor sell-off intensified, with the custom-silicon maker swept up in the same profit-taking hitting AI chip names.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $62,074 (▼ -1.95%)

Ethereum (ETH): $1,737 (▼ -1.87%)

XRP: $1.08 (▼ -2.68%)

Equity Indices (Futures):

S&P 500: 7,485 (▼ -0.88%)

NASDAQ 100: 28,996 (▼ -1.35%)

FTSE 100: 10,506 (▼ -1.36%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.57% (▲ 0.44%)

Oil (WTI): $74 (▲ 2.77%)

Gold: $4,051 (▼ -1.21%)

Silver: $58.43 (▼ -2.41%)

Data as of: UK: 12:15 BST / US: 07:15 EDT / Asia (Tokyo): 20:15 JST

✅ 5 Things to Know

⚔️ Trump Says the Iran Ceasefire Is “Over,” Oil Surges

The interim peace between the US and Iran cracked this morning when President Trump said the three-week-old ceasefire is “over” and “a waste of time,” speaking beside NATO’s chief at a summit in Ankara. His words followed an overnight US barrage on more than 80 sites in Iran, hitting air defences, command centres and coastal radar, in retaliation for the tanker attacks in the Strait of Hormuz, and the revoking of a waiver that had let Iran sell its oil. Iran’s Foreign Ministry called the deal “ineffective,” and its Revolutionary Guard said it struck bases in Kuwait and Bahrain. Oil surged, with Brent up about 6% toward $79 a barrel (Bloomberg).

Markets read it as a supply and inflation shock rather than a simple flight to safety. Brent had settled 3% higher at $74.16 yesterday and pushed on again today, and the strait that carries about a fifth of the world’s crude is back in question a week before US inflation data. The reaction was revealing: US stock futures pointed sharply lower, the S&P by 1% and the Nasdaq 100 by 1.4%, yet gold fell about 1.3% toward $4,050 and Treasury yields rose to a four-week high, the opposite of the usual haven trade. Trump left the door open for talks to continue. Watch whether tankers keep moving through Hormuz and how Iran answers (Barron’s).

Sensei’s Insight: Look at what sold off together: stocks, crypto and even gold, while oil and yields rose. That mix says the market fears an inflation and rates shock, not a growth scare. Barrels still flow through Hormuz; a real blockade would be the bigger break.

💻 DeepSeek’s Own Chip Deepens a Global Chip Rout

The other force pulling markets down began yesterday, when Reuters reported that Chinese AI startup DeepSeek is designing its own chip to cut its reliance on Nvidia and Huawei, a year-long effort aimed at inference, the stage where a trained model answers a query. The report hit the whole AI complex: the VanEck Semiconductor ETF fell more than 3%, Micron dropped about 4.7% and Western Digital about 6.3%, and the Nasdaq Composite closed down 1.16% at 25,818.69. The selling spread overnight, with Samsung and SK Hynix dragging South Korea’s Kospi into a bear market, down more than 20% from its recent peak (Yahoo Finance).

The move is as much rotation as retreat. As investors sold the priciest semiconductor names, money flowed toward cheaper AI plays, and Alibaba jumped about 12% in Hong Kong on hopes China’s own champions gain from a home-grown chip. This is the second DeepSeek shock in eighteen months, after its low-cost model wiped a record sum off Nvidia in early 2025, and each time the memory names took the brunt because their pricing leans on AI-server demand staying scarce. The first hard test of that demand comes with Q2 chip guidance from 9 July (Bloomberg).

Sensei’s Insight: Every DeepSeek headline sounds like the end of the AI trade, and both times it has really been a rotation, not a collapse. The money left the priciest chip names and moved elsewhere, it did not leave the theme. The 9 July guidance settles who is right.

🏛️ Warsh’s First Fed Minutes Land Today

The minutes of the Fed’s June meeting publish at 7pm BST, and they carry unusual weight because Chair Kevin Warsh withheld his own rate projection, leaving the record of the committee’s debate as the only detailed guide to how close a 2026 hike really is. At that meeting the Fed held its benchmark at 3.50% to 3.75% but shifted its projections toward a hike, with nine of nineteen officials pencilling in at least one increase this year and the committee’s 2026 inflation forecast revised sharply higher. Warsh’s statement ran about 130 words and dropped the easing bias that had survived three prior meetings (CNBC).

The timing is awkward, and today’s events sharpen it. The minutes predate the soft June payrolls report of 57,000, so they may read more hawkish than the committee now feels, yet the oil shock from the Iran escalation pushes inflation risk the other way, and Treasury yields have already climbed to a four-week high. Markets will hunt for how many of the hawkish votes belong to voting members, and whether officials tied their inflation worry to energy or to prices broadening. A firm signal that a hike is live would land straight into a jittery tape. Watch the 2-year yield (Barron’s).

Sensei’s Insight: These minutes were written before the jobs miss, so they show where the Fed’s head was, not where its hand is now. They set the hawkish ceiling; today’s oil jump and the 14 July inflation print decide how much of it survives to the decision.

🚀 SpaceX Slides Toward Its IPO Price

SpaceX joined the Nasdaq-100 before the open, and instead of the pop that index inclusion often brings, the stock slid toward the price at which it floated last month. The drag was a legal fight over the gas turbines powering its Colossus 2 data centre in Memphis, which a civil-rights group says are running without the air permits the Clean Air Act requires. That plant underpins a compute contract worth about $45 billion over three years, under which Anthropic pays roughly $1.25 billion a month to rent capacity, so a forced shutdown would strike at real revenue rather than a projection (CNBC).

The turbines matter because power, not chips, is now the choke point for AI, and SpaceX built its own gas generation to get Colossus running fast; that same speed is what the permit case targets. For a company that raised the largest sum in IPO history last month and was fast-tracked into the index after fifteen trading days, the debut is a reminder that the compute boom rests on physical plant a regulator can switch off. Watch the court date and any move by Anthropic to line up backup capacity (Forbes).

Sensei’s Insight: Index inclusion is meant to be a tailwind, and it still got sold. The real lesson is where AI’s risk now sits, not in the model or the chip, but in whether a data centre can keep its power on. Permits are the new bottleneck.

₿ Bitcoin Slides Toward $62,000 as Iran Fears Bite

Bitcoin fell about 2.6% to around $62,000, touching an intraday low near $61,836, as Trump’s ceasefire remarks and the US-Iran strikes drove investors out of risk. Ether dropped about 2.5% to near $1,738. The slide gives back much of the bounce that had carried Bitcoin back toward $64,000 on the soft jobs report, and it leaves the coin well below the $65,000 to $66,000 zone it needed to reclaim to signal the recovery was real. Spot Bitcoin ETFs remain a drag, with net outflows over the past month even after a handful of positive sessions (Barron’s).

The drop is a reminder that Bitcoin still trades like a risk asset, not the haven its backers describe: it fell today alongside equities, and even gold slid. Now it meets a second hurdle in today’s Fed minutes, where a hawkish read that lifts yields and the dollar would add pressure. A calmer Middle East headline or a softer minutes tone could steady it, while a clean break below the overnight low would put the June trough under $58,000 back in view. Watch the ETF prints and whether $62,000 holds.

Sensei’s Insight: The haven story failed its test again today: when the shock hit, Bitcoin sold off with stocks while gold fell too. Below $62,000 the June low near $58,000 is back in play. The ETF flows, not the price, show whether real money is buying.

Stories You Might Have Missed

💊 Vertex to Buy Crinetics for About $10 Billion

Vertex Pharmaceuticals agreed to buy Crinetics Pharmaceuticals for $85 a share in cash, valuing the biotech at about $10 billion and sending Crinetics shares up nearly double in extended trade. The deal, expected to close in the third quarter, hands Vertex a late-stage drug for a hormonal disorder and a pipeline in endocrine disease, a push to widen beyond the cystic-fibrosis franchise that has long carried its revenue. Large biotech takeovers at rich premiums have been scarce this year, so a $10 billion cash bid is a signal that cash-rich drugmakers are willing to pay up for growth again, and it tends to lift smaller drug names on hopes they are next (CNBC).

🎮 Microsoft’s Xbox Cuts 3,200 Jobs in a Major Overhaul

Microsoft is cutting about 3,200 jobs at its Xbox division and selling five game studios, in what its gaming chief Asha Sharma called the biggest restructuring in Xbox history. Around 1,600 of the cuts take effect at once, with studios including Ninja Theory, Double Fine and Compulsion set to be divested and France’s Arkane to follow. The blunt rationale, that the unit runs at margins several times lower than rival platform and publishing businesses, matters beyond gaming: even after the $69 billion Activision Blizzard deal, Microsoft is willing to shrink a consumer arm to protect profitability as it pours money into AI (Bloomberg).

🥤 PepsiCo Opens Earnings Season Tomorrow

PepsiCo reports before the open tomorrow, the unofficial start of the Q2 season, with analysts looking for earnings near $2.19 a share on revenue of about $23.9 billion, roughly 5% higher than a year ago. The read that matters is volume: Frito-Lay North America grew about 2% in the first quarter, and a second quarter of improvement would suggest shoppers are absorbing past price rises rather than trading down. The stock has lagged, up about 8% over the year against the S&P’s 22%, so the bar is low. Delta follows on Friday, and the big banks report from 14 July (Yahoo Finance).

🔍 Deep Dive

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.