Sensei’s Morning Forecast: XRP ETF Without SEC Approval? 14 Days to Go — While Apple and Amazon Shatter Big Tech Expectations.

XRP ETF countdown, Apple battles China headwinds, Amazon’s AI-driven AWS surges, Coinbase’s crypto rebound accelerates, Saylor raises Bitcoin yield, and regulators rethink global stablecoin rules.

👀 Today’s Stories at a Glance

🍏 Apple narrowly beat revenue forecasts, but China’s flat sales and delayed AI rollout cloud holiday optimism.

🛒 Amazon smashed Q3 expectations as AWS growth reaccelerated, pushing stock up 11% after strong guidance.

📊 Coinbase’s Q3 profit jumped 6x as institutional trading soared 122% and Bitcoin holdings grew aggressively.

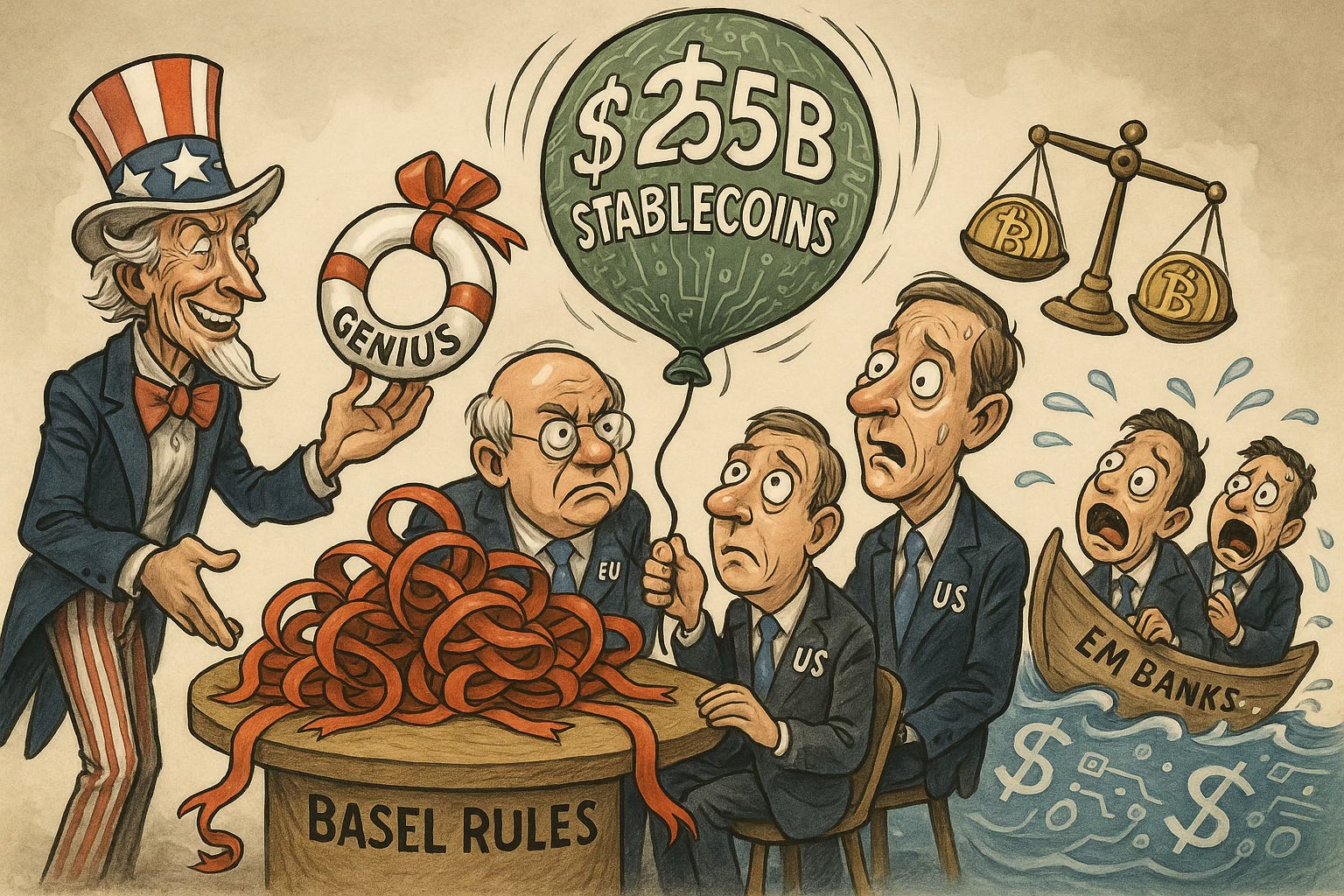

🌐 Global regulators are reassessing stablecoin capital rules as market size doubles and policy gaps widen.

🚀 MicroStrategy raised its preferred stock yield, reinforcing Saylor’s bold bet on Bitcoin’s maturing trajectory.

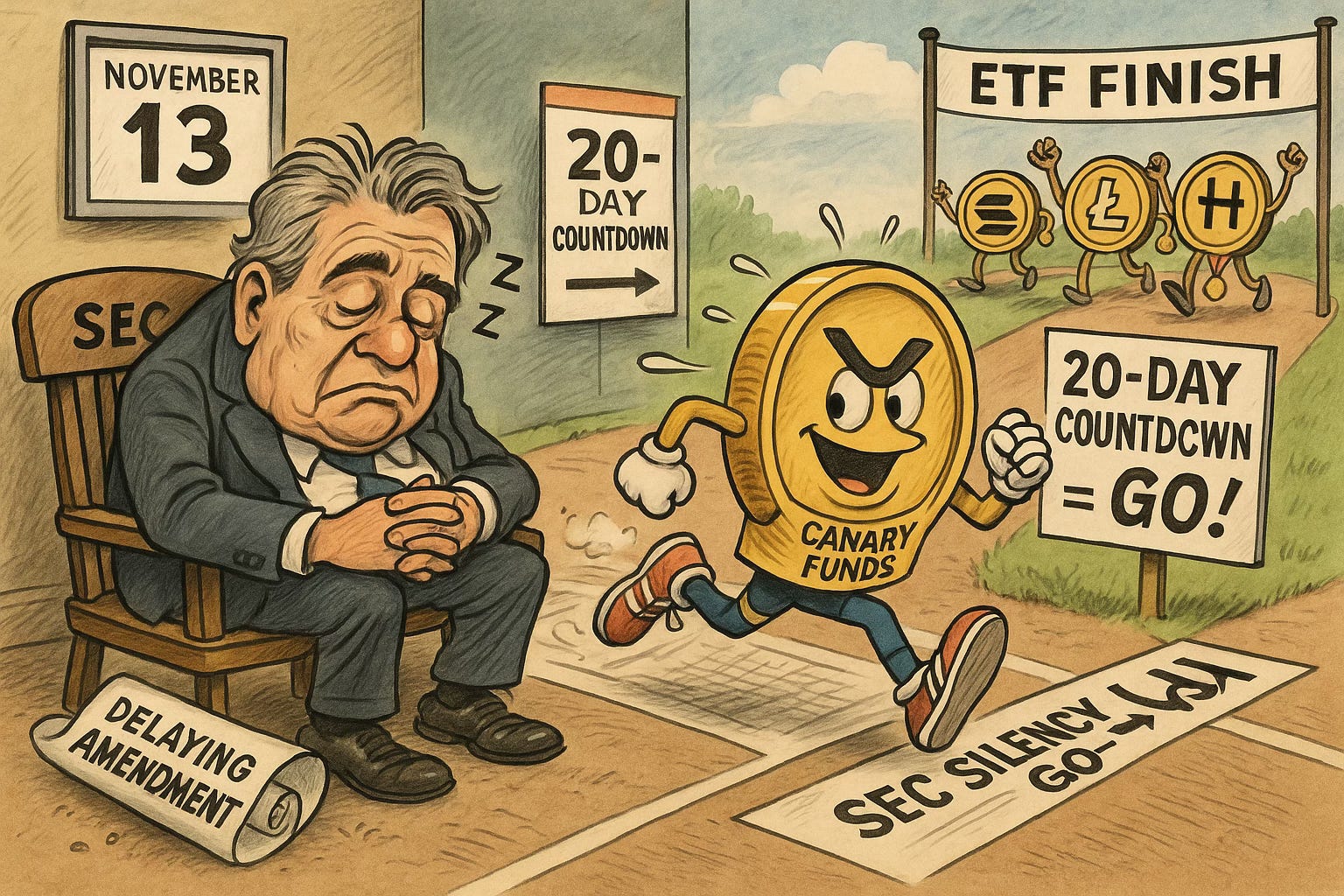

🔍Canary’s XRP ETF may launch by November 13 via SEC silence, testing legal boundaries for spot crypto funds.

🧠 One Big Thing

From Big Tech to crypto to Bitcoin-bet enterprises, yesterday’s earnings painted a powerful yet fragmented picture. Apple hit a revenue record but flagged weakness in China; Amazon reignited AWS growth to 2022 levels; and Coinbase saw institutional trading surge 122%. Meanwhile, MicroStrategy tightened its capital machine as Bitcoin holdings soared past 640,000 BTC. The common thread? Growth is back—but the paths to it are diverging sharply across sectors.

💰 Money Move of the Day

Big earnings beats can spark rallies—but chasing them isn’t always wise. Consider sector ETFs to ride broader themes like cloud growth or crypto adoption. It’s a way to gain exposure without betting on just one name.

📊 Market Snapshot

Cryptocurrencies:

Bitcoin (BTC): $110,000.22 (▼ -0.04%)

Ethereum (ETH): $3,881.38 (▼ -0.58%)

XRP: $2.55 (▲ +0.06%)

Equity Indices (Futures):

S&P 500: 6,888.1 (▲ +0.03%)

NASDAQ 100: 26,232.00 (▼ -0.12%)

FTSE 100: 9,712.95 (▼ -0.45%)

Commodities & Bonds:

10-Year US Treasury Yield: 4.080% (▲ +0.05%)

Oil (WTI): $60.364 (▼ -0.46%)

Gold: $3,978.788 (▲ +1.27%)

Silver: $48.003 (▲ +1.04%)

🕒 Data as of UK (BST): 11:12 / US (EST): 07:12 / Asia (Tokyo): 20:12

✅ 5 Things to Know Today

🍏 Apple Beats on Revenue But China Weakness Casts Shadow Over iPhone 16 Cycle

Apple posted a September quarter revenue record of $94.9 billion, narrowly beating Wall Street’s $94.46 billion consensus and marking a 6% year-over-year gain. Adjusted EPS hit $1.64, exceeding expectations after removing a $10.2 billion one-time tax charge tied to a lost EU case. Net income excluding the charge would have grown 12% to roughly $25 billion. iPhone revenue grew 5.5% to $46.22 billion, reversing two straight quarters of declines. The Services segment surged 12% to an all-time high of $25 billion, signaling continued strength in monetizing Apple’s user base. Gross margin reached 46.2%, while operating cash flow came in at $27 billion. The company also declared a quarterly dividend of $0.25 per share, payable November 14.

China remains a weak spot, with sales staying flat year-over-year. CEO Tim Cook cited FX tailwinds and emphasized Apple retained the top two smartphone spots in urban China. The quarter included only nine days of iPhone 16 sales, which began on September 20, making full-cycle performance unclear. Management noted that Apple Intelligence adoption accelerated, doubling the iOS 18.1 upgrade rate versus iOS 17.1, though most features rolled out post-quarter. With the December quarter traditionally Apple’s strongest, all eyes now turn to how well iPhone 16 and Apple Intelligence resonate during the holidays.

Sensei’s Insight: Apple’s ability to expand margins while iPhone growth slows validates the Services strategy, but the China headwind and delayed Apple Intelligence rollout create execution risk heading into what should be a blockbuster holiday quarter for iPhone 16.

🛒 Amazon Crushes Q3 Expectations: AWS Reignites Growth at 2022 Pace

Amazon delivered a decisive earnings beat on October 30, reporting Q3 net sales of $180.2 billion—up 13% year-over-year and surpassing analyst consensus of $177.91 billion. The headline number that truly grabbed attention was adjusted earnings per share of $1.95, crushing estimates of $1.57 by roughly 24%. The e-commerce and cloud powerhouse demonstrated broad-based strength: North America revenue climbed 11% to $106.3 billion, international sales advanced 14% to $40.9 billion, and advertising services expanded 24% to $17.7 billion. CEO Andy Jassy emphasized that “AWS is expanding at a rate we haven’t witnessed since 2022,” marking a significant acceleration in what has become Amazon’s crown jewel amid intensifying cloud competition (BusinessWire).

What made this report particularly compelling for growth investors was AWS’s 20% revenue growth to $33 billion—handily beating the expected 18.1% growth rate. Operating income hit $17.4 billion, though this figure was depressed by a $2.5 billion FTC legal settlement and $1.8 billion in severance costs; adjusting for these charges yields operating income of $21.7 billion. The quarter showcased Amazon’s pivot toward high-margin businesses, with Jassy pointing to AI-driven improvements across operations fueling the company’s momentum. For Q4, Amazon guided to revenue between $206 billion and $213 billion with operating income guidance of $21–26 billion—both substantially ahead of Wall Street consensus. The market’s reaction was unambiguous: Amazon’s stock surged over 11% in after-hours trading (Yahoo Finance, Investors).

Sensei’s Insight: This earnings beat reframes the AI capex debate—Amazon’s heavy infrastructure spending is delivering measurable returns, with AWS growth returning to 2022 momentum levels. For growth-focused investors, the question shifts from “is Amazon spending too much on AI?” to “can AWS maintain this acceleration?” Watch Q4 guidance execution closely; any stumble could quickly reverse today’s enthusiasm

📊 Coinbase Q3 Crushes Expectations: Institutional Trading Surges 122%, Bitcoin Holdings Hit 14,548 BTC

Coinbase delivered a standout third quarter on October 30, reporting net income of $432.6 million—up nearly 6x from $75.5 million in Q3 2024—with diluted EPS of $1.50, smashing consensus estimates of $1.10. Revenue climbed 55% year-over-year to $1.87 billion, topping FactSet projections of $1.8 billion, as transaction revenue jumped 37% quarter-over-quarter to $1 billion. Trading volumes rebounded sharply: institutional volumes hit $236 billion (up 22% QoQ), while retail volumes rose to $59 billion (up 37% QoQ). Institutional transaction revenue surged 122% to $135 million, driven by the launch of a premium trading tier and integration with Deribit’s options and futures platform, which added $52 million in revenue (CNBC, Futunn, Crypto News).

The company continued strengthening its balance sheet, acquiring 2,772 BTC during Q3 via weekly DCA purchases totaling $299 million, bringing its total Bitcoin holdings to 14,548 BTC (Yahoo Finance). Subscription and services revenue rose 14% to $747 million, now accounting for 28% of total revenue, backed by record stablecoin activity—USDC market cap and average balances hit all-time highs of $74 billion and $15 billion respectively. CEO Brian Armstrong reaffirmed Coinbase’s pivot toward the “Everything Exchange” strategy, expanding beyond spot into derivatives, tokenized stocks, and prediction markets. The Deribit acquisition notably reinforced its institutional derivatives segment, a key growth lever amid ongoing volatility (Futunn, Crypto News).

Sensei’s Insight: Coinbase’s rebound from Q2’s disappointment signals renewed institutional confidence in crypto markets, but the 122% surge in institutional trading revenue and aggressive Bitcoin accumulation suggest management is betting heavily on sustained volatility and broader crypto adoption. Watch for margin compression as competition intensifies in derivatives; the company’s profitability depends significantly on maintaining this elevated institutional activity.

🌐 Global Regulators Rethink Stablecoin Rules as Market Surges Beyond Expectations

Global financial regulators are revisiting the Basel Committee’s prudential standards for banks’ crypto exposure ahead of the January 1, 2026 implementation deadline, as the stablecoin market ballooned from $125 billion in 2023 to $255 billion in mid-2025. Originally introduced in late 2022, the Basel rules were seen as a deterrent, imposing punitive capital requirements that stifled bank participation. But the GENIUS Act, passed by Congress in July 2025, introduced a new federal regime mandating one-to-one reserve backing and monthly composition disclosures. This regulatory clarity, combined with institutional demand and growing White House support, has pushed crypto into the financial mainstream, with the Basel Committee now exploring reforms to reflect the asset class’s evolving risk profile.

Current Basel standards apply a 1250% risk weight to many crypto assets, but a July 2024 update introduced “Group 1b” treatment for qualifying stablecoins—those issued by regulated entities with robust stabilization mechanisms. However, global inconsistencies remain a concern. The European Systemic Risk Board warned in October 2025 about redemption risks from stablecoins issued by third-country entities lacking harmonized safeguards. Meanwhile, Standard Charteredprojected a $1 trillion drain from emerging market banks as savers pivot to dollar-backed digital currencies amid inflation and currency volatility. The recalibration efforts suggest a broader regulatory acceptance, but also expose new vulnerabilities in a fragmented policy landscape.

Sensei’s Insight: The recalibration signals regulatory acceptance of crypto’s institutional role, but fragmented global frameworks risk creating arbitrage opportunities and financial stability gaps—watch implementation timelines and jurisdictional coordination closely.

🚀 Saylor Raises Preferred Yield as MicroStrategy Claims Bitcoin ‘Inflection Point’

Michael Saylor is tightening the screws on his Bitcoin accumulation machine. After reporting blockbuster Q3 earnings—net income of $2.8 billion with diluted EPS of $8.42, crushing analyst expectations of $8.15—Saylor announced he’s raising the dividend rate on MicroStrategy’s Variable Rate Series A Perpetual Preferred Stock from 10.00% to 10.25% (Bloomberg Law). The yield boost reflects Saylor’s strategic move to keep investor appetite for these preferred shares flush. As the company’s primary funding mechanism for Bitcoin purchases, maintaining demand for the preferred stock is critical to his ongoing accumulation plan. MicroStrategy now holds 640,808 BTC valued at roughly $70 billion—acquired for $47.44 billion at an average price of $74,032 per coin. Year-to-date, the company has generated a 26% Bitcoin yield, pocketing $12.9 billion in unrealized gains. Q3 revenues climbed 10.9% YoY to $128.7 million, while subscription services revenue surged 65.4% YoY to $46 million, signaling recovery in the software business beneath the Bitcoin treasury narrative (Business Wire).

Saylor framed the dividend increase as a response to what he calls a structural “inflection point” in the Bitcoin market. “We are at what we consider a turning point; our ratio of net asset value has been declining over time as the Bitcoin asset class evolves and volatility diminishes,” he said during Thursday’s earnings call (Bloomberg Law). The comment underscores a tactical reality: as Bitcoin becomes more institutionalized and price swings compress, the variance between MicroStrategy’s stock price and its net asset value (primarily its BTC holdings) narrows—meaning preferred share valuations require support. Looking ahead, Saylor is projecting FY2025 operating income of $34 billion and net income of $24 billion, or $80 per share, crystallizing MicroStrategy’s transformation from enterprise software provider into a de facto Bitcoin ETF (Bitcoin Magazine). Notably, Saylor also ruled out M&A activity with other Bitcoin treasury firms, reaffirming a disciplined, capital-efficient growth model focused on organic Bitcoin accumulation rather than consolidation plays.

Sensei’s Insight: Watch the preferred share mechanics closely—yield adjustments signal Saylor’s confidence in Bitcoin’s near-term trajectory but also reveal tension between funding costs and asset appreciation. The “inflection point” language hints at structural shifts in crypto market maturity that could reshape corporate Bitcoin strategies long-term

🔗 Connect with Us

Stay plugged in across platforms:

Sensei on X: sensei_crypto_

Martyn Lucas on X: MartynInvestor

Vaz on X: eVTOLHUB

💎 Premium Discord Access: Join the Discord

📺 YouTube Channel (Live & Replays): Martyn Lucas Investor

👕 Limited Merch: Shop Here

🔍Deep Dive: XRP Spot ETF Countdown — 14 Days to a Potential Breakthrough

Keep reading with a 7-day free trial

Subscribe to Sensei.news to keep reading this post and get 7 days of free access to the full post archives.